Tariffs threats and trade tensions lift the Asian sour market as gluts emerge in the West of Suez

Market & Trading calls

- Bearish on differentials of heavy Canadian and LatAm grades due to higher Venezuelan crude production and flows to the USGC.

- Bullish on Mideast medium crude as Indian refiners seek alternatives amid uncertainty over US tariffs on Russian oil; solid middle distillate cracks and firm Chinese demand continue to buoy prices.

- Bearish on WAF OSPs with seasonality and ample light supply in the Atlantic Basin, weighing on set prices for the September-loading cargoes.

Trades of the Month:

- Aramco September OSPs: Aramco is likely to raise its August-loading Arab Light and Arab Medium OSP by around $0.50–$0.70/bbl. Arab Heavy and Arab Extra Light could see a softer hike of $0.40–$0.60/bbl and $0.30-$0.40/bbl, respectively. Pricing into Europe and the US is likely to decrease by $0.80/bbl and $1.00/bbl, respectively, reflecting the weaker market structure than in Asia.

- Short Oct-Nov WTI spread with a potential cool down in global macro and Russia-related supply shock talk weighing on structure as end of summer balances come into closer focus.

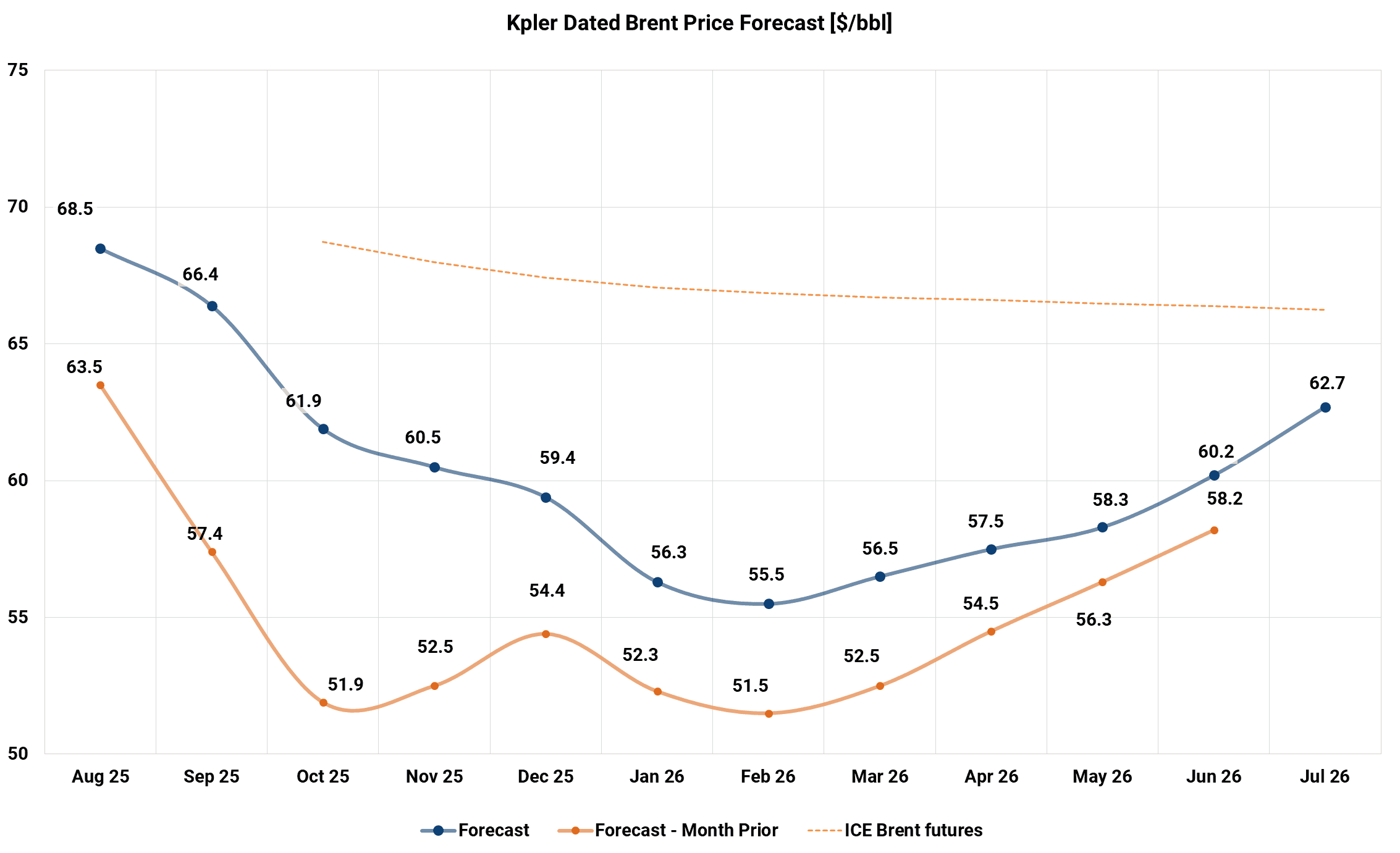

Price forecast: A disconnect from fundamentals amid geopolitical risks

Despite a notable deterioration in supply-demand fundamentals since last month’s Crude View, we have significantly revised our oil price forecast higher. Our new 12-month forecast for NSD now averages $60.30/bbl, up from $55/bbl in our previous update. This upward adjustment is not rooted in improving balances, in fact, our data points to a growing oversupply, but rather in the increasing disconnection between market sentiment and fundamentals. Oil prices are reacting more to political noise, especially signals from President Trump, than to actual physical imbalances.

Our updated balances show a sustained oversupply of roughly 2 Mbd through to the end of 2026. Yet, investor sentiment has turned more bullish, particularly on Brent. According to CFTC data, net long positions from portfolio investors and money managers on ICE Brent have surged from 166 Mbbls a month ago to 261 Mbbls today. WTI, in contrast, has seen net length halve over the same period, from 178 Mbbls to 88 Mbbls, suggesting a geopolitical skew in positioning.

One of the key drivers behind this divergence is the rising risk premium linked to Russian oil. The US administration has floated the possibility of secondary sanctions or tariffs on buyers of Russian barrels, creating uncertainty among market participants, particularly India. While no immediate supply disruption has materialised, the threat alone has been enough to lend support to prices.

Interestingly, other headline developments have failed to trigger material price corrections. Market participants brushed off bearish news such as the potential Trump administration reversal of Chevron’s license in Venezuela. Similarly, rising trade tensions and tariff announcements did not catalyse a sell-off. As a result, front-month ICE Brent has remained in a relatively tight range, oscillating between $67 and $73/bbl throughout July.

While we still expect the market to eventually absorb and react to the underlying weak fundamentals, we now believe that downside risks are more limited in the short term. One reason is the erratic, headline-driven nature of market reactions. President Trump's potential for sudden announcements has diminished speculative appetite on both the long and short sides. His recent quote that “WTI at $64/bbl is great” exemplifies the kind of verbal intervention that adds a floor to price expectations.

Politically, Trump’s position is also complex. While he advocates for lower fuel costs to support the broader US economy, he is unlikely to alienate key oil-producing states like Texas, North Dakota and Alaska, where his voter base is strong (56%, 67%, and 54%, respectively in 2024). With breakeven prices for new Permian wells estimated between $60–65/bbl WTI, we view this range as a short-term price floor.

That said, we still see scope for market fundamentals to reassert themselves in the medium term. By early 2026, as the oversupply weighs more heavily and inventories start to rebuild, prices could slip below $60/bbl. Yet even then, the downside will be limited by low OECD stock levels, particularly in the US, where the government may resume SPR refillings should WTI fall below $60/bbl.

Source: Kpler, ICE

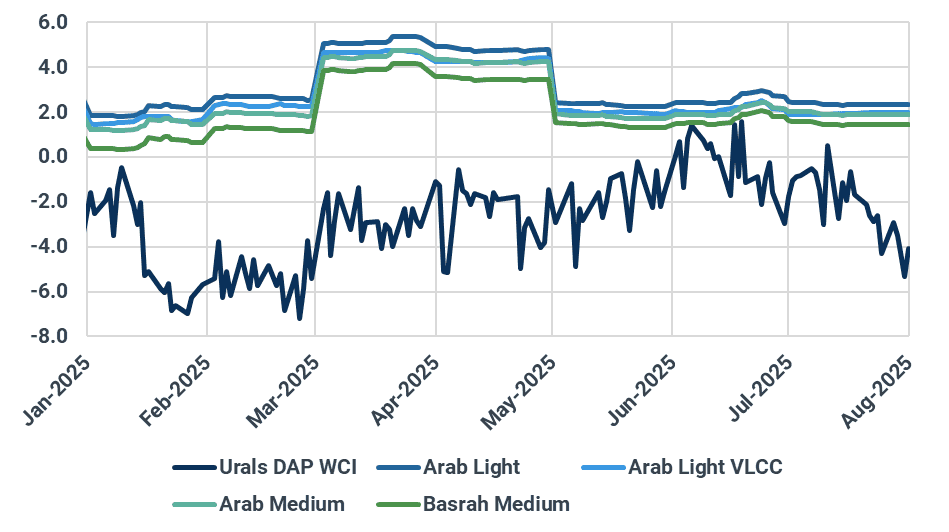

Chart of the Month: Urals depreciation to entice Indian buying appetite despite US threats

Tensions between Washington and New Delhi are rising as the Trump administration intensifies efforts to curtail Russian oil exports. President Trump, who once leaned more favourably toward Moscow, now appears to be recalibrating his stance, and his administration has ratcheted up pressure on the Kremlin. Recent US moves include sharply reducing the proposed ceasefire deadline from 50 to just 10 days, alongside escalating threats of secondary sanctions and punitive tariffs on countries continuing trade with Russia, notably India.

These moves have placed India in a difficult diplomatic and economic bind. On one hand, New Delhi is reluctant to abandon its long-standing policy of non-alignment and its access to deeply discounted Russian crude. On the other hand, it now faces the harshest tariff regime in the region, a 25% duty, imposed unilaterally by Washington. This marks a stark deterioration in relations, especially considering Prime Minister Modi was one of the first world leaders hosted by Trump earlier this year in Washington.

Yet, the “bullying tactic” may prove counterproductive. We understand that the Indian government has empowered its state-owned refiners to continue purchasing Russian oil based strictly on commercial terms and internal compliance. The economics are compelling: in response to US pressure and market jitters, Urals pricing into India has fallen sharply. The discount of Urals versus Arab Light on a DES India basis has now widened to more than $6/bbl, a level generous enough to outweigh political risk in the eyes of Indian refiners.

As long as formal secondary sanctions are not implemented, India is unlikely to reverse course. Since the outbreak of the Russia-Ukraine war, India has become Russia’s top seaborne crude customer, with Russian grades accounting for an average 36% of India’s crude imports year-to-date.

The pricing signal remains stronger than the political one, for now. And unless penalties move from words to enforceable actions, discounted Urals barrels will continue to find a home in Indian refineries.

