September 10, 2025

Iron ore holds firm while coal, wheat and alumina prices under pressure

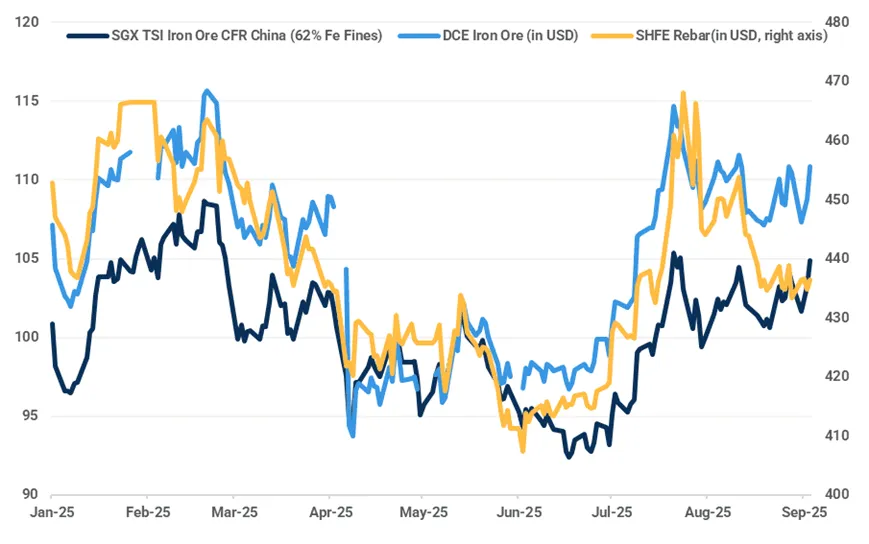

Iron Ore & Steel: Iron ore remains resilient despite weaker steel prices

- Global seaborne iron ore exports reached 35.10 Mt in the week ending 31 August, the second-highest weekly figure since June and well above the five-year seasonal average of 33.70 Mt. This strength was driven by a two-month high in shipments from Australia, where miners FMG, Hancock Iron Ore and MinRes reported multi-week highs in loadings following the completion of maintenance works earlier this quarter.

- In South Africa, the future of the Beeshoek mine is under threat. Assmang has been considering the closure of the mine as its primary customer, ArcelorMittal South Africa (AMSA), moves ahead with plans to shutter its long steel operations in Newcastle and Vereeniging. AMSA’s decision follows failed negotiations with the government and stakeholders to secure the viability of the plants. Meanwhile, efforts to pivot Beeshoek’s output toward export markets appear to have faltered due to infrastructure bottlenecks, high operating costs, and the difficulties of securing long-term buyers in an increasingly oversupplied market environment. Unaffected by the development, we expect South African seaborne iron ore exports to remain slightly above 50 Mt annually over the next three years.

- On the demand side, China continues to absorb iron ore at scale. Seaborne imports reached 25.60 Mt last week, well ahead of the five-year average of 22.10 Mt. Total imports for August reached a near-record 112.40 Mt, supported by record seasonal Brazilian shipments and the clearing of port backlogs caused by late-July typhoon disruptions. These elevated arrivals are expected to support steel production in the post-military parade period.

- Iron ore prices have demonstrated resilience over the past week, even as steel prices have softened. The most-traded iron ore contract on DCE, January 2026, edged up 0.13% w/w to 791.50 yuan/t on 4 September, while the SGX TSI 62% Fe second-month contract gained 0.67% to $104.90/t at the time of writing. By contrast, during the same period, hot-rolled coil (HRC) and rebar futures on SHFE declined by 0.38% and 2.13%, respectively. We have revised up our iron ore price forecasts for September to reflect current market sentiment and the short-term firmness in Chinese steel output after the military parade. However, our long-term view on iron ore remains bearish with structural oversupply and weakening fundamentals looming large in the outlook.

Iron ore prices proved more resilient than Steel in recent days, tightening mill margins ($/t)

Source: DCE, SHFE, SGX, Kpler Insight

Coal: Thermal coal demand to ease in Asia-Pacific

- Thermal coal prices in China are trending lower following the end of the peak summer demand season. Domestic thermal coal prices at northern ports weakened, with 5,500 Kcal/kg NAR coal market falling below 700 yuan/t FOB Qinhuangdao. Steel mills are withholding responses to price hikes, and some are reducing coke intakes. Coking plants are making on-demand purchases amid a blurred market outlook.

