September 3, 2025

Iron ore and coal markets watch production curbs linked to China’s Victory Day parade

Iron Ore & Steel: Beijing’s new steel blueprint sparks more questions than answers

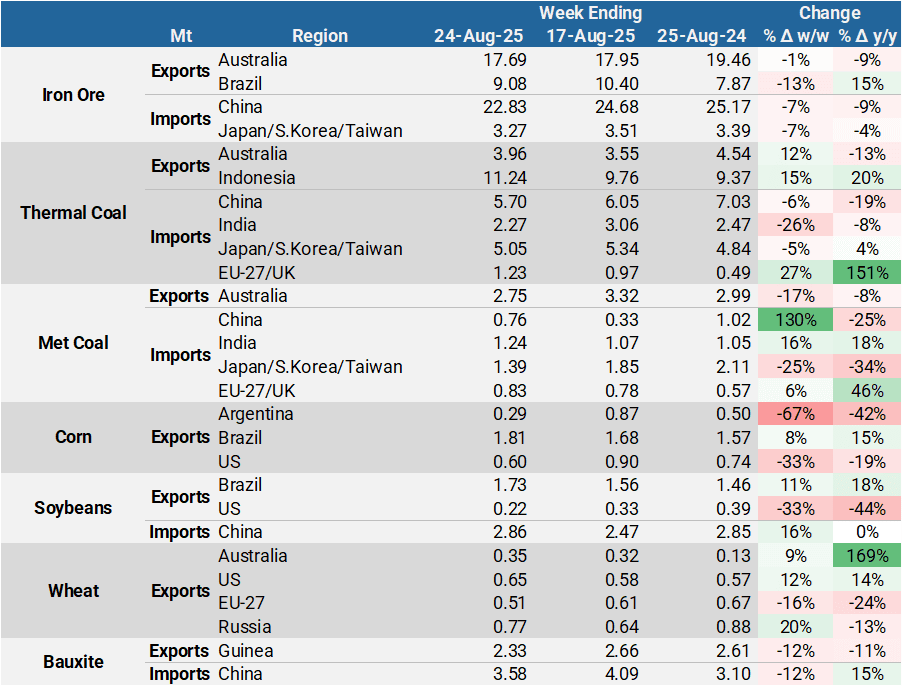

- Global seaborne iron ore exports totalled 32.30 Mt in the week ending 24 August, pulling back from the previous week’s 13-month high and falling below the five-year seasonal average of 33.70 Mt. BHP’s exports from Nelson Point slumped by more than half w/w to just 1.29 Mt, their lowest since February, amid what appears to be maintenance works. Conversely, FMG saw shipments from Anderson Point rise to a four-week high of 3.84 Mt, signalling the end of its seasonal maintenance.

- On the demand side, Chinese seaborne iron ore imports declined to 22.80 Mt last week, continuing to retreat from early August’s weather backlog-driven peak of over 28 Mt. Meanwhile, daily average crude steel output by CISA member mills rose 6.10% y/y to 2.12 Mt during the 10 days from 11 to 20 August, aiming to frontload output ahead of stricter environmental curbs linked to the 3 September Victory Day parade.

- Beijing’s policy stance added to market intrigue following the release of a planning document titled Work Plan for Stabilising Growth in the Steel Industry 2025–2026 on 28 August. Jointly drafted by five ministries, the plan targets annual growth of 4% in the steel industry’s value-added, improved supply-demand alignment, and structural optimisation. While it references long-standing production cut policies, it stops short of specifying reduction targets or introducing new curbs. Following the disclosure of the document, the DCE iron ore price increased by 1.74% on 28 August, while the SHFE rebar and HRC only edged up by 0.55% and 0.78%, respectively. The larger increase in iron ore prices may be a reaction to signs of hesitation in Beijing about imposing steel production cuts.

