April 15, 2026

Shaky ceasefire has yet to unwind the war’s grip on dry bulk commodities

Iron ore markets are poised for stronger exports as Australian and Brazilian shipments recover, though Chinese demand remains weak. Coal prices softened following a ceasefire but remain supported by tight gas supply and potential European demand. Agricultural markets remain volatile, with Hormuz bottlenecks, US drought risks, and robust South American exports shaping the outlook. Aluminium prices remain elevated due to Gulf supply damage, contrasting with weaker alumina amid oversupplies. Freight markets show Pacific-led strength in Capesize.

Iron Ore & Steel: Recovery in Australian and Brazilian flows set to lift global iron ore exports

- Global seaborne iron ore exports finished at 29.74Mt in the week ending 5 April, down 3% y/y but broadly in line with the five-year average. As of early April, Australian daily shipments have recovered to normal levels, following disruptions caused by Cyclone Narelle in late March. Vessels waiting to be loaded in Western Australian ports are also declining from late March highs. This opens the door to stronger-than-seasonal-average global iron ore exports in April, as Brazilian loadings are also recovering from a particularly wet March.

- The ongoing Middle East war continues to exert pressure on the iron ore market. In Australia, while the government’s temporary reduction in fuel excise has provided some relief, structural fuel shortages remain a constraint, particularly for smaller miners. In Oman, to mitigate the impacts of the war, Vale has reportedly brought forward maintenance at its two pellet plants, which together produced 8.73Mt in 2025, equivalent to around 28% of the miner’s total pellet output. Kpler data show that Vale’s Omani facilities have neither imported iron ore nor exported pellets since early March, despite their location outside the Strait of Hormuz.

- Iron ore prices have mostly traded within a relatively narrow range over the past week, but have come under renewed pressure since 8 April. A temporary ceasefire in the Middle East has eased concerns over fuel costs. At the same time, the visit of BHP’s incoming CEO to China has raised expectations of a potential resolution to the dispute with CMRG. As a result, the most traded DCE contract, May 2026, fell 4.10% w/w to 772 yuan/t on 9 April, while the SGX 62% Fe May contract declined 3.32% w/w to $102.85/t at the time of writing.

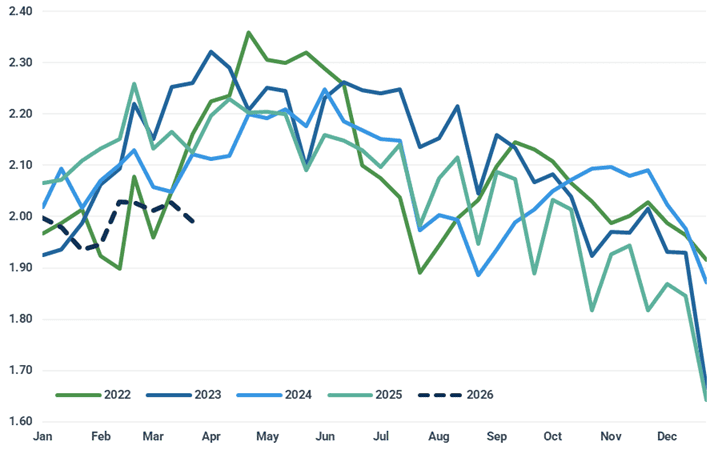

Daily crude steel production by CISA member mills down 6.26% y/y in late March (Mt)

Source: CISA, Kpler Insight

Coal: Coal prices ease with the temporary peace deal

- Coal markets fell steeply in the aftermath of the ceasefire deal, tracking lower gas and oil prices across the energy complex. The month-ahead paper cif ARA contract on ICE traded as low as $105.7/t at 14:35 GMT on 9 April. The temporary peace deal opens the possibility of a resolution to the conflict, though it remains unclear at the time of writing whether it will produce a conclusive agreement. No LNG vessels have transited the Strait of Hormuz since the announcement, with 14 LNG tankers idling in the Middle East Gulf at the time of the report.

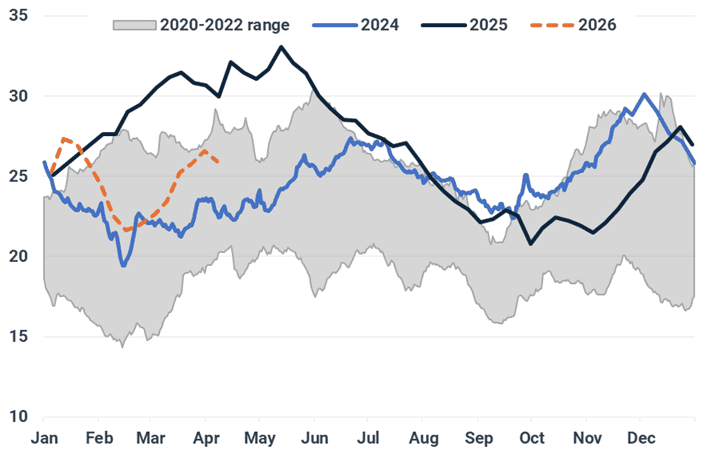

- China's coal inventories in the Bohai Rim edged lower by 650,000t w/w to 25.92 Mt, as month-long maintenance on the Daqin Railway reduced coal transportation. Stocks at Qinhuangdao fell by 300,000t w/w to 6.7 Mt, and stocks at Caofeidian declined by around 500,000t w/w to 12.9 Mt, according to SXCoal data.

Bohai Rim Coal inventories (Mt)

Source: SXcoal

Grains & Oilseeds: US winter wheat crop needs a drink

- The announcement of a two-week ceasefire for the conflict in the Middle East has shed some geopolitical risk, but the situation is still fragile. Vessels laden with grain or fertiliser will be hesitant to transit the Strait of Hormuz. Over the past week, only one vessel carrying grain and oilseed products has passed the Strait, bringing the total number of such transits since 28 February to seven. In contrast, ballast vessels appear less hesitant. The New Ambition, which unloaded soybeans in Bandar Imam Khomeini on 31 March and is now positioned in the Gulf of Oman. Vessels laden with either fertiliser product or feedstock remain bottled in the Middle East Gulf, with no new transits since the Nadab on 22 March.

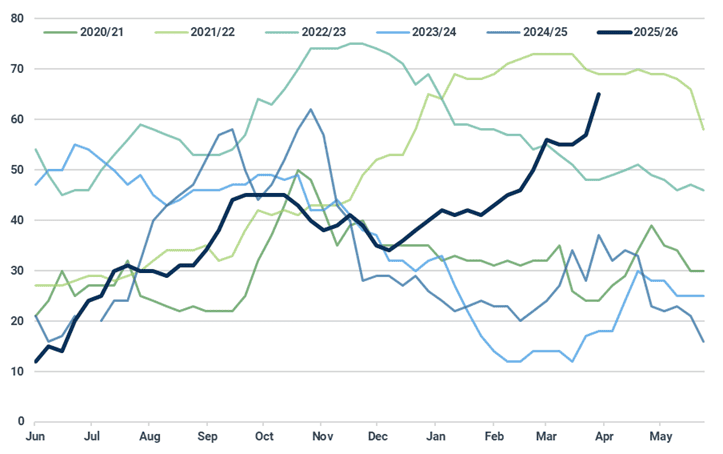

- The US winter wheat crop, experiencing moderate or more intense drought conditions, increased by eight percentage points on the week to 65% by 31 March, the highest for this time of year since 2022. By 5 April, the national crop was rated 35% in good or excellent condition, 13 percentage points less than last year. The forecast of much-needed rainfall across the Great Plains in the next two weeks will partially alleviate production concerns, as the crop begins to transition to key yield-determining growth stages. More rainfall will be necessary in subsequent weeks to support yield potential.

US winter wheat crop in moderate or more intense drought conditions (%)

Source: USDA

Want the complete report?

The full report is available within Insight and contains:

- Iron Ore & Steel: Recovery in Australian and Brazilian flows set to lift global iron ore exports

- Coal: Coal prices ease with the temporary peace deal

- Grains & Oilseeds: US winter wheat crop needs a drink

- Minor Bulks: Aluminium prices defy ceasefire as war damage delays supply recovery in the Gulf

- Dry Bulk Freight: Pacific earnings premium continues

- Key Dry Bulk Market Developments

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Request a demo

Get real-time market intelligence on how the Middle East conflict is reshaping dry bulk trade

Request free trial

![[UPDATE] Running out of barrels: cumulative oil losses reach 430 mbbls](https://cdn.prod.website-files.com/65059ad784ac02253c62356c/69d64fcb4cc368a999bc0b05_sea_at_night_optimized_350.jpeg)