Urals and Middle Eastern diffs against NSD, DES India, $/bbl

Source: Kpler based on Argus Media and company OSP data

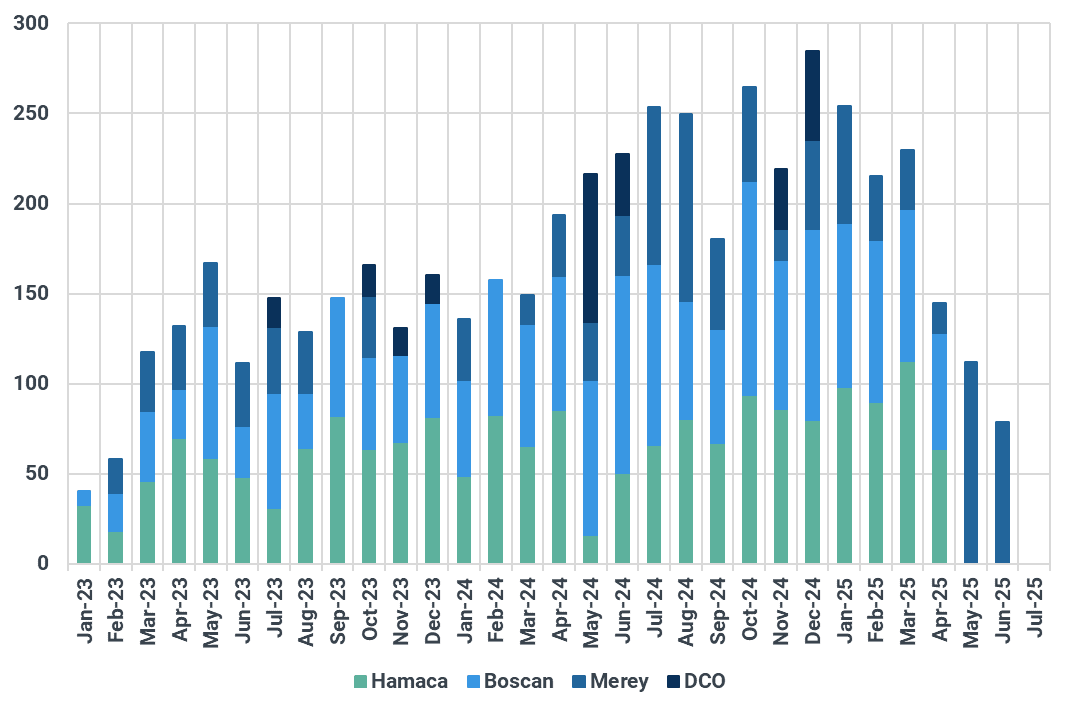

Heavy crude: Global crude balance lengthened by returning Venezuelan oil following Trump’s policy shift

Following President Trump’s decision in May to revoke Chevron’s waiver to produce and export Venezuelan oil, USGC imports of Venezuelan crude dropped sharply—falling to multi-year lows of 80 kbd in June and reaching zero in July. This marks a significant decline from year-ago levels of 230–250 kbd. At the same time, steep discounts on grades like Merey have redirected Venezuelan crude toward China, which has emerged as the country’s primary export destination. Imports into Shandong surged to a multi-year peak of 400 kbd in July. However, in a policy reversal in late July, the Trump administration issued a new license allowing Chevron to resume crude oil production in Venezuela. This move will prevent a previously anticipated drop in Venezuelan output and has led us to revise our supply forecast upwards for Q4 2025 (60 kbd for October, 120 kbd for November, 140 kbd for December) and 2026 (150-180 kbd). We now project crude and condensate production to rise from current levels of 830 kbd to approximately 900 kbd by year-end and trend within 900-930 kbd next year. The anticipated return of Venezuelan barrels is likely to weaken the valuation of competing heavy crude grades. In July, differentials for Latin American heavy grades such as Colombia’s Vasconia strengthened by up to $0.80/bbl versus WTI and Western Canadian Select (WCS) is currently trading near record highs (Argus Media). But with Venezuelan crude poised to re-enter the market, LatAm and Canadian heavy grades should come under pressure.

