Which Russian commodities does the EU still import, and for how much longer?

As of November 2025, the EU still imports Russian natural gas, crude, certain LPG types, VGO, fertilizers, metals, and nuclear materials. This report outlines the remaining flows, exemptions, and phase-out timelines.

- Natural gas: Despite significant ongoing deliveries, all EU imports are scheduled to stop by the end of 2027.

- Crude: Druzhba pipeline flows into Hungary and Slovakia persist under EU exemptions with no defined end date.

- VGO: Croatia’s refinery exemption expires this year, closing the EU’s final outlet for Russian refined products.

- LPG: Remaining loopholes are closing as EU sanctions now cover all major LPG categories.

- Fertilizers: EU imports surged post-2022 but new tariffs will make them uncompetitive by 2028.

- Metals: Steel slabs and primary aluminum continue under limited quotas, but CBAM will curb inflows from 2026. Nickel faces no restrictions, but EU reliance has already declined through diversification.

- Uranium and nuclear fuel: With 19 Russian-designed reactors still in operation in the EU, imports face no restriction, though substitution of nuclear fuels is advancing.

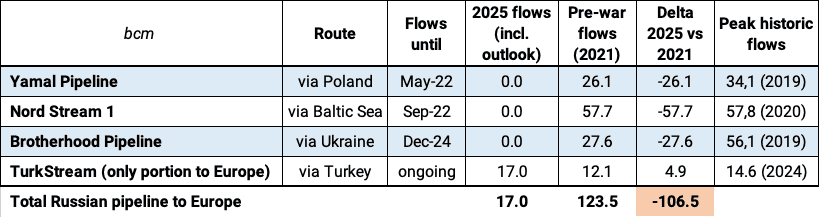

Russian natural gas: Despite significant ongoing deliveries, all EU imports are scheduled to stop by the end of 2027.

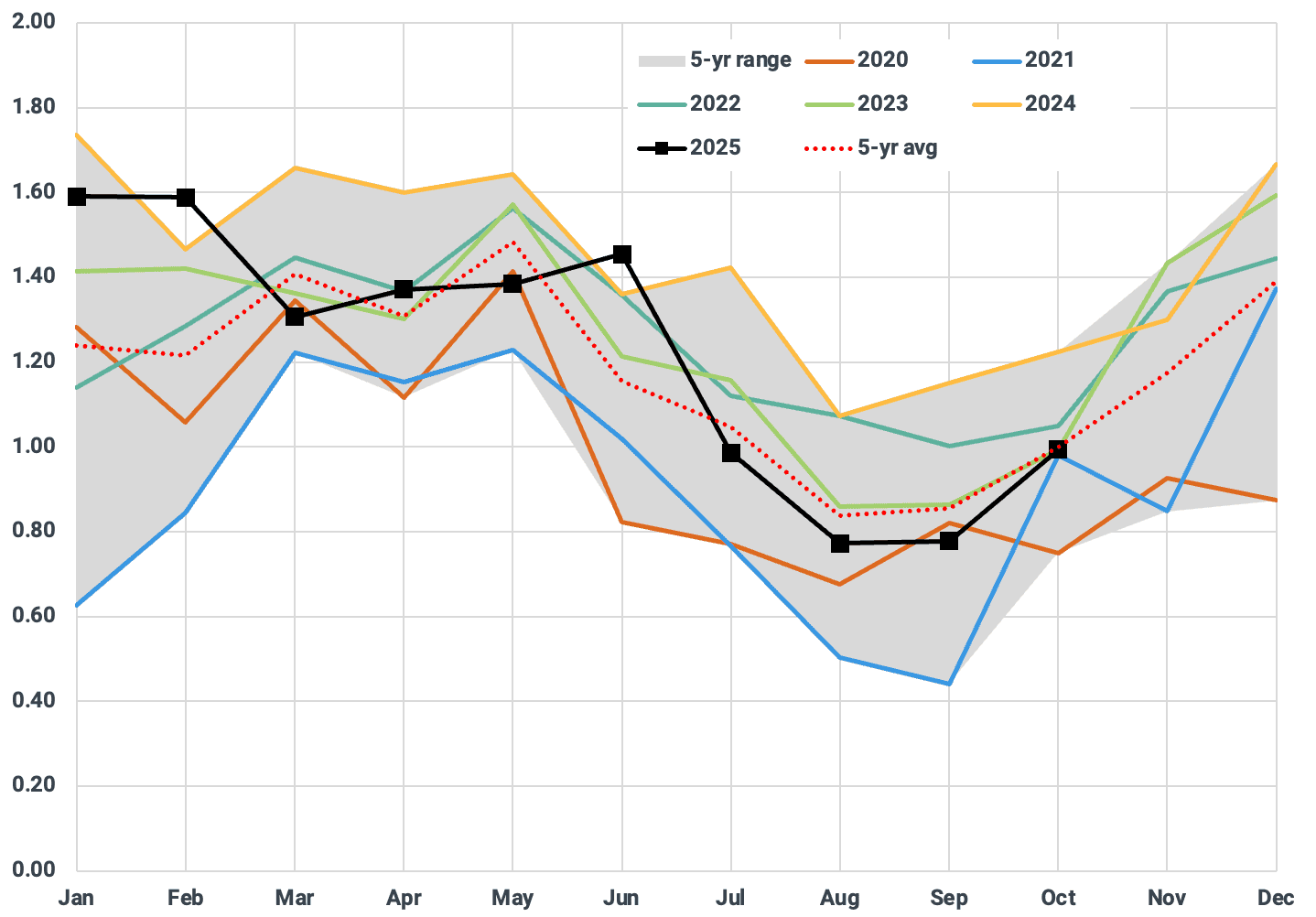

While Russia-EU flows across the three largest pipelines have already been halted (see table), inflows via TurkStream (14.6 bcm) and via LNG (17.3 Mt) both reached record highs in 2024.

In October 2025, the Council of the European Union agreed to phase out all imports of Russian gas by January 1, 2028. Short-term contracts concluded before June 17, 2025 may continue until June 17, 2026, while existing long-term contracts may run until January 1, 2028 (applying to the remaining pipeline flows via TurkStream). The same month, the timeline for Russian LNG imports has been accelerated under the EU’s 19th package of sanctions. For short-term contracts, the ban takes effect on April 25, 2026, followed by a complete ban on all Russian LNG imports from January 2027 onward. Around 12 Mtpa of Russian LNG under long-term contracts would need replacing, which could be cushioned by the nearly 40 Mtpa of new export capacity due online next year. Reliance on US LNG, which supplies around 56% of EU imports needs (2025 ytd), is set to rise further. Additionally, higher domestic EU production (Romania’s Neptune Deep project is set to come online in 2027), easing pipeline bottlenecks, and lower gas consumption should offset the impact. As a side note: in addition to Russian LNG, the ARA region continues to import gas condensate from Russia’s Yamal LNG plant (0.9 Mt across 26 cargoes in 2025 ytd).

Monthly EU LNG imports from Russia (Mt)

Source: Kpler

Russian crude: Druzhba pipeline flows into Hungary and Slovakia persist under EU exemptions with no defined end date.

The EU has banned seaborne imports of Russian crude in December 2022, and, similarly to natural gas, the EU Commission proposed a regulation that aims for a “complete stop of Russian oil imports by the end of 2027”. However, legislative carve-outs allow for Druzhba pipeline flows to two MOL refineries in Hungary and Slovakia – the only remaining channel for direct Russian crude sales to Europe - to continue. MOL argues that it needs both Druzbha and the Adriatic pipelines from Croatia to sustain intake levels at these two refineries. This EU exemption legislation has no defined end date and a halt to these flows is unlikely under Hungary’s Prime Minister Orban and Slovakia’s Prime Minister Fico, particularly following recent statements by President Trump suggesting that Hungary could retain exemptions. Reportedly, even an extension of the Druzbha pipeline to Serbia has been under consideration this year.

Russian VGO: Croatia’s refinery exemption expires this year, closing the EU’s final outlet for Russian refined products.

While the EU implemented an import ban on seaborne refined products in February 2023, Croatia’s Rijeka refinery has been granted an exemption allowing it to import Russian vacuum gas oil (VGO) until December 31, 2025, provided no other alternative supply is available. However, respective volumes have been minor (6 kbd in 2025 ytd). Despite substituting VGO volumes from Saudi Arabia and Turkey, overall EU imports of the hydrocracker and FCC feedstock have declined sharply since 2022, providing structural support to HSSR and HSFO cracks.

Russian LPG: Remaining loopholes are closing as EU sanctions now cover all major LPG categories.

The 12th EU sanctions package from 2024 excluded some types of LPG such as N-butane and iso-butane. They were seen as petrochemicals feedstocks, but wide discounts have encouraged European buyers to blend growing volumes into the autogas pool - a trend reflected in ongoing seaborne flows into Bulgaria and rail shipments into Poland (Argus Media). The latest 19th package from October 2025, however, closed that loophole, although a deadline has yet to be disclosed.

Russian fertilizers: EU imports surged post-2022 but new tariffs will make them uncompetitive by 2028.

The sharp reduction in EU natural gas imports from Russia since 2022 has weighed heavily on domestic production of nitrogen-based fertilizers which use natural gas as a main feedstock. Subsequently, the EU ramped up its buying of fertilizers not only from Russia but also from Belarus, accounting for a combined 33% of imports, with Egypt and Algeria covering most of the rest. In May 2025, the EU agreed to phase in fertilizer tariffs on Russia and Belarus, rising from €40-45/t (July 2025 to June 2026) to €315-430/t by 2028 (lower range for urea and nitrogen, higher range for NPKs and phosphates), in addition to a 6.5% imports duty. This move is set to make Russian and Belarussian volumes uncompetitive within three years. Europe will need to source additional supplies from North Africa and the Middle East, likely raising costs for farmers amid reduced competition and upcoming carbon taxes under the CBAM from 2026. Similarly, a 50% EU tariff on live animals, meat vegetables, animal fats, preparations for animal feeding and raw textiles from Russia came into effect on July 1, 2025.

Monthly EU seaborne fertilizer imports from Russia (Mt)

Source: Kpler

Russian metals: Steel slabs and primary aluminum stay under quotas, but CBAM will curb flows from 2026, while nickel remains unrestricted yet its EU share is shrinking.

The EU’s 12th sanctions package from December 2023 introduced a quota system for pig iron (0.70 Mt for 2025, 1.14 Mt for 2024), with most volumes heading to Italian steel mills. An outright import ban will be implemented from January 1, 2026. Import quotas for Russian-origin steel slabs are currently in place up until 2028, however, CBAM will pose challenges to these imports next year. Although imports of intermediate and finished aluminum were banned in December 2023, a 12-month transitional period—lasting until February 26, 2026—permits the import of up to 275 kt of primary aluminum from Russia, with an additional quota of 50 kt allowed until December 31, 2026. From 2027 onward, all imports of Russian aluminum into the EU will be prohibited. On the other hand, there are no formal restrictions on imports of Russian nickel, which is considered a “strategic raw material” in EU nomenclature (battery grade). However, the EU has diversified its sourcing, with Russia’s share of imports having dropped from 41% in Q1 2021 to 15% as of Q2 2025 (Eurostat).

Uranium and nuclear fuel: With 19 Russian-designed reactors still in operation in the EU, imports face no restriction, though substitution of nuclear fuels is advancing.

The European Commission has not imposed an EU-wide ban on Russian uranium products (uranium, enriched uranium, converted uranium, nuclear fuel), as 19 Russian-designed reactors remain operational across the bloc. Instead, it supports diversification and the development of domestic VVER-fuel capabilities. Given the complexity of nuclear supply chains, Western firms needed several years to produce compatible fuel. As of November 2025, the transition is advancing but incomplete: Bulgaria, Finland, and the Czech Republic have already loaded Westinghouse nuclear fuel assemblies into Russian reactors, while Hungary and Slovakia still rely partly on Russia’s TVEL until new Framatome and Westinghouse lines come online from 2027. With 12–18-month reload cycles, full independence is expected only late this decade. According to Eurostat, EU imports of Russian uranium and fuel products totaled over €700 million in 2024. Meanwhile, Rosatom’s power plant construction unit Atomstroyexport remains active in the EU—finalizing Slovakia’s Mochovce 4 (440 MWe) and leading Hungary’s Paks II project (2.4 GWe), where site work continues and major construction is due in 2026 despite a September 2025 EU court ruling annulling prior state-aid approval.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data