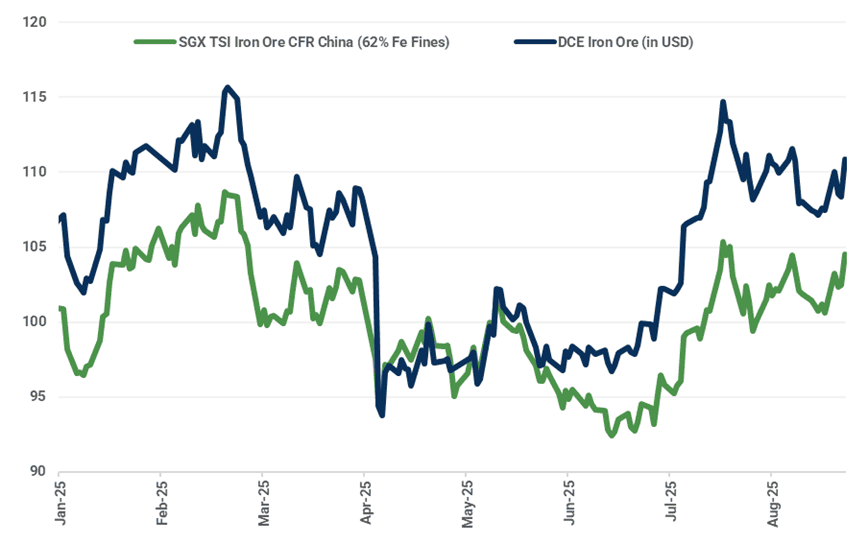

- Iron ore prices continued their sentiment-driven rally last week, mirroring similar gains in July. Optimism was fuelled by several factors: the temporary halt of Rio Tinto’s operations at Simandou in Guinea following a fatality, hopes of increased Chinese steel production after the military parade, and a policy document for the Chinese steel industry that left room for positive interpretations rather than signalling production constraints. Nevertheless, market fundamentals remain anchored in oversupply, and these developments are unlikely to alter the near-term balance significantly. The most-traded iron ore contract on DCE, January 2026, rose 2.33% w/w to a two-week high of 790.50 yuan/t (110.86/t) on 28 August. On the SGX, the TSI 62% Fe second-month contract increased by 3.29% w/w to $104.50/t at the time of writing.

Daily DCE and SGX iron ore prices ($/t)

Source: SGX, DCE, Kpler Insight

Coal: Taiwan votes against nuclear restart in referendum

- Taiwan’s referendum to restart the 1.9GW Maanshan nuclear plant failed to meet the legal threshold, despite majority support. Although generation economics favour coal over gas, Taiwan will rely more on gas to offset the loss of nuclear power in line with its coal phase-out agenda.

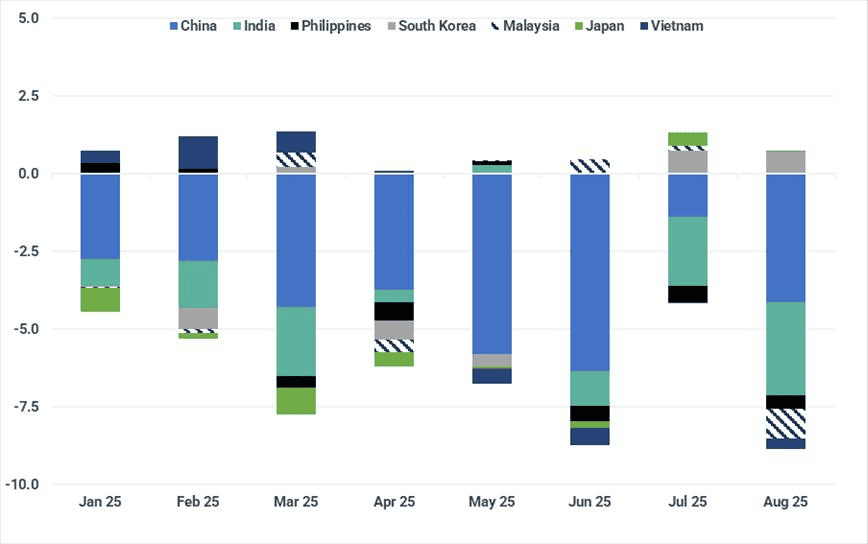

- Indonesia’s energy ministry (ESDM) has eased pricing rules for coal sales by scrapping the requirement to use benchmark prices as the minimum selling price. Under the new decree, sales can occur below benchmark levels, but royalties and tax calculations will continue to be based on the benchmark price.

Indonesia coal exports by destination (Mt)

Source: Kpler

- Chinese thermal coal markets stabilised after steady gains as summer demand peaked. The NAR 5,500 kcal/kg coal price at Qinhuangdao port fell below 700 yuan/t, retreating from multi-month highs. Power plant inventories are covered for 14-15 days of coal usage, reducing immediate procurement needs as air-conditioning demand declined after the end of heatwaves.

