Record US supply meets unusually robust demand

Executive summary

Market & trading calls

Americas:

- Neutral US crude supply over Q4 as growth comes to a halt amid a slowdown in efficiency gains and lower upstream activity.

- Optimistic regarding US crude demand, which is rising counter-seasonally as refiners take advantage of robust product cracks.

- Neutral US M1 versus M2 spreads, which will remain volatile over the remainder of Q4, as both US crude supply and demand remain exceptionally strong.

Europe and Africa

- Likely short-term disruptions of Western Russian crude flows with enhanced vessel checks in the Danish straits, targeting the ‘shadow’ fleet

- Neutral-to-pessimistic on Central European runs should refiners struggle to source barrels in case of a longer disruption with the TAL pipeline

- Optimistic on Libyan crude oil production with growing offshore exploration efforts

Middle East and Asia

- Neutral to slightly bearish on Dubai backwardation, as more data indicates rising supply from the Middle East.

- Bullish on Saudi crude exports to China, with Aramco’s November OSPs viewed as “friendly” and Chinese SOEs expected to accelerate SPR replenishment.

- Bullish on Iraq’s capacity expansion, following ExxonMobil’s move signalling a return to the country’s upstream sector.

Americas: Record US crude supply is being met by unusually high demand

US shale supply remains at peak levels

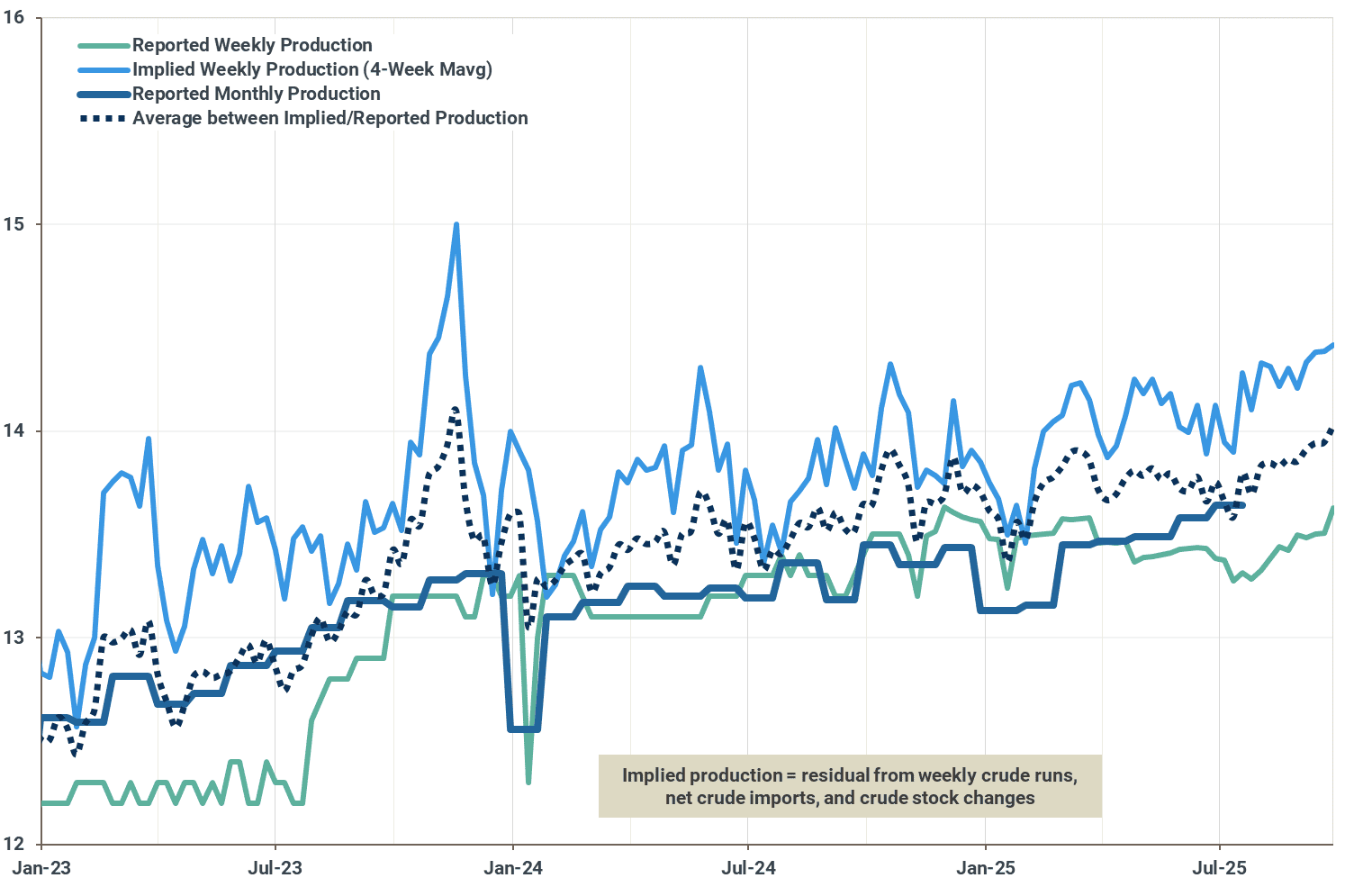

US crude output remains at record highs, with the EIA’s recalibrated weekly figure hitting 13.63 Mbd in early October, which is roughly in line with official monthly data for July. This upward pressure on production continues to stem from significant efficiency gains, as output per new well has risen consistently. According to the latest STEO report, the average output for a new Permian well increased to 1.67 kbd in September, up 0.2 kbd versus year-ago levels. Similar gains in the Bakken, where new wells surpassed 2 kbd for the first time since late 2021, have more than offset declines in the Eagle Ford basin.

However, this growth trajectory appears unsustainable. The number of active rigs in the Permian Basin has fallen to between 250-260, a sharp drop from the 300+ rigs seen last year. This reduction in drilling activity will inevitably lead to a supply plateau in the coming months. Compounded by strong natural declines in other basins, we forecast that overall US crude supply will enter a downward trend in the first half of 2026, signaling a future tightening of the domestic market.

Reported and implied US crude supply, Mbd

Source: EIA

US crude stocks ready to swell despite strong demand

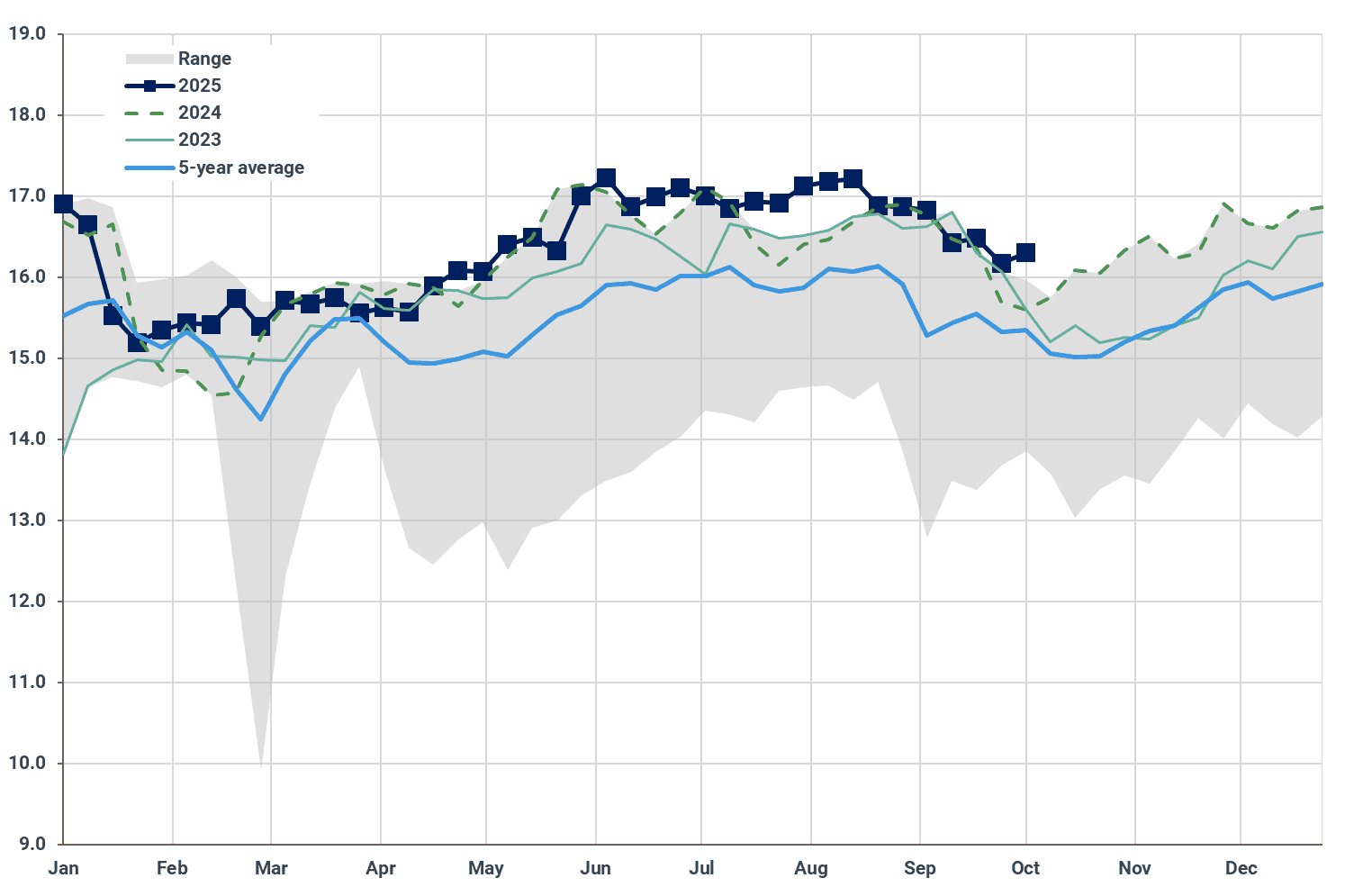

Record-high domestic supply is being met by robust US crude demand, which is supported by elevated crack spreads for refined products. Demand rose counter-seasonally to 16.3 Mbd in early October as refiners either postponed maintenance or kept utilization rates elevated to capitalize on favorable margins. This surge in refinery intake underscores a strong incentive structure in the downstream sector, where product demand is pulling barrels through the system at a rate that defies typical seasonal slowdowns, keeping the market fundamentally tight for the time being.

The upward pressure for crude demand has been largely concentrated in PADD 1, 2, and 3, where consumption is exceeding normal levels by a larger margin. Despite this, US crude stocks recorded an uptick in early October, rising by almost 4 Mbbls week-on-week to 420 Mbbls amid strong production and higher imports. While underlying demand is set to remain firm, the market is entering a period of lengthening balances. We expect this dynamic to drive inventories higher over the next few EIA readings, signaling a near-term supply surplus.

