August 26, 2025

Capesize earnings retreat as mounting vessel supply in Asia-Pacific pressures rates

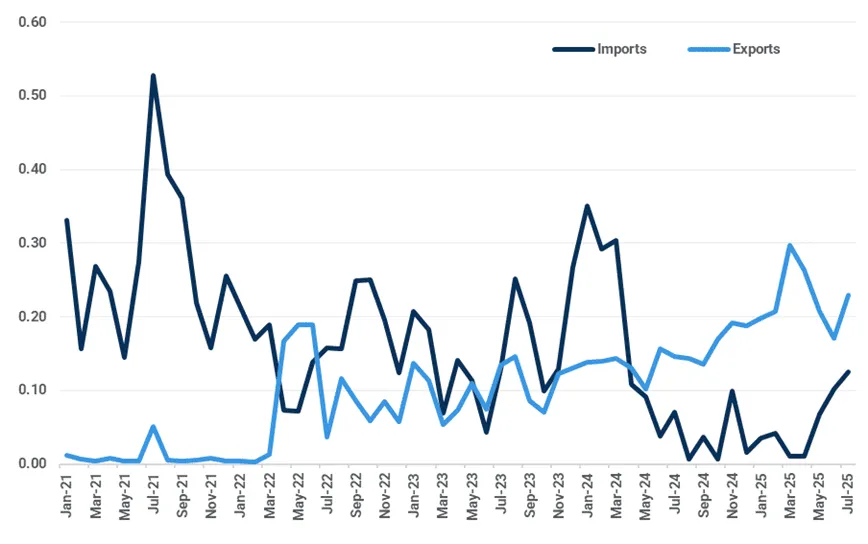

Iron Ore & Steel: Iron ore exports hit the highest level in over a year

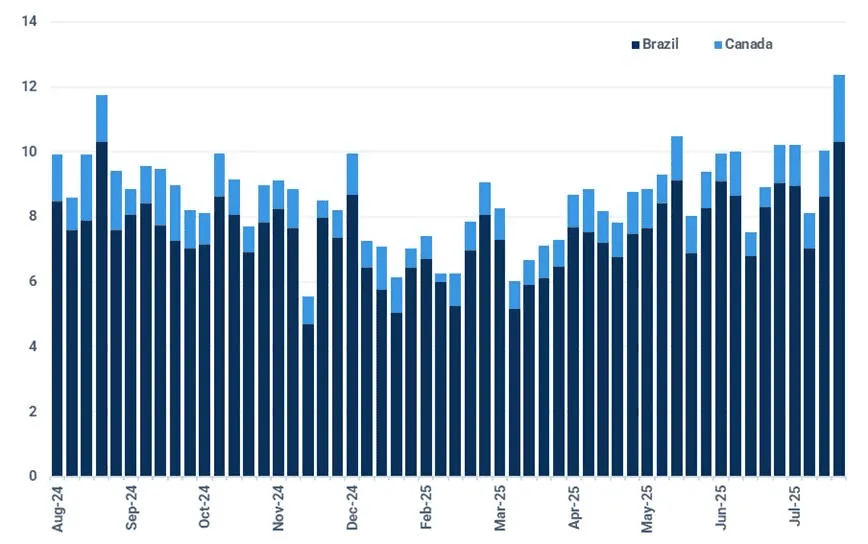

- Global seaborne iron ore exports surged to 36.90 Mt in the week ending 17 August, marking a 13-month high. This is mainly driven by record shipments from Brazil, where exports build towards their typical seasonal peak in August. A record high in Canadian shipments also supported the upswing as departures from Baffinland gain further momentum.

- In Australia, iron ore exports finished at 17.90 Mt last week, recovering from early August’s dip. The conclusion of maintenance works at Hancock Iron Ore’s operations enabled its shipments from Stanley Point to resume at over 1 Mt. Meanwhile, Fenix Resources marked a milestone with the first shipment from its recently commissioned Beebyn W-11 project (Nameplate capacity: 1.50 Mtpa). According to Kpler data, the Panamax vessel Bangor, carrying 60,000 tonnes of iron ore, departed Geraldton Port on 17 August and is en route to Qingdao, China, with arrival expected in early September.