- Military parade preparations drove production curbs across northern China from August 20. Coke producers in Shandong, Hebei, and Henan reduced capacity by 30-40%, while steel mills cut output by 20-40%. Metallurgical coke producers secured a seventh price increase, bringing cumulative gains to 350-385/t since mid-July. Steel mills are resisting further hikes as finished steel prices softened and inventories rose.

- Australian coking coal prices continued upward momentum, as weather disruptions weighed on production in recent months. However, Chinese domestic coking coal maintains its cost advantage, limiting demand for imported Australian material despite the quality premium.

- European thermal coal markets tested cost support levels as cif ARA prices fell to mid-$90s/t. This level challenges production economics for its major suppliers, including Colombian producers. German coal generation capacity is tightening as the 1.1GW Datteln 4 coal plant will be offline for planned maintenance from August 26 to October 6.

Grains & Oilseeds: Chinese soybean imports look to rebound in October

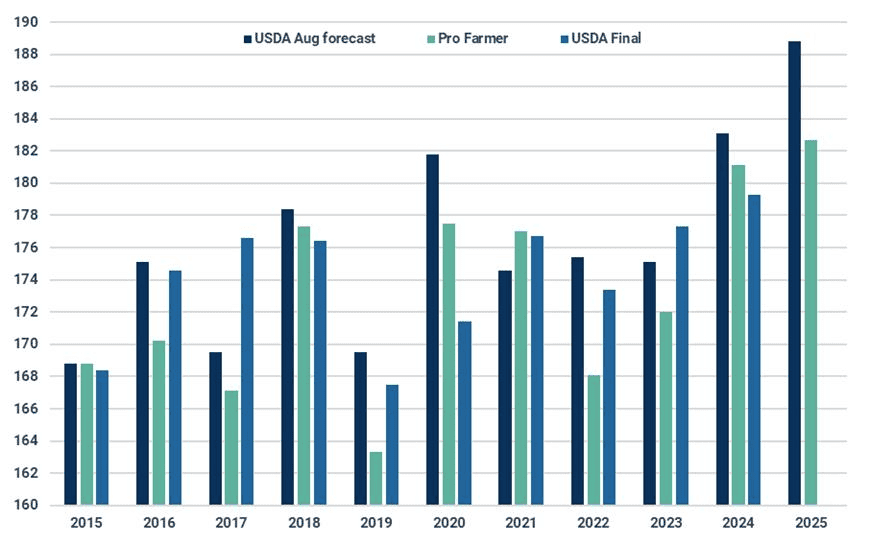

- Last week, after scouting corn and soybean production in key-producing US states, Pro Farmer estimated the national average yield for corn at 182.7 bu/ac and 53.0 bu/ac for soybeans; in comparison to the USDA’s current 188.8 bu/ac and 53.6 bu/ac for corn and soybeans, respectively. Pro Farmer yield estimates are lower than the USDA following reports of disease pressure across both the corn and soybean crops which can accelerate the maturation of the crop and result in yield penalties. There are reports of US producers conducting another fungicide application in efforts to mitigate the yield loss, however this will increase the variable cost of production and squeeze already tight margins.

Pro Farmer Crop Tour national corn yield estimate vs USDA (bu/ac)

