August 20, 2025

Brazilian iron ore drives Capesize upside despite ballast build-up in Asia-Pacific

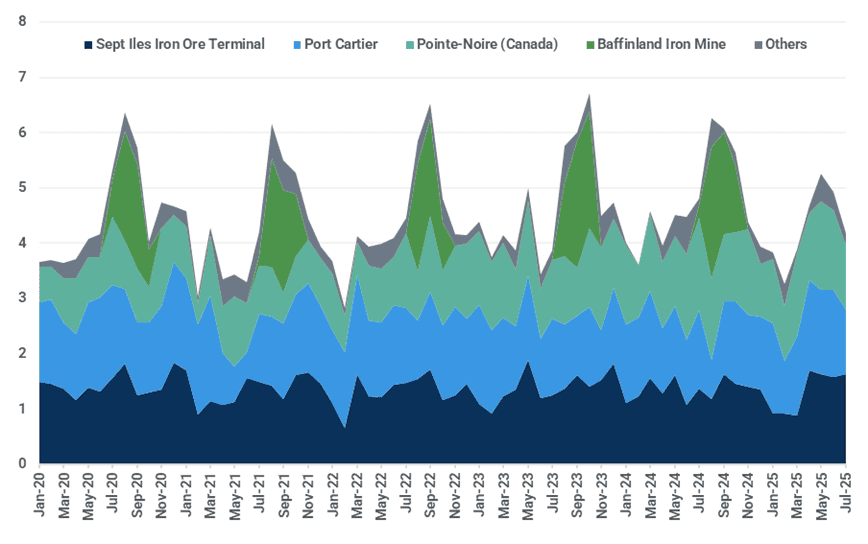

Iron ore & steel: Baffinland opens for business, pushing up Canadian iron ore exports

- Global seaborne iron ore exports dropped to a three-month low of 30.20 Mt in the week ending 10 August, falling short of the previous five-year average of 31.60 Mt for the period. The decline comes as both FMG and Hancock Iron Ore shipments dip to multi-month lows due to maintenance works. Meanwhile, Canadian exports reached a nine-month high of 1.40 Mt as Baffinland resumed operations in line with its traditional summer shipping window.

- In Russia, the Taman terminal handled its first iron ore exports since 2023, with a Panamax and Capesize vessel departing in late July and early August, respectively. This is likely because soft demand for coal transport has freed some capacity for other bulk cargo. Nevertheless, the majority of Russia’s iron ore exports continue to originate from Novorossiysk, Murmansk, and Ust-Luga, a trend unlikely to change in the near term.

- On the demand side, Chinese seaborne iron ore imports soared by a quarter w/w and 12% y/y to 28.65 Mt last week, one of the highest on record. The rise reflects the clearing of weather-related backlogs after multiple typhoons, alongside a seasonal peak in shipments from Brazil. Meanwhile, crude steel production by CISA member mills averaged 2.07 Mt in the first ten days of August. Although the reading improved from the year-to-date low of 1.98 Mt in late July, it remains subdued compared to the previous months.

- Despite modest fundamentals, iron ore prices remained resilient over the past week, partially supported by buoyant market sentiment following the US-China tariff truce for another 90 days. The most-traded contract on DCE, January 2026, closed flat w/w at 775 yuan/t ($107.93/t) on 14 August, while the SGX TSI 62% Fe second-month contract edged up by 0.09% to $102.35/t at the time of writing. We continue to believe that the recent price strength is unsustainable given the absence of firm demand-side drivers.

Baffinland shipments drive Canadian exports to a seasonal peak in Q3 (Mt)

Source: Kpler

Coal: Renewables weigh on European coal demand, coking coal market rebounds

- The cif ARA market weakened recently, testing mining costs for producers in the Atlantic basin as prices fell below $100/t. Colombian miners face negative margins with net-backs around $85/t versus their $70-75/t mining costs. Meanwhile, high-grade Australian coal remains strong above $110/t in the Asia-Pacific.

- Unseasonably high wind output in early August reduced thermal generation needs in Germany, limiting coal plant operations to essential grid support. About 400,000t of coal will arrive at Amsterdam-Rotterdam-Antwerp this week. These deliveries are mostly Australian coking coal cargoes.

- Indonesia will reduce coal production as demand recovery in China and India appears unlikely. The Indonesian Coal Mining Association (APBI) forecasts 2025 exports at 500Mt, down 55Mt year-on-year, with total production falling 100Mt y/y to 739Mt.

Indonesia coal exports y/y (Mt)

Source: Kpler

- China's supply tightening has grown more pronounced, with NEA inspections planned for Shanxi, Shaanxi, Inner Mongolia, and Xinjiang. Heavy rainfall disrupted mining in Ordos and Shaanxi, pushing up mine-mouth thermal coal prices. This should support imported coal prices in the coming weeks. Shanxi Coking Coal Group limited 11 mines to 276 working days annually. Further cuts would raise prices as Shanxi is a key coking coal producer. Coking coal prices have rebounded in the Asia-Pacific region, with the FOB hard-coking-coal price rising above $190/t level in recent days.

- The US and China extended their trade truce, avoiding tariff hikes. Due to tariff risks, Chinese buyers had limited US coal and petroleum coke purchases. Reduced petcoke availability may boost short-term pricing sentiment in the wider market.

Grains & Oilseeds: Record yields forecast for US corn and soybeans weighs on ending stocks

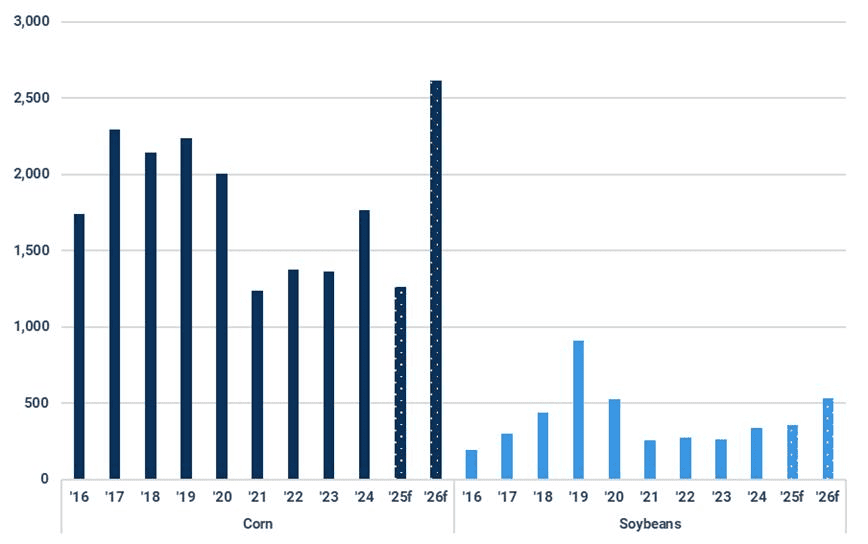

- In the USDA’s August WASDE report, the US corn yield estimate for 2025 was raised from 181 bu/ac to 188.8 bu/ac and area planted was increased from 95.2 Ma to 97.3 Ma. This is the highest national corn yield on record and the second greatest planted area since 1936. For 2025 soybeans, yield was raised from 52.5 bu/ac to 53.6 bu/ac and area planted was decreased from 83.4 Ma to 80.9 Ma. This would also be the highest national soybean yield on record, but the second-lowest planted area since 2013. The larger corn yield and planted area see ending stocks balloon past two billion bushels. While for soybeans, despite the reduced area, the US soybean balance sheet remains heavy following the absence of Chinese demand.

