Fading speculative attention masks persistent diesel tightness

Atlantic Basin diesel tightness is far from resolved — lean PADD 1, PADD 2, and European stocks leave the market structurally undersupplied into Q4. US Gulf refiners are locked into the Americas as Latin America leans harder on them, while heavy Middle East turnarounds strip out another 875 kbd of winter ULSD capacity. Europe’s fallback on Indian diesel will be short-lived, with new EU sanctions on Russian feedstock looming in January and US pressure raising the risk that flows disappear sooner.

Market & trading calls

- Bullish skew remains: PADD 1, PADD 2, and European stocks are still lean.

- Q4 trigger looms: USGC barrels tied to the Americas as heavy Middle East turnarounds bite.

- Irony abounds: India can plug Europe’s Q4 gap, only to be hit hardest by EU sanctions in January.

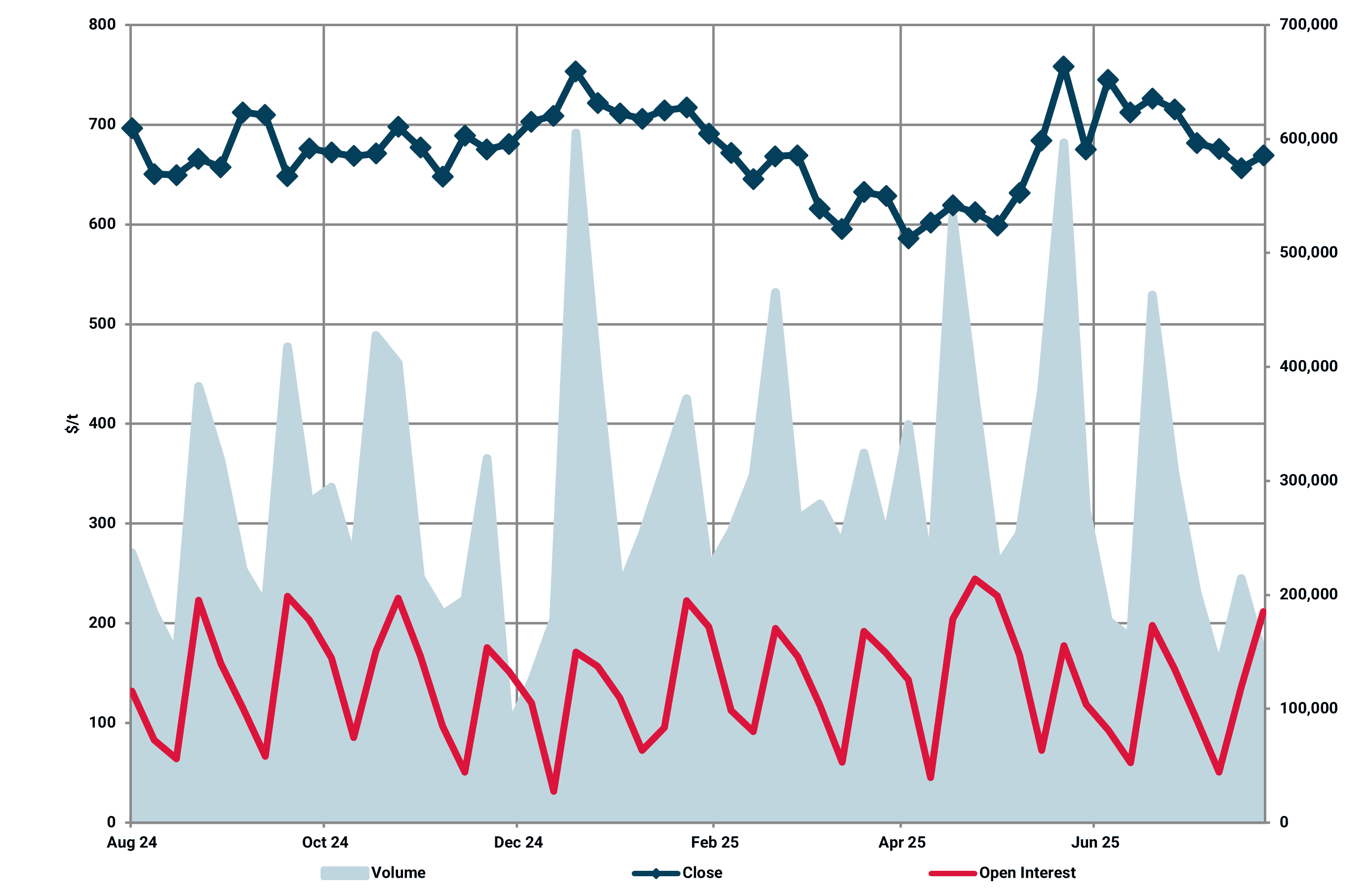

ICE Gasoil Futures close ($/t) vs open interest, and volume (RHS)

Source: Marketview

The pullback in ICE Gasoil futures has fostered the impression that July’s tightness has run its course. In reality, the correction reflects a retreat in speculation, not a structural shift in the fundamentals. We continue to view the Atlantic Basin diesel market as fundamentally tight, led by chronic shortages in PADD 1 and PADD 2. Headline US inventory builds have distracted the market, but stocks remain 15% below seasonal norms. Both PADDs remain deeply undersupplied heading into the harvest season, with balances set to tighten further through Q4. The recent floods at BP’s 430 kbd Whiting, Indiana refinery have underscored this fragility, removing a key source of Midwest supply just as seasonal demand ramps up.

Diesel ULSD Colonial 62 FOB Cycle 3/WTI Houston M1 Crack ($/bbl)

