May 6, 2025

Iron ore price weakness, coal trade shifts, and agri supply outlook

Iron Ore & Steel: Iranian pellet exports curtailed, iron ore price slides

- Global seaborne iron ore exports reached 129 Mt in April, easing from the March high of 147 Mt but consistent with the previous five-year average. Australian shipments totalled 73 Mt, following the typical post-March decline. In contrast, Brazilian loadings continued their seasonal improvement, rising to a four-month high of 29.40 Mt.

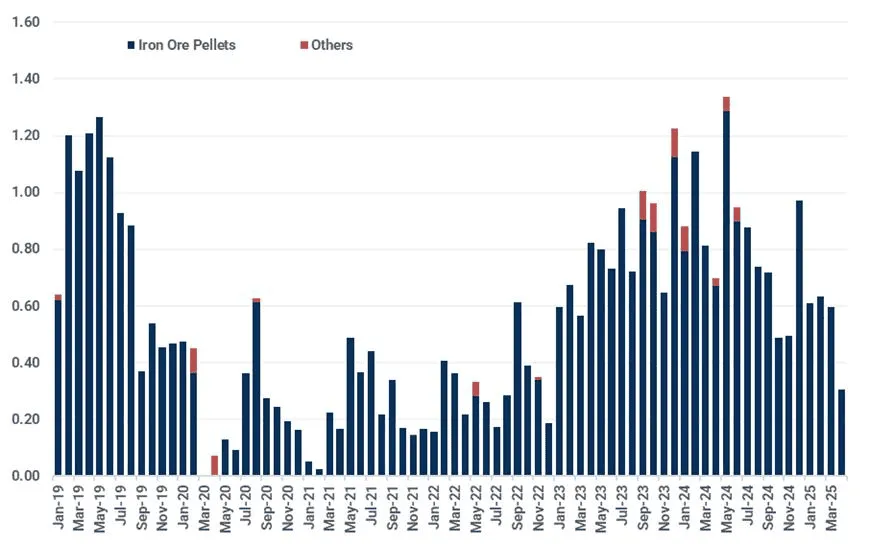

- In Iran, iron ore exports appear to have halted following an explosion at the Bandar Abbas port on 26 April. No vessels have departed since 22 April. As a small iron ore exporter, Iran shipped 10.11 Mt in 2024, overwhelmingly iron ore pellets. China has long been the destination for almost all Iranian iron ore volumes as US sanctions restrict access to other markets. While the disruption may affect a handful of Chinese pellet consumers in the short term, the overall impact on the Chinese and global iron ore market is expected to be negligible, particularly in the current oversupplied market environment. Exports from other Gulf nations, notably Bahrain, continue uninterrupted.

- On the demand front, Chinese seaborne iron ore imports finished at 102 Mt in April, almost flat y/y. Imports are expected to remain firm in May, in line with seasonal patterns. However, potential steel output cuts later this year could still weigh on iron ore demand. Baoshan Iron & Steel, the country’s largest listed steelmaker, has suggested a nationwide production cut is “likely” and forecasts a decline in direct and indirect steel exports by an estimated 15 Mt and 20 Mt, respectively, due to mounting global trade restrictions.

- Iron ore prices weakened over the past week as sentiment soured on the back of anticipated steel production curbs. The DCE’s most traded iron ore contract (Sept 2025) fell by 3.23% w/w to 703.50 yuan/t ($96.72/t) on 30 April, while the SGX TSI 62% Fe June 2025 contract price closed at $95.20/t on the same day. Despite recent declines, $100/t remains an important psychological resistance level for the iron ore price, and we do not expect it to stray too far from this mark in the short term.

Iranian seaborne iron ore exports (Mt)

Source: Kpler

Coal: European thermal coal market slips, petcoke regains competitiveness in Turkey, India

- Metallurgical coal market volumes declined by 600,000t w/w to 4.9 Mt last week. Demand from India and China slipped, with Chinese buyers holding back due to more competitive domestic supply and a weaker economic backdrop. Indian volumes will likely rebound in the coming weeks in line with firm economic activity. India’s interest in Russian hard coking coal has strengthened in recent weeks. Indian coal-fired utilities are also booking more volumes from Russia because of cheaper prices. Given the lack of alternative demand markets, the Russian government is encouraging producers to increase their shipments to India.