- India’s coal import demand is on track to recover due to the slowdown in coal production. Some 12.42 Mt of thermal coal is expected to arrive in the country by the end of September, implying a 1 Mt m/m increase.

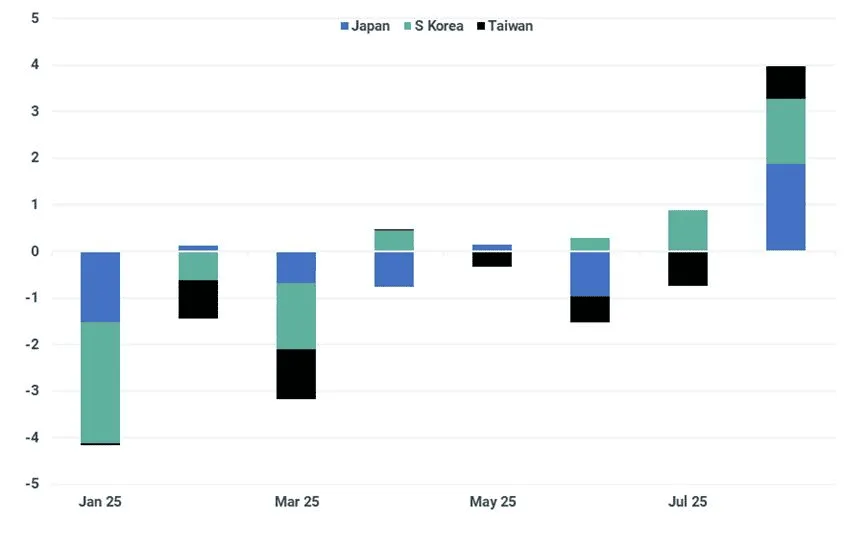

- Coal demand holds firm in northeast Asia as hot temperatures boost coal burn. In August, Japan's thermal coal imports reached 10.73 Mt, the highest since January 2024, but utilities are reducing capacity. South Korea's thermal coal imports also rose to a multi-year high of 9.28 Mt with a steep increase in discounted Russian coal alongside Indonesian supply.

Japan, S Korea, Taiwan thermal coal imports by destination (Mt)

Source: Kpler

- In Europe, Atlantic thermal coal prices moved lower, falling to the mid to low $90s/t cif, the weakest since late February. Both cif ARA and FOB Richards Bay futures contracts fell to near three-month lows. However, imports are expected to gain pace in September due to winter restocking.

- As the cooling season ends, Turkey's thermal coal imports eased from July’s 3.43 Mt to 2.72 Mt in August. Power sector coal burn remains firm, and high petcoke prices support coal demand from the cement industry.

Grains & Oilseeds: French wheat faces delayed harvest pressure

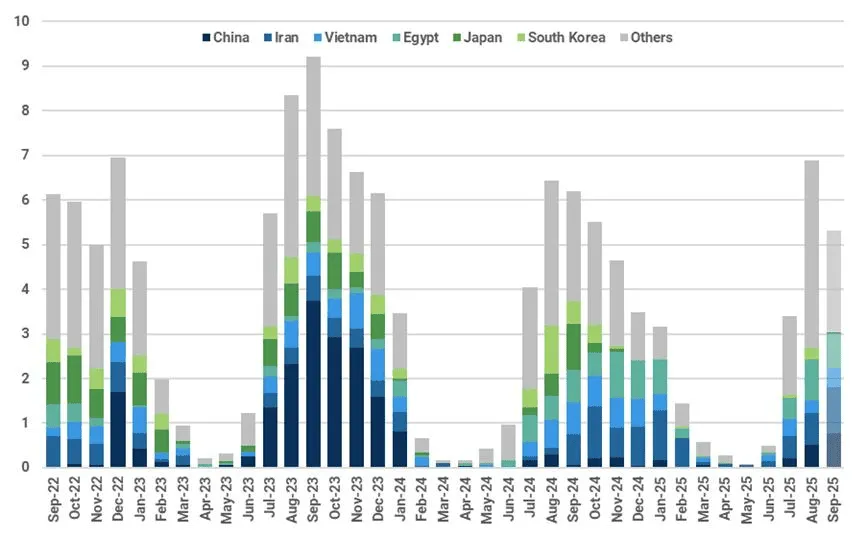

- Argentine corn exports for August dropped back m/m to 2.8 Mt as exports of other agricultural goods, particularly soybeans and soybean meal, challenged port capacity. In contrast, Brazilian corn exports accelerated in August to 6.9 Mt, the largest monthly volume since October 2023. On the FOB market, spot offers show US corn is no longer cheaper than Brazilian origin, now pricing above both Brazil and Argentina. The combination of a challenging export market and anticipation of a record US corn crop will continue to put a lid on the front month (Dec) CBOT futures. Corn has found strength following adverse US weather conditions and disease pressure across the US crop, but under the bearish fundamentals, spreads should move further lower, towards full carry.

