US supply drops sharply, but WTI support may prove short-lived

The latest Arctic plunge disrupted US shale, currently cutting output by up to 300-400 kbd across key regions, including the Bakken, Oklahoma, and Texas (likely peaked >1.5 Mbd on Saturday). While production is already rebounding, we see US crude supply dipping below 13.7 Mbd in February, in line with our view that Q4 marked the US supply peak. Weather-related refinery outages complicate the picture, softening crude demand even as supply tightens, with an expected rebound in CPC flows increasing competition in the Med and Europe for WTI.

Key Takeaways

- Cold temperatures and severe weather have currently shut in an estimated 300-400 kbd of US shale supply across the Bakken, Oklahoma, and parts of the Permian (likely peaked above 1.5 Mbd on Saturday).

- Despite these supply outages, power outages and lower utilization rates are likely to keep regional differentials pressured.

- WTI will see additional downward pressure amid a rise in CPC flows, with SPM-3 restarting operations, lifting CPC flows to normal levels by late January.

Cold temperatures and severe weather swept across key US shale-producing regions, forcing operators to sharply curtail output. Temperatures fell well below -10℃ in the Bakken, Oklahoma, and parts of the Permian—including Midland—causing immediate freeze-offs. According to state regulators, North Dakota alone saw outages between 80–110 kbd, representing up to 10% of state output. Cumulative weather-related shut-ins are currently estimated at around 300–400 kbd nationally (likely peaked above 1.5 Mbd on Saturday), although most of this is expected to return early this week as temperatures rebound.

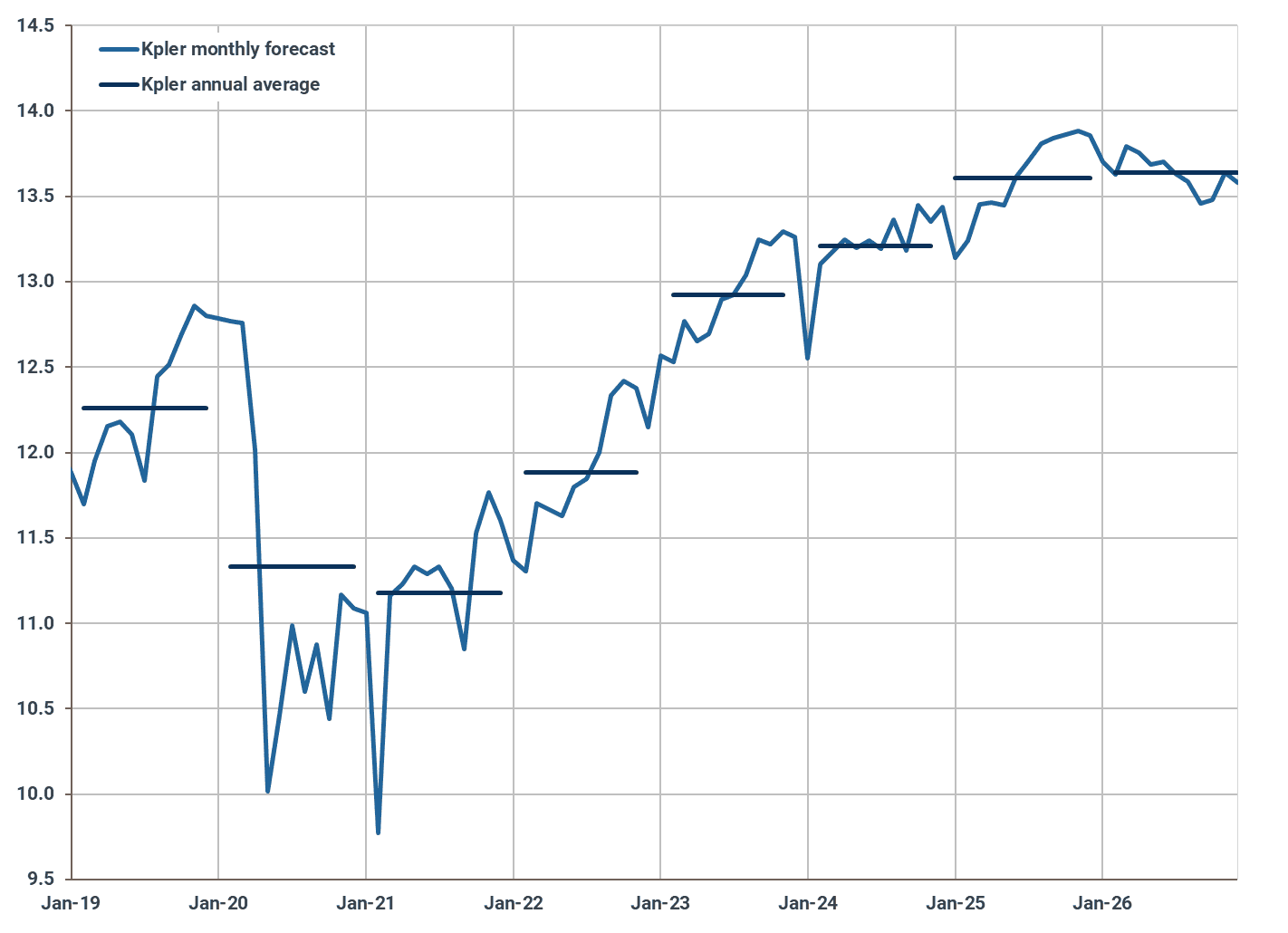

Our base case had already factored in a 150 kbd hit to output in January, bringing average US crude production to around 13.7 Mbd—down from Q4 highs of over 13.8 Mbd. We have since revised this figure downward to around 13.6 Mbd for this month and we expect supply to remain pressured into February, with production likely to remain below 13.7 Mbd as recovery lags and renewed outages remain very likely in parts of the Bakken and Permian next month. This also supports our broader view that US crude output peaked in Q4 2025. We expect structural declines and reduced activity to push domestic supply toward 13.5–13.6 Mbd by year-end.