Source: Argus

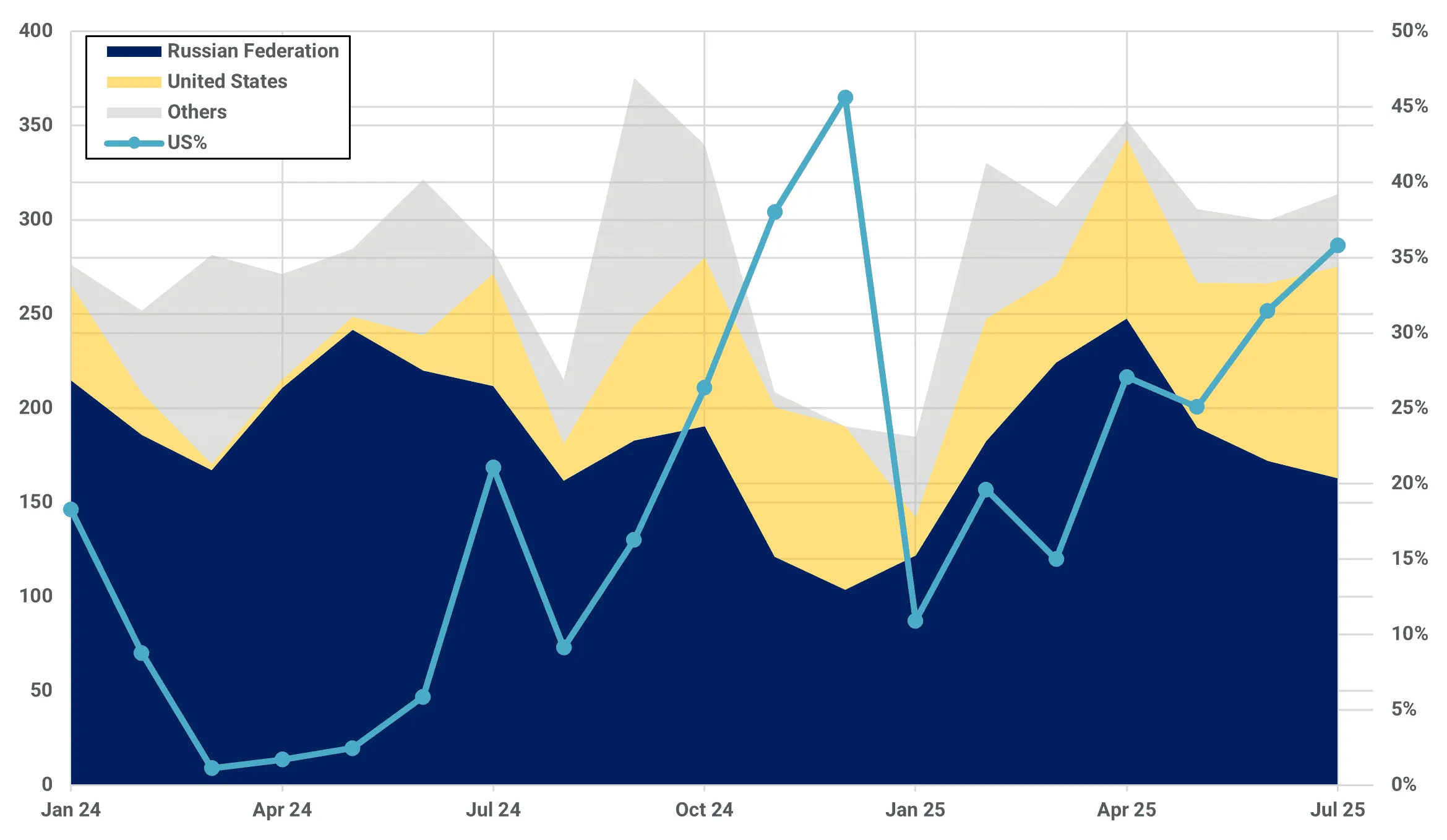

This structural tightness limits the US Gulf Coast’s ability to supply Northwest Europe through year-end. At the same time, Gulf refiners have been forced to backstop Latin America, as drone strikes on Russian refineries have curtailed exports. Brazil has been hit hardest, with Russian diesel arrivals dropping to a six-month low of 160 kbd in July. Kpler data shows US suppliers have already lifted their share of Brazilian imports to a year-to-date high of 36%.

Brazil gasoil/diesel imports (kbd) vs US market share % (RHS)