Source: Pro Farmer, USDA

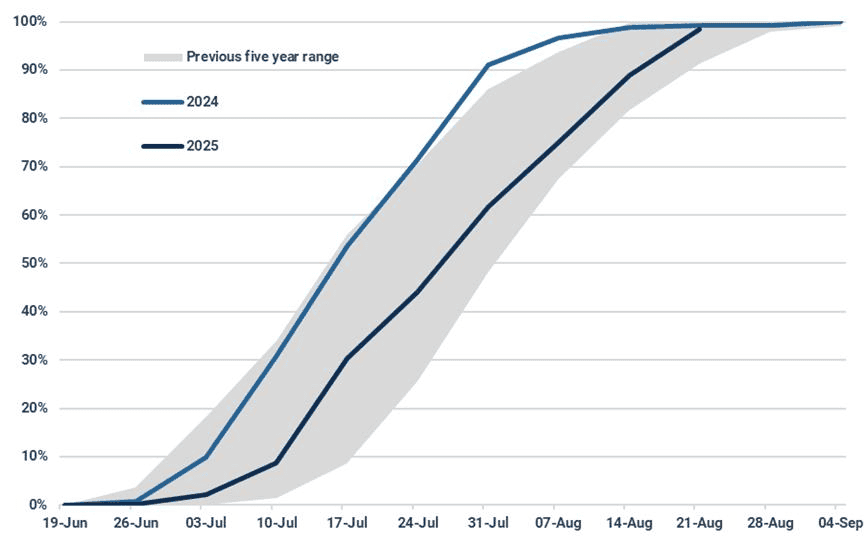

- As of 21 August, 98% of the wheat harvest in Ukraine was completed with an average yield of 4.3 t/ha, slightly below the five-year average of 4.4 t/ha as at a similar harvest completion. Following continued rains into August, there are concerns of poor crop quality in western and northern Ukraine due to a greater presence of fungal disease. As a result, this has increased the share of feed wheat produced in Ukraine for the 2025 crop. For the south and eastern areas, hot and dry conditions caused disappointing yields.

Ukrainian wheat harvest nears completion in line with seasonal average (% complete)

Source: Argus

- EU wheat exports are forecast to rise for August however, in comparison to seasonal volumes, pace still remains below average. Mixed harvest conditions and results across the EU has led to a greater share of exports from France, Romania, and Bulgaria. EU member states in the northeast have been struggling with harvest progression due to excessive rainfall which has also led to concerns regarding crop quality. In turn, this has discouraged wheat exports from these origins, such as the Baltic States, due to an uncertainty regarding the availability of milling and feed wheat.

- As the wheat harvest develops across Russia, which is approximately 60% complete nationally, greater supply of wheat from the Central and Volga districts is being received at Russian ports in the Black Sea. As a result, this is improving the availability of grain for export and is seeing Russian export values slide lower. However, the return of the tax on Russian wheat exports may slightly encourage farmer retention. Exporters also face pressure due to increased inspection at Kavkaz, which has lowered vessel availability.

- US corn exports for August have remained firm, nearing the highest volume for the month in recent years after seeing exports in June and July exceed volumes of the previous five years. However, as Brazilian corn becomes increasingly more present on the global market, US corn exports will begin to see greater competition. Brazil has been focusing on soybean exports in recent months following its record crop, which has contributed towards the delay of Brazil’s record corn crop on the market.

- Chinese soybean imports look to rebound in October, supported by increased supply from Argentina and a robust stream from Brazil. Under the current trade policy, US soybeans are 20% more expensive than the South American supply due to import tariffs. Therefore, while US soybeans continue to price lower than Argentine and Brazilian origin on the FOB market, for delivery to China, they are far more expensive. Reports highlight that some soybean crush facilities in China have South American soybeans lined-up for delivery to November, when the current US-China trade agreement is due to expire.

- Last week, Bunge announced that it was rerouting the Nordtajo from China to Vietnam. This came following concerns that the cargo may not successfully pass Chinese quality specifications. Bunge has since announced it will be sending the 30 Kt of Argentine soybean meal to China on the Kashing instead.

Minor Bulks: First Guinean alumina export in three months signals progress at Friguia

- Seaborne bauxite exports from Guinea remained subdued, totalling just 2.16 Mt in the week ending 24 August, as adverse weather conditions continued to disrupt mining and logistics operations.

- EGA’s Guinean subsidiary, GAC, announced it would complete “the orderly termination of employees and contracts with all its on-site service providers” after Friday, 22 August, due to “illegal measures” by the Guinean government to take over its operations and assets. The move formalises EGA’s full exit from Guinea, a move that’s not surprising following the state’s forced nationalisation of its mines through abrupt concession transfer earlier this month.

- In a separate development, Kpler data shows that Guinea recorded its first alumina shipment in three months, potentially signalling progress in negotiations between Rusal and workers at the Friguia refinery. A Handysize vessel, Cool Breeze, departed Conakry on 27 August carrying over 30,000 tonnes of alumina. Previously, operations at Friguia had been severely disrupted since May due to strikes and labour unrest.

- Alumina prices extended their downward trend, with the most active January 2026 contract on SHFE falling 1.95% w/w to 3,063 yuan/t ($429.55/t) on 28 August. Rising domestic inventories in China, now at a 16-month high, alongside sustained record production levels, continue to weigh on prices. Additionally, fading concerns over bauxite supply disruptions in Guinea, as the rainy season nears its late stage, have contributed to bearish sentiment in the alumina market.