Brazil monthly corn exports by destination (Mt)

Source: Kpler

- While Argentine soybean exports rose in August to 1.9 Mt, the line-up for September is already exceeding this volume. If realised, a second consecutive monthly export volume of at least 1.9 Mt has not been seen in several years and is solely due to Chinese demand. In addition to the sale of domestic soybean reserves, Chinese demand for South American soybeans remains firm as US trade policy prices US soybeans out of competition. The soybean market closely follows any developments regarding the trading relationship between the US and China. However, as the current tariff policy remains undisturbed, CBOT soybean futures are trending lower as nothing substantive has followed since President Trump posted on social media a message urging China to purchase US soybeans.

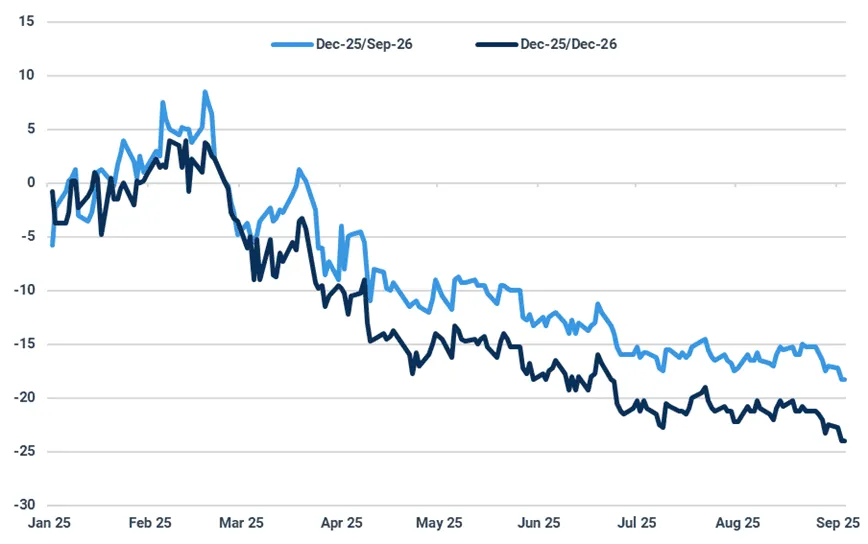

- Canadian wheat exports for August dropped to the lowest volume in the past five years as the increased availability of wheat across the Northern Hemisphere has challenged Canada’s competitiveness. Harvest of the spring wheat crop has just begun in Canada and is facing little weather-related disruption, which will support the replenishment of exportable supply. Russian and Ukrainian FOB offers have begun to slide lower as the availability of exportable supply increases, seeing exports rise. Matif Dec futures are currently trading at an all-time low as aggressive Black Sea wheat prices and the strength of the Euro are causing downward pressure. Calendar spreads Dec-25/Sep-26 and Dec-25/Dec-26 reflect the largest carry since the turn of the new year.

MATIF milling wheat Dec-25 contract under pressure of Europe and Black Sea supply (€/t)

Source: Euronext, MarketView

- In Russia, winter wheat planting for the 2026 harvest has started in the South amid dry conditions. While there is ample window for precipitation to aid soil moisture, traders will closely watch weather fearing a repeat of last year’s dryness during planting. 2025 crop estimates were reduced by more than 10% even before emergence of the crop due to dryness.

- ABARES reported that Australia is close to completing a phytosanitary framework, which would address the concerns China has regarding the historical detection of disease in the rapeseed crop. Once finalised, ABARES notes this would allow for the trial of five rapeseed cargoes to occur, although it has also been reported that at least three separate cargoes have already been booked by COFCO for delivery in Q4 2025. This development comes following China’s preliminary 75.8% tariff on Canadian rapeseed. A trade delegate from Canada is due to travel to China later this week in an effort to resolve the trade tariff. The rapeseed market will closely follow the outcome of this trip, as the RSX2025 contract has declined since the announcement of the tariff due to concerns of weaker export demand.