US crude intake, Mbd

Source: EIA

M1/M2 spreads to remain volatile

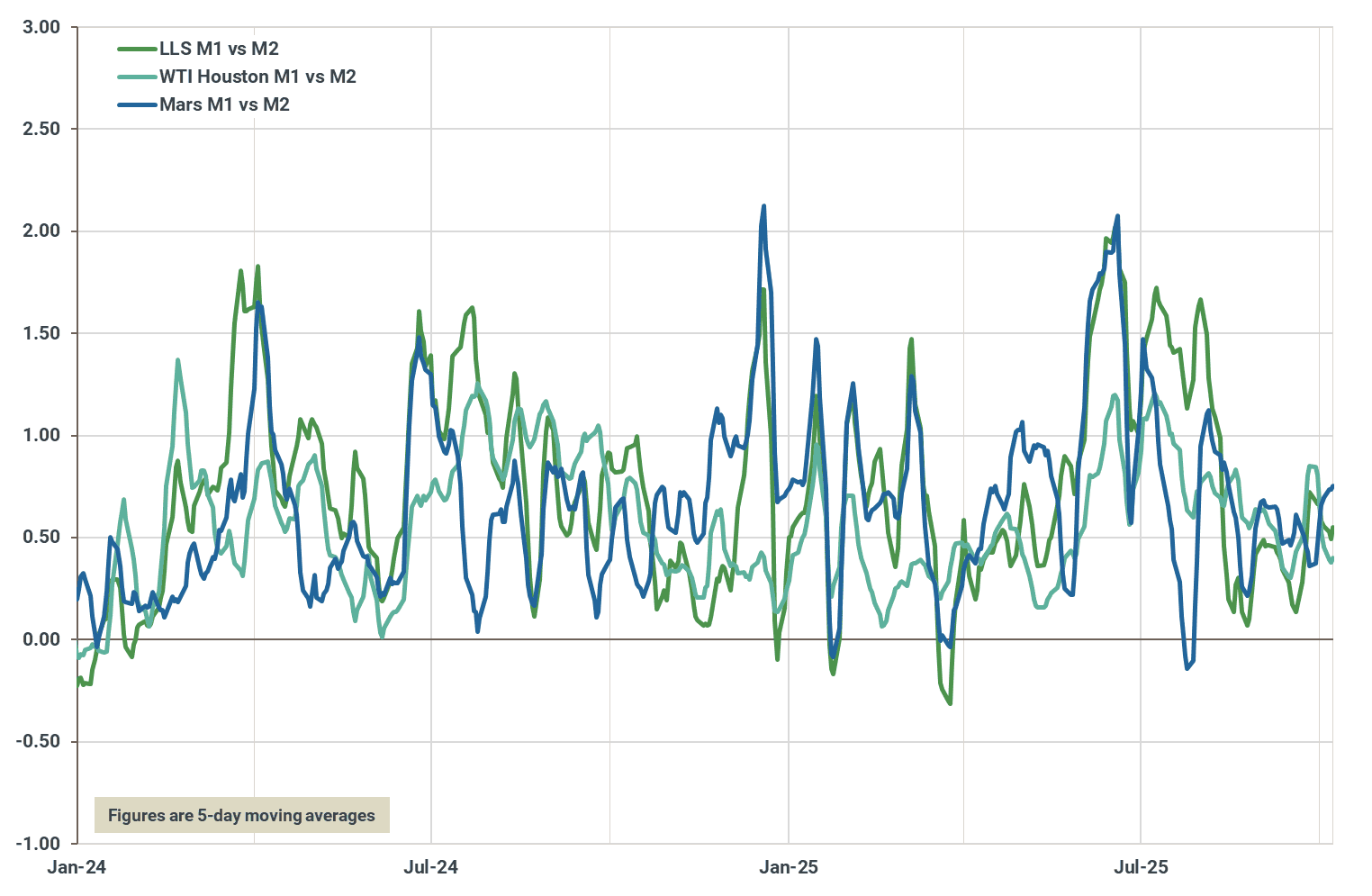

The combination of unusually high US crude supply and elevated demand is keeping regional market structures volatile. Spreads for domestically consumed grades, such as Mars, have seen a minor uptick recently. The Mars M1 versus M2 spread reached a one-month high of around $0.80/bbl this week, reflecting the near-term tightness as refiners continue to run hard. This volatility is a direct result of the market struggling to price in strong, immediate demand against a backdrop of overwhelming supply.

Looking ahead, a brief seasonal dip in US crude demand to 16 Mbd is expected in October, down 400 kbd from September. However, throughput is forecasted to rebound to around 16.8 Mbd by December. While this will provide some support to regional grades, the relief will be limited. Record-high supply of both light (shale) and medium-density (Gulf of Mexico) crudes, coupled with high availability of heavier barrels from Canada and Venezuela, will ensure regional markets remain oversupplied and volatile through the end of the year.

US M1 versus M2 spreads for selected grades, $/bbl

Source: Argus Media

Atlantic Basin: Potential European flow disruptions with logistical chokepoints

Danish Straits environmental checks add scrutiny to Russian Baltic flows

Denmark announced this week that it is significantly tightening its environmental scrutiny of ships at the Skagen anchorage, a critical chokepoint between the North Sea and the Baltic Sea, in a clear move to clamp down on the high-risk "shadow fleet" transporting Russian crude.

The country’s Environment Ministry explicitly stated the goal is to take more effective action against older tankers that pose a particular risk to the marine environment.

This policy directly targets the large number of aged tankers, often with opaque ownership and questionable insurance, that have been acquired to maintain the flow of sanctioned oil.

While Denmark is bound by the 1857 Copenhagen Treaty to allow freedom of navigation, these enhanced checks introduce a new layer of operational risk, including the potential for costly delays, demurrage charges, and vessel rejections.

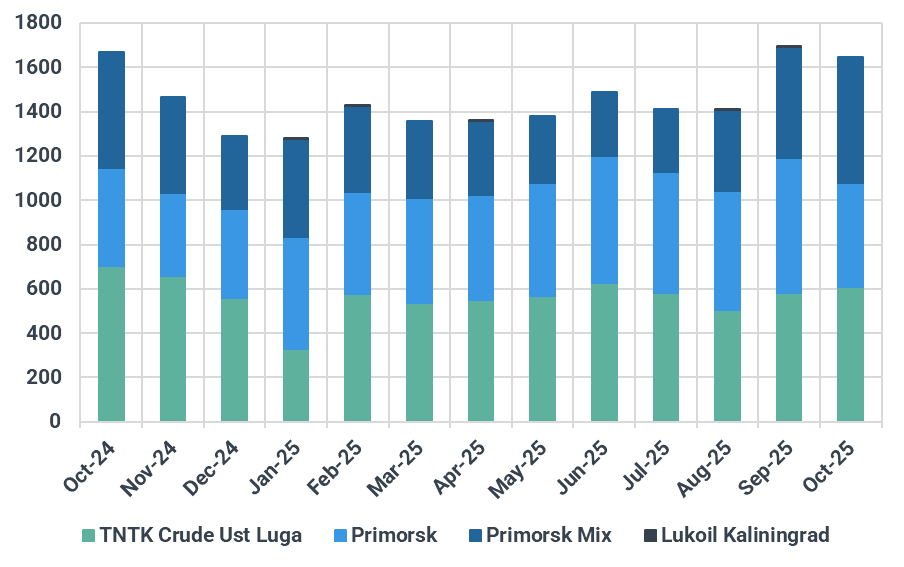

The strategic importance of this waterway cannot be overstated; Russia exported 1.7 Mbd of crude from its Baltic ports in September, which represents 49% of the country's total seaborne exports for the month. Any disruption, however minor, could have significant ripple effects on tanker scheduling and would raise landed prices for Russian barrels into India.

Russian crude exports from Baltic ports, kbd

Source: Kpler

Central European supply faces shock with TAL pipeline maintenance

Central Europe's non-Russian supply chain is facing a significant stress test, forcing the Czech Republic to tap its strategic reserves. Orlen Unipetrol, operator of the country's two refineries, has agreed to a loan of 1.5 Mbbl of oil from the State Materials Reserves Authority to plug supply gaps.

This emergency measure was prompted by a severe drop in deliveries through the Transalpine Pipeline (TAL) system, which has been hampered by extensive modernization and repair work at its origin point, the Italian port of Trieste.

The port works, which are restricting tanker movements and limiting offtake capacity, are expected to continue into mid-November.

