When will Saudi Arabia’s utilities ditch oil?

Saudi Arabia is radically transforming its utilities, targeting a 50% renewables and 50% gas energy mix under Vision 2030. This ambitious pivot could wipe out 1.1 Mbd of its utility-led liquids consumption, unleashing more crude for export and dramatically curbing the typical summer surge in HSFO demand while reshaping the seasonal strength in residual fuel prices. But how soon will this future arrive?

Not yet. Major new gas plants that are meant to replace oil-fired stations are not due to be commissioned for at least another two years, limiting any significant disruptions to crude and fuel oil utility consumption.

Despite renewable capacity additions and some power plant oil-to-gas conversion projects, Saudi Arabian utilities still have a few more years of sustained liquids consumption given the Kingdom’s push for economic reform which is boosting its electricity demand through industrial diversification.

In the first two months of the year, official JODI data showed a notable decline in Saudi Arabia’s direct crude burn falling 11% and 21% y/y in January and February, respectively, sparking concerns of shifting demand dynamics. But rather than a structural shift in liquids demand, we believe the generally milder temperatures at the start of the year and the marginal increase in the Kingdom’s renewable power generation capacities contributed to the decline in direct crude burn over this period.

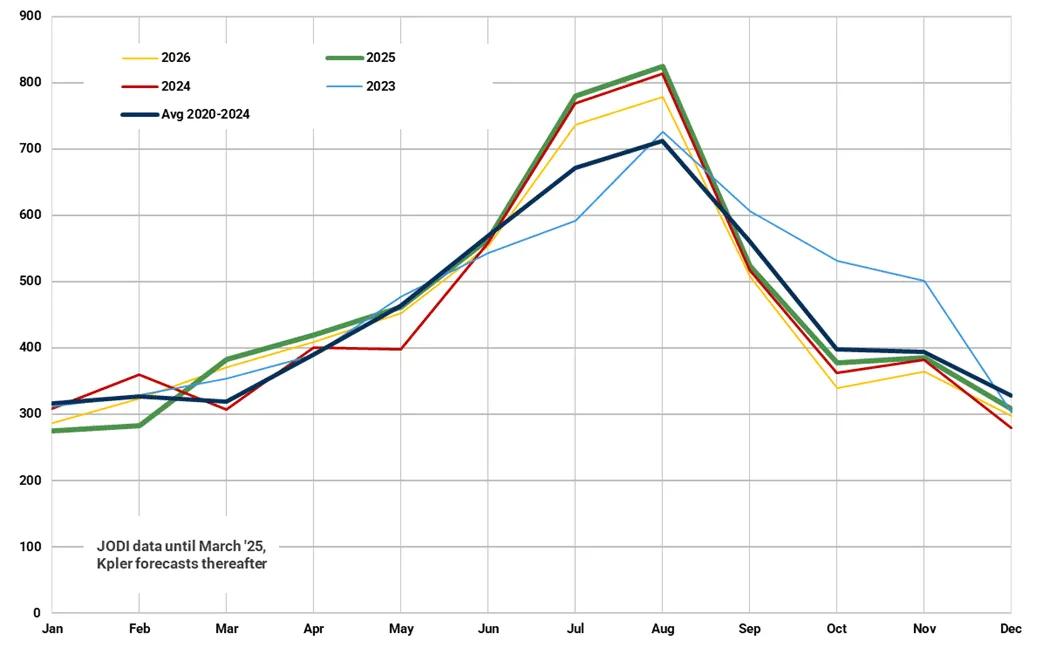

Saudi Arabia crude oil burning (kbd)

Source: JODI, Kpler forecasts

Fresh March data showed a 25% y/y rebound in direct crude burn with gradually rising temperatures, and we believe this strength in crude burn will be sustained over the coming months. For Saudi Arabia, the accelerated OPEC+ oil production increases from May will likely support its utilities elevated feedstock requirements and help reduce its HSFO import requirements, particularly given the particularly strong HSFO prices in recent weeks, which have seen Asian HSFO cracks trade at a strong premium to benchmark Dubai crude.

Natural gas accounts for about 62% of electricity generation, with oil contributing approximately 38% while renewables account for less than 1% of the energy mix, according to the EIA.

Oil-fired utility demand surges in the summer to supplement peak electricity demand as temperatures soar above 40 degrees Celsius. Saudi Arabian liquids demand should therefore continue to increase this summer, keeping both HSFO and crude oil requirements elevated.

