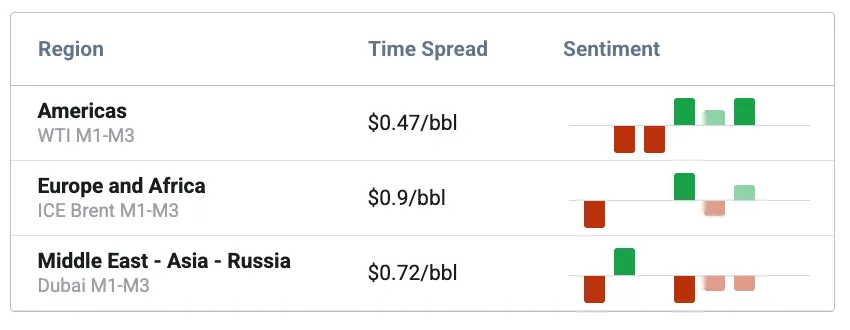

Crude diffs buoyed by Russia sanctions deadline and Venezuela upgrader disruption

Market Calls

Executive Summary

Market & Trading calls

Americas:

- Expect Venezuelan crude supply to hit multi-year lows in November as ~500kbd of upgrading capacity remains shut.

- US-Venezuelan tensions create a potential upside supply scenario if the Maduro regime or its successor strike a deal where the US invests into its oil industry, paving the way for higher availability of heavy sour barrels in the Americas.

- Optimistic regarding a continued tightening of US crude stocks in the weeks ahead as imports remain low and robust product cracks as well as declining refinery maintenance pave the way for tighter US crude markets.

Europe and Africa

- Bearish on Russian oil prices as floating storage rises. Post-sanctions uncertainty around Urals sellers point to near-term downside risk.

- Neutral-to-bearish Angola diffs: US sanctions on Rizhao terminal weigh on Angolan demand despite lower Jan loadings.

- Bullish Libyan light sweet grades: Open Asia arbitrage and strong European refining margins suggest support will persist through year-end.

Middle East and Asia

- Decline expected for Russian crude exports to India and China in the next 1-2 months as these countries scale down buying following the November 21 deadline.

- Increase expected for crude exports out of Kuwait in November/December due to continued operational issues at Al zour, prompting us to revise refinery runs lower.

- Stable on pressured Iranian crude flows into China for the rest of the year amid low import quotas in Shandong, however rebound expected for early 2026.

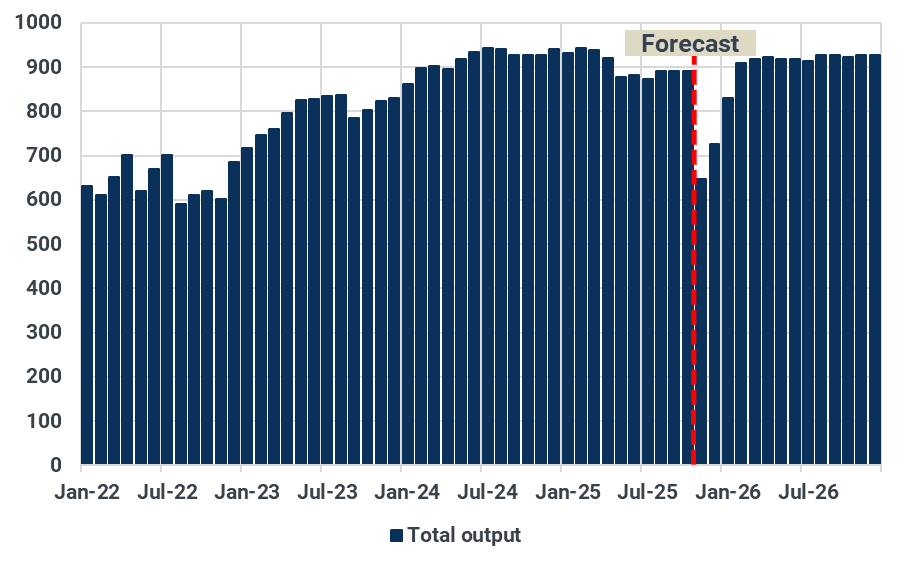

Americas: 500kbd of Venezuelan upgrading capacity remains shut

500kbd of Venezuelan upgrading capacity remains shut

The operational crisis at Venezuela's José industrial complex escalated this week, following a fire at the Petrocedeno upgrader's distillation unit (~200kbd capacity). This outage compounds the closures of the Petromonagas and Petrororaima units (~300kbd combined capacity) earlier in the month, leaving only the Petropiar unit (~200kbd capacity) operational.