Guinea’s Friguia alumina refinery resumes exports on 27 August (t)

Source: Kpler

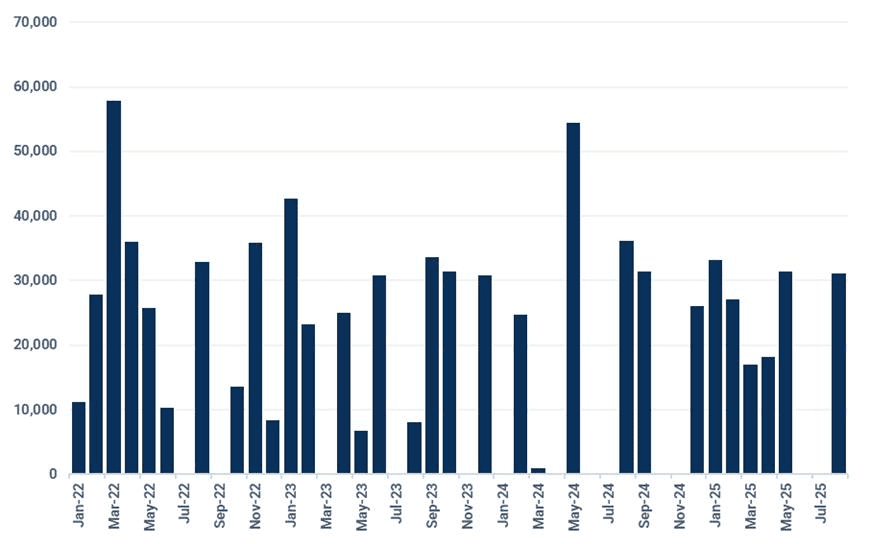

Dry Bulk Freight: Capesize earnings surged past three-year August highs on fronthaul demand

- The Capesize 5 TC average earnings climbed by $1,500/day net w/w to $23,918/day, driven by a surge in the Pacific basin. August earnings are on track to meet our expectation for the strongest month since September 2024, as Brazil’s iron ore shipments hit a seasonal peak and with Guinea’s bauxite chartering ramp-up. However, we think firmer Pacific rates (up $5,546/day w/w to $25,323/day) are down to tonnage repositioning from the Pacific basin to meet the demand in the Atlantic, where we expect a rebound in Guinean bauxite chartering to add to greater fronthaul export volumes in September.

- The Panamax market firmed further with the 5 TC average earnings rising to a multi-week high of $16,865/day (up $1,396/day w/w). Strength in Brazilian corn chartering lifted the P6 Singapore round-voyage (up $1,108/day w/w to $16,430/day) to complement the upward momentum in the North Atlantic.

- P1A (Atlantic round-voyage) and P2A (fronthaul) rose to the highest since July to $19,300/day and $26,463/day (up $2,709/day and $2,434/day w/w), respectively. US coal exports have firmed due to seasonal demand. At 1.11 Mt, coal loaded on Kamsarmax/Panamax at US Gulf and East Coast ports jumped to a 15-week high. US wheat exports are building strength and will drive short-term demand in the North Atlantic.

- The Supramax 11 TC average earnings rose to the highest level since May 2024 at $18,466/day (up $710/day w/w), with firmness in the Atlantic and Pacific basins.

- Strength in US wheat chartering and coal exports lifted rates on US Gulf routes. S1C (US Gulf-Far East) rose to $28,764/day (up $1,321/day w/w) while the S4A (US Gulf-Continent) rose to $29,857/day (up $657/day w/w). Supramax coal chartering activity in the Pacific will retreat in September, following peak Chinese summer demand for coal in August.

- Strength in US Gulf grain exports also supported the Handysize market. The HS4 (US Gulf-Continent) rose to the highest since January 2024 at $18,308/day (up $1,279/day w/w). At $13,555/day, the 7 TC average earnings rose to a one-year high on the back of Atlantic market strength, where regional Handysize loadings were up y/y in July and are on track to be higher again in August.

Capesize 5TC average in August 2025 outperforms August 2022–2024 earnings ($/day)

Source: Baltic Exchange

Key Dry Bulk Market Developments

Dry Bulk Commodity Flows

Source: Kpler

Dry Bulk Port Congestion

Source: Kpler

Dy Bulk Freight Metrics

Source: Kpler, Baltic Exchange

See why the most successful traders and shipping experts use Kpler

Request a demo

Gain clarity on dry bulk flows, rates & fundamentals to navigate market shifts precisely

Request access