USGC imports of Venezuelan crude, kbd

Source: Kpler

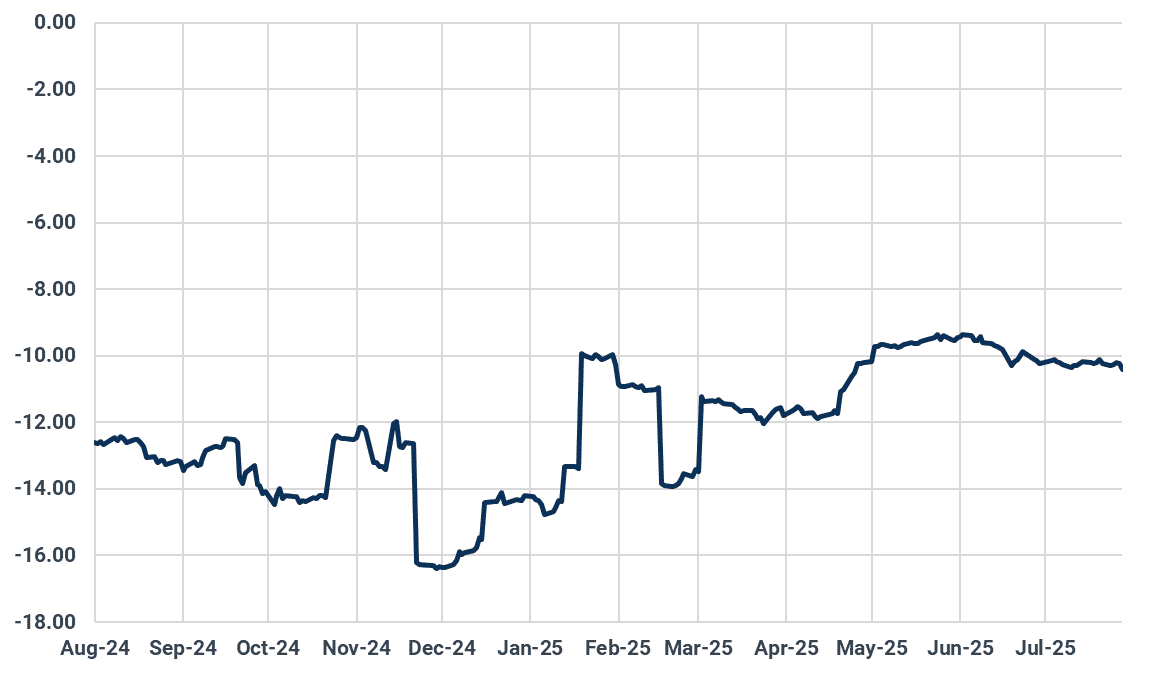

Ecuador’s crude and condensate production is estimated to have dropped to multi-decade lows of 175 kbd in July, following disruptions to two key crude export pipelines. Both the 450 kbd OCP pipeline and the 360 kbd SOTE pipeline were halted due to riverbank erosion. The OCP pipeline remained shut from July 1 to 22, while the SOTE pipeline resumed operations only in the final week of July. As a result, Ecuador’s crude exports were severely curtailed, falling to just 120 kbd in July, compared to an average of 390 kbd in the first half of 2025. Export volumes are expected to recover in August, rebounding toward typical levels of around 400 kbd. On the downstream side, the 110 kbd Esmeraldas refinery restarted operations on 31 July, ending an unplanned two-month outage that had suppressed the country’s domestic crude demand. The plant was initially taken offline on 26 May following a fire that damaged its power substation and several storage tanks. Earlier, from 25 April to 10 May, the refinery was also forced to shut down after an earthquake damaged ovens and equipment in multiple processing units. Despite higher domestic refinery throughput anticipated in August, the sharp increase in crude availability should weigh on differentials for Napo, which are currently trending around levels of -$10/bbl versus ICE Brent (Argus Media).

Napo crude differentials vs ICE Brent, $/bbl

Source: Argus Media

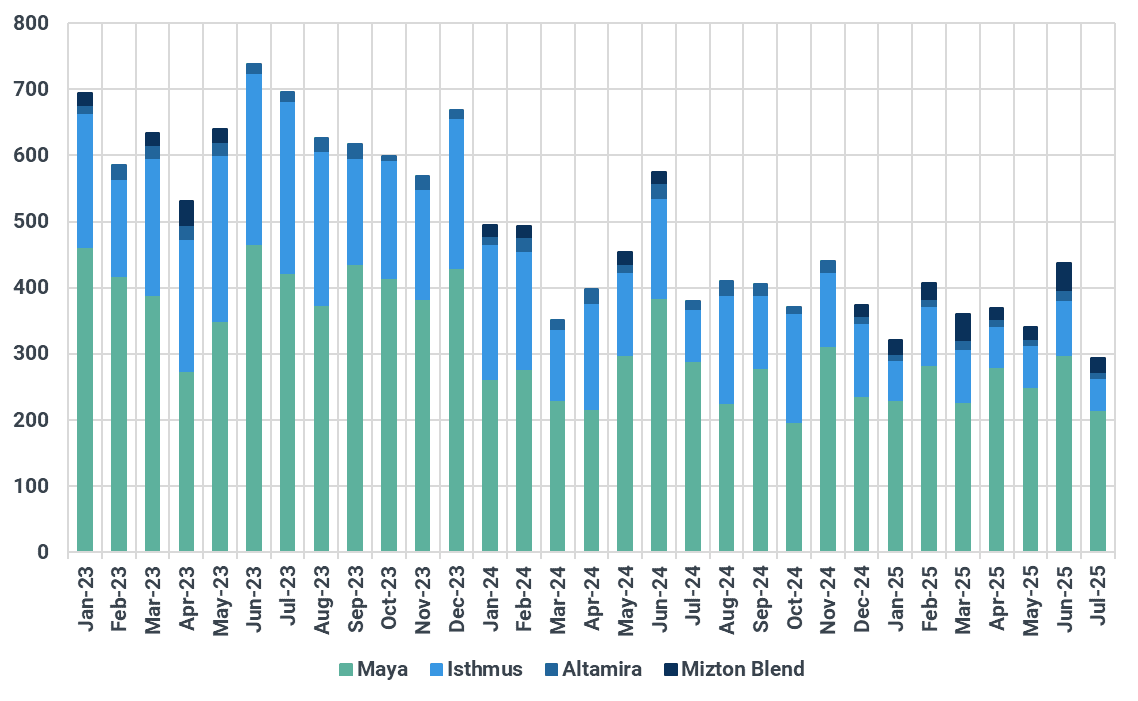

USGC crude imports from Mexico fell to 300 kbd in July, marking the lowest level on record in Kpler’s data history. This represents a decline of nearly 100 kbd compared to the same period last year and reflects the ongoing structural contraction in Mexico’s oil supply. We estimate that Mexican crude and condensate production declined from 1.82 Mbd in 2024 to 1.65 Mbd in the first half of 2025, with output projected to fall further to around 1.6 Mbd by the end of the year. This trend is supported by recent data from the Mexican Petroleum Fund, which shows that crude production from contracts awarded between 2015 and 2018 dropped by 17% y/y in May, reaching the lowest level in over two years. The reduced availability of Mexican crude, along with broader supply tightness in the Americas heavy crude market, has contributed to Pemex’s upward adjustment to its pricing formulas. For August, Pemex raised its K-factor across all crude grades and destination regions. Crudes destined for the Asia-Pacific market recorded the largest increases, with values rising by $0.65 to $1.15/bbl. Grades bound for Europe and the Middle East saw hikes of $0.50-$0.60/bbl. For destinations such as the USGC, the Atlantic coast of the Americas, and the Caribbean, increases ranged from $0.25-$0.65/bbl while crudes heading to the US West Coast and the Pacific coast rose by $0.15-$0.60 per barrel. Given that the USGC remains the primary destination for Mexican oil, benchmark grades like Maya and Isthmus will come under pressure from the return of Venezuelan barrels to the market.

USGC imports from Mexico, kbd

Source: Kpler

Medium crude: Tariff uncertainty and firm cracks lift Dubai market

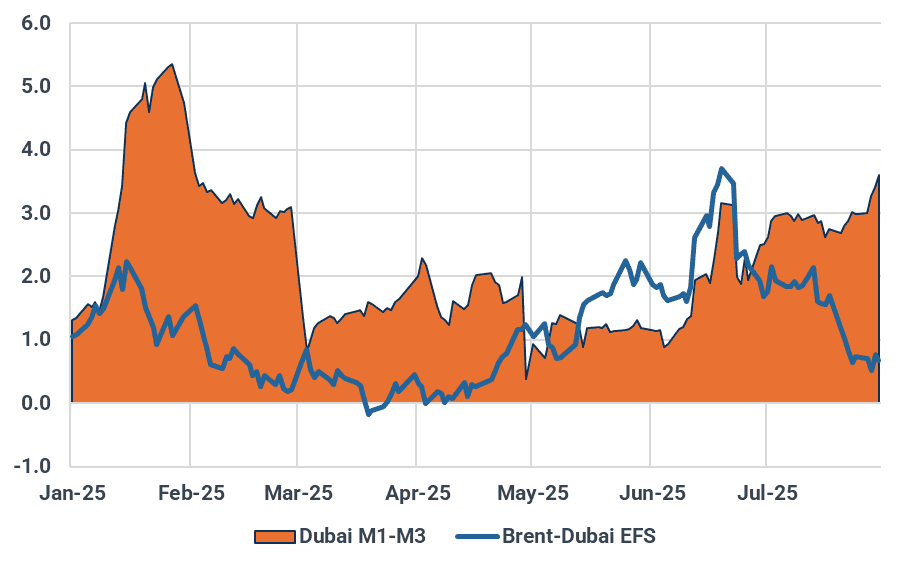

The Middle Eastern medium-density crude market heated up in July, even as some Asian refiners—who would typically start easing off purchases for September/October arrivals with peak summer demand waning and autumn maintenance looming—held back. However, a counter-seasonal rally, driven by China’s stockpiling and Trump’s tariff threats targeting Russian oil buyers, pushed the Dubai benchmark to a six-month high of $3.6/bbl by late July, according to Argus Media assessment. The spread between the front- and third-month Dubai contracts, a key indicator Middle Eastern producers consider when setting OSPs, widened by $1.10/bbl in July from the prior month. However, we expect Saudi Arabia to raise the price of its flagship Arab Light crude for Asian buyers at a smaller scale, by $0.50–$0.7/bbl in August, balancing recent buying strength with the need to stay competitive as the Kingdom ramps up output under the latest OPEC deal.

U.S. President Donald Trump threatened to impose 100% secondary tariffs on buyers of Russian oil if no ceasefire agreement is reached between Moscow and Kyiv by August 7–9. As a result, Indian refiners, who rely on Russian crude to meet nearly 40% of their feedstock requirements, have reportedly distanced themselves from Russian oil procurement, while simultaneously issuing more tenders last week for cargoes scheduled for September and early October arrival. The preferable replacement for Urals would be medium sour crude with high middle-distillate yields from the Middle East. However, Saudi crude is fully locked in term contracts, and most Iraqi barrels are similarly tied to long-term deals, while the bulk of Omani crude flows to China. Even UAE cargoes, which are actively traded in the spot market, appear tight as ADNOC has reduced Murban exports and the Upper Zakum oil field is slated for maintenance in October.

That suggests Dubai-pegged crude are expected to extend their strengths in early August as the uncertain US policy will keep the market inflated. The sour benchmark is likely to wane if Trump decides not to materialise the threat—which we think is highly likely—but firm gasoil cracks and ongoing Chinese stock replenishment will put a floor on the pricing.

Dubai M1-M3 spread, Brent-Dubai EFS, $/bbl

Source: Argus Media

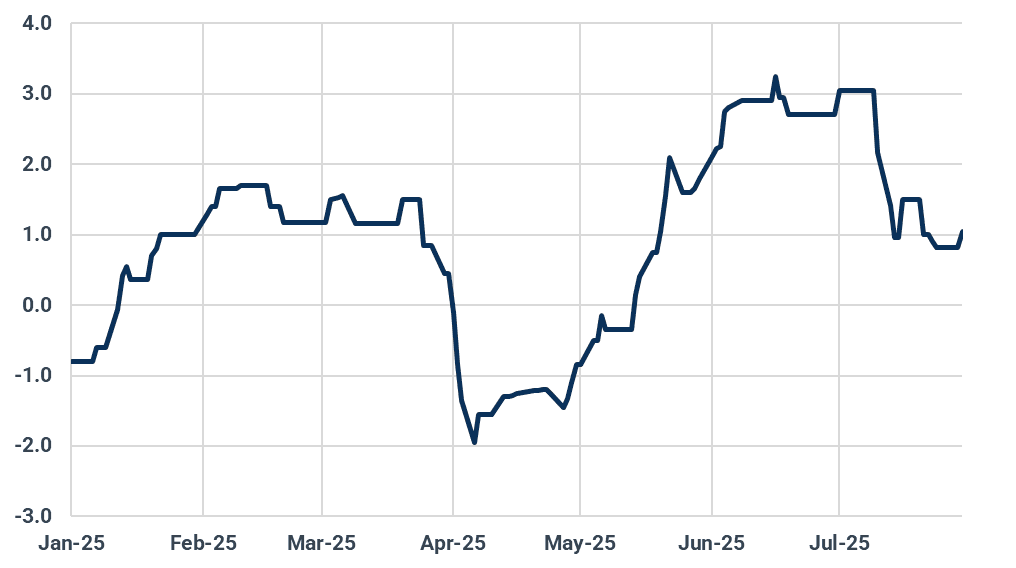

Medium sour Johan Sverdrup premiums saw a sharp correction in mid-July, plunging from over $3/bbl to $0.80/bbl against Dated Brent on an FOB Monstad basis within just two weeks, according to Argus Media assessment. The Norwegian grade had been rallying since June, as European refiners ramped up crude intake to meet peak summer demand. Meanwhile, the 12-day Israel–Iran conflict in the Middle East intensified concerns over tight gasoil supplies in Europe, pushing gasoil cracks to a 1-1/2-year high in early July. Lucrative arbitrage opportunities have prompted producers from the Middle East, India, and the U.S. to ramp up gasoil exports to Europe, signalling potential pressure on cracks as inventories build.

