Chinese oil demand weakness masked by petrochemical feedstock growth

360kbd oil demand growth in 2026 in China is exclusively petrochemical-led, as new capacity ramps up. Transport fuels continue to contract, weighed down by accelerating electrification in the passenger car segment and alternative fuels in the heavy-duty fleet.

Key Takeaways:

- Petrochemical feedstock demand, i.e. ethane, LPG and naphtha, will grow by 410kbd in 2026, supported by growing propylene and ethylene production capacity. China’s push to reduce import dependency could hint at further additions, hence a decline in the petchem feedstock demand is nowhere near the horizon this decade.

- Rising EV penetration continues to erode gasoline demand, which is projected to fall by 33kbd in 2026. Despite moderating battery electric vehicle (BEV) sales growth (14% in 2026 vs. 31% in 2025), the expanding EV fleet is set to displace 540kbd of gasoline demand in 2026.

- The rollout of LNG and electric HDVs is set to slow in 2026 following the halving of the purchase tax exemption, but diesel displacement remains material at 500kbd this year.

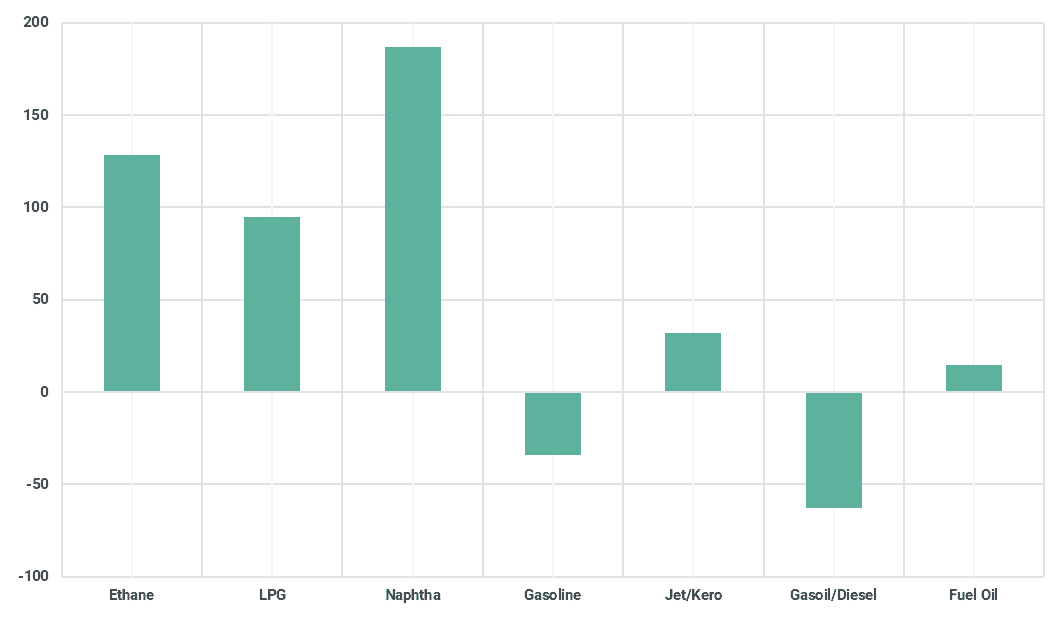

China’s total liquids demand is projected to rise by approximately 360kbd in 2026 y/y, a headline figure that, at first glance, echoes the robust growth rates observed in the previous decade. However, this aggregate increase masks a weakening underlying demand profile, particularly for transport fuels. Incremental growth is entirely concentrated in petrochemical feedstocks, specifically ethane, LPG, and naphtha, with core refined products in a declining phase overall. Ethane alone is expected to add 128kbd of demand next year, while LPG and naphtha demand are projected to increase by 94kbd and 180kbd, respectively. In aggregate, petrochemical feedstocks are forecast to contribute 410kbd of incremental demand in 2026, more than offsetting the 50kbd contraction across core refined products.

China 2026 liquids y/y demand growth by product (kbd)