- On the demand side, China imported 25.40 Mt of seaborne iron ore last week, retreating from the near-record high witnessed in early August but remaining well above the previous five-year average of 23.90 Mt for the period. However, the demand for iron ore may soften as steel output may be curtailed due to environmental restrictions ahead of the Victory Day military parade on 3 September. As a result, this could contribute to a further build-up in port inventories, which had already risen for two consecutive weeks in the first half of August.

- Iron ore markets have traded in a narrow band over the past week as the market weighs two major policy variables: the extent to which China’s environmental measures ahead of the military parade will disrupt steel production, and how new US tariffs on “derivative” steel products could shape global demand. The most-traded contract on DCE, January 2026, closed marginally lower, down 0.32% w/w at 772.50 yuan/t ($107.58/t). Meanwhile, the SGX TSI 62% Fe second-month contract slipped 0.82% w/w to $101.25/t at the time of writing.

Brazilian and Canadian iron ore shipments hit record highs (Mt)

Source: Kpler

Coal: Peabody terminates Moranbah mine agreement

- Peabody Energy terminated its $3.8 billion agreement to acquire Anglo American's metallurgical coal mines in Queensland, Australia on 19 August. Peabody cited a material adverse change due to an explosion at Anglo American's Moranbah North Mine in March. The Moranbah North Mine has remained shut since 31 March, with no clear timeline for resuming sustainable longwall production at forecasted volumes and costs. Anglo American estimates monthly holding costs of $45 million at Moranbah North and plans to initiate arbitration seeking damages for wrongful termination.

- China's domestic coal production fell 3.8% year-on-year in July, the first decline in 14 months. Government safety audits and heavy rainfall in Shanxi, Inner Mongolia, and Shaanxi disrupted mining operations. Domestic NAR 5,500 kcal/kg coal prices exceeded 700 yuan/t at northern China’s ports, rising by around 14% since June. Northern port inventories dropped to 23.6Mt, the lowest level since this year. Heatwaves in China buoyed demand for imported coal and push up domestic coal prices. Major Chinese coke producers proposed a price hike ahead of the upcoming production cuts mandated for the 3 September military parade in Beijing. Steel mills must scale down production by 20-40% over 30 August-3 September.

- India's coal production in July fell to an 11-month low of 65Mt, down by around 25% y/y due to monsoon disruptions. But power plants hold sufficient stocks, suggesting a y/y increase in coal imports is unlikely.

- European physical thermal coal prices fell below $100/t earlier this week but rebounded later in the week, as producers are unwilling to offer volumes below their production costs. Coal stocks at the Amsterdam-Rotterdam-Antwerp hub declined despite weak coal burn in Germany in August owing to strong renewables output.