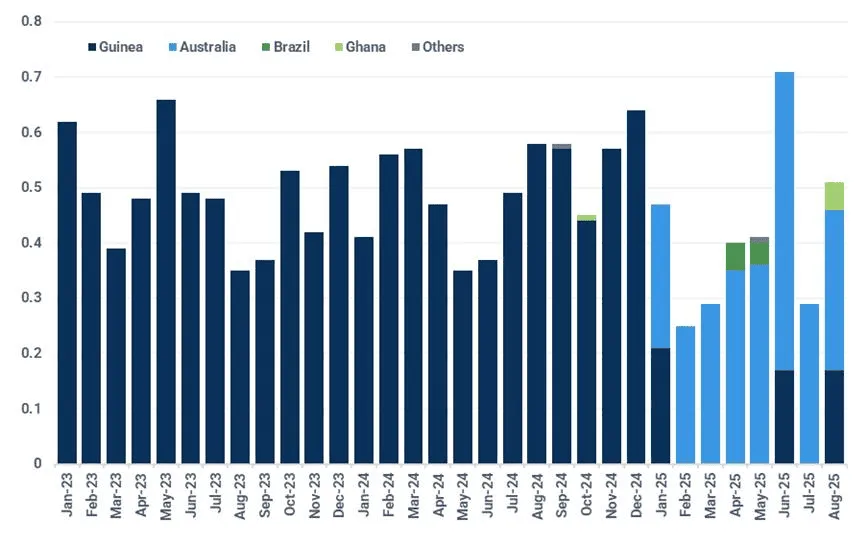

Minor Bulks: EGA continues to source Guinean bauxite via third parties while securing Ghana as a supplier

- Guinea’s seaborne bauxite exports fell to a 12-month low of 9.94 Mt in August, reflecting weather-related disruptions during the peak of the rainy season. Nevertheless, the volumes still represent 14% growth y/y. Looking ahead, exports will likely recover from September after hitting a seasonal low in August. For 2025, we expect annual bauxite shipments from Guinea to expand by around 20% y/y to around 160 Mt.

- Emirates Global Aluminium’s (EGA) Al Taweelah alumina refinery received its second bauxite shipment from Guinea since January. On 28 August, the Capesize Navios Luz delivered over 172,000 tonnes of Guinean Bauxite to the refinery, following a similar shipment by the Winning Progress in June. These shipments are believed to have been arranged by third-party traders, given that EGA’s Guinean subsidiary GAC has been banned from exporting since late 2024 and formally exited the country in August. Guinean bauxite remains a necessity for the Al Taweelah refinery in the near term, as the refinery undergoes “modifications to enhance the refinery’s efficiency in processing other bauxite types”.

- Al Taweelah received over 55,000 tonnes of bauxite from Ghana in August, the largest monthly volume on record, marking a significant step in EGA’s effort to diversify supply. Alongside expanded sourcing efforts, EGA announced the completion of a debottlenecking project at the refinery, which is expected to add up to 0.5 Mt of annual alumina production and reduce reliance on imported alumina.

- Alumina prices on the SHFE continue to trend lower, with the most actively traded January 2026 contract falling 2.71% w/w to 2,980 yuan/t on 4 September, the lowest in nine weeks. Despite temporary maintenance works prompted by environmental curbs linked to the Victory Day military parade, near-record national output and expectations of improving bauxite supply from Guinea have intensified oversupply concerns.

Al Taweelah bauxite imports (Mt)