US crude and condensate supply, Mbd

Source: Kpler

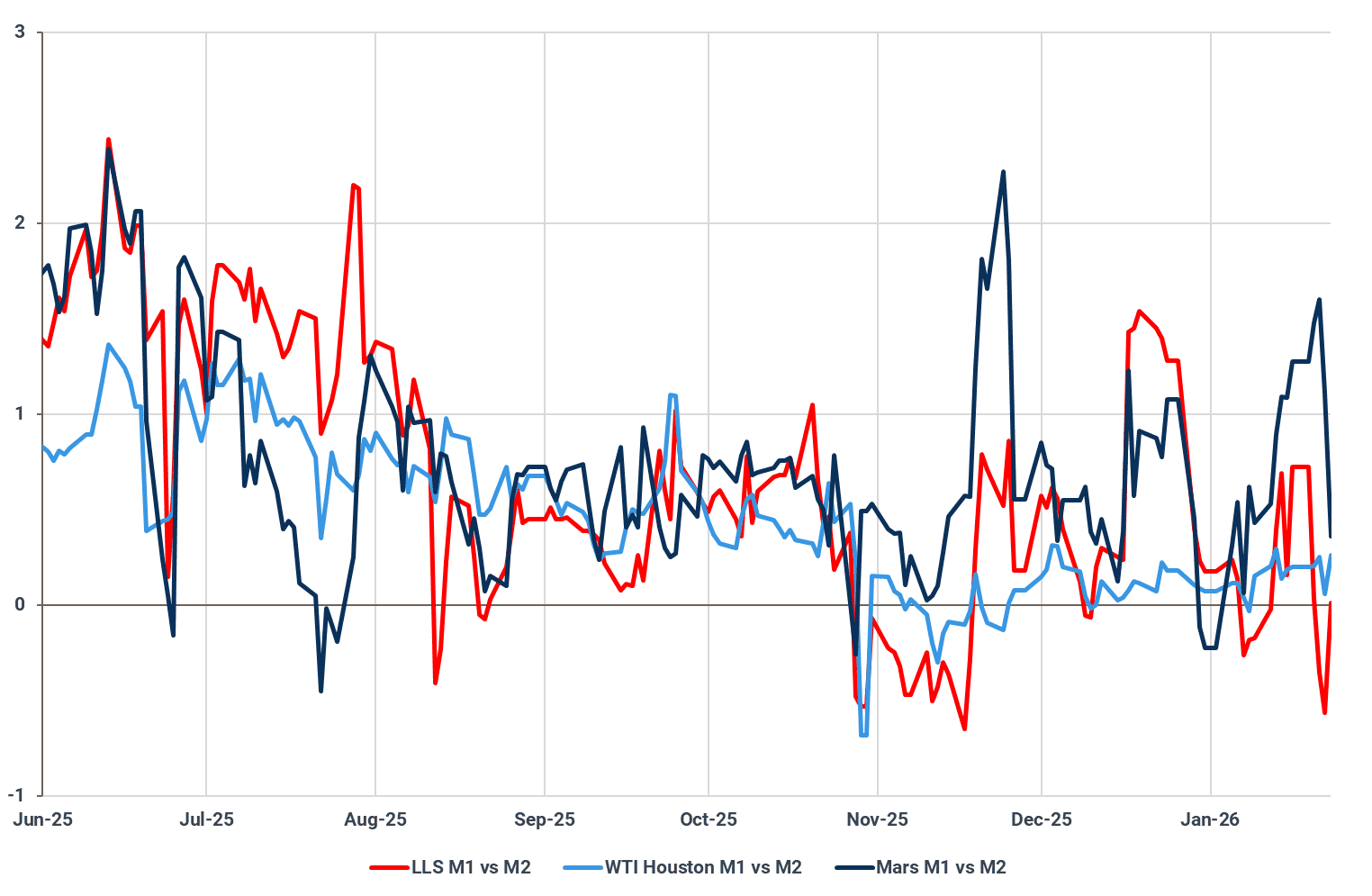

Power outages and extreme cold have also hit downstream assets as well. Power sensitivity, slower stabilisation timelines, and reliability constraints have exposed up to 1.5–2 Mbd of CDU capacity to partial disruptions. Within the core distribution hub, nearly 700 kbd of refining capacity faces elevated outage risk. This presents a two-sided dynamic for WTI: while lower crude supply offers temporary support, reduced refining demand tempers the bullish impulse. It should be stated, however, that any disruptions to US crude throughput will be felt more strongly on grades that are typically consumed domestically, such as Mars and LLS.

US Gulf M1/M2 spreads, $/bbl

Source: Argus Media

Adding to near-term volatility for WTI is the return of CPC flows. The Caspian Pipeline Consortium confirmed that offshore Mooring 3 is back online as of 25 January, in line with expectations. With Moorings 1 and 3 both operational, flows are set to rebound to normal levels by the end of the month. This restores the primary route for Kazakh crude exports and unwinds recent disruptions that had boosted WTI's competitiveness. US grades had rallied to a $3.80/bbl premium over North Sea Dated (cif Rotterdam; Argus Media), the strongest in over two years, as European refiners shifted away from constrained CPC barrels. With this arb closing, we expect WTI to soften despite recent US supply losses.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler