New European gas transmission tariffs: A growing east-west divide

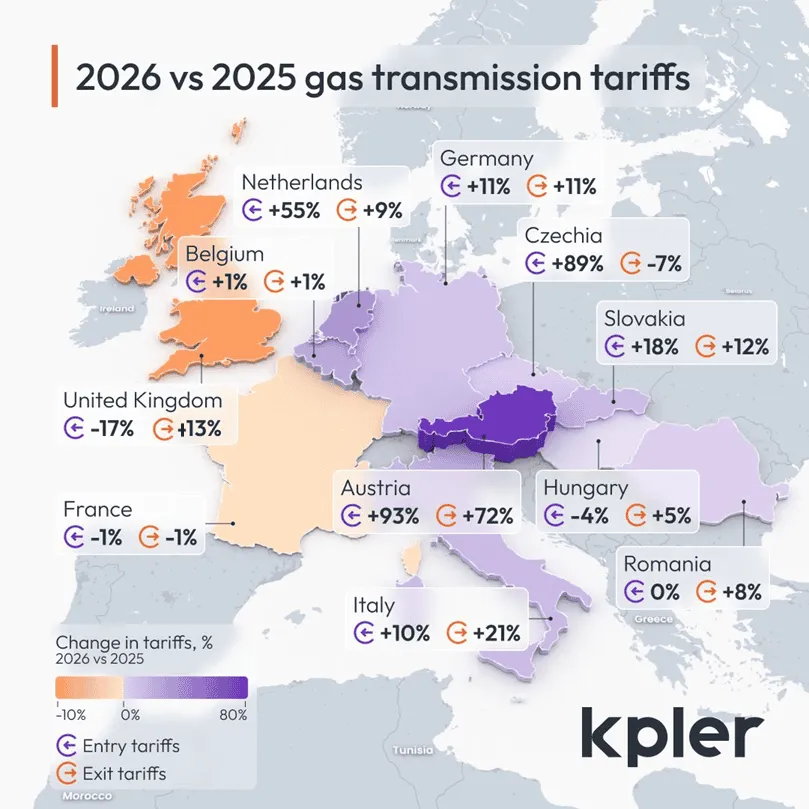

European gas transmission tariffs reveal a growing East-West divide, with stable or lower tariffs in the West but sharp increases in Central and Eastern Europe due to reduced Russian flows. The Netherlands stands out with a significant tariff hike for entry flows driven by lower domestic demand, while rising transmission costs are pressuring Ukraine to seek alternative, more affordable import routes.

Market & Trading calls

- Higher tariffs in the CEE region gas market will likely widen price spreads to TTF

- The Polish corridor to remain a key route for Ukraine’s supply in H2 2025 – 2026

- Bullish pressure on CEE hub prices next year

Call to action: Check the latest transmission tariff updates and real-time pipeline flow data, and explore our new tariff route calculator—now available on Kpler’s recently launched European Gas product.

As most European TSOs have now published their new transmission tariffs for the upcoming gas (or calendar) year, a widening rift between Eastern and Western Europe continues to emerge, driven by evolving gas flow dynamics across the continent. Following the recent launch of Kpler’s European Gas product, Kpler Insight has delved into the analytics behind these tariff changes.

In most of Western Europe, newly announced transmission tariffs have remained relatively stable year-on-year. This reflects, in part, robust pipeline supply and the growing utilisation of LNG regasification terminals, particularly in contrast to developments elsewhere on the continent.

In France, transmission tariffs have remained almost unchanged year-on-year, while aggregate UK tariffs have even decreased by an average of 12%, driven by a 17% reduction in entry tariffs. This move is part of a continued effort to gradually increase the competitiveness of the UK transmission grid, which has historically been burdened by some of the highest entry tariffs in the market, contributing to low utilisation rates at UK LNG terminals.

An outlier in Western Europe has been the Netherlands, where the regulator has increased entry tariffs by more than 50% year-on-year. This sharp rise is primarily driven by lower gas consumption from households and businesses, which in turn raises the per-unit cost of maintaining the grid.

2026 and 2025 gas transmission tariffs, % change

Source: Kpler European Gas

The picture is markedly different in Central and Eastern Europe (CEE), where tariffs are trending higher for 2026. The sharp decline in gas volumes transiting the region, following the loss of Russian pipeline gas via Ukraine on 1 January, has left the grid under-utilised and more expensive to maintain. This has resulted in notable year-on-year tariff increases, particularly in Slovakia (+15%) and Austria (+79%), with Austria’s average tariff set to reach €0.42/MWh.

Although Austrian tariffs remain considerably lower in absolute terms than those of its Slovakian (€1/MWh) or Italian (€0.85/MWh) neighbours, the magnitude of the increase is significant, especially given Austria’s pivotal role as a transit hub for gas supplies from Germany and Italy.

The regional supply situation is further strained by the ongoing outage at the 5.5 bcm Alexandropoulis terminal – one of the key LNG entry points in Central and South Eastern Europe– has been offline for the past 5 months, adding to the market tightness in the area.

2026 and 2025 average gas transmission tariffs, volume (€/MWh, left) and y/y delta (%, right)

Source: Kpler Insight, Kpler European Gas, Amber Grid, Gaz-System. Bars represent the arithmetic average of all entry & exit points in every country.

This tightening environment increases supply risks for Ukraine, which continues to rely on imports from the EU to replenish gas stocks ahead of the winter season. Ukrainian hub prices have surged as a result, with an average premium of €22/MWh over the TTF since mid-June. This compares to a €5.6/MWh premium in Slovakia and an average of around €2/MWh at other major European hubs.

Importing gas through Austria and Slovakia may prove prohibitively expensive, pushing Ukrainian TSOs to explore alternative supply routes. The "northern route" via Lithuania or Poland presents a potentially more economical option. Poland’s average tariffs have risen by a modest 2.7%, while Lithuania’s have actually decreased by 4.4%. However, the Polish TSO Gaz-System has reportedly not renewed the previous 100% discount for LNG storage for the coming year, which could add additional costs for end users, particularly Ukrainian TSOs.

The significant variation in transmission tariffs across Europe is likely to contribute to further divergence in hub prices relative to TTF and to widen competitiveness gaps. Persistently high tariffs in Central Europe raise the question of whether some firm capacity may need to be decommissioned in the short term to alleviate grid-related costs. Conversely, infrastructure debottlenecking in the region could enable higher transit volumes, improving grid utilisation and boosting TSO revenues.

See Europe's gas flows clearly

Kpler European Gas tracks physical flows, capacity, and outages across the European network - so you can move faster than the market.

Want market insights you can actually trust?

Our analysts are updating Insight in near real-time, delivering critical intelligence on trade flows, pricing shifts, and geopolitical risk.

Updates are live across oil, LNG, and cross-commodity sectors.

Request access here.

See why the most successful traders and shipping experts use Kpler

Gain full visibility over European gas markets with Kpler European Gas