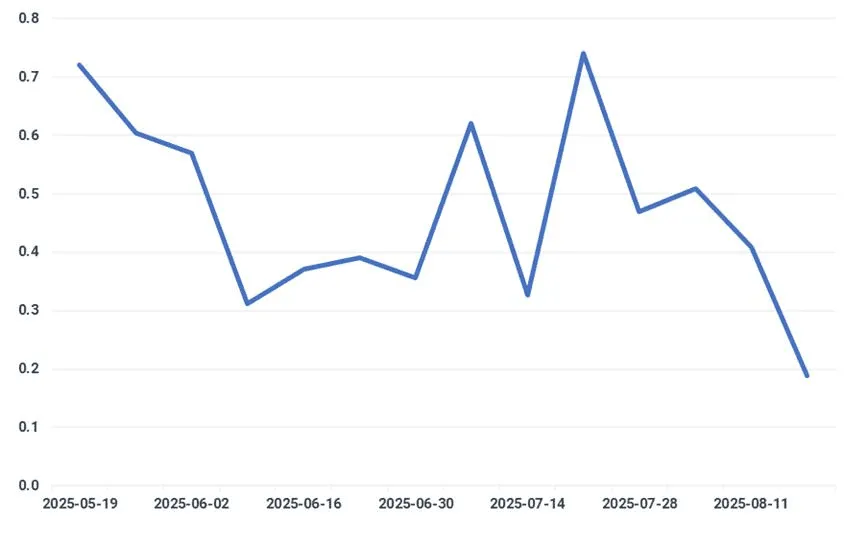

- One of the two berths at Westshore Terminals will remain offline for about ten weeks due to a fire on a shiploader on 16 August. This closure should lower Westshore's 2025 throughput volumes from a previous projection of 26Mt to 24-24.5Mt.

Westshore weekly coal exports (Mt)

Source: Kpler

- No vessel queue exists at Cerrejon's Puerto Bolivar despite the ongoing blockade on the railway feeding into the terminal. The handymax Fjord Pearl is loaded at the port this week.

Grains & Oilseeds: US crop tour sees lower corn yields than USDA

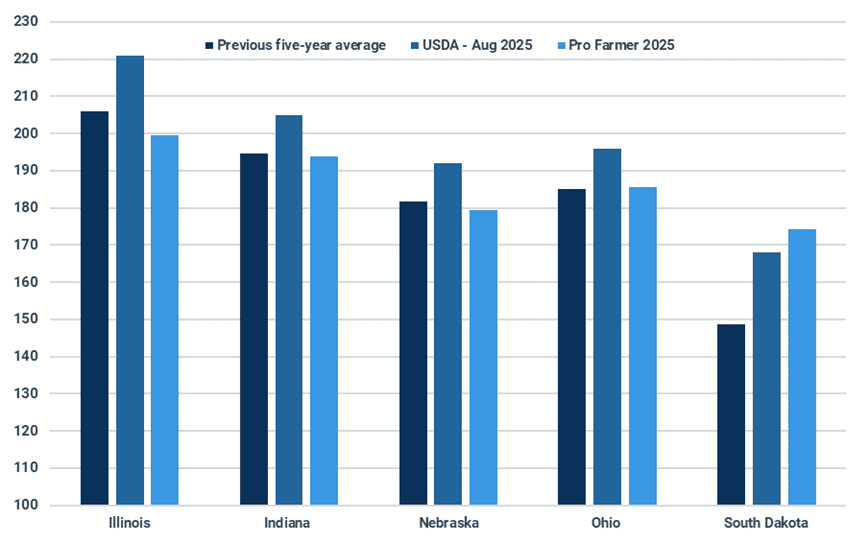

- At the beginning of this week, the Pro Farmer crop tour began, where crop scouts assess how corn and soybean crops are developing across key-producing states. While the tour is ongoing, recent findings from the states visited show most corn yields are up on the year, as well as most states showing increased soybean pod count y/y; but early corn yield estimates vary from the USDA forecasts. There are reports of disease being seen across the crops, which is leading to some concerns about how the crops will finish in the lead-up to harvest.

Pro Farmer crop tour estimates corn yields below USDA (bu/ac)

Source: Pro Farmer, USDA

- After last week’s tariff on Canadian canola, China booked its first cargo of Australian canola since 2020. The cargo is expected to be delivered to China during November or December, however, it is not certain whether this is one of the five trial canola cargoes China had discussed with Australia in July. During discussions in July, the acquisition of GMO approval had been a barrier to the agreement of the cargoes. Last week, China’s Ministry of Agriculture and Rural Affairs granted approval of seven GMO Safety Certificates to COFCO Oils & Oilseeds Trading Co., but specific details were not disclosed.