The cascade of failures severely compromises Venezuela's critical heavy crude processing capability, limiting operations, which will result in a month-on-month decline of ~250 kbd in domestic crude supply to 650kbd in November, a multi-year low (see chart). The decline is corroborated by lower flows, which have averaged <600 kbd so far this month.

These outages will provide near-term support to Merey crude differentials, which came under pressure more recently amid higher availability and a rise in floating storage in Asia (amid weaker Chinese buying), with the grade averaging a discount of ~$12/bbl versus ICE Brent in mid-November (Argus Media).

Venezuelan crude and condensate supply, kbd

Source: Kpler

US-Venezuelan tensions create a supply upside scenario

The US continues to escalate tensions with Venezuela, building a larger naval presence in the Caribbean (Operation Southern Spear) and carrying out boat strikes on alleged drug trafficking routes. The US administration’s assertive posture—including President Trump considering attacks on Venezuelan soil—has faced strong criticism from G7 allies and the EU, who cite disregard for international law, but US officials maintain a focus on removing "narco-terrorists" from the hemisphere.

The current pressure, however, highlights the possibility of unlocking a larger medium-term supply increase from Venezuela’s massive oil reserves should the Maduro regime be replaced or if the US strikes a deal with Venezuela. The Maduro regime has reportedly already offered a substantial deal to the Trump administration, proposing to open all existing and future oil projects to American companies, grant preferential contracts, and reverse the flow of Venezuelan oil exports from China to the US. Such a scenario would free up significant volumes of heavy sour crude in the Americas, weighing on prices of regional competitors, such as Colombia's Castilla or Canada's WCS Hardisty.

The US has imported 130-150kbd of Venezuelan crude over the last three months, down from a peak of 300kbd seen in December 2024 (see chart). Amid the heightened risk, Chevron remains uniquely exposed as the sole major US oil company operating in the country. Nevertheless, Chevron's CEO emphasizes playing a "long game," committed to remaining and aiding the country's economic rebuilding "when circumstances change", corroborating a potential scenario where the oil major could invest further into new developments in Venezuela in the future.

US crude imports from Venezuela by buyer, kbd

Source: Kpler

US crude stocks drop as markets tighten

US crude stocks declined counter-seasonally last week amid a sharp drop in imports and a tightening crude market, with US imports averaging 1.8-1.9Mbd, representing a decline of around 500kbd month-on-month. Whilst our predictive flows feature implies a rebound to 2.2-2.3Mbd by the end of the month, it represents the very bottom of the multi-year range, indicating that imports will likely remain structurally tight.

The decline in crude arrivals is coming at a time when US crude demand is rising, with primary distillation offline capacity expected to average a mere 500kbd this month, down almost 1 Mbd compared to October (IIR). Whilst crude availability remains high, with US crude supply expected to hit its peak this month, the rise in demand, coupled with lower imports, is keeping regional balances tighter. This is particularly true when we consider that middle distillate cracks are hovering near multi-year highs.

The latter, coupled with an expected decline in primary distillation offline capacity in December (no significant outages reported; IIR), will keep regional markets tighter and utilization rates high, thereby keeping a lid on US crude stocks in the weeks ahead.

US crude stocks, Mbbls

Source: Kpler

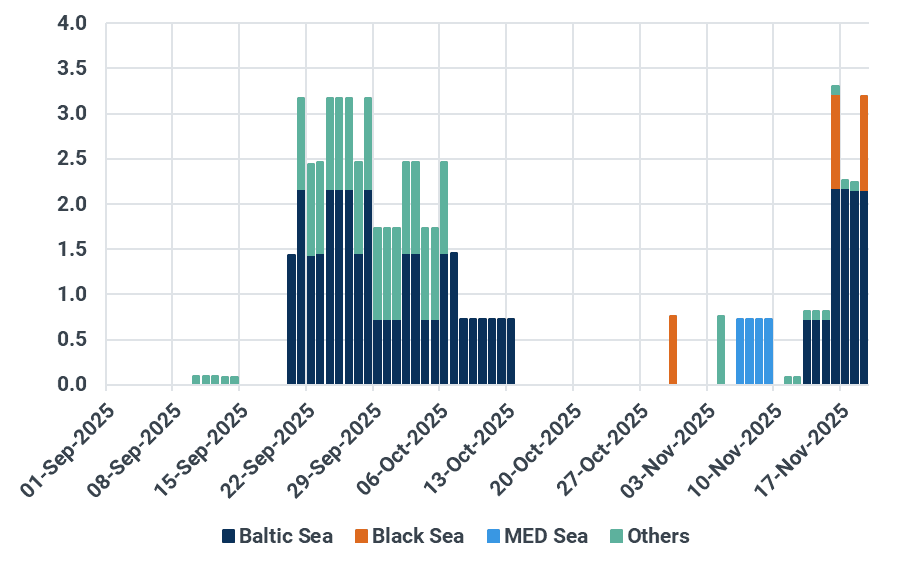

Atlantic Basin: Russian floating storage in Europe hits new highs

Russian oil in West of Suez floating storage hits 1-year high

Russian crude in floating storage west of Suez surged to over 3Mbbls, up by 2Mbbls w/w, with three Urals cargoes idle in the Baltic and one in the Black Sea, the highest in over a year. It is indicative of Russia’s upcoming troubles when it comes to finding a home for part of its crude. Three shipments are currently headed to Turkey, Russia’s sole buyer of crude in the West of Suez, and will arrive after the 21 November deadline. Two of them are being sold by Tatneft and the third one by Rusvietpetro.

With Russian FOB Urals trading at a >$22/bbl discount to NSD (Argus Media), and Turkish gasoil exports declining, refiners may selectively absorb Rosneft or Lukoil barrels. However, just like Indian and Chinese refiners, both Tupras and SOCAR will stay on the cautious side in the short-term and look for cargoes that are supplied by non-sanctioned Russian companies. New sellers have entered the game, meaning that Russian flows to Turkey will decrease over the coming weeks, but are likely to normalise closer in early 2026.