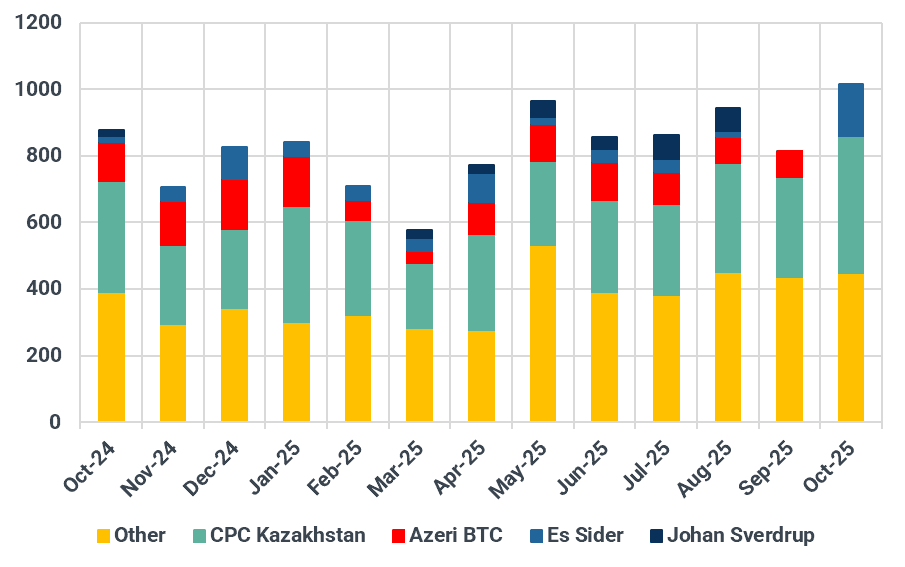

Since the Czech Republic formally ended all Russian crude imports via the Druzhba pipeline in April, the TAL-IKL pipeline network has become the sole, indispensable artery for its refineries. The disruption directly impacts the flow of key seaborne grades, like CPC Blend, Johan Sverdrup and Azeri BTC, which have become the new baseload crudes for the country's 175 kbd refining system.

The need to draw on emergency stocks, a move last seen when Druzhba flows were halted, highlights the fragility of this new supply route and the potential impact on regional grade differentials.

Crude imports into Trieste, kbd

Source: Kpler

Libya’s upstream sector attracts renewed interest

Libya’s oil sector is showing further signs of stabilization as Italian producer Eni resumed exploration drilling in an offshore area for the first time in over five years.

The country's National Oil Corporation confirmed on October 5 that Eni is re-entering an exploratory well. This move is part of a broader trend of returning international interest in Libya, with major producers like BP, Shell, and ExxonMobil all recently agreeing to restart activities amid an improving security environment.

The renewed investment coincides with a significant rebound in the country's crude output, which rose to 1.31 Mbd in August, the highest output since at least the start of 2017. As a key supplier of crude to Europe, the health of Libya's oil sector is critical for the regional balance. Flows from Libya to Europe stood at 1.1 Mbd last month.

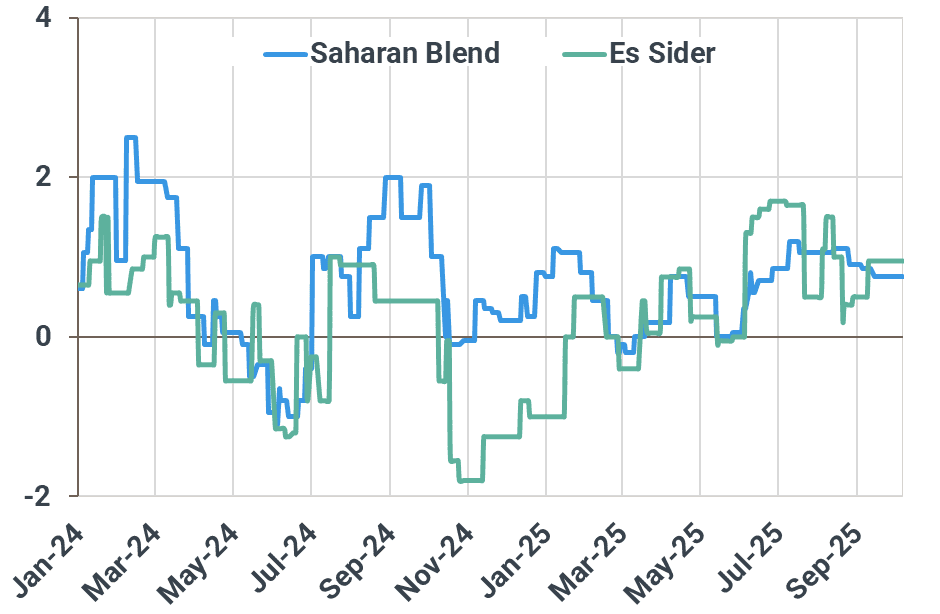

The strength of its supply is reflected in the pricing of its flagship Es Sider grade, which was assessed at around a $1/bbl premium to North Sea Dated at the start of October (Argus Media).

Libyan crude grade differentials to NSD, $/bbl

Source: Argus Media

--

This week’s Atlantic Basin related Market Pulse Reports:

- Med diesel market to tighten as Türkiye and Russia stem supply

- Kurdish crude returns to market, squeezing competing sour grades

- Africa Energy Week 2025: Drill, baby, drill

Middle East and Asia: Dubai backwardation flattens amid supply glut signs

Saudi sets “refiner-friendly” Nov OSPs as OPEC+ presses ahead with quota hikes

Saudi’s state oil giant Saudi Aramco earlier this week trimmed most of its official formula prices for November-loading crude cargoes across key markets earlier this week, another clear sign that the long-anticipated supply glut is starting to take shape. While keeping the flagship Arab Light crude for Asian buyers unchanged, Aramco lowered the prices of Arab Medium and Arab Heavy by $0.3/bbl m/m for the region, broadly in line with our forecast. That compares with the Dubai M1–M3 spread strengthening by roughly $0.3–$0.4/bbl in September, underscoring Aramco’s intent to spur additional liftings from term buyers as global supply growth looks poised to outstrip demand.

Kpler data shows a steady rise in crude oil-on-water volumes over the past five weeks, reaching a 5-1/2-year high of 1,247 mb last week, largely fuelled by higher exports from the Middle East and North America. More Middle Eastern shipments are expected in Q4 as OPEC+ continues to roll back its voluntary cuts—albeit at a measured pace— while regional refineries are set to undergo extensive maintenance in October and November.

As a result, Dubai’s backwardation has eased sharply this month, hovering around $0.8/bbl compared with about $2/bbl in late September, according to Argus Media data. Spot premiums for Abu Dhabi’s Upper Zakum have also slumped to below $1/bbl against Dubai, down from an average of $2.8/bbl last month.

That said, Aramco’s more moderate approach to setting November OSPs may not necessarily trigger a wave of new nominations, as refiners have already covered most of their December-arrival requirements last month, while competing grades are becoming increasingly cost-competitive.