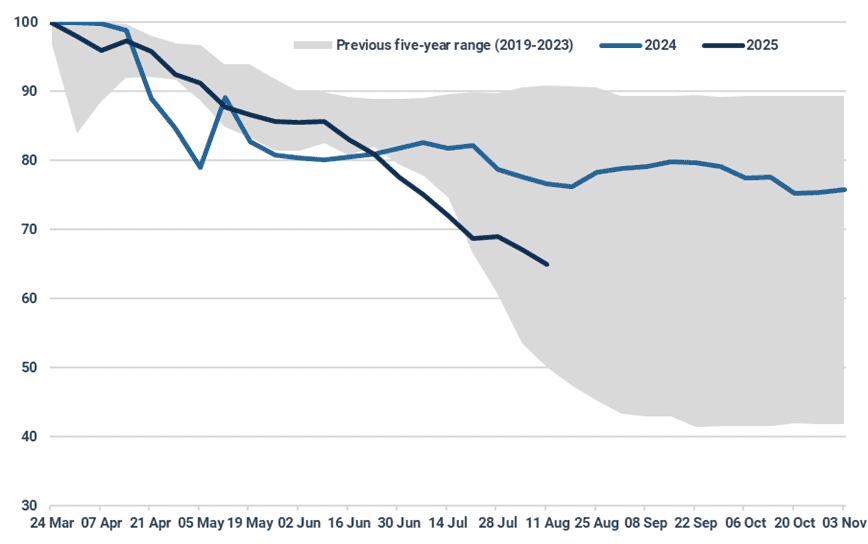

- With the harvest of the French soft wheat crop nearing completion, 96% on 11 August, reports regarding the quality of the crop are mostly favourable. Of the 71% of national samples analysed, FranceAgrimer reports that 65% of the crop at least satisfies the minimum specifications of the MATIF Milling Wheat contract, up from the five-year average of 49%. French wheat exports have recently been able to take advantage of the tighter Russian supply, with reports that Egypt has booked more than 400 Kt of French wheat in the past two weeks. As well as French wheat exports, focus is also turning towards the developing corn crop, which has been subject to stress following hot and dry conditions, leading to a deterioration in condition.

French corn crop feels the heat (% crop rated in good or excellent condition)

Source: FranceAgriMer

- Turkish wheat imports have remained fairly subdued since the turn of the new marketing year as the availability of Russian and Ukrainian wheat remains tight and prices above rival origins. In March, Türkiye had lifted duties on wheat imports in support of its flour milling industry, which had seen its competitiveness wane to the benefit of rival flour exporters such as Egypt. Turkish wheat imports are expected to rebound once Black Sea wheat supply becomes more readily available and prices become more competitive.

- Following last year’s poor crop, Ukrainian corn exports remain near absent on the global market, allowing rival major corn exporters the opportunity to obtain greater demand. There are concerns regarding the currently developing crop, too, as crops in the central and southern regions are seeing yields under pressure following adverse weather conditions. Rains and near-normal temperatures forecast for the coming weeks are key to supporting the development of the crop.

- Brazilian soybean exports lined up for September delivery continues to buck the seasonal trend, showing a far more gradual decline in exports following the harvest of its record soybean crop. With US soybeans subject to a 34.07% import tariff in China, this has helped to support Brazilian soybean demand as recent FOB offers show Brazilian soybeans pricing higher than US origin.

- Following the safrinha harvest, Brazil corn exports have picked up, with over 5 Mt sailed or loading and over 8 Mt estimated for August exports. China, Iran and Egypt are the main buyers, but significant volumes are also lined up for Japan, South Korea and Europe.

Minor Bulks: China maintains a net alumina export position for the sixteenth consecutive month

- Guinean seaborne bauxite exports totalled 2.46 Mt in the week ending 17 August, recovering from the early August low of 1.61 Mt. As heavy rains continue to disrupt mining and logistical operations, weekly volumes may stay below 2.50 Mt in the near term. Meanwhile, Rusal’s Friguia alumina refinery has reportedly re-entered negotiations with workers following weeks of strikes and labour unrest. The outcome of the negotiations may shape operational stability in the coming months.