Russian oil in floating storage in the West of Suez by current seas, Mbbls

Source: Kpler

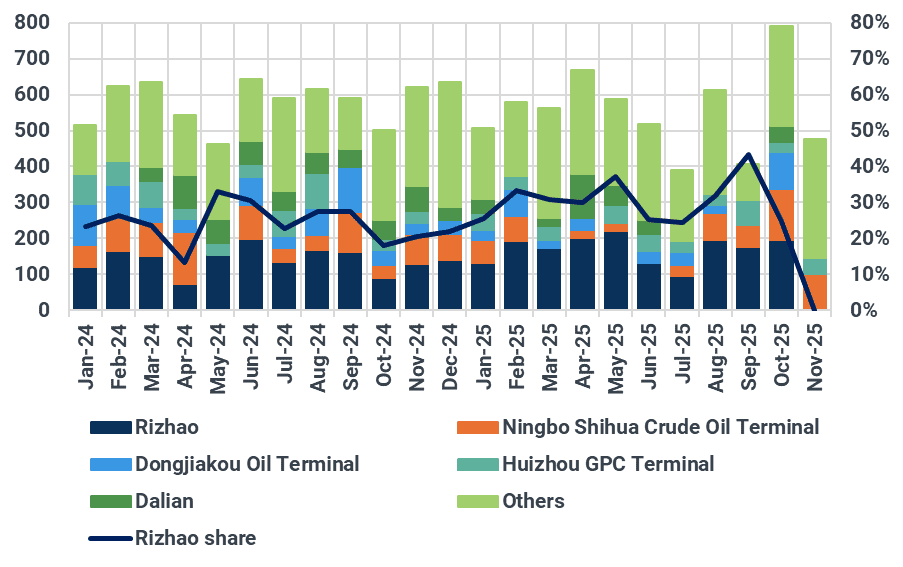

WAF diffs rise but Angola lags on sanctions fallout

The WAF basket gained $0.35/bbl w/w to over $1/bbl vs NSD (Argus Media), supported by strong European cracks. Lower availability of cargoes have also acted as support. Exports from West Africa have been 195 kbd lower m/m in November thus far, averaging 3.32Mbd, with the main decrease coming from Nigeria. Lower refining maintenance amid decreasing offline capacity in Europe until February 2026 is likely to support demand for WAF crude in the short-term, although such support will be limited by the start of heavy maintenance in spring which will start in March.

Yet Angolan grades underperformed. Light sweet Nemba fell $0.30/bbl, and sour grades were flat, while sour grades Dalia, Hungo and Kissanje were flat w/w. US sanctions on the Rizhao Shihua terminal started impacting Angolan grades’ diffs to the downside compared to other WAF grades as the terminal is a large importer of Angolan crude.

In the short-term, lower availability will act as support as Angola’s January loadings are set at 933kbd, down from 1.06Mbd in December. Earlier in the week, ExxonMobil took FID on Block 15 in Angola's deepwater, aiming to fight decline at the Mondo and Saxi-Batuque fields. Block 15 produces around 180 kbd while total Angolan production averaged 1.07Mbd according to ANPG.

China oil imports from Angola by port, kbd

Source: Kpler

Libyan oil exports to Asia reach a 13-month high; Azerbaijan oil exports on track to hit a new month low

