Softer gasoil/diesel values drag refining margins lower in the US and Asia

Some of the uncertainty regarding the EU's latest sanction package seems to have been lifted but fundamentals should provide a floor to middle distillate values. With refinery offline capacity getting more intense in the upcoming weeks, we maintain our positive view on refining margins.

Market & trading calls

Light Ends:

- West of Suez naphtha cracks remain neutral: European fundamentals are improving but lack durability. Refinery outages provide temporary support, yet waning blending and cracking demand will cap the upside and point to renewed softness from H2 February.

- Asian cracks stay moderately constructive: A rebound in Russian exports limits upside, but lingering Middle East refinery outages keep balances tighter. East Asian cracks should continue to outperform NWE, supported by firmer Chinese demand and flexi-crackers favoring naphtha until H2 March.

- E/W spread remains elevated: The E/W spread is set to trade above the five-year average through February and March, as Western fundamentals deteriorate more rapidly than those in the East.

- Propane ratios to diverge regionally: European propane-to-crude ratios should stay marginally firmer into March as tightening supply forces incremental US inflows. Elsewhere, ratios will weaken towards March as fading heating and PDH demand collide with rising field supply from the US and Middle East.

- Butane sees softer West, firmer East: Western ratios will gradually ease into March as blending demand fades and US output recovers. In contrast, Eastern markets find support into March, with cooking and petchem demand growth outpacing expanding Middle Eastern supply, although fading Chinese MTBE margins pose downside risk to this view.

Gasoline:

Slightly bullish West of Suez cracks: Values seem to have bottomed out, with balances set to tighten into February as offline capacity peaks in the US, followed by Europe in March. In Latin America, Brazilian imports are looking solid as blended gasoline gains competitiveness versus ethanol.

Neutral East of Suez cracks: Asian gasoline remains soft at the prompt, weighed down by elevated South Korean exports and weak Indonesian buying. That said, with South Korean turnarounds soon ramping up, seasonal demand improving into Eid al-Fitr, fundamentals should firm from late February.

Middle Distillates:

- PADD 1 remains the key WoS distillate pull: The reopening of the rare NWE–PADD 1 arbitrage underscores persistent tightness along the US East Coast, keeping the region as the primary outlet for Atlantic Basin gasoil and diesel barrels.

- EoS ULSD set to lose momentum: Improving Chinese export economics should lift gasoil outflows in the coming weeks, while steady arrivals from the Mideast Gulf and India rebuild prompt supply and cap further upside.

- EoS jet/kero approaching seasonal peak: The impending end of the Japanese heating season, alongside softening transpacific arbitrage economics, removes a key source of demand support and points to weaker cracks ahead.

Heavy Distillates:

- Neutral East of Suez fuel oil cracks: Singapore HSFO remains underpinned by Venezuela and Iran supply risk and a more backwardated structure. VLSFO has firmed, but momentum is fading as contango persists and steady Kuwait inflows cap further upside.

- Slightly bearish West of Suez fuel oil cracks: HSFO stays weighed by Venezuelan barrels increasingly clearing into both the US and Europe, widening supply options. VLSFO faces structural NWE headwinds, and any boost from US East Coast tightness is likely to be localized and short-lived.