- In China, July marked the sixteenth consecutive month in which alumina exports exceeded imports. Customs data show that outbound shipments totalled 0.23 Mt, while imports stood at 0.13 Mt, yielding a net export surplus of 0.10 Mt. This trend continues to be underpinned by sustained Russian demand, as Rusal buys spot volumes in the global market to replace around 40% of its self-owned alumina supply lost since 2022, following Australia’s export ban and the closure of its Nikolaev refinery in Ukraine.

- Alumina prices have accelerated their decline over the past week, weighed by record production levels and mounting domestic inventories. The most active SHFE contract, January 2026, fell 3.58% w/w to 3,124 yuan/t ($435.06/t) on 21 August, the lowest in four weeks. In the absence of significant supply disruptions to either bauxite or alumina output, bearish fundamentals are expected to persist, exerting further pressure on prices in the short to medium term.

China has been a net alumina exporter since Q2 2024 (Mt)

Source: China Customs

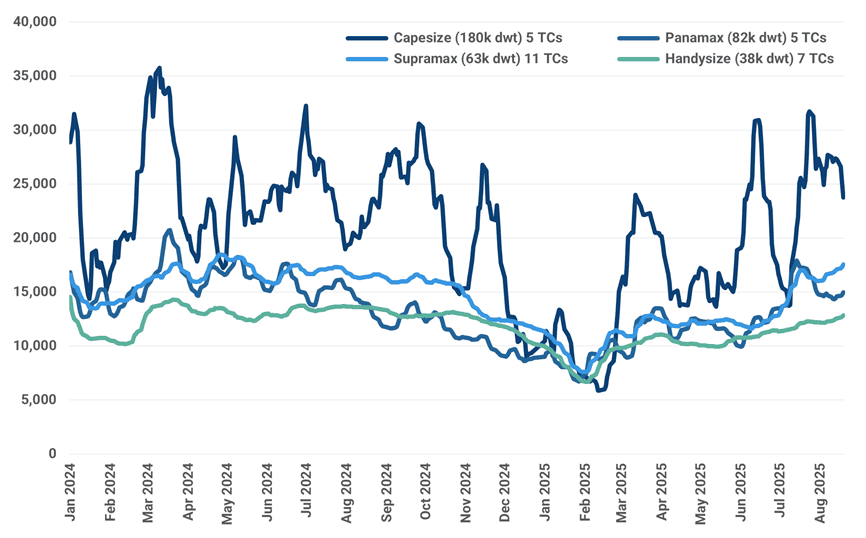

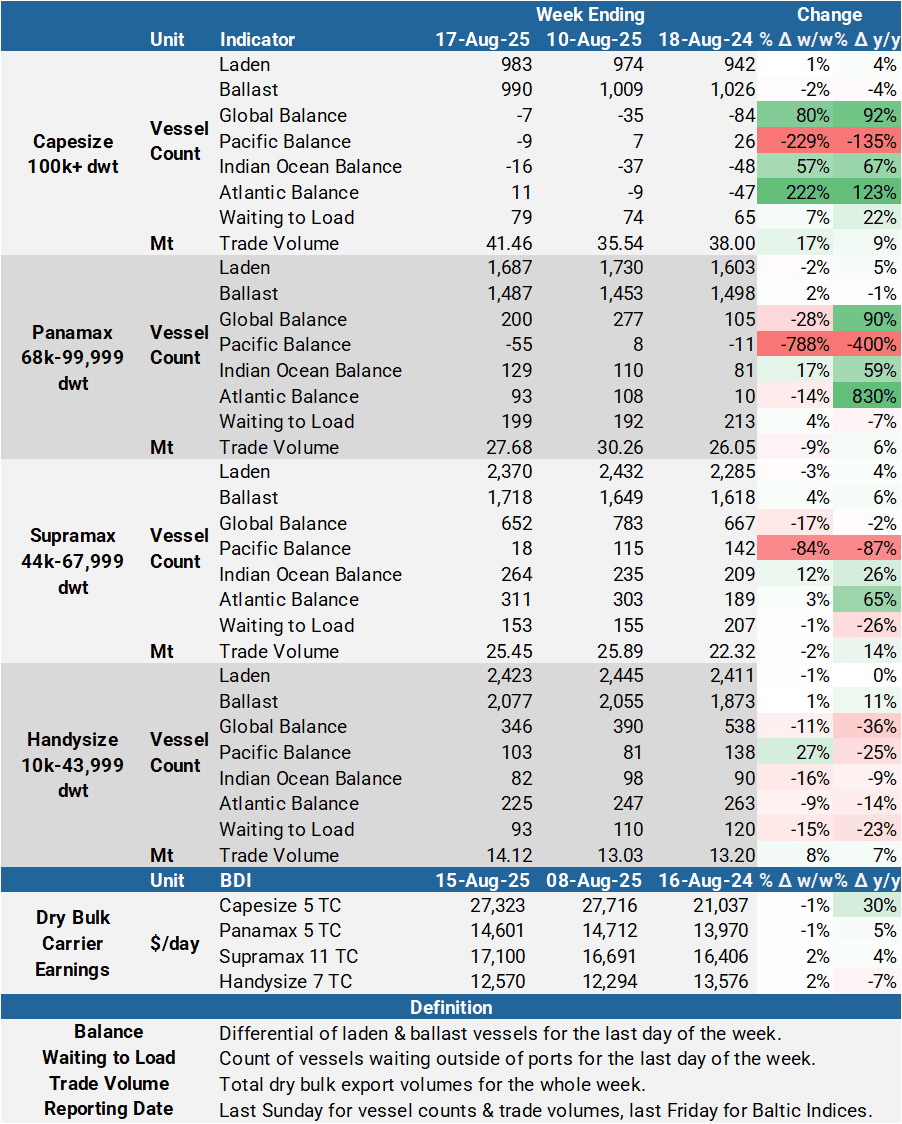

Dry Bulk Freight: Mounting Capesize ballast supply adds pressure to earnings

- The Capesize 5 TC average earnings retreated by $3,428/day w/w to $23,778/day on Pacific basin weakness. Slower Australian iron ore chartering and lower bunker prices can be seen in the W.Australia-China iron ore spot voyage rates (C5), which declined by $0.94/t w/w to $9.04/t, at the time of writing. Mounting vessel supply in the Asia-Pacific region has weighed on vessel earnings. Capesize ballast tonnage on the week ending 17 August increased by over one and a half percent w/w while laden tonnage declined by almost twice that amount. However, demand for Brazilian iron ore exports, which we expect to peak in August, may redirect some of the ballast tonnage out of the basin.