Source: Kpler

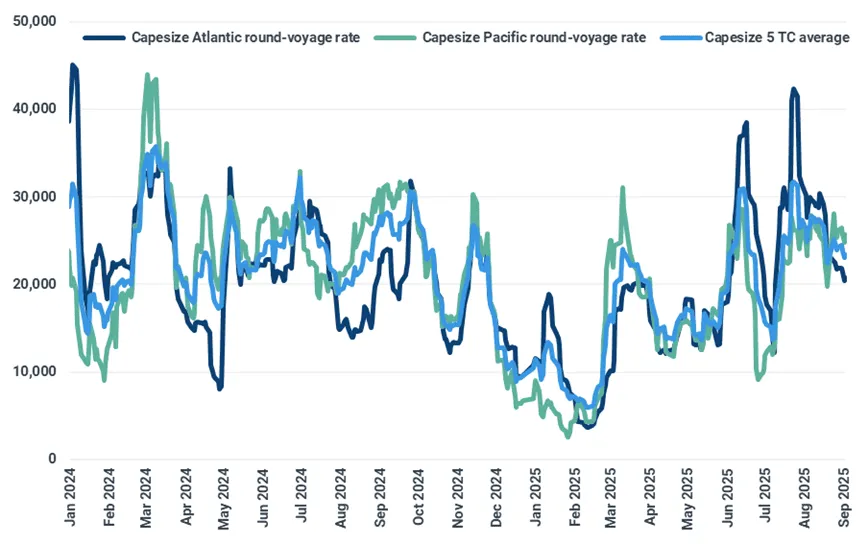

Dry Bulk Freight: Capesize earnings declined to multi-week lows

- A softening in rates across the Atlantic and Pacific basins drove the Capesize 5 TC average earnings to a multi-week low at $22,994/day on 3 September, before it edged higher to $23,355/day. The upturn in ballasters in West Africa, positioning for Guinean bauxite loading, contributed to a weaker Capesize Atlantic earnings with the round-voyage and fronthaul rates declining to $20,729/day and the fronthaul rate close to flat at $32,938/day. However, a rebound in Guinean bauxite chartering following the end of the West African rainy season should increase the uptake of ballasting tonnages and lift fronthaul earnings.

- At $25,655/day, the Pacific round-trip now commands a $4,926/day premium to the Atlantic equivalent. This trend will continue with the seasonal strength of Australian iron ore exports driving demand in the Pacific basin over the short term.

- The Panamax 5 TC average earnings declined by $1,039/day w/w to $15,826/day, driven by weakness in both basins. A public holiday on Monday meant a shorter trading week for loadings in North America.

- Panamax (68k-99,999 dwt) ballast supply in the Pacific surged to 904 vessels (up 8% w/w and 24% y/y) and pushed Pacific round-voyage rates to $13,031/day (down $1,363/day w/w). Peak Chinese summer demand for seaborne coal imports is typically followed by lower shipments in September, which will put further downward pressure on the Pacific basin.

- The Supramax 11 TC average earnings were almost unchanged w/w at $18,467/day, as higher earnings on Black Sea and Atlantic routes cancelled out losses in the Pacific. Black Sea wheat exports are entering a period of seasonal strength. However, there could be delays to exports as vessels scheduled to load wheat at Ukraine’s Chornomorsk port have been instructed to divert to Sulina following an attack on a ship at the former. Chornomorsk has been closed for entry since 1 September. Lotus 6 has been waiting at the anchorage to load wheat at Chornomorsk port since 29 August.

- The Handysize 7 TC average rose by $597/day w/w to $14,152/day, driven by strength in the Atlantic basin, where the rates on HS3 (Brazil-Continent) and HS4 (US Gulf-Continent) rose to year-to-date highs at $19,689/day and $20,886/day on 3 and 4 September, respectively.

Capesize 5 TC earnings driven lower by a steeper Atlantic-round voyage drop ($/day)

Source: Baltic Exchange

Key Dry Bulk Market Developments

Dry Bulk Commodity Flows

Source: Kpler

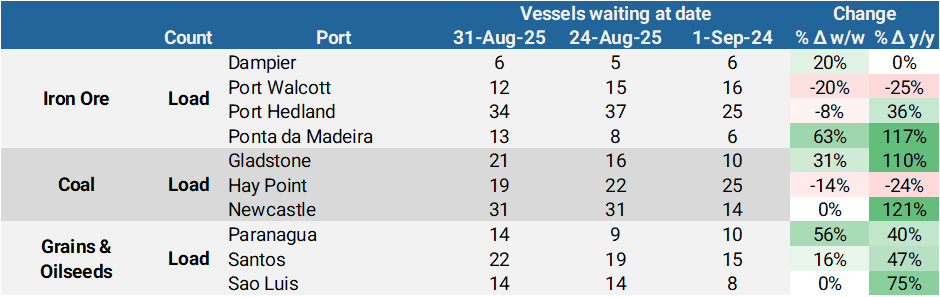

Dry Bulk Port Congestion

Source: Kpler

Dry Bulk Freight Metrics

Source: Kpler, Baltic Exchange

See why the most successful traders and shipping experts use Kpler

Request a demo

Gain clarity on dry bulk flows, rates & fundamentals to navigate market shifts precisely

Request access