US ending stocks for August (Mbu)

Source: Kpler Insight

- The US and China trade agreement, which was due to elapse and return to higher tariff rates on 12 August, has been extended by a further 90 days. However, the current tariff rates in effect are already pricing US agricultural commodities out of competitiveness due ample availability in South America. Furthermore, US trade officials are not expected to meet with their Chinese counterparts until the next two or three months, potentially delaying the opportunity the US has to sell soybeans or corn to China.

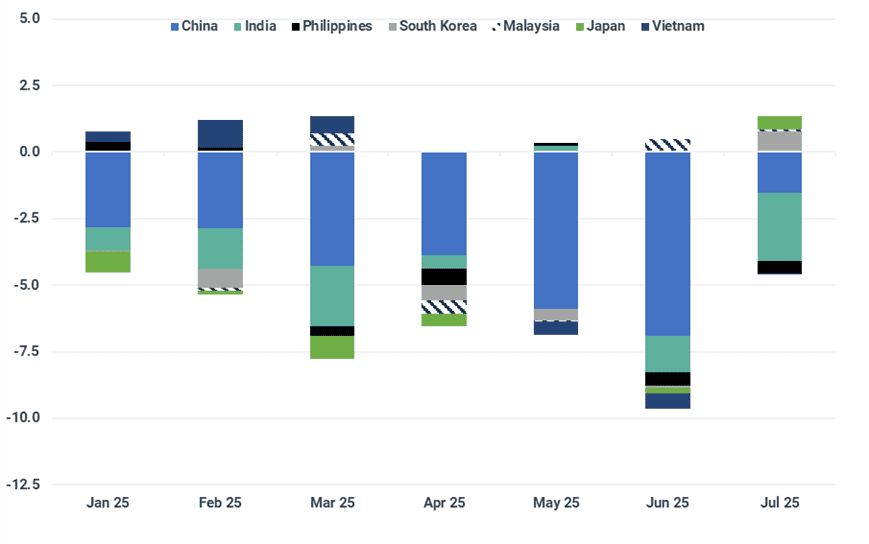

- China announced that it would impose a preliminary anti-dumping duty of 75.8% on Canadian rapeseed imports effective 14 August. This announcement comes following China’s decision in March to impose a 100% tariff on Canadian rapeseed meal and oil. Not only does China account for a large share of Canadian exports, but Canada is the largest origin of Chinese rapeseed imports. In July, China was in discussion with Australia regarding five trial cargoes of rapeseed which could see Australian exports to China return if the trial cargoes are agreed and are successful.

Rapeseed trade volumes (Mt)

Source: GTT

- Russian wheat exports for August are expected to rise m/m after a sluggish start in July. Drought conditions in the south and wet conditions in the north saw the supply of Russian wheat fall below expectations as harvest began. By 8 August, 52% of the Russian wheat crop was harvested, behind the five-year average of 62% for the same period. For Ukraine, exports are yet to show a notable sign of improvement as August’s volume is currently in line with July. Ukraine is also experiencing a poor harvest and rains in the north are worsening crop quality. By 7 August, 74% of the wheat crop had been harvested with an average yield of 4.0 t/ha, lower than last year’s 4.4 t/ha.

- EU imports of Brazilian corn is expected to surge in August following a drop in demand as Ukrainian corn stocks neared exhaustion and the uncertainty of trade policy between the EU and US made imports of US agricultural goods less attractive. Across the EU, some of the corn crops are experiencing stressful conditions due to hot and dry conditions, leading to yield concerns. Rainfall across the northern region of Ukraine will be beneficial for the development of the corn crop; however, the current EU tariff on Ukrainian corn significantly limits imports.

- Seasonally, Chinese soybean imports would usually drop lower in September as it prepares for the supply of US soybeans and Brazil’s exportable surplus nears depletion. However, with no US soybeans on the books and a record Brazilian soybean crop, Chinese imports of South American soybeans remain notably above the historical trend. Also, the lower soybean export tax in Argentina has continued to release more soybeans from the country, boosting the lineup for Chinese soybean deliveries in September.

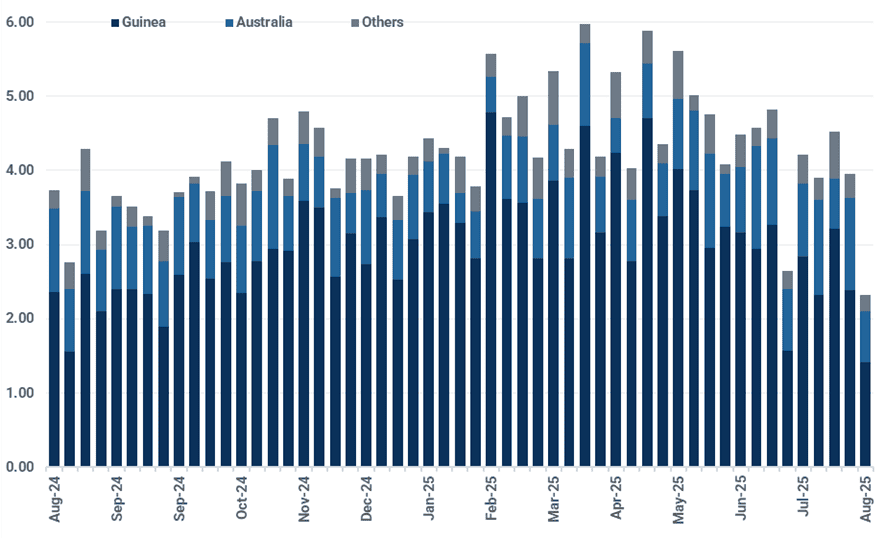

Minor bulks: Guinean bauxite exports slide as wet season disruption peaks

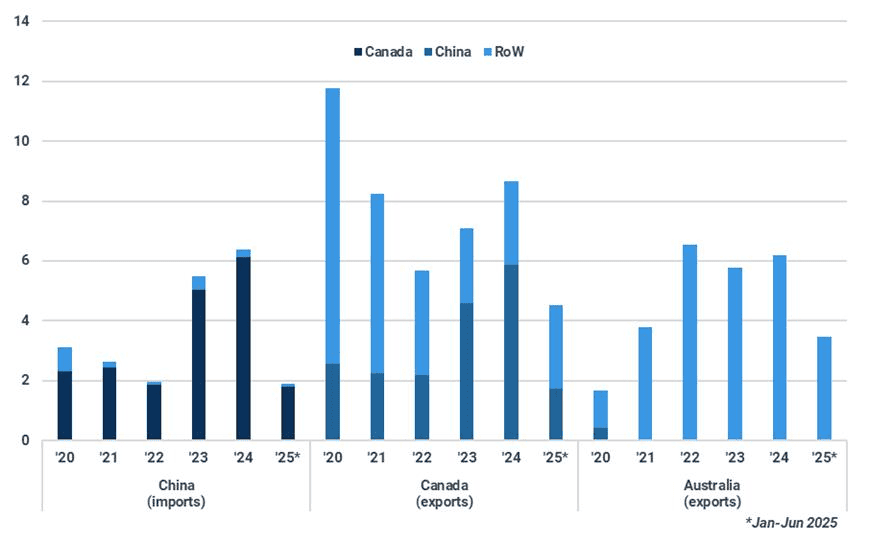

- Guinean seaborne bauxite exports hit a 21-month low of 1.42 Mt in the week ending 10 August, as torrential rains and widespread flooding across the country severely impacted mining and logistical operations. Given seasonal patterns, August will likely see the worst of this year’s rainy season disruption, with a tentative rebound in shipments expected from September onward. Meanwhile, Guinea alumina exports have remained halted since May as strikes and protests against Rusal’s Fria refinery continue.

- Rio Tinto has commenced work in Australia on the Norman Creek access project at the Amrun bauxite mine on Queensland’s Cape York Peninsula. With the first production targeted in 2027 and full construction to be completed in 2028, the project will enable mining of the Norman Creek region of Amrun, which holds approximately half of the currently declared Amrun Ore Reserves of 978 Mt. Rio Tinto announced early works and a final feasibility study on the Kangwinan project (capacity: 20 Mtpa) in May this year, a project that is intended to replace output from the retiring Andoom and the Gove mine at the end of this decade.

- Alumina prices have been volatile over the past week. The most active SHFE contract, January 2026, reached a two-week high on 12 August before retreating, ultimately closing flat w/w at 3,240 yuan/t ($451.23/t) on 14 August. Despite concerns over weather-related supply disruptions in Guinea, high alumina stockpiles in China and new capacity additions across Asia continue to fuel oversupply pressures.

Global seaborne bauxite exports (Mt)

Source: Kpler

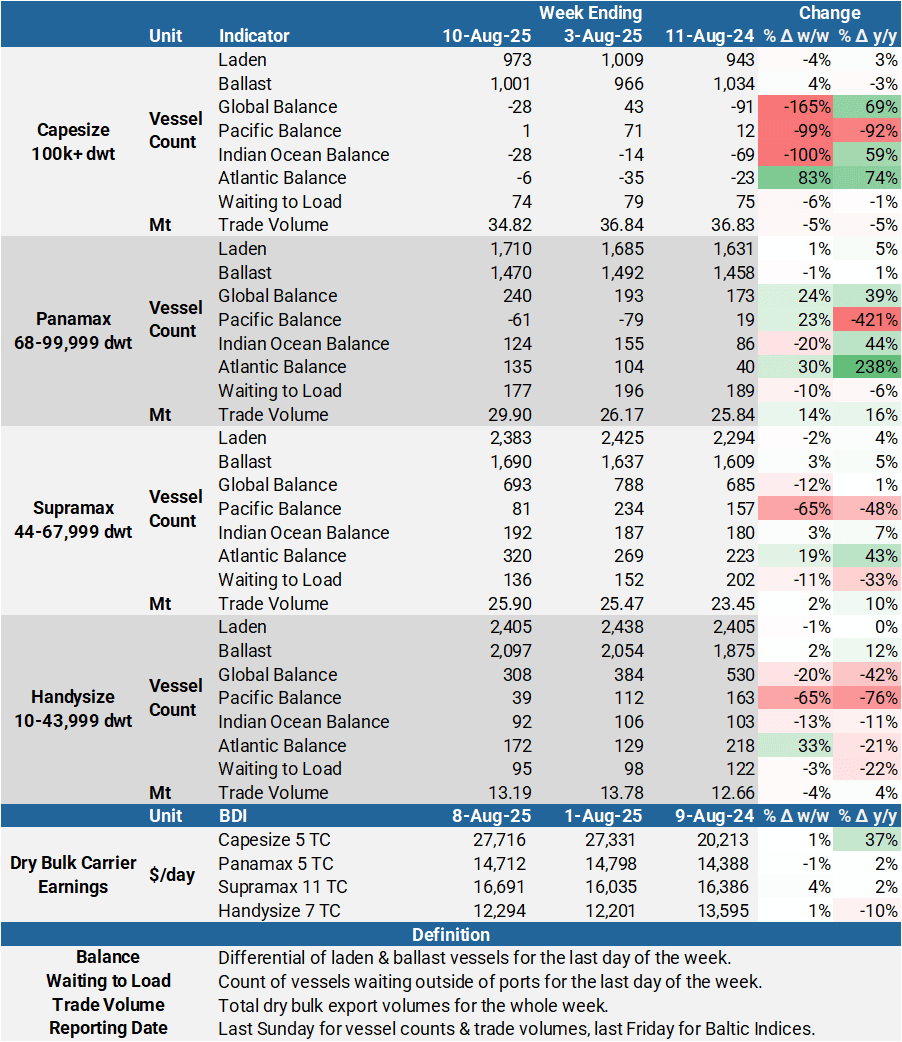

Dry bulk freight: Atlantic demand lifts Capesize market, while Panamax slides

- The Capesize 5 TC average climbed by $828/day w/w to $27,404/day on stronger Brazilian iron ore chartering. The China-Brazil round-voyage rates jumped by $2,030/day w/w to an eight-week high of $25,985/day, lifting the overall index. By contrast, the Atlantic round-voyage retreated, although it remains at a premium to the Pacific equivalent.

- A surge in iron ore cargoes discharged in China in the week ending 10 August, following weather disruption to shipping, caused a spike in Capesize ballast tonnage in the Asia-Pacific region. This will pressure rates, but the firm Brazilian market should encourage some ballasters out of the basin.

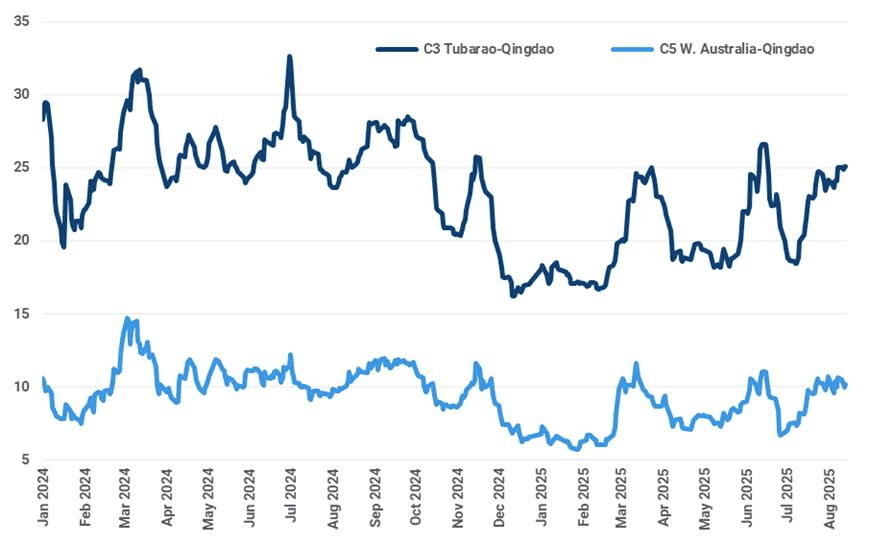

- Brazilian iron ore export strength was seen in the Brazil-China iron ore spot voyage rates (C3), which rose by $1.03/t w/w to $25.10/t, despite a sharp decline in bunker prices. July’s export performance and strong lineups at Brazil iron ore loadports for August mean the Capesize earnings outlook remains firm.

- Weakness in the Atlantic basin led to a softer Panamax market. The drop in the 5 TC average (down by $420/day w/w to $14,425/day) was due to a correction in the Atlantic round-voyage rates (down by $1,454/day w/w to $15,023/day), although it looks to have found a floor. The Pacific Panamax market was supported by higher Indonesian coal exports.

- The Supramax 11 TC average earnings increased by $457/day w/w to $16,887/day. Seasonal Chinese seaborne coal demand supported the Supramax market and lifted the Indonesia-S.China round-voyage rates to a YTD high of $14,950/day, up by $239/day w/w.

- Indian coal imports by Supramax vessels jumped by 0.27 Mt w/w to 0.84 Mt during the week to 10 August, supporting the BSI S8 Indonesia-East CoastIndia rate (up by $554/day w/w to $18,492/day). An Indonesia-India voyage is attractive for Supramax owners as it begins the process of repositioning to the higher earning Atlantic market. At $20,415/day, an implied Supramax Atlantic round-voyage (average of S4A and S4B) is at a premium of $5,579/day to the Pacific equivalent.