- The Panamax 5 TC average earnings rebounded by $643/day w/w to over a two-week high at $14,985/day on Atlantic basin strength. Increased minerals shipments from the US Gulf are supporting demand in the Atlantic, which saw Atlantic round-voyage rates (P1A) rise by $845/day w/w to $15,795/day, while fronthaul rates (P2) rose by $1,477/day w/w to $22,971/day. Seasonal strength in US wheat exports will add demand in the North Atlantic. While most shipments are carried by Supramax and Handysize vessels, a substantial volume is shipped on Panamax/Kamsarmax.

- The Supramax 11 TC average earnings rose by $663/day w/w to $17,550/day, the highest since July 2024, on strength across both basins. Pacific round-voyage rates (S2), which rose to the highest since October 2024 at $15,764/day (up $1,050/day w/w), have been benefiting from stronger wheat exports from the US West Coast (USWC) and seasonal Chinese coal imports. The strength of Supramax Pacific round-voyage rates has pushed the premium to the Panamax equivalent higher, which could provide an upside to the larger vessel segment.

- Meanwhile, Supramax Black Sea-Far East rates (S1B) jumped to the highest since November 2024 at $17,517/day (up $1,217/day w/w), where Black Sea wheat exports are building strength and will continue to drive demand in the short term. However, tighter security compliance since July for Russia’s Kavkaz port has been causing delays to port lineups where foreign-flagged vessels need national security service approval on top of port authority clearance before entry.