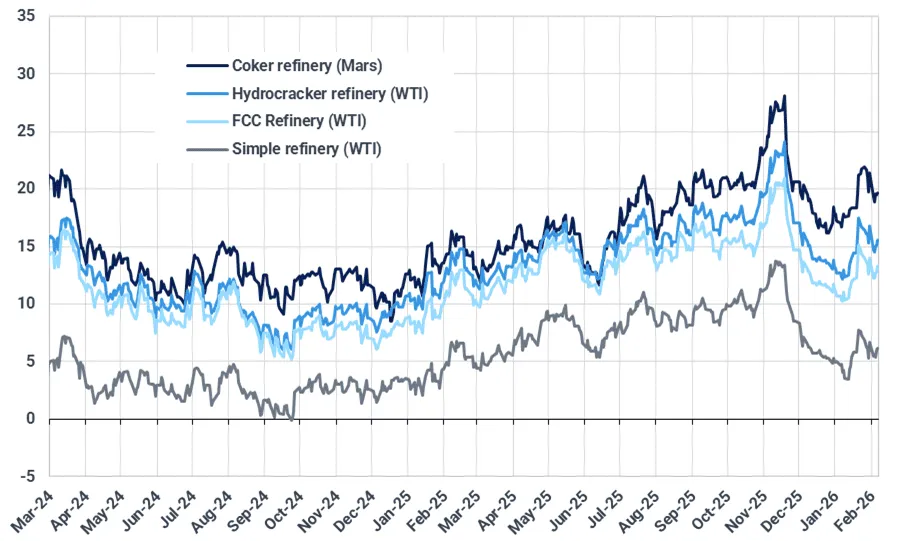

Americas: USGC refining margins soften as middle distillate cracks retreat

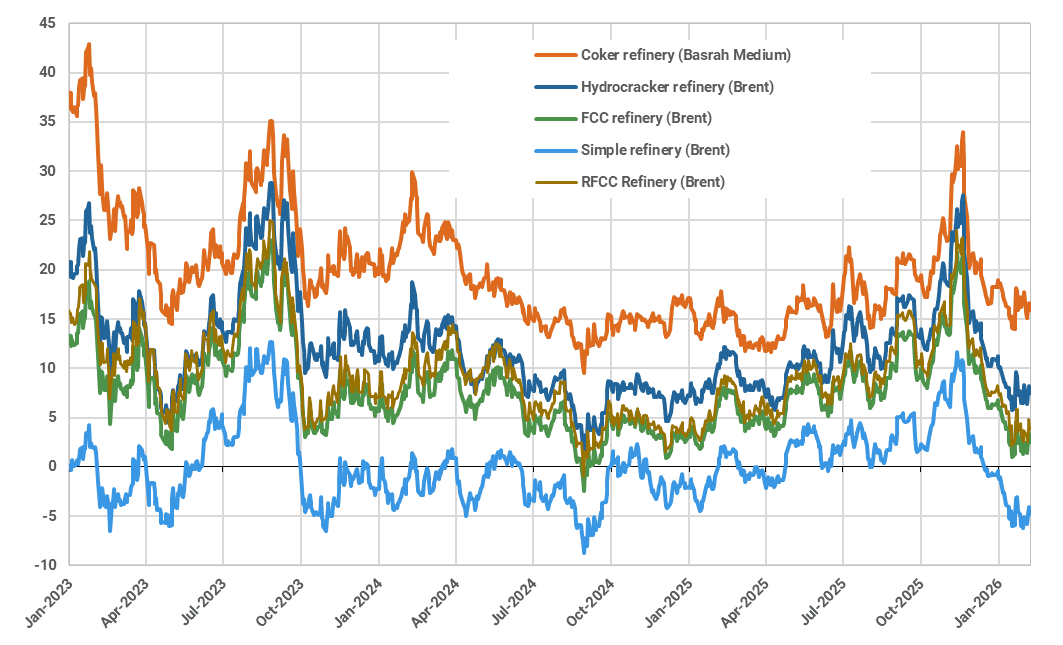

After the previous week’s significant gains, US Gulf Coast (USGC) refining margins eased across all configurations over the reporting week as middle distillate cracks pulled back. Hydrocracker margins fell by $1.15/bbl (-7%) w/w, while FCC refinery margins edged down by $0.85/bbl (-6%) w/w. Margins for complex refineries (equipped with cokers, hydrocrackers, and FCC units) declined by $1.75/bbl (-8%) w/w, while simple refinery margins slipped by $0.55/bbl (-9%) w/w, based on calculations using Argus Media pricing data. With refinery runs reduced during maintenance season, tighter product supply should continue to underpin margins in the coming weeks.

USGC refinery margins ($/bbl)

Source: Kpler calculations based on Argus Media data

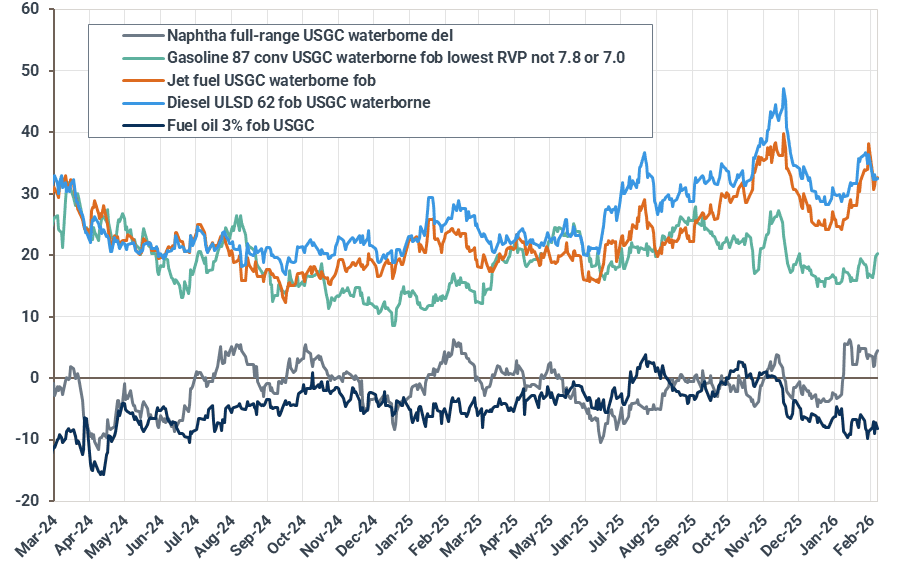

USGC gasoline cracks excluding RVO increased by $0.55/bbl (+6%) w/w, while RVO-included cracks rose by $0.80/bbl (+4%). US gasoline production fell sharply by 820 kbd w/w in the week ending January 30, while implied demand declined by 605 kbd w/w (EIA), reflecting the impact of cold snaps. Inventories have now built for twelve consecutive weeks, although the pace of builds slowed in the second half of January. With winter demand struggling and stocks remaining at the highest seasonal level of the past five years, gasoline cracks will have limited upside in the near term.