Russian coal shipments to India (Mt)

Source: Kpler

- Seaborne thermal coal volumes edged higher by 3.5 Mt w/w to 19.9 Mt, driven by restocking demand ahead of the summer season in the Asia-Pacific region. Chinese demand remains subdued due to peak hydro season, but receipts in India, Japan, South Korea, and Taiwan edged higher as utilities prepare for the peak-summer period. Most of the key demand countries in the Asia-Pacific basin rely on thermal generation to meet power demand, while renewables reduce the need for thermal generation in Europe.

- Thermal coal prices in Europe declined sharply last week to the low $90s/t, dropping by around $10/t w/w tracking weakness in gas markets. Australian high-CV coal is still trading at a discount to the European market, but this discount has narrowed after the recent drop in European prices. Fob South Africa price held steady in the range of $85-90/t, as the primary export market for this grade is India, where stable sponge iron demand and heatwaves support interest.

- Glencore’s 1Q production figures show the company has not scaled down output from its Colombian assets as of 31 March, which is likely to have increased the available volume in the Atlantic basin and offset the impact of India-bound shipments from Colombia in recent months. The announced 5-10 Mt production cut from Cerrejon will shrink availability in the Atlantic basin, as we understand key producer Drummond is also cutting production. Glencore produced 23.4 Mt of thermal coal over January-March, down from 25.2 Mt a year earlier. Metallurgical coal production from Australian assets rose to 1.7 Mt, up by 300,000t y/y, while output from Canadian assets acquired from Teck stood at 6.6 Mt.

- Coal demand from Turkish and Indian cement sectors will ease in the coming weeks as petcoke has regained its competitiveness against coal in both markets. High sulphur petcoke prices fell below $90/t level on a cif Turkey basis last week, implying the price of coal needs to fall below $70/t to remain competitive.

Grains & Oilseeds: US spring crop planting undisturbed by welcomed rains

- The planting pace for US corn and soybean crops is in line with the five-year average at 24% and 18% complete, respectively. Regionally, the planting pace is slightly slower in the US Midwest than in the Great Plains due to varied rainfall. While rains have been forecast for the upcoming two weeks, planting progress is unlikely to be significantly hindered. It is more likely to benefit the establishment of recently drilled crops.

US corn and soybean planting progress (% completed)

Source: USDA

- The percentage of the national US winter wheat crop rated in good or excellent condition increased by four percentage points to 49% on the week ending 27 April, with Kansas rising by six percentage points over the same period. Rainfall over the Great Plains aided winter wheat crop development and tempered dryness concerns. More rains have been forecasted for the upcoming two weeks, subduing dryness concerns.

- Chicago soybean futures have been finding support from the strength of Chicago soybean oil futures following optimistic demand for biodiesel as a feedstock. However, as oil markets have weakened recently, this has weighed on vegetable oil markets, including soybean oil. China has continued to deny that it has been negotiating with the US regarding the trade war between the two nations, adding to the pressure on US soybeans.

- The line-up for exports of French wheat for April could reach a high not seen since April 2024, as exports look to increase for the third consecutive month. After producing its smallest wheat crop in forty years, the export campaign was expected to be below average. FranceAgriMer forecasts wheat exports to drop just below 10 Mt for the first time since at least 1996/97 when the country has recently exported approximately 17 Mt in a typical year.

- After a relatively sluggish start to its crop year, Australian wheat exports are expected to rise in April after finding increased demand from African destinations. Usually, Africa finds much of its wheat demand satisfied by Russia; however, following Russia’s wheat export quota, which tightened up its exportable surplus, Africa sought supplies from alternate origins. Australia’s wheat export campaign has been struggling following China’s continued absence in the cereals market, as in previous crop years, China would account for approximately one-fifth of Australian wheat exports.

- The corn and soybean harvest remains underway in Argentina, at 31% and 23% complete on 30 April, respectively. The corn harvest usually begins slightly earlier than the soybean harvest and the latter was delayed due to heavy rains and high humidity. However, progress has improved on the week due to drier conditions. Exports of both are now rising as the new crop comes online.

Argentine corn and soybean harvest progress (% completed)

Source: Buenos Aires Grain Exchange

Minor Bulks: US Urea prices may hit peak

- Urea prices in the Midwest surged to $555–585/st FOB, up $53/st from last week, marking the highest prices since late 2022. Contributing factors include a 30% y/y drop in April imports, tight UAN availability, logistics delays, and the 10% tariff on imported urea. Increased corn acreage adds further pressure. With spring fieldwork underway, affordability is at its worst seasonal level since 2012, and if planting figures exceed expectations, prices could rise further.