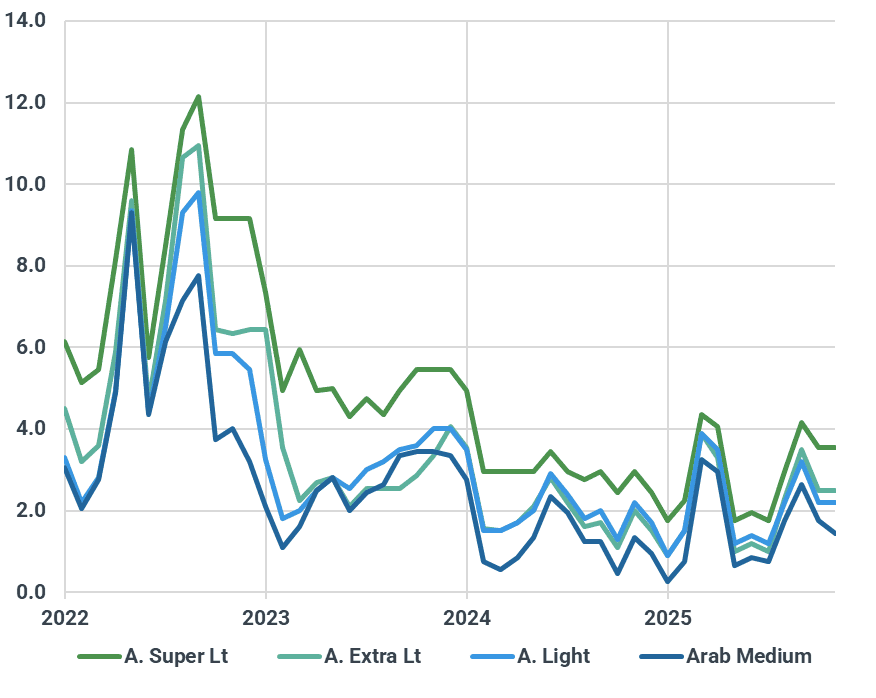

Saudi crude OSPs to Asian clients (vs Oman/Dubai avg), $/bbl

Source: Saudi Aramco

China likely to maintain high November Saudi crude nominations

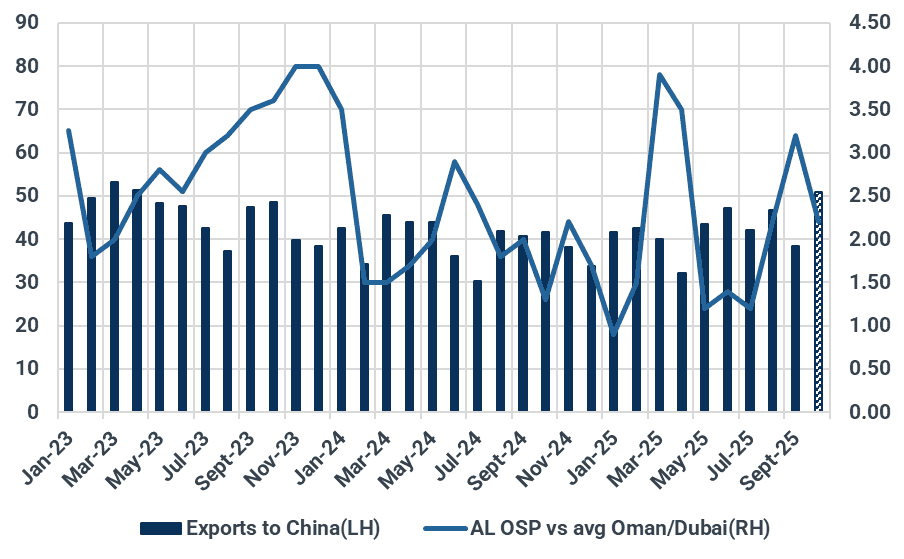

China’s lifting of November-loading Saudi crude is being closely watched, as the market views it as a key gauge of the country’s stockpiling pace and its capacity to absorb the anticipated global supply glut. State-owned Chinese refiners reportedly nominated a combined 51 mb of October-loading Saudi crude, a sharp increase from 43 mb in September, when Saudi formula prices were set above market expectations. The relatively “friendly” November Saudi OSPs are expected to encourage Chinese refiners to keep nominations elevated at around 50 mb, though it remains uncertain whether there is scope for further increases, potentially for strategic reserve refilling.

China’s onshore crude inventories declined in September, reflecting lower seaborne arrivals and strong refinery runs during the month. Given that most of the crude delivered in September was purchased back in June—when prices were elevated amid Middle East tensions—Chinese state oil companies likely refrained from taking extra cargoes at the time for SPR injection. That said, with oil prices softening through Q3 and facing steeper headwinds into Q4, Chinese buyers may have already stepped up—and would keep increasing—both term and spot purchases to advance their SPR refilling program, which is widely expected to continue through end-March 2026.

Arab Light crude OSPs, $/bbl; Saudi crude exports to China, mb