- The Handysize 7 TC average earnings rose by $279/day w/w to $12,512/day, supported by seasonal demand for Indonesian coal exports.

Brazil-China iron ore spot voyage rates rose w/w despite a decline in bunker prices ($/t)

Source: Baltic Exchange

Key dry bulk market developments

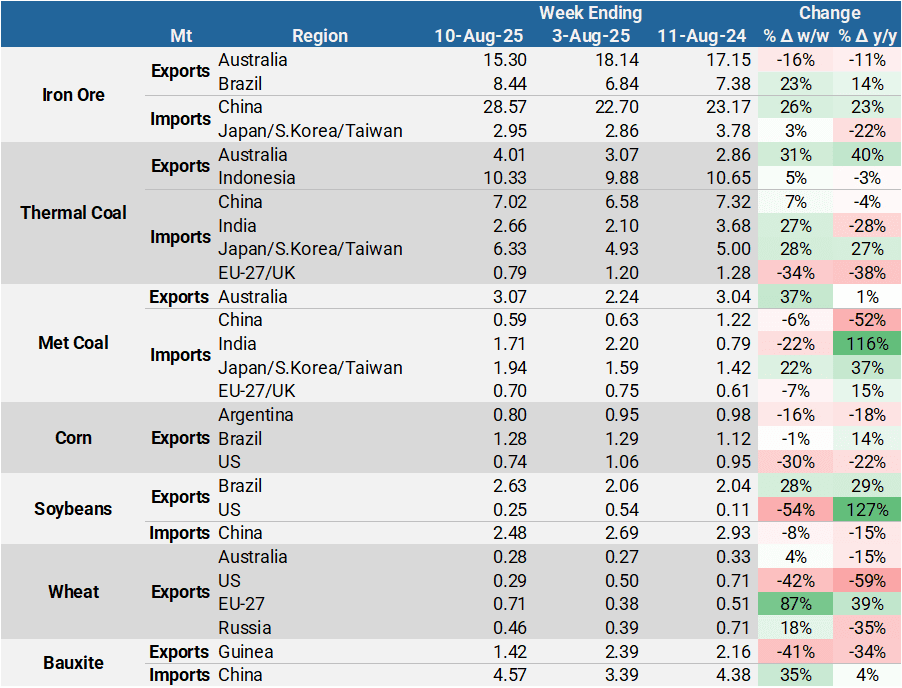

Dry bulk commodity flows

Source: Kpler

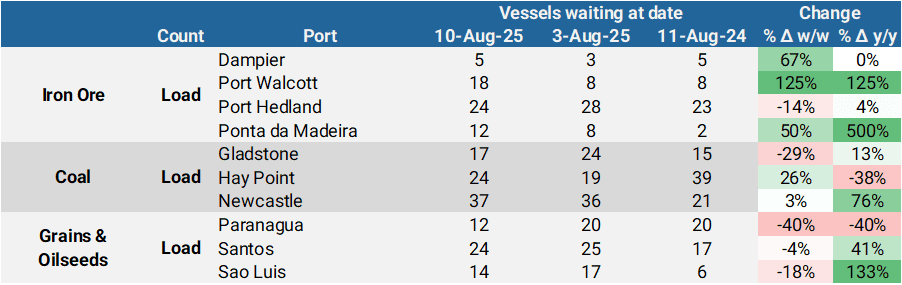

Dry bulk port congestion

Source: Kpler

Dy bulk freight metrics

Source: Kpler, Baltic Exchange

New dry bulk insights

Gain instant clarity on dry bulk flows, rates and fundamentals with real-time AIS tracking and proprietary supply- demand models. Seasoned analysts deliver concise reports and live briefings spotting emerging trends and market imbalances. Navigate shifts with precision and confidence.

See why the most successful traders and shipping experts use Kpler

Request a demo

Gain clarity on dry bulk flows, rates & fundamentals to navigate market shifts precisely

Request access