Supporting expectations of strong electricity demand in Saudi Arabia and beyond, the World Meteorological Organization cited by Argus said that global temperatures, on an annually averaged basis, "are likely to continue at or near record levels" over 2025-29 and will stay "well above" the annual temperatures seen in the last 60 years.

Coupled with the tightening of global HSFO supplies amid rising refinery complexities and firming demand for HSFO bunkers, this has been a key driver behind the unprecedented strength in HSFO cracks across all key regions.

Saudi Arabia monthly oil burn (kbd)

Source: JODI

*assumes fuel oil demand is burned in utilities

Saudi Arabia’s HSFO imports in the first five months of the year are on par with year-ago volumes, pointing to a maintained status quo in liquids demand. Meanwhile, last year direct crude burning rates went on to climb to nine-year highs of 814 kbd in August, and there is a strong likelihood this year will see similarly substantial volumes for the above-mentioned reasons. The accelerated OPEC+ production increases could also help boost Saudi Arabia's direct crude burn this summer.

The Switch

The shift towards gas will be gradual and Saudi Arabia’s ambitious transition towards renewables is likely to fall short of its announced 100-130 GW target, reinforcing our view that liquids utility demand will remain strong for most of this decade.

Riyadh’s PP10 power plant fuel conversion project, which aims to switch from using liquid fuels to natural gas, is the most significant in terms of reducing the utility sectors’ near-term liquids consumption. Phase 1 of the project, slated for completion “by 2025”, will convert 20 of the 40 turbines at the 3.5 GW plant to run on natural gas, with the remaining 20 likely to be converted in the future. When completed, the first phase of the gasification project could cut approximately 40-60 kbd (170-250 kt/month) of liquids consumption, depending on the operational profile of the turbines. At the time of writing, there were no official announcements of the project’s completion.

Meanwhile, the Saudi Electricity Company (SEC) has stated that the PP10 conversion is part of a broader portfolio of 8 generation projects, totaling 22.3 GW, being converted from liquid fuel to gas by 2030. This includes conversion of the 825 MW Yanbu 2 oil-fired power plant, due for completion by 2028. Most other major conversion projects are slated for completion “by 2030”.

The Gas

At the same time, Saudi Arabia has made significant investments into greenfield gas-fired power plants totaling as much as 25 GW in new capacity additions by 2030, according to data compiled by Kpler. These will complement or replace its existing assets. The first of these, however, are scheduled for commissioned in 2027 while a bulk of them are due to come online in 2028. A large-scale decommissioning of less efficient oil-fired power plants is therefore unlikely until at least 2028.

The Jafurah unconventional gas field is a cornerstone of the strategy to replace oil consumption with gas. The Jafurah field aims to boost the Kingdom’s gas production by 60% from 2021 levels. The field is expected to ramp up from 200 million standard cubic feet per day (scfd) in 2025 to reach a sustainable gas rate of 2 billion scfd of sales gas by 2030. This again indicates that a switch from oil to gas will be gradual over the coming years before ramping up towards the end of the decade.

Saudi Aramco has not officially announced that the Jafurah gas field has commenced production. However, the company has indicated that initial operations are expected to begin later this year, potentially in Q3.

According to Aramco, its unconventional gas program, led by the Jafurah field, is projected to displace up to 500 kbd of crude oil from domestic use at peak output—with Jafurah alone accounting for over 300 kbd of that total.

The Renewables

Renewables accounted for just about 1% of the Kingdom’s total electricity generation mix as of 2023, or 3.2 GW of installed capacity. Since then the kingdom has been steadily rolling out projects which are on track to nearly double the current installed capacity to 12.8 GW by the end of 2025.

As part of Vision 2030, the Kingdom aims to generate 50% of its electricity from renewable sources by 2030, targeting a total capacity of 130 GW. Despite the accelerated capacity additions since 2023, this gives the target of 100-130 GW by 2030 remains highly ambitious.

By July this year, renewable power sources connected to the grid is around 10.213 GW and the remaining to be connected until the end of the year is 2.5 GW from three projects. While an additional 34.4 GW of projects planned for completion by 2027.

Depending on how far its energy mix strays from its renewable target, this strengthens the notion that the complete switch away from oil-fired power plants will have to be postponed, delaying plans to retire oil-fired plants and extending the utility sectors’ reliance on liquid feedstocks for longer.

The Growing Demand

Another pillar of the Kingdom’s Vision 2030 is its aim to diversify the economy away from its reliance on oil. The economic reforms are boosting electricity consumption and placing increased demands on power generation capacity. This compounds the country’s energy demands and means that more power generation will be needed to satisfy its growing demand and prevent oil-fired consumption from expanding further, let alone replacing it.

While Saudi Arabia is promoting energy efficiency in homes and industry under Vision 2030, efficiency gains will be outweighed by the rapid growth of its industrial sectors.

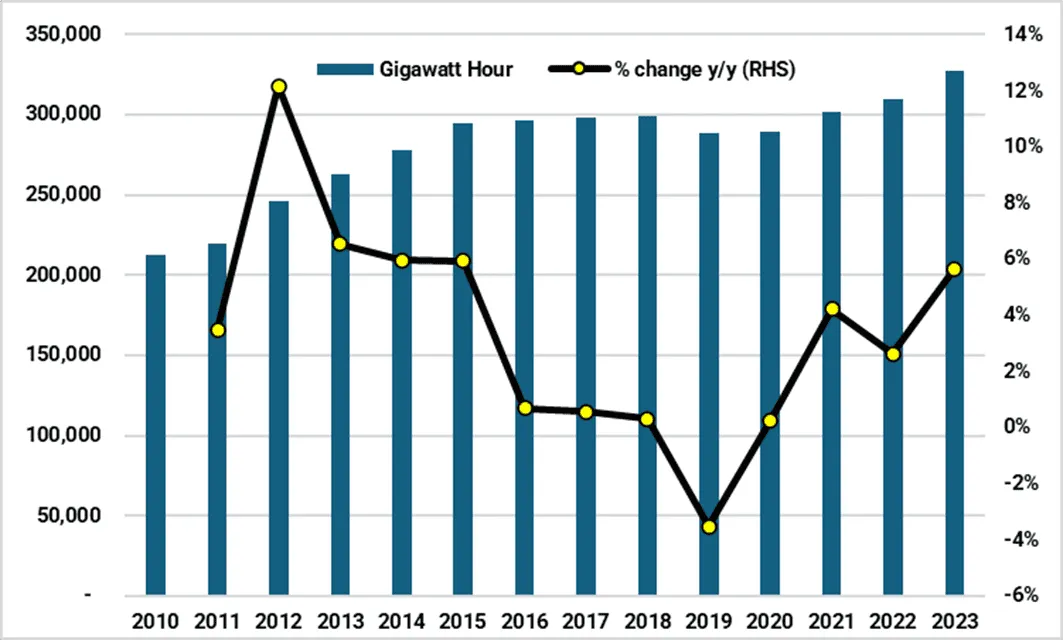

Saudi Arabia total electrical energy consumption (GWh)

Source: Saudi Arabia General Authority for Statistics

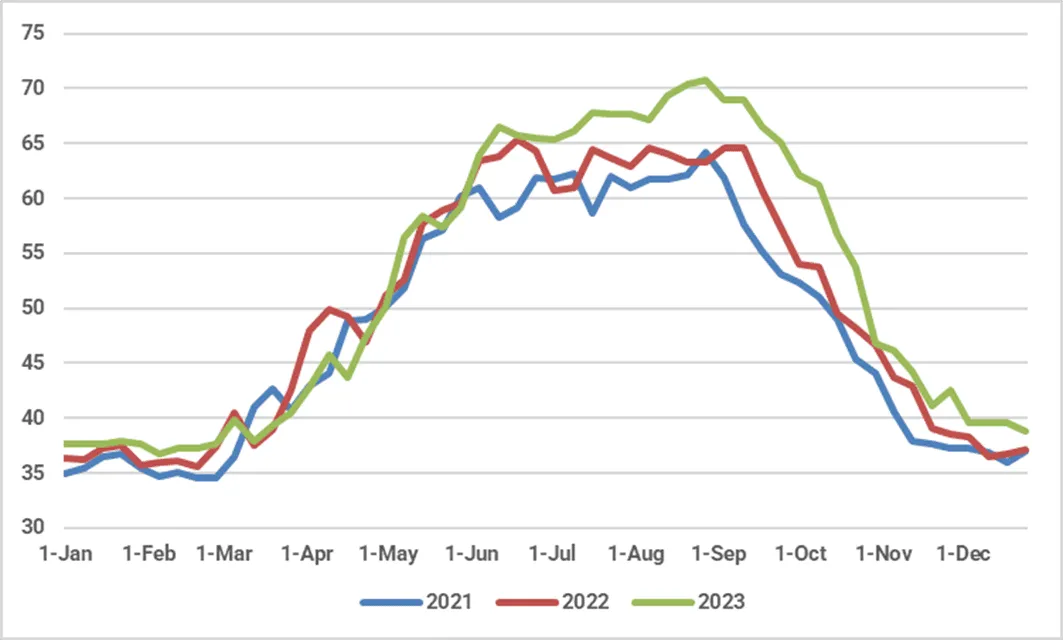

Saudi Arabia weekly peak load (GW)

Source: Saudi Electricity Regulatory Authority

Water desalination is also a significant consumer of power in the Middle East. In the context of Saudi Arabia, the primary energy source for most new large-scale Reverse Osmosis (RO) desalination plants is electricity drawn from the national grid.