Source: Kpler

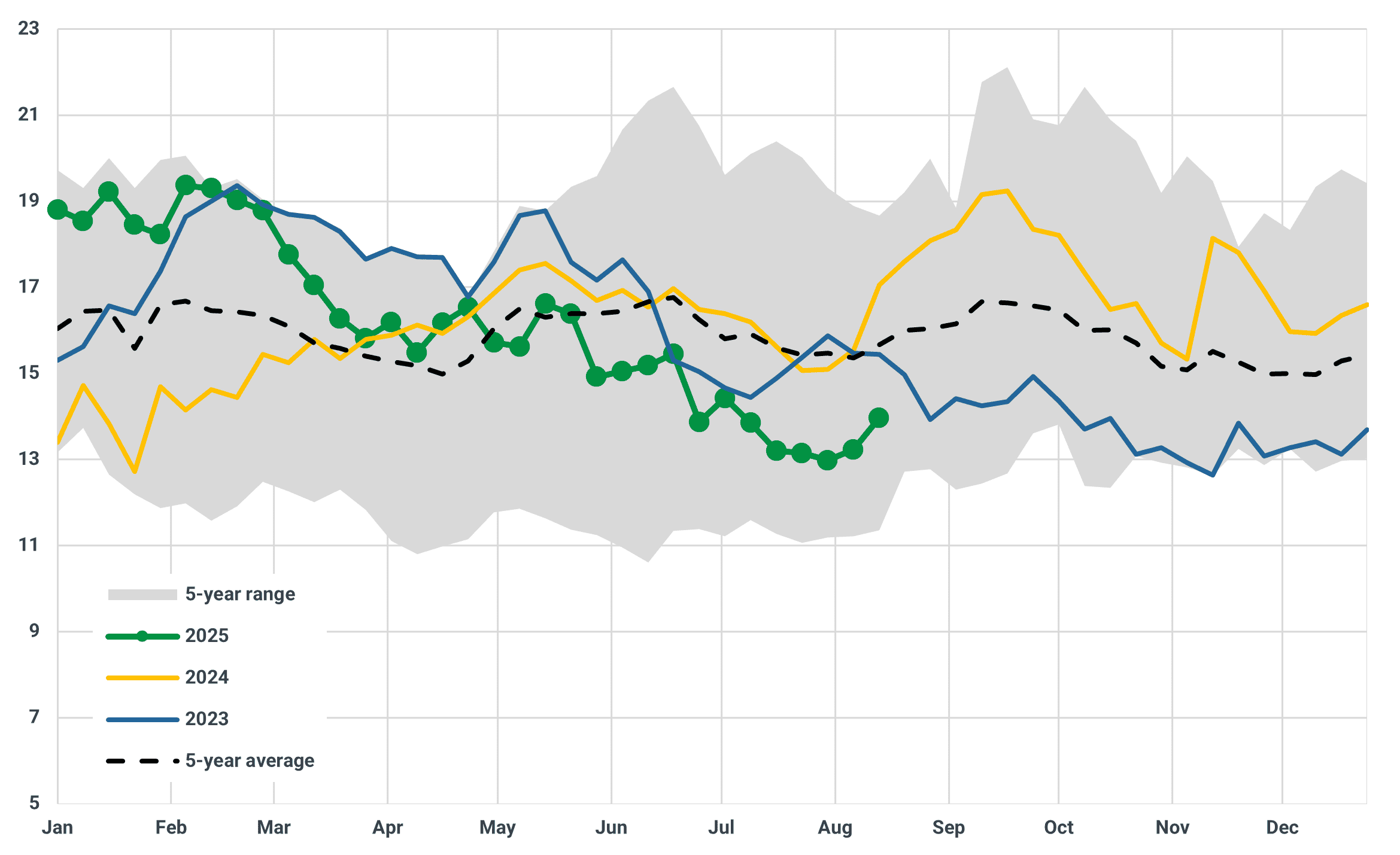

Europe is not in a comfortable position either. Continent-wide stocks have drawn steadily since January and now sit 7% below seasonal baselines (Kpler using JODI). ARA inventories are even leaner at 13.97 Mbbls, down 10% versus norms. This leaves Northwest European diesel cracks highly exposed to the upside as winter-grade demand emerges. The US Gulf Coast will remain focused on the Americas, while Middle Eastern CDU turnarounds strip out another 875 kbd of winter ULSD capacity across October–November (SATORP, SASREF, Mina Abdullah). That equates to around 195 kbd of winter-spec diesel lost in October and 250 kbd in November.

ARA: gasoil/diesel stocks in independent storages (Mbbls)

Source: Kpler using Insights Global

The alternatives are thin. South Korean and Chinese refiners can produce winter-spec cargoes, but arbitrage rarely clears, and Korea is expected to prioritize summer-grade barrels for Australia’s summer deficit. India has emerged as Europe’s likeliest savior, but this outlet is fleeting. Indian refiners have leaned heavily on discounted Russian crude, allowing them to ship diesel into Europe at competitive economics. Yet that window closes in January, when EU sanctions will prohibit CPP produced from Russian feedstock. The dynamic will likely prompt a rush: European buyers could accelerate liftings from India in Q4, echoing the stockpiling surge seen ahead of the February 2023 ban on Russian products.

Still, risks persist. Washington has grown increasingly vocal over India’s role as a conduit for Russian crude. Any escalation in US pressure could constrain flows earlier, whether through banking scrutiny, insurance restrictions, or diplomatic pressure on counterparties. This leaves Europe highly exposed — reliant on Indian diesel for the winter, yet with the very real risk that this fallback disappears faster than expected.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Get research & analysis driven by proprietary data