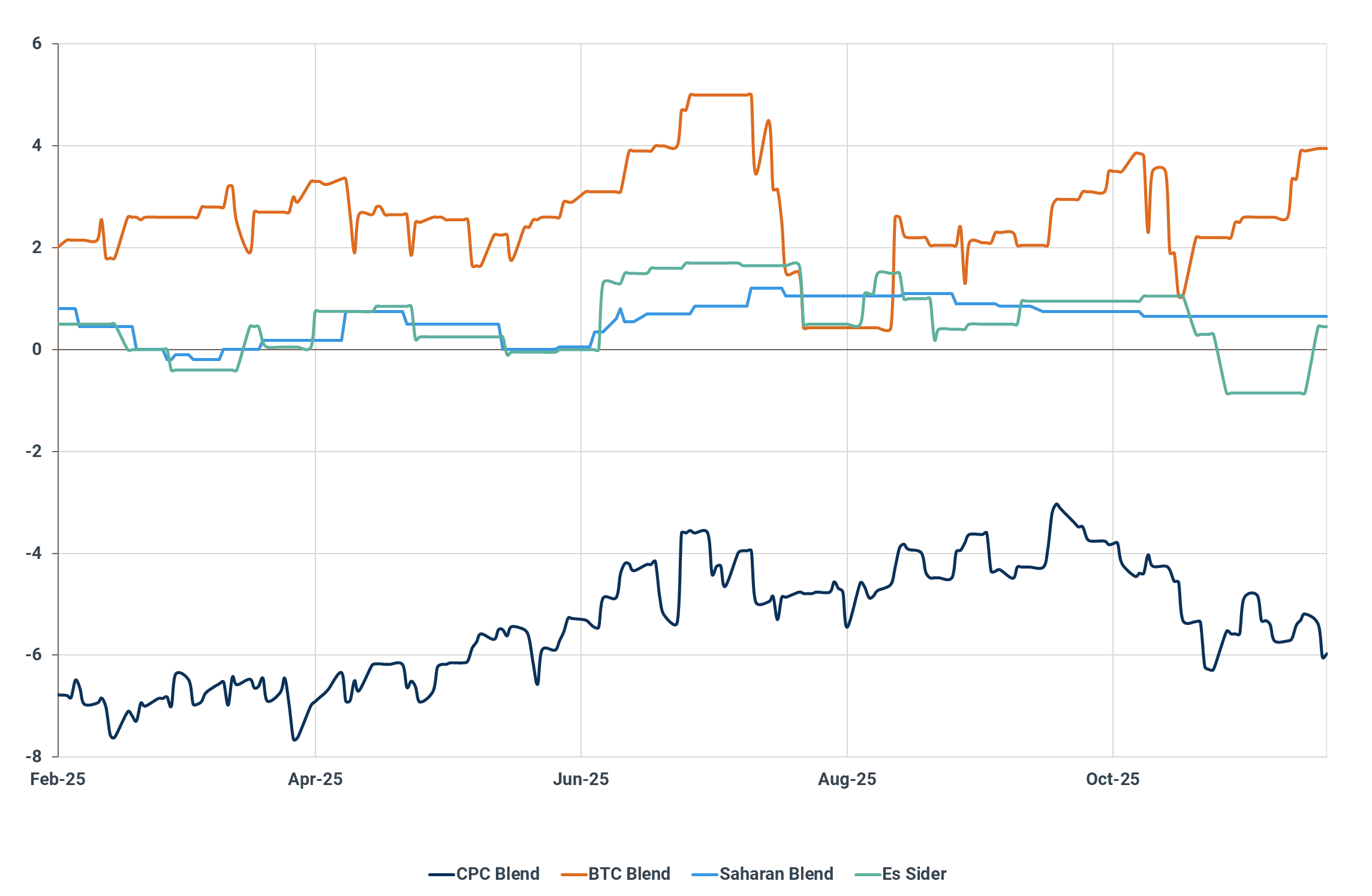

The wide-open arbitrage between the Atlantic Basin and Asia is attracting an increasing number of Libyan cargoes to the East of Suez. Libya’s oil exports to Asia are jumping for the fourth month in a row, currently averaging 185kbd although our predictive function shows the average could rise to 190kbd for the month of November. Total country exports are holding above 1.2Mbd, rebounding by 105kbd m/m as shipments of Es Sider fell last month. Strong refining margins in Europe and low Murban availability in Asia are providing support to Es Sider’s differentials. Diffs for the middle-distillate rich crude jumped by $1.30/bbl w/w to trade at a premium to NSD.

Elsewhere in the MED, BTC diffs were also supported by strong product cracks. The grade’s diff jumped by $0.60/bbl to nearly $4/bbl above NSD, its highest differential since early July. Diffs have also been supported by lower exports as Azerbaijan’s oil exports are on track to hit a new monthly low since at least 2013, how far Kpler data goes back. Since September, exports averaged 443kbd, down by 86kbd y/y.

MED light sweet diffs against NSD, $/bbl

Source: Argus Media

Middle East-Asia-Russia: Despite near-term declines, a complete halt to Russian imports into India and China unlikely

US sanctions on Rosneft and Lukoil to reduce buying of Russian barrels in the short term