However, a significant and growing trend is the integration of dedicated renewable energy sources, predominantly solar PV, to power these facilities partially or, in some cases, fully. As of 2024, the Saudi Water Authority (SWA) has reported that 20% of the energy used in its new desalination plants comes from renewable sources, primarily solar power.

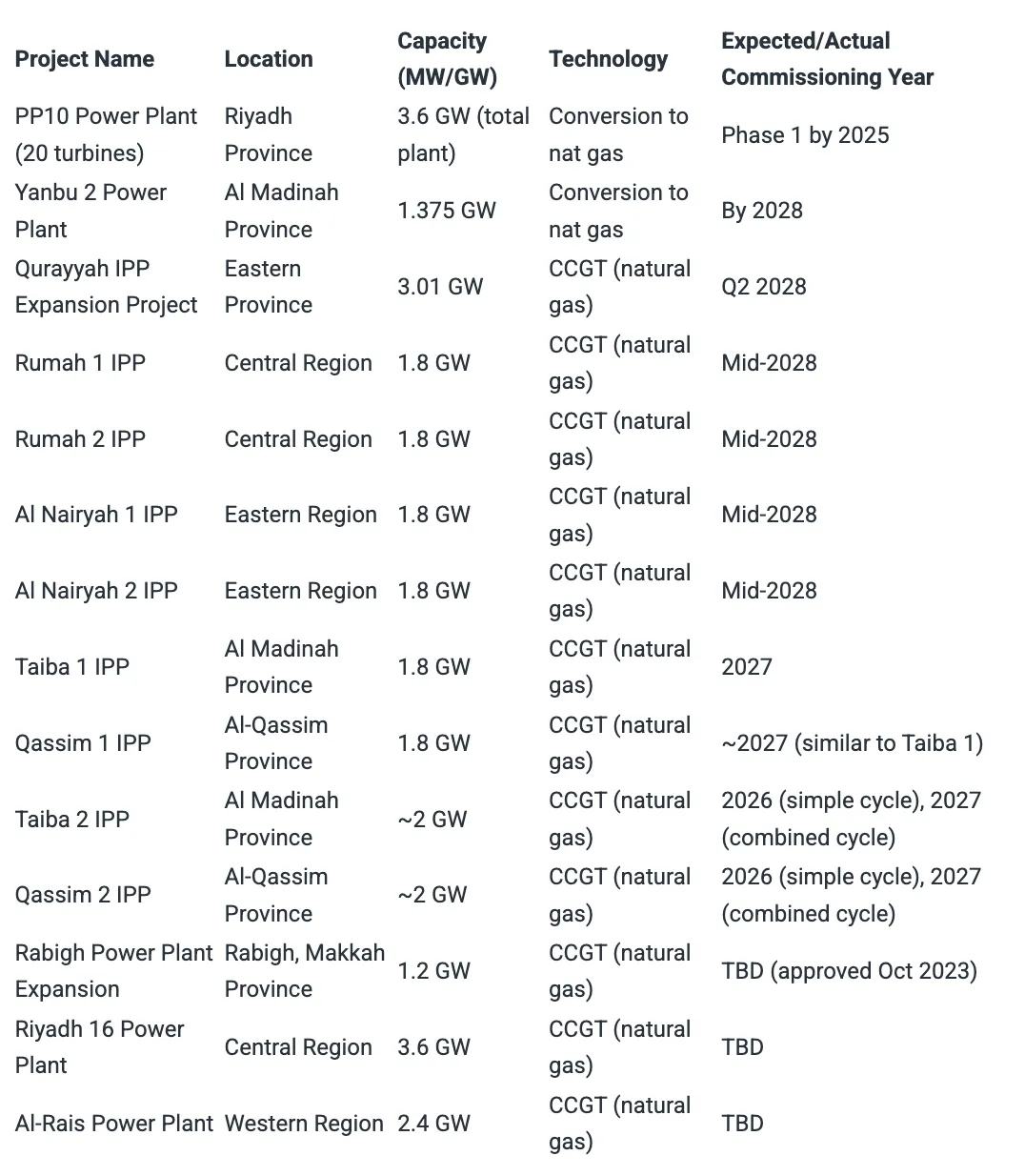

Major operational and planned natural gas power plants in Saudi Arabia since 2023