Source: Kpler

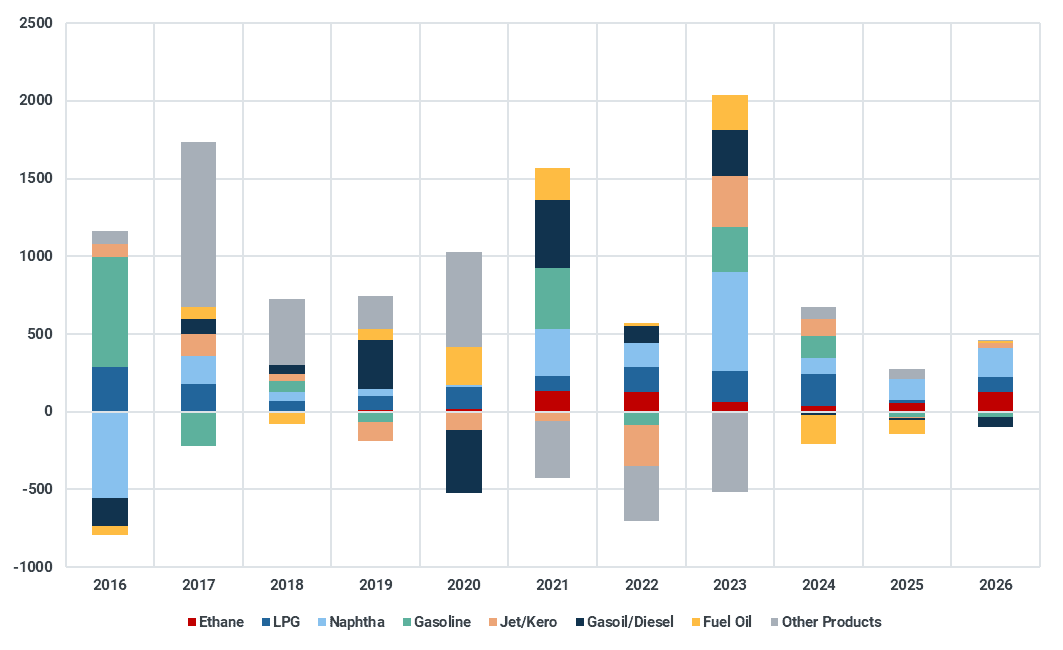

China liquids demand growth by product (kbd)

Source: Kpler

Petrochemical feedstock demand growth is being driven by China’s continued strategic push to substitute base chemical imports and expand downstream export capacity, particularly into non-US markets. This policy thrust is clearly reflected in trade flows. Over January–November 2025, polypropylene imports declined by 11% year-on-year, while exports surged by 27%, resulting in China becoming a net polypropylene exporter for the first time this year, according to Chinese Customs Statistics.

China polypropylene trade balance (kt)

Source: Kpler

A similar trend is evident in polyethylene trade flows. During January–November 2025, polyethylene imports declined by 42% y/y, while exports increased by 20% over the same period. Despite this sharp import substitution, China remains a net polyethylene importer, with the trade deficit still estimated at $8 billion, underscoring the structural gap in domestic supply.

In the olefins complex, China also continues to rely on net imports, notwithstanding the aggressive expansion of base chemical capacity. Propylene and ethylene imports increased by 10% and 32.3% y/y, respectively, over the first eleven months of 2025. These sizable import gains reflect not a lack of investment, but rather the pace of downstream capacity additions and sustained feedstock demand growth.