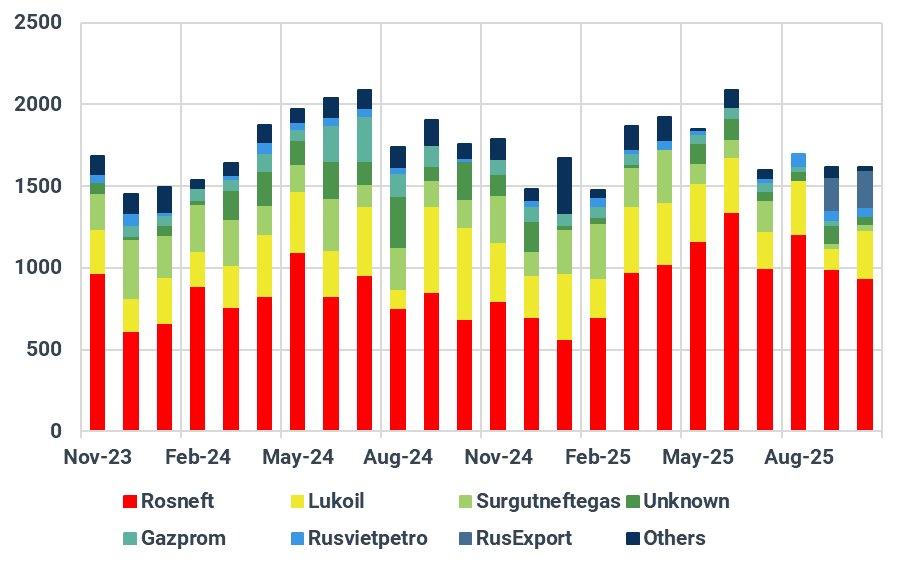

Following the US Treasury’s 23 October announcement of sanctions on Rosneft and Lukoil, the 21 November wind-down deadline for companies is now approaching. With India being the largest buyer of Russian oil, the key question is how this will affect India’s purchasing behaviour. We expect India’s imports of Russian crude to temporarily—but meaningfully—decline after 21 November, giving time for supply chains to reorganise. India has already been working to diversify its crude slate, and this process should accelerate, with higher purchases from the Middle East, the US, Latin America, and West Africa. In October and so far in November, Indian imports of Russian crude have averaged 1.6Mbd and 1.89Mbd, respectively—with this month’s hike reflecting refiners’ efforts to secure economical barrels ahead of the sanctions cutoff. These volumes could decline sharply in December and January. However, the broader market impact is likely to remain limited over the longer term. Unless more expansive secondary sanctions are introduced, India and China will continue to buy Russian oil. The reasons are straightforward: Russian barrels remain highly cost-competitive for both Indian refiners and Shandong teapot refineries, and workarounds to maintain flows are likely to emerge. For example, a non-designated company could purchase crude from Lukoil and then re-sell it onward. Indian refiners may increasingly pivot to non-sanctioned Russian entities and opaque trading channels. Complex logistics—such as ship-to-ship transfers near Mumbai and mid-voyage diversions—highlight Russia’s adaptive commercial response.

Indian imports of Russian crude, by seller, kbd

Source: Kpler

Extended maintenance at Al Zour in December drives Kuwait’s crude exports higher

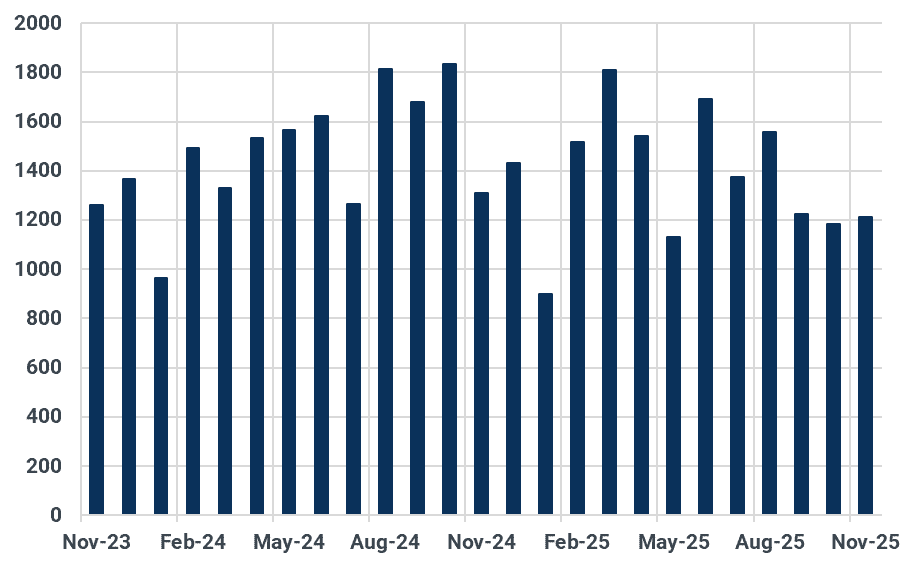

Kuwait’s 615 kbd Al Zour refinery, which started up in late 2022, has faced a series of unplanned outages in recent months. Maintenance on the refinery’s 205kbd crude distillation unit (CDU)—offline since 21 October—has been extended into December (now expected back on 9 December, versus the earlier 11 November target). In addition, the atmospheric residue desulfurization (ARDS) units have been partially offline since mid-October and are unlikely to return before mid-December. At the same time, one CDU at the 454kbd Mina Abdullah refinery was offline throughout October. As a result, Kuwait’s total refinery runs fell from typical levels of around 1.2Mbd to 1Mbd kbd in October. Reflecting recent developments, we have revised down our estimates for November and December, now projecting the country’s crude intake at 890kbd and 1Mbd, respectively. Amid the repeated operational setbacks at Al Zour, Kuwait’s reduced domestic runs have pushed crude exports to a 23-month high of almost 1.5Mbd in October, with further increases likely. We now expect November–December exports to average around 1.6mb/d. Looking ahead, India and China are set to absorb more Kuwaiti crude as they diversify supply in response to tightening US sanctions (see paragraph above). For example, 500kb of Kuwaiti heavy crude loading 6–7 December were recently awarded to Reliance.

Kuwait crude exports, kbd

Source: Kpler

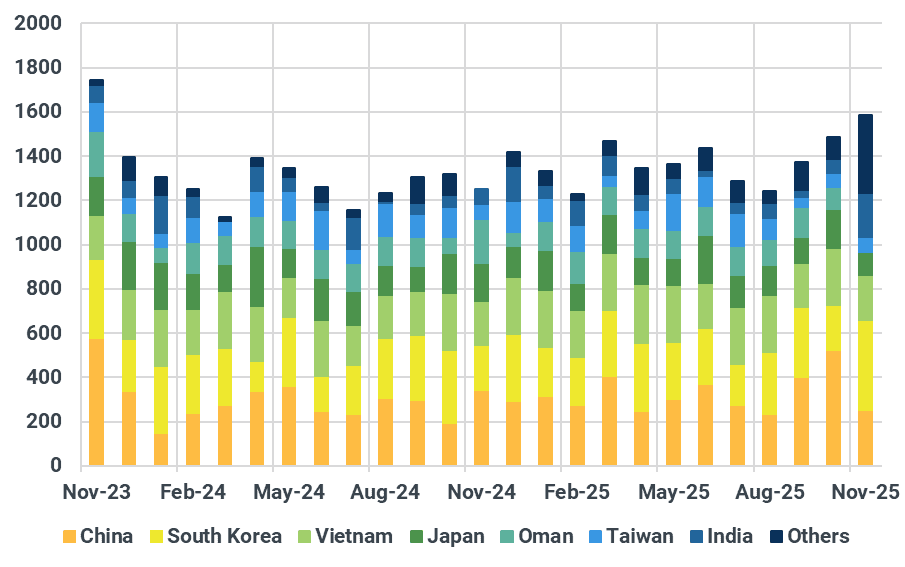

Iranian crude flows to China to remain suppressed for the rest of the year

Despite the recent tightening of sanctions on Iranian crude, Iranian loadings have remained elevated, holding close to 2Mbd in September and October. While Iranian barrels typically flow almost entirely to China, it is notable that only an average of 1.2Mbd have arrived there over the past two months. Part of the gap between Iranian loadings and Chinese arrivals represents crude currently floating on water. This reflects the fact that not all cargoes leaving Iran have secured final buyers, leaving a portion of supply in transit or in floating storage. This dynamic has pushed Asian floating storage to a three-year high. One of the main factors limiting short-term demand has been the exhaustion of crude import quotas among Shandong refiners. However, given the deep discounts on Iranian crude (currently around –$8/bbl versus ICE Brent, delivered Shandong), we expect buying activity to rebound quickly at the start of 2026.

Chinese imports of Iranian crude, kbd

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data

.jpg)