At the same time, medium crude supply appears ample in Europe, supported by steady Johan Sverdrup loadings, Johan Castberg production peaking at 220 kbd, and rising inflows from other regions. Kpler data showed Iraq’s crude exports to the Mediterranean region climbed to a 10-month high in July, reaching 452 kbd. More August-loading, destination-free Iraqi barrels were reportedly offered in the market, as the OPEC member ramped up output in line with the broader production plan. According to Argus, Basrah Medium was traded at just $0.05/bbl over its OSP to Mediterranean refiners in late July—down from $0.50/bbl in the first half of the month. Europe-bound Guyanese crude also surged in July, reaching a five-month high of 446 kbd, as it was priced more than $1/bbl below Johan Sverdrup on a landed basis. Now that Johan Sverdrup prices have collapsed—making it slightly cheaper than the Guyanese medium sweet crude—the resulting downward pressure is likely to ripple across the Atlantic Basin.

Johan Sverdrup diff to North Sea Dated, $/bbl

Source: Argus Media

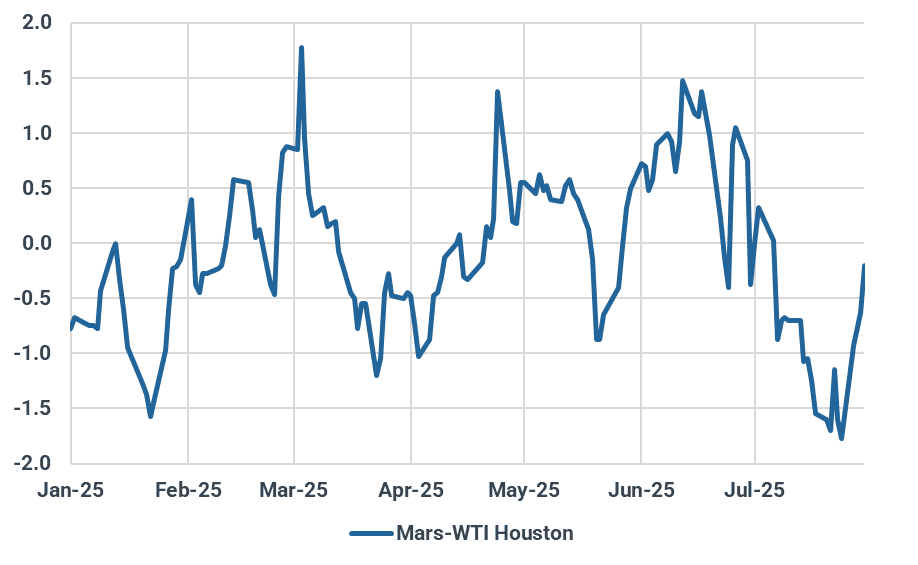

In the U.S., Mars crude traded at a steep discount to WTI throughout July due to zinc contamination issue, prompting refiners to shy away from lifting the barrels. As a result, ExxonMobil borrowed 500 mb from the SPR to meet its refinery requirements. However, after the quality issue was resolved in late July, Mars crude’s discount to WTI Houston quickly narrowed to -$0.20/bbl, recovering from a low of -$1.70/bbl earlier in the month, according to Argus Media assessment. While firm gasoil cracks in the U.S. may fuel a rebound in Mars crude, the potential resumption of Venezuelan oil flows could cap gains for medium sour grades. Washington has reportedly reauthorized Chevron’s operations in Venezuela, although the license has not yet been issued and the detailed terms remain unclear at the time of writing. To compensate for the loss of Venezuelan barrels following the expiration of the previous license at the end of May, U.S. Gulf Coast refiners increased imports from Saudi Arabia, Colombia, and Guyana. However, total arrivals in June and July still fell short of May levels.

At the same time, firm demand in Asia for Middle Eastern crude—driven by growing concerns over the risks associated with buying Russian oil—suggests that a sizable portion of the additional Middle Eastern supply in August and September, even as the OPEC+ group ramps up production, will remain in Asia, leaving limited volumes available for the U.S. market. A stronger Dubai benchmark narrowed the Brent-Dubai EFS to around $0.70/bbl by late July, down from nearly $2/bbl at the start of the month. This has improved the economics of Brent-pegged crude, such as medium-density Brazilian grades, in the Asian market. Tupi is now assessed at about $1.50/bbl below Oman and nearly $1.00/bbl below Upper Zakum on a delivered basis. With the Brent-Dubai spread expected to remain narrow in the near term and Chinese refiners ramping up crude purchases for SPR replenishment, Brazilian crude prices are likely to remain supported—even as the country’s oil production continues to grow steadily.

Mars diffs against WTI Houston, $/bbl

Source: Argus Media

Light crude: Differentials steady as regional gluts emerge despite strong runs

The global light crude market painted a mixed picture in July. While strong summer refinery runs provided a solid demand floor, growing length in key regions and specific quality issues weighed on differentials, particularly in the Atlantic Basin.

Spot buying activity slowed as the month progressed, with many end-users having already secured their prompt requirements to capitalize on peak margins. This led to a softening of physical values from West Africa to the US Gulf Coast, forcing barrels to find new homes and reopening long-haul arbitrage routes to Asia that had been shut for months.

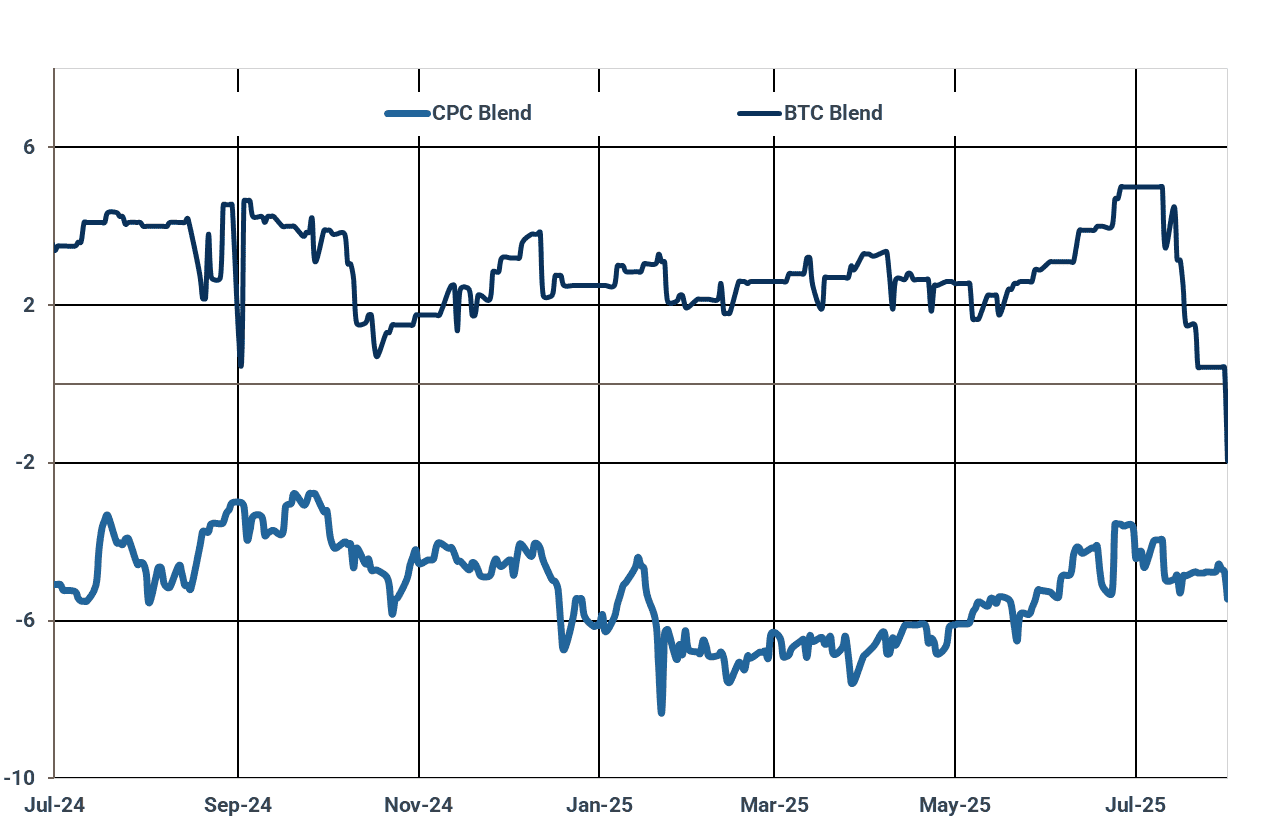

The Mediterranean was a particularly heavy region this past month, with prices for prime light sweet Azeri Light falling to long-term lows due to a quality issue. Organic chloride contamination discovered in Azeri BTC cargoes caused loading delays and soured buyer sentiment, sending the grade’s CIF Augusta value tumbling to its lowest since August 2022, assessed around a $0.50/bbl premium to Dated Brent on July 22, according to Argus Media.

Although the quality specifications are reportedly back to normal, the incident contributed to a build-up of prompt length in the region. To help ease this glut, the arbitrage window for CPC Blend crude to Asia opened substantially for the first time in four months. Four August-loading cargoes were fixed for buyers in the Far East, a significant shift after punitive freight rates and a firm differential had kept nearly all CPC volumes loading from May to July locked within Europe. This reopening comes as sweet crude supply in the Med has lengthened on lower-than-expected demand from some European refiners, causing CPC differentials to ease from their recent highs.

Mediterranean sweet differentials to Dated Brent, $/bbl

Source: Argus Media

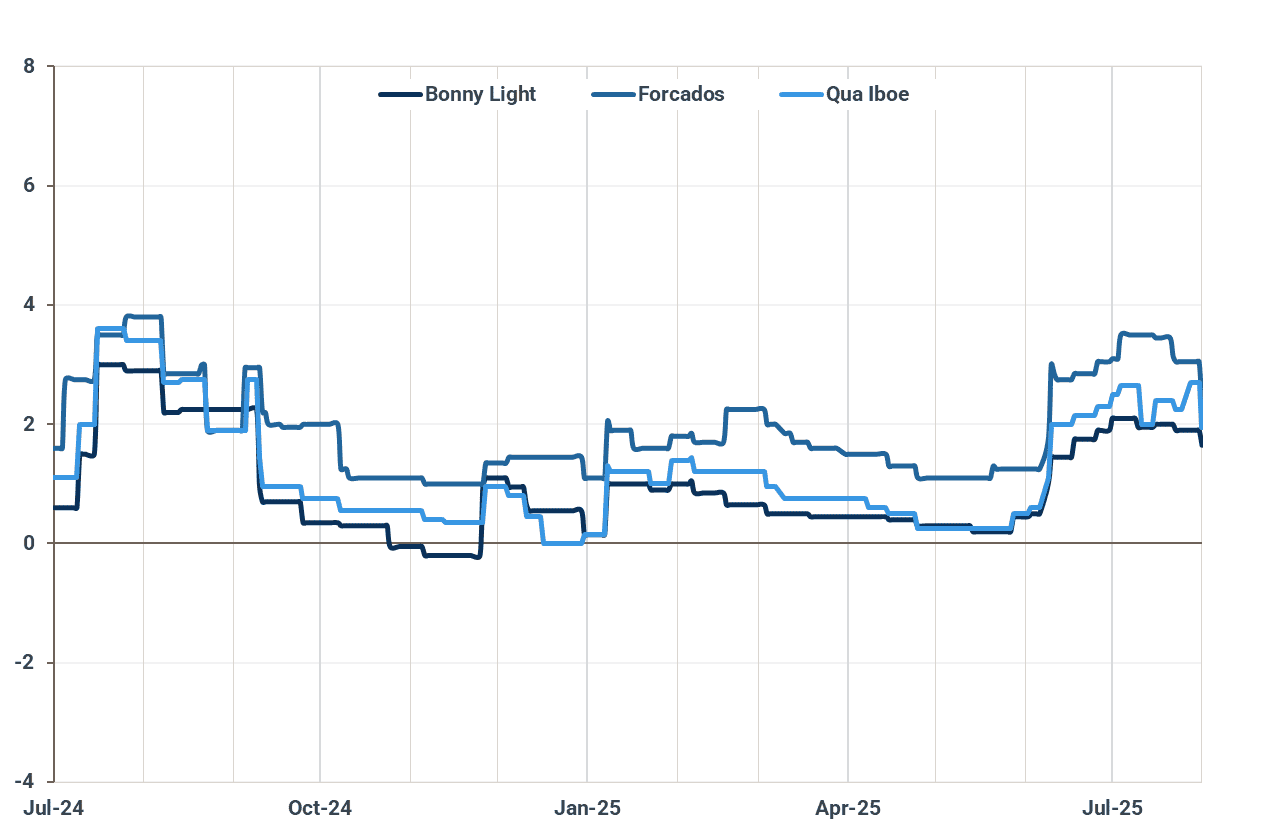

The impact of softening Mediterranean sweet values has been a key concern for sellers in West Africa, with traders worried about the ability of prompt-loading cargoes to compete in a softening Atlantic Basin.

However, despite an overhang of Nigerian cargoes for August still needing to clear, valuations for key light sweet grades remained fairly steady through the latter half of the month. The prior strength in June was significant enough to prompt Nigeria's state-owned NNPC to raise its official formula prices for nearly all August-loading exports by between $0.23/bbl and $2.20/bbl. The hikes, which were slightly more than expected, reflected peak summer demand from European and Indian refiners. Overall WAF flows dipped slightly in July to around 3.8 Mbd.

Looking ahead, Chinese state-owned buyers were reportedly pivoting towards more Angolan crude for September loading, potentially as an alternative if sanctioned barrels become harder to source. Nonetheless, the outlook for light WAF barrels is likely to dim as approaching refinery maintenance in September will weaken regional demand and put downward pressure on differentials.

WAF sweet differentials to Dated Brent, $/bbl

Source: Argus Media

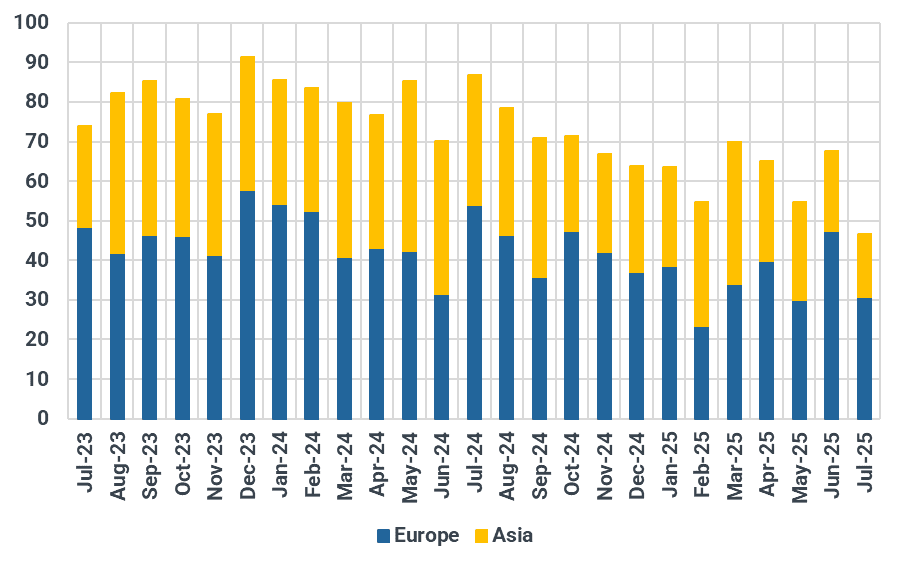

On the other side of the Atlantic, WTI valuations remained fairly steady for the month, but a clear lack of demand pull from Europe is weighing on CIF values and forcing barrels to look east. Differentials for WTI Midland on a CIF Rotterdam basis fell to a two-month low on July 28, according to Argus Media, pressured by an emergence of ample end-August light barrel availability in the region.

With expectations of further pressure on prompt European cargoes, Asia is now expected to increase its WTI imports. The arbitrage window has been pushed open by strengthening Middle East official selling prices, particularly for grades like Murban, which has seen increased regional demand. The WTI-Murban spread on a CFR China basis is now in favour of WTI, likely prompting demand for US crude in the weeks ahead. Furthermore, the threat of US secondary sanctions on buyers of Russian oil has prompted some buyers, like those in India, to seek more supply from the Gulf, tightening the East of Suez market and making US barrels more attractive.

Sentiment for a major transatlantic demand boost from the new US-EU trade deal remains muted. This lack of a clear directional catalyst is also reflected in WTI futures, where positioning suggests a lack of clear conviction, with the light market needing a clear external factor to create a new price trend.

WTI exports to Europe and Asia, Mbbls

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Get research & analysis driven by proprietary data