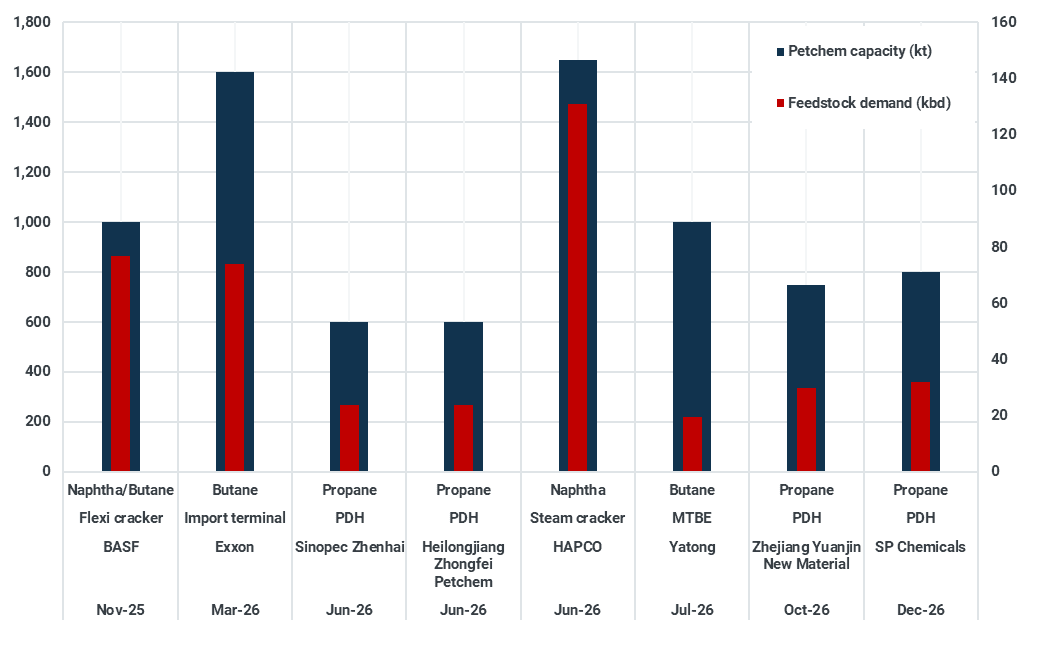

Throughout 2026, China is expected to add three PDH plants totaling 2mt are due to start up while SP Chemical’s 800kt unit commissioning could shift to Q1-2027 or further until operations become profitable. Further, BASF’s 1mt butane cracker and 1mt of MTBE plant are also scheduled to come online will lift butane demand. Ethane demand will be supported by Wanhua Chemical’s retrofit of its No.1 cracker in Yantai, converting feedstock from propane to ethane. Additionally, Sinopec/Ineos flexi-cracker (1.2mt) will increase ethane feed as the import terminal was commissioned in December 2025. Additionally, BASF flexi cracker (1mt) commissioned in late 2025 will ramp up during 2026 while HAPCO’s 1.65mt cracker will start operations in the middle of this year. While HAPCO is a refinery integrated cracker, naphtha demand will find support from BASF's flexi cracker and three paraxylene complexes with 6.5mt capacity set to come online in Q4-2026. As China continues to pursue greater self-sufficiency in strategic base chemicals and primary polymer grades, particularly polyethylene, given its persistent trade deficit, further capacity additions through 2030 appear highly likely.

China 2026 petrochemical capacity addition and feedstock requirements (kt)

Source: Argus, company reports, public news outlets

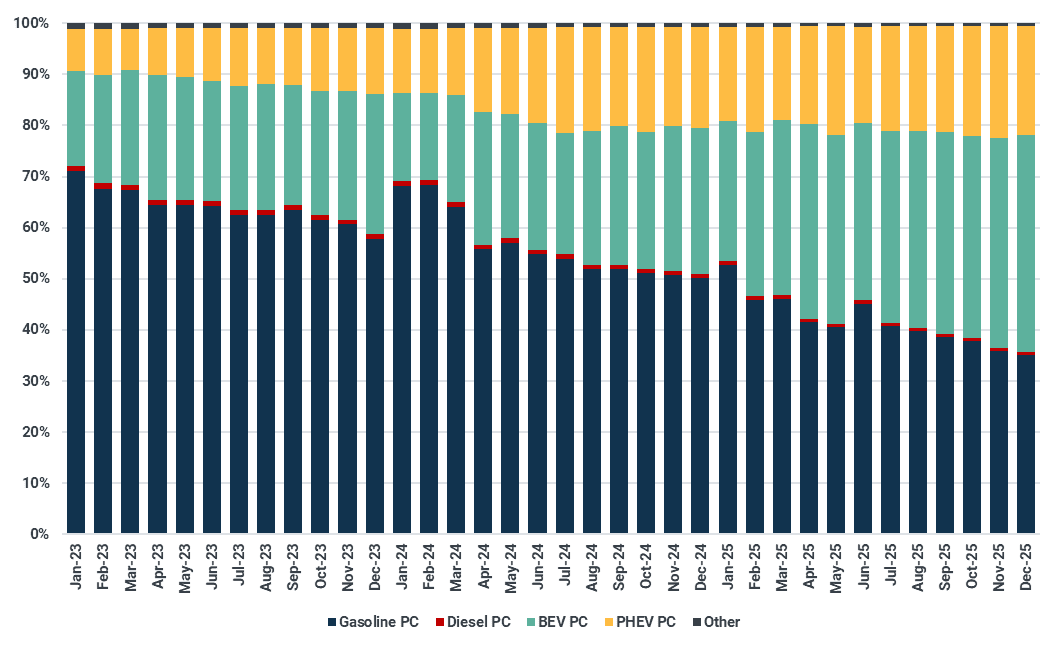

Road fuel demand in China has entered a structural decline, driven by the accelerating transformation of both the passenger vehicle and heavy-duty fleets. In 2025, electric vehicles, including battery electric vehicles (BEVs) and plug-in hybrid vehicles (PHEVs) accounted for 57% of new passenger car sales. Our analysis indicates that BEV sales growth will moderate to around 14% in 2026 y/y, following an estimated 31% increase in 2025 thanks to sweeping subsidies, while PHEV sales growth is expected to stabilize at approximately 2% after dropping 0.3% in 2025.