- The Handysize 7 TC average earnings rose by $432/day w/w to a year-to-date high of $12,849/day on Atlantic basin strength.

Geared vessel markets strengthen: Supramax and Handysize earnings rose to a year-to-date high ($/day)

Source: Baltic Exchange

Key Dry Bulk Market Developments

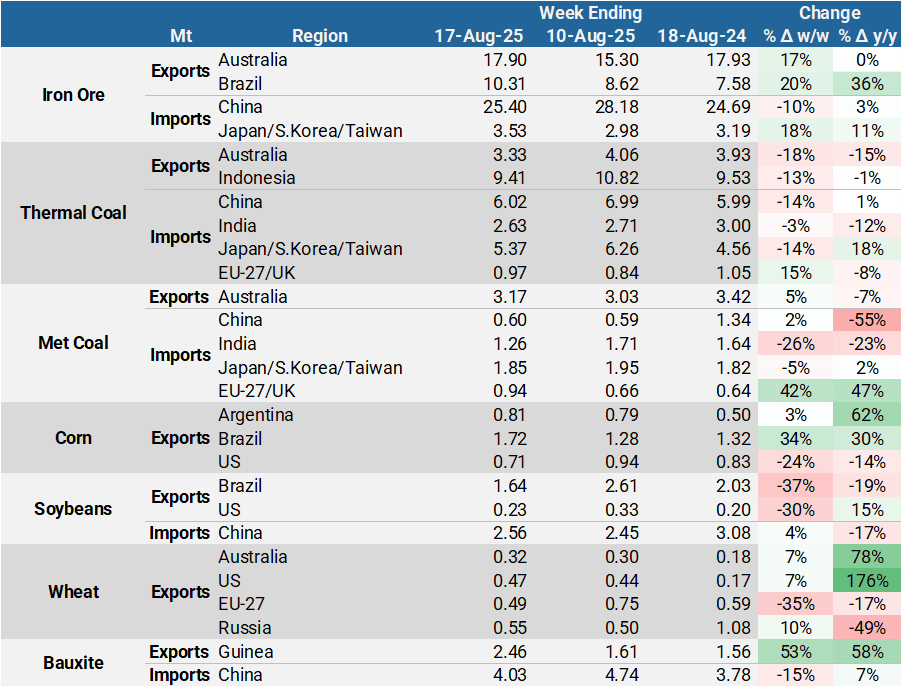

Dry Bulk Commodity Flows

Source: Kpler

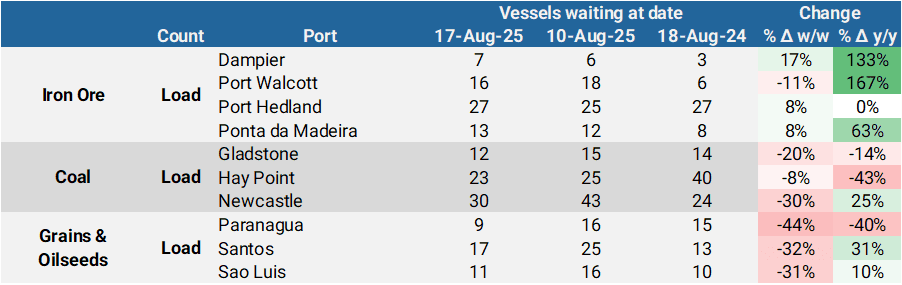

Dry Bulk Port Congestion

Source: Kpler

Dry Bulk Freight Metrics

Source: Kpler, Baltic Exchange

New dry bulk insights

Gain instant clarity on dry bulk flows, rates and fundamentals with real-time AIS tracking and proprietary supply- demand models. Seasoned analysts deliver concise reports and live briefings spotting emerging trends and market imbalances. Navigate shifts with precision and confidence.

See why the most successful traders and shipping experts use Kpler

Request a demo

Gain clarity on dry bulk flows, rates & fundamentals to navigate market shifts precisely

Request access