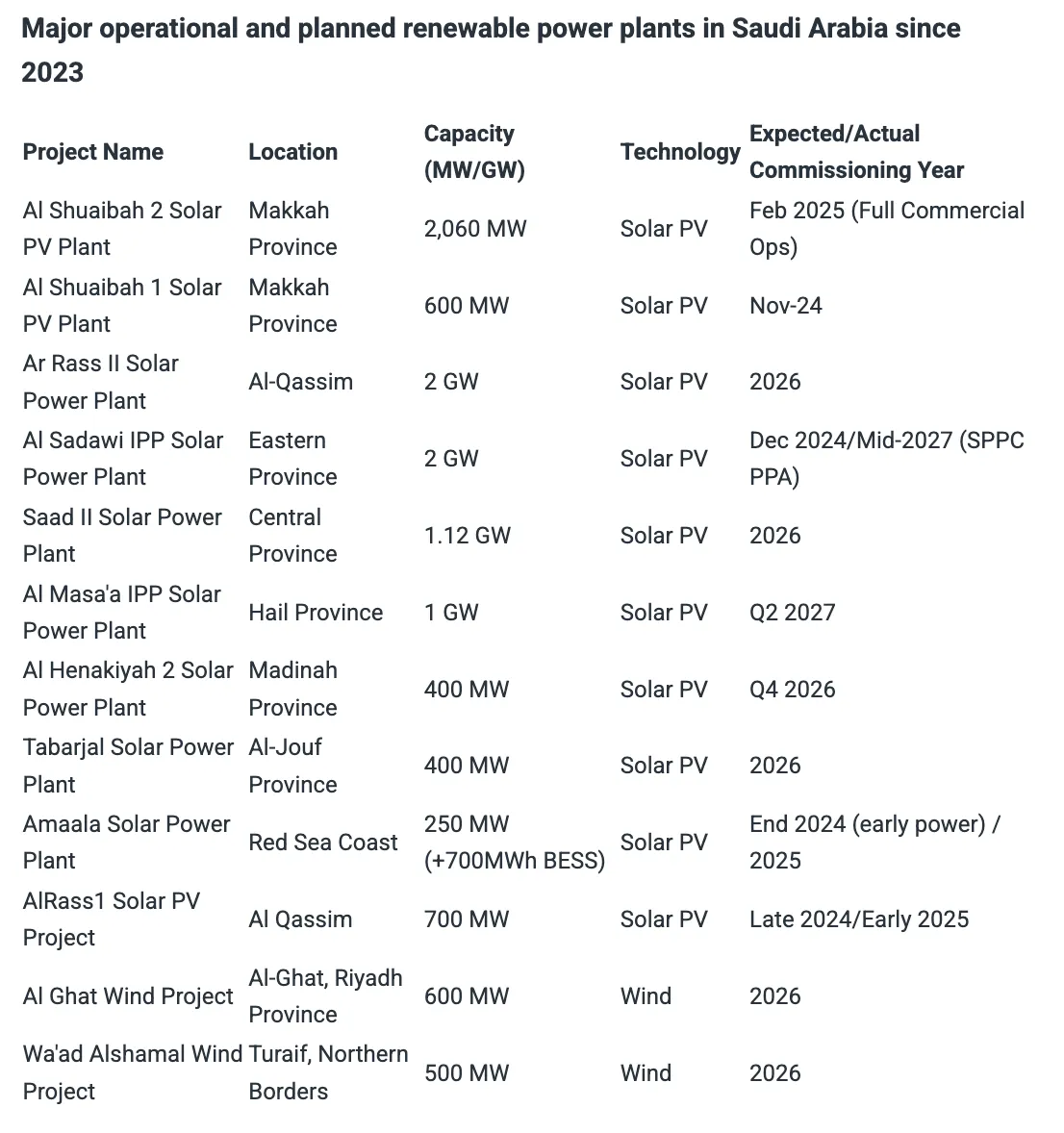

Major operational and planned renewable power plants in Saudi Arabia since 2023

Source: SPPC, SEC, ACWA Power, GE Vernova, etc. Note: Some commissioning dates are estimates based on available information and may be subject to change. BESS = Battery Energy Storage System. TBD = To Be Determined.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions - backed by the most accurate oil price predictions two years running.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data