From a fleet perspective, BEVs are projected to represent around 13% of China’s total passenger car parc in 2026, with PHEVs making up a further 6%. As a result, gasoline displacement from the EV fleet is forecast to reach approximately 540kbd in 2026, up 25% y/y from an estimated 430kbd in 2025. Reflecting this displacement, we forecast a further 34kbd decline in China’s gasoline demand in 2026, following a 32kbd contraction in 2025.

China Monthly Car Sales by Powertrain share (%)

Source: China Association of Automotive Manufacturers (CAAM), Kpler

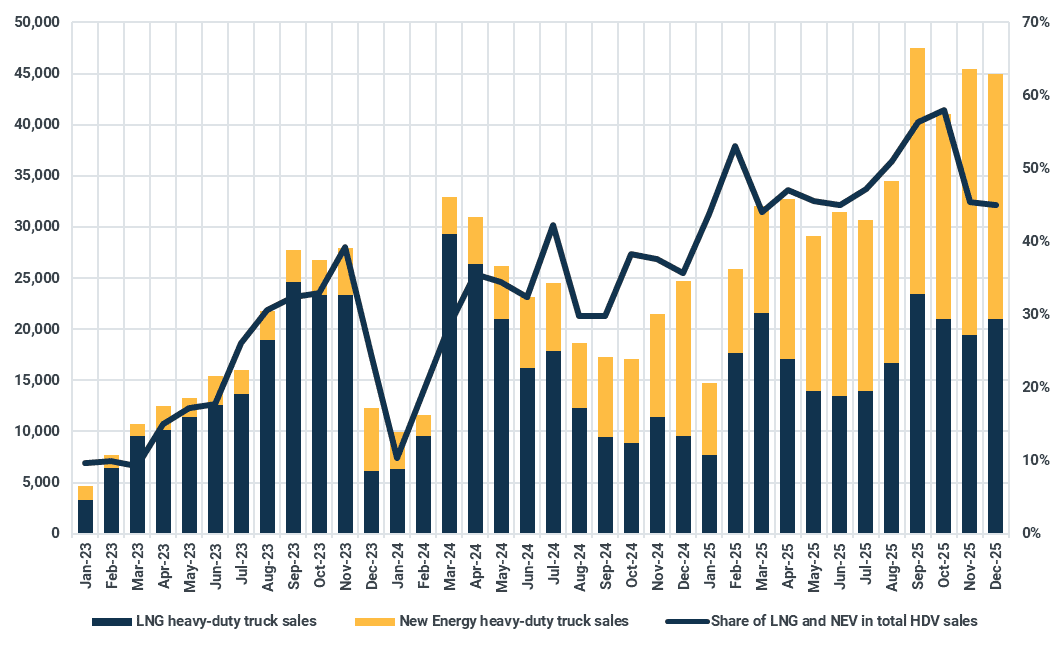

The transformation of China’s heavy-duty vehicle (HDV) fleet, historically almost entirely diesel-powered and accounting for the bulk of the domestic diesel demand, is now exerting structural downward pressure on diesel consumption. While highway freight activity remained resilient, with freight ton-kilometers expanding by 3.7% year-on-year during January–November 2025, our implied demand model indicates a modest contraction in diesel demand of approximately 0.3% (15kbd) over the same period. Looking ahead, we expect freight activity to continue growing at similar rates; nevertheless, gasoil/diesel demand is forecast to decline by a further 63kbd in 2026, reflecting ongoing fleet substitution.

The transition of the HDV fleet has accelerated since 2023, underpinned by generous subsidies and increasingly stringent transport emissions policies. The initial phase of displacement was driven primarily by the rapid uptake of LNG-fueled trucks, which materially reshaped the fleet mix from 2023 onward. More recently, however, policy support for new energy vehicles (NEVs) has enabled electric heavy-duty trucks to gain substantial traction. In 2025, electric HDV sales caught up with and surpassed LNG truck sales, recording a 170% y/y surge. Combined, electric and LNG trucks accounted for nearly half of total HDV sales last year.

Momentum is expected to moderate in 2026 following the halving of the purchase tax exemption for all NEVs, effective January 2026–December 2027, with the maximum per-vehicle exemption capped at RMB 15,000. This policy adjustment prompted a front-loading of purchases in late 2025, temporarily inflating sales volumes. Against this backdrop, our projections point to 12% growth in electric HDV sales and a more modest 4% increase in LNG-powered HDVs in 2026. In terms of fuel demand impact, the combined penetration of electric and LNG heavy-duty trucks is expected to displace approximately 500kbd of diesel demand in 2026, following an estimated 400kbd displacement in 2025, reinforcing the relatively bearish outlook for China’s gasoil demand despite continued growth in freight activity.

Share of LNG and NEV heavy-duty truck sales (%)

Source: CVWorld, Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler