January 2, 2026

2025 Dry bulk carrier earnings lag 2024 across all classes despite strong H2 performance

Iron Ore & Steel: Iron ore shipments surge to near-record as miners accelerate year-end loadings

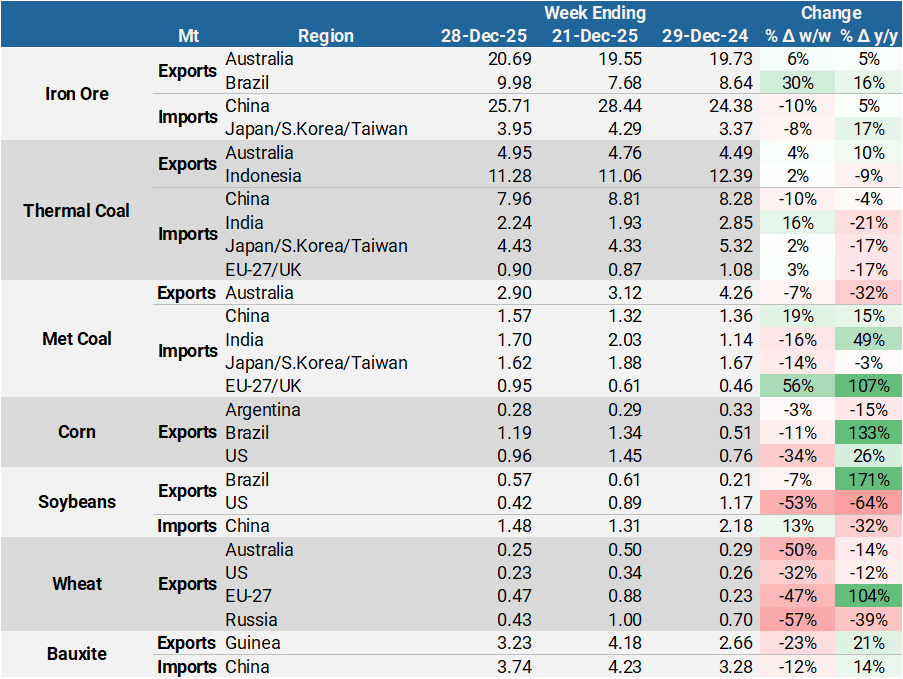

- Global seaborne iron ore exports climbed to a near-record 38.50 Mt in the week ending 28 December, as miners expedited quarter-end shipments for reporting purposes. Rio Tinto led the charge, with loadings surging to a three-year high of 7.72 Mt, while Vale’s exports from Brazil also rose to a three-month peak despite heavier seasonal rainfall.

- In Guinea, Simandou’s second cargo, carried by the Capesize vessel Great Sui, departed in late December and is scheduled to arrive in China in the second half of February. Meanwhile, the Winning Youth, carrying the inaugural shipment, is currently transiting the Indian Ocean and is expected to berth at Majishan in mid-January.

- On the demand side, Chinese seaborne iron ore imports rose 5% y/y to 25.70 Mt in the final week of 2025. With crude steel output continuing its seasonal slowdown in December, port stockpiles have surged to the highest level since February 2022. Port inventories increased by more than 18Mt in Q4 2025, an unsustainable pace as many ports are reaching near capacity. A recovery in January steel production may help to absorb some of the near-record inventories.

- Iron ore prices remained resilient through the year-end holiday season. The ongoing contract pricing dispute between BHP and China’s CMRG, along with a Brazilian court order suspending Samarco’s expansion on environmental concerns, lent support. The most-traded iron ore contract on DCE, May 2026, rebounded 4.85% from the 15 Dec low to 789.50 yuan/t on 31 December. Meanwhile, the most traded contract for 62% Fe Fines CFR China, Jan 2026, rose 3.76% to $105.35/t during the same period.

Capesize Great Sui, loaded with the second Simandou cargo, is heading to China

Source: Kpler

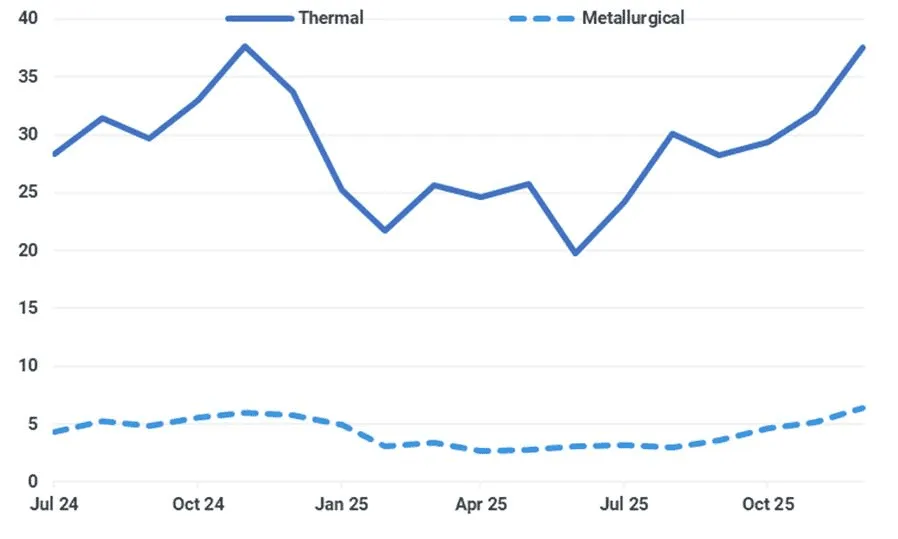

Coal: Indonesia mulls production cuts in 2026

- Indonesia will cut approved mining output under annual RKAB plans to support prices for coal and other minerals, Energy and Mineral Resources Minister Bahlil Lahadalia said. The government wants steadier prices, companies to increase revenue, and higher royalty and tax income. Bahlil gave no details on the size of any quota cuts. Indonesia is tightening control over the coal sector as it moves against companies that operate outside mining laws and permitting rules, the minister also said. Authorities describe these groups as miners that use state forest land illegally, ignore licensing requirements and bypass good mining practices. To curb illegal activity, regulators are tightening oversight through the RKAB work plan and budget system, warning hundreds of companies of sanctions for non-compliance and deploying special task forces to reassert state control over natural resources.

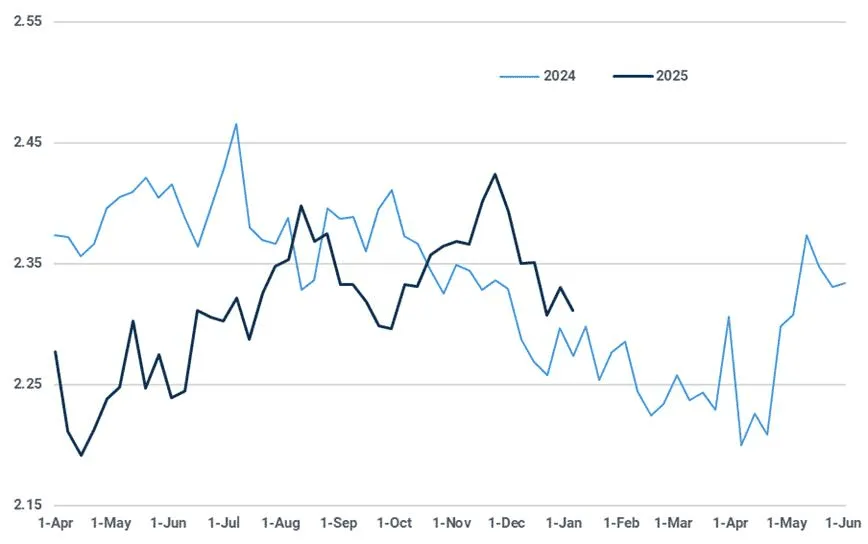

- Chinese thermal coal receipts rebounded in December, pushing thermal coal receipts to their highest level since November 2024. However, the surge in purchases has left utilities less eager to secure additional supplies, leading to a m/m price drop of $10-15/ton in southern China.

Chinese seaborne coal imports (Mt)

Source: Kpler

- India’s decision to extend safeguard duties on selected flat steel products for three years should weigh on China’s met coal demand in the coming months, which was also trending higher.

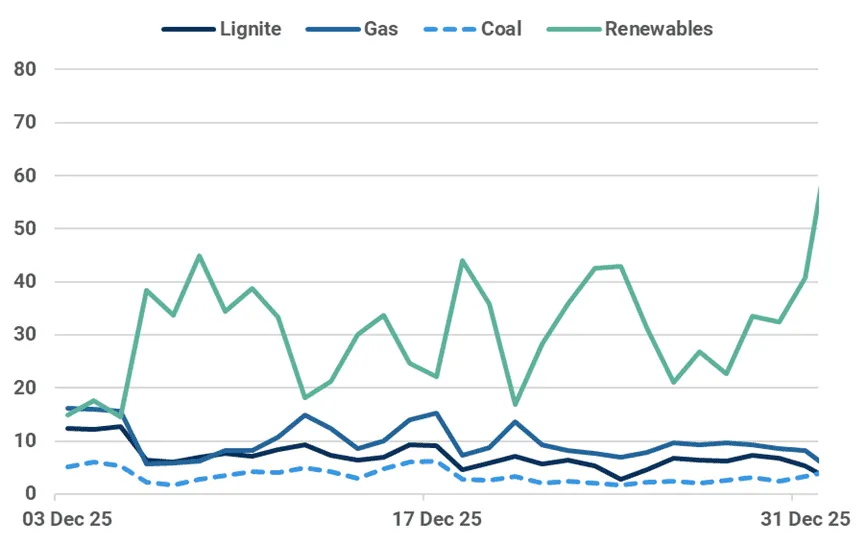

- Strong wind generation has recently curtailed thermal power output in Germany, reducing coal consumption. Forecasts indicate that elevated wind generation will persist in the coming days, further limiting spot demand for the remainder of the winter period.

Germany thermal vs renewable average generation (GW)

Source: Entso-E

Grains & Oilseeds: Friendly weather keeps markets damp through the holiday season

- Estimates for Argentina’s 2025 wheat crop continue to rise, with the Buenos Aires Grains Exchange raising its estimate to 27.8 Mt, 25% above the previous record set in 2021. The massive increase in production is combined with low protein levels, and a large portion of the crop is expected to be of feed quality. We expect Argentine wheat to compete for destinations not just in Africa but also in Asia. December exports were the highest in four years and featured Asian destinations like Bangladesh, Vietnam and Indonesia.

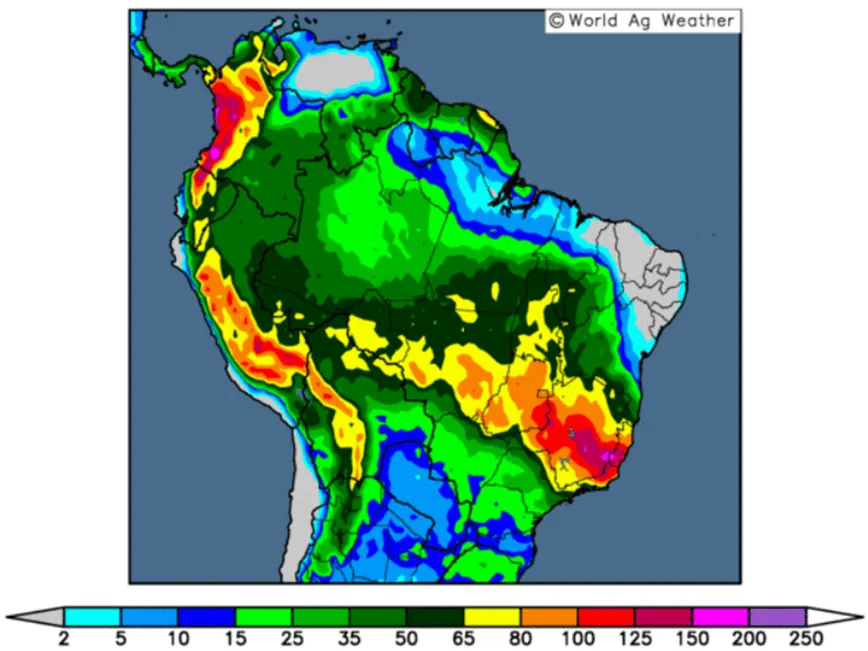

- Excellent weather has improved Brazilian soybean production prospects. Local estimates are already over 177 Mt, clearly surpassing last year’s record. Harvest is expected to begin in the second half of the month, with exports rising from February onwards. Successive years of high production have extended the soybean export season for Brazil, which exported more than 3 Mt of old crop in December. The forecast for the week ahead is generous in precipitation, which will further increase yield estimates. Current estimates will throw the 2026 balance sheet into further oversupply.

Soybean regions will receive good precipitation in the next 7 days (1 Jan 00Z, mm)

Source: WorldAgWeather

- Increased soybean crop estimates from Brazil have weighed on the new crop soybean-corn ratio, suggesting US farmers will plant more corn and fewer soybeans vs last year. The ratio of Nov soybean futures and Dec corn futures is now at 2.31, down from 2.4 a month ago. Our models estimate row crop areas to be unchanged if the ratio stays at 2.34 through February and early March. Below that, corn acres should increase, which will add to already high corn stocks.

New crop Nov soybean/ Dec corn futures ratio favours an increase in corn acres

Source: Barchart, Kpler Insight

- USDA announced the details of its $12bn Farmer Bridge Assistance (FBA) program, indicating direct payments to crop farmers at announced rates per acre. Soybean farmers will get $30.88 per acre, which translates to 58c per bushel at the national average. Farmer associations have expressed their gratefulness to the Trump administration, but say further support is necessary, hinting that it should come from increasing the preference for soy-based feedstocks in biofuel policies.

Minor Bulks: Guinean bauxite exports increase amid political clarity and seasonal tailwinds

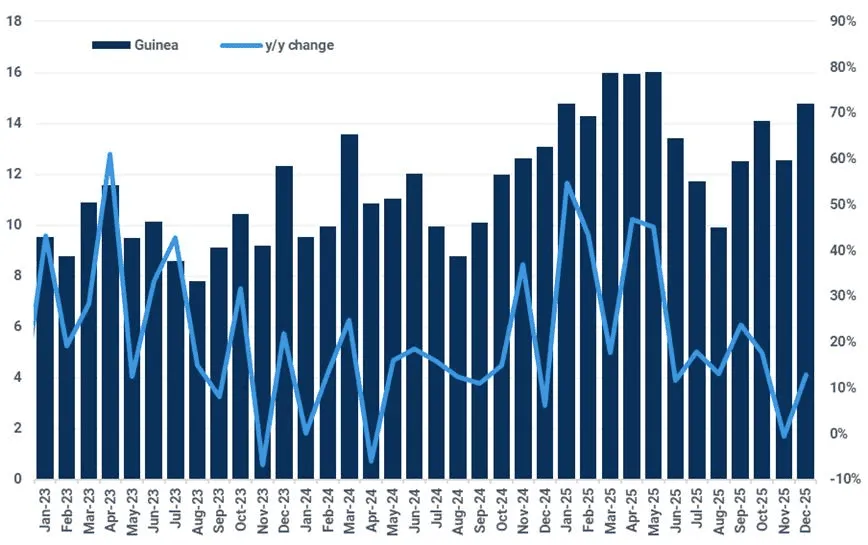

- Guinea's bauxite exports climbed 13% y/y to 14.80 Mt in December, the highest in seven months, supported by favourable dry season conditions. Mining firm AGB2A-GIC received authorisation from the Ministry of Mines in late December to resume operations. The company, which operated in the former Axis Minerals mines through a leasing agreement, had been forced to suspend activities since May 2025 following the revocation of Axis Minerals’ mining permit. The resumption follows a new royalty agreement with the government and is expected to add up to 15 Mt of new bauxite supplies to the seaborne market in 2026.

- Guinea’s junta leader, General Mamady Doumbouya, has been elected president with an absolute majority in the 28 December elections. The relatively smooth transition, calmer than many had anticipated, offers a measure of political stability, particularly for the country’s mining sector. Simandou, the country’s flagship iron ore project, is closely aligned with Doumbouya’s long-term economic agenda and is likely to see continued political backing. While long-term policy uncertainty persists, given the increasing popularity of resource nationalism, Guinea is poised to maintain its status as the leading global supplier of bauxite and have a growing influence in the seaborne iron ore market as Simandou progresses.

- Alumina prices staged a modest recovery after Beijing announced on 26 December it would tighten oversight of new alumina projects to curb irrational investment and disorderly expansion between 2026 and 2030. The most traded contract on SHFE, May 2026, rose 5.34% from a recent low of 2,637 yuan/t ($374.75/t) to 2,778 yuan/t ($396.50/t) on 31 December. However, without further output cuts, oversupply concerns persist, capping the prospect for a sustained price rally.

Guinea seaborne bauxite exports and y/y change (Mt,%)

Source: Kpler

Dry Bulk Freight: Pacific Panamax ballast supply declined to a multi-week low

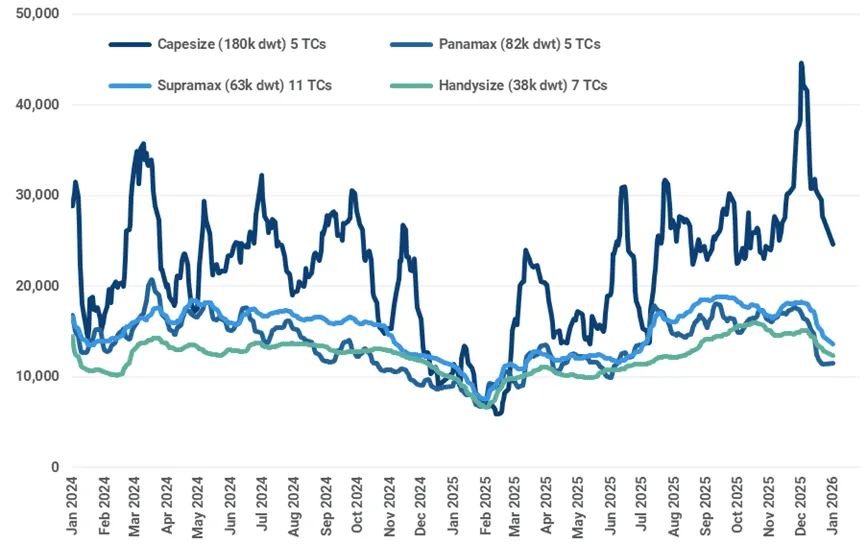

- The Capesize 5 TC earnings (180k dwt) declined further to a multi-week low of $24,687/day, down $24,687/day w/w on 2 January. The most significant decline was observed on the Pacific-round voyage, as seasonal softness in Australian iron ore chartering reduced demand. In the very short term, competition from cheaper Panamaxes for Australian coal shipments will put more downward pressure on Capesize earnings. At 2.14, the Capesize:Panamax average earnings ratio is higher than the long-term average of 1.21, although still down sharply from the recent high of 2.56 on 22 December.

- From 2 January, the Baltic Exchange will transition the Capesize index vessel definition from 180k dwt to 182k dwt. We will adopt the specification in our subsequent report.

- After some steep declines in December, average Panamax earnings look to have found a floor, with the 5TCs edging higher to $11,536/day on 2 January, although still slightly lower w/w. There are signs of a shift in the deployment of vessels between the basins. Panamax ballast supply in the Pacific Ocean declined to a three-week low of 777 vessels on the week of 29 December, while ballasters in the North Atlantic Ocean increased sharply. US soybean chartering should provide some alternative demand outside the Pacific basin at the start of the year, as exports are expected to peak in January rather than the typical October to November period. Nonetheless, annual volumes are forecast to be lower y/y for the September-August 2026 export season.

- Both Supramax and Handysize average earnings slipped further to $13,601/day (down $1,840/day w/w) and $12,329/day ($1,103/day w/w), respectively. Rates were softer across both basins.

- A Chinese military exercise in the South China Sea, including waters surrounding Taiwan, between 29 and 30 December 2025, delayed cargo discharges at Taiwanese ports. There was a notable increase in Handysizes waiting to unload shipments at the ports during the period, leading to a drop in overall cargo liftings on the following day. Congestion has eased since then.

- Methanol- and biofuel-powered vessels will be exempt from entry fees when calling at Japan’s Yokohama Port starting in 2026. At 4.6Mt, dry bulk loaded to the port in 2025 were mostly Panamax-carried, where most of these were coal shipments. At least six methanol Kamsarmax/Panamax vessels are scheduled for delivery in 2026, with the remaining three vessels due in 2027.

- Despite a strong second half of the year, average dry bulk carrier earnings underperformed 2024 across all four main vessel classes in 2025. The Baltic Exchange Supramax 11 TC recorded the most significant y/y decline at 9.2% to $14,275/day, while Capesize (180k dwt) 5 TC, Panamax 5 TC and Handysize 7 TC slipped lower by 5.7% ($21,297/day), 5.2% ($13,361/day) and 5.9% ($11,911/day), respectively. The outlook for 2026 will be published in our Freight Monthly Report next week.

Steep declines in dry bulk carrier earnings at the start of 2026 ($/day)

Source: Baltic Exchange

Key Dry Bulk Market Developments

Dry Bulk Commodity Flows

Source: Kpler

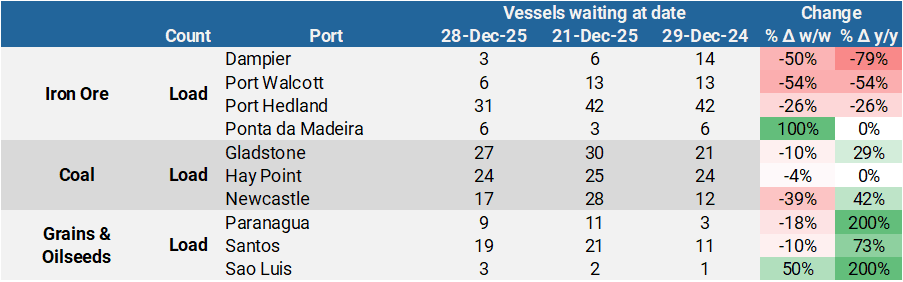

Dry Bulk Port Congestion

Source: Kpler

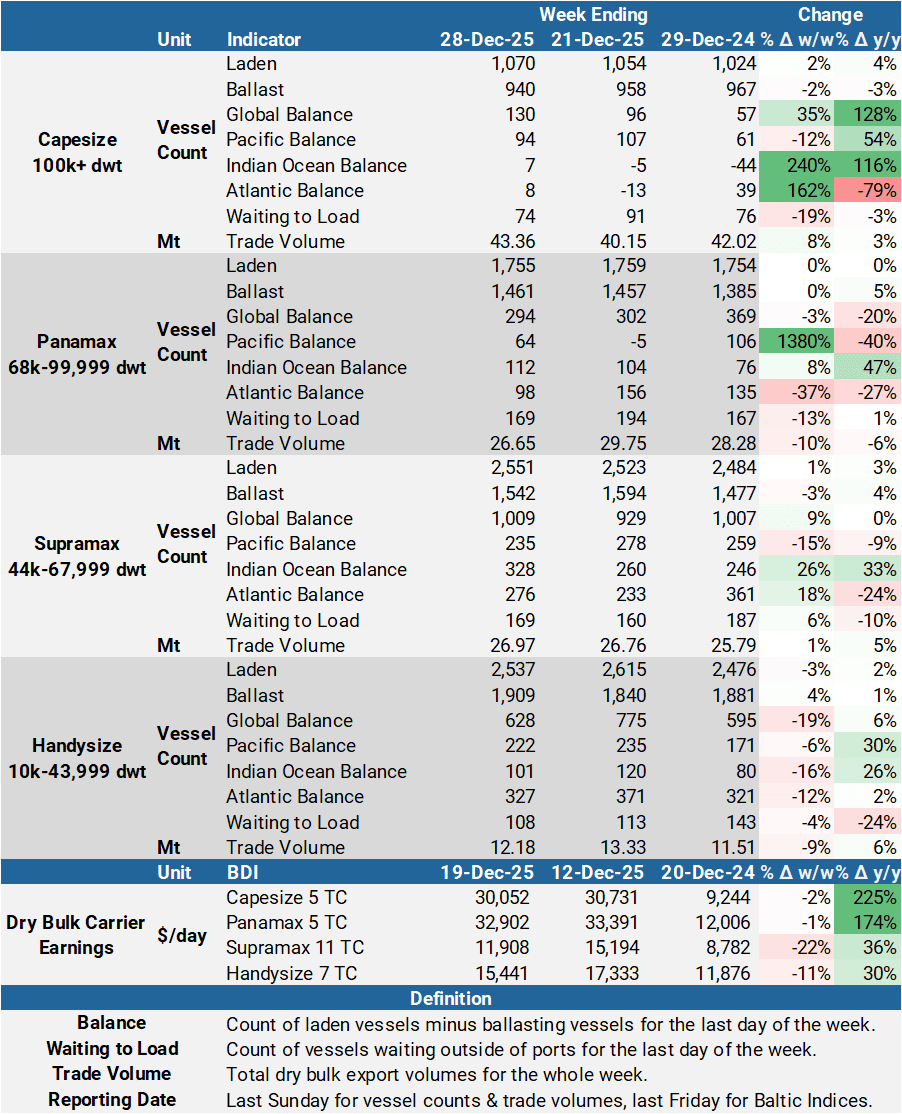

Dry Bulk Freight Metrics

Source: Kpler, Baltic Exchange

See why the most successful traders and shipping experts use Kpler

Request a demo

.webp)

Ready to navigate dry bulk shifts with precision and confidence?

Request trial access