Source: Saudi Aramco, Kpler

ExxonMobil inks deal to boost capacity at Iraq’s Majnoon field

ExxonMobil has signed a preliminary accord with Iraq’s Basra Oil Company and SOMO to advance development of the country’s upstream assets and strengthen export infrastructure. The plan calls for ramping up output at the 240 kbd Majnoon field in southern Iraq, a key stream of the medium-sour Basrah Medium crude. Although oil output expansion will not begin until ExxonMobil finalizes an operating contract, the move signals the U.S. major’s return to Iraq’s upstream sector after its 2023 exit.

The U.S. firm’s re-entry is expected to support Iraq’s goal of raising its crude production capacity to 6 mbd by 2029, up from the current level of about 4.5 mbd. Earlier in 2025, BP signed an agreement with Iraqi partners to boost output capacity at the Kirkuk field by 150 kbd, bringing it to at least 450 kbd within the next two to three years. Meanwhile, state-owned and private Chinese firms are expanding their footprint in Iraq’s upstream sector, as the OPEC producer faces mounting pressure to accelerate project timelines. Production capacity at the West Qurna-1 field, now operated by PetroChina, is targeted to rise by 200 kbd by end-2025 to 750 kbd, and by an additional 50 kbd by end-2028. In May, China’s Geo-Jade Petroleum also agreed to expand the 40 kbd Tuba field to 100 kbd by mid-2027.

Iraq's seaborne crude exports by destination, kbd

Source: Kpler

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Research & analysis driven by proprietary data