- Global seaborne bauxite exports surged 20% y/y in April to 18 Mt. While this marked a pullback from the record 21 Mt shipped in March, it still represented the third-highest monthly total. Guinea exports surged 27% higher y/y to 13.60 Mt. This strong performance came despite ongoing logistical bottlenecks related to transhipping and tensions between some mining companies and local authorities.

- Alumina prices remain soft due to a persistent supply surplus. The most traded contract on SHFE (September 2025) closed at 2,729 yuan/t ($375.18/t), the lowest since the futures launched in June 2023. The vast majority of alumina producers in China face negative margins at prevailing prices, a dynamic that is likely to maintain downward pressure on bauxite prices.

Global seaborne bauxite exports (Mt)

Source: Kpler

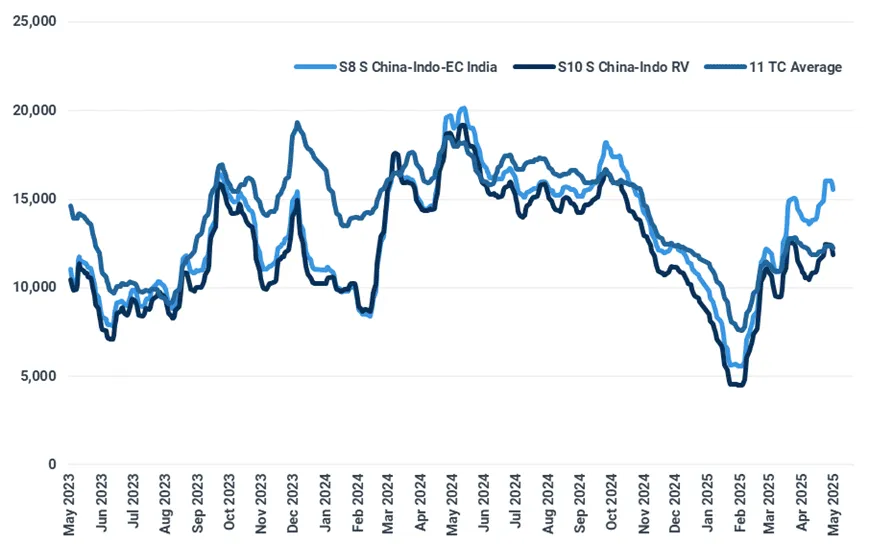

Dry Bulk Freight: Pacific earnings turning bearish for sub-Capesizes

- The Capesize 5 TC average peaked at $16,420/day on 29 April before slipping lower to $16,265/day at time of writing, still higher w/w. Upward momentum was stalled in the short term by a drop off in demand due to public holidays on 1 May, alongside an increase in Capesize supply in the Asia-Pacific region. Nevertheless, a seasonal upturn in Australian iron ore chartering should support earnings, although lower bunker prices will cap the upside for spot voyage rates.

- Softer Chinese coal import demand is weighing on both Capesize and Panamax markets however, the latter has seen additional short-term support from Australian grain exports and wheat cargoes out of West Coast Canadian ports to go with seasonal strength in Brazilian soybean exports. Pacific Panamax earnings declined w/w, but an increase in the Atlantic saw the 5 TC average rise by $794/day net to $12,423/day. The Atlantic round-voyage rate is now higher than the Pacific equivalent for the first time since February.

- Supramax and Handysize TC averages traded sideways this month as support from grains trades was cancelled out by softer Pacific coal trade and downward pressure on Chinese steel shipments and Indian iron ore exports. EV-driven demand that supports minor bulk exports will struggle to offset demand falls elsewhere.

- The Supramax 11 TC average was close to unchanged w/w at $12,224/day, while the Handysize 7 TC average stands at $10,061/day.

- The IMO has approved a global carbon pricing framework and a fuel standard to achieve net-zero emissions by 2050. Effective from 2027, this will see additional fees for owners of high-emission tonnage, adding to voyage costs and potentially encouraging slow steaming. It may be harder for older vessels to find employment amongst cost-conscious charterers, potentially pushing up scrapping.

Pacific Supramax earnings lag on weaker Chinese coal imports ($/day)

Source: Baltic Exchange

Key Dry Bulk Market Developments

Source: Kpler

Dry Bulk Port Congestion

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions - backed by the most accurate oil price predictions two years running.

Unbiased. Data-driven. Essential.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Request a demo

Expert research & analysis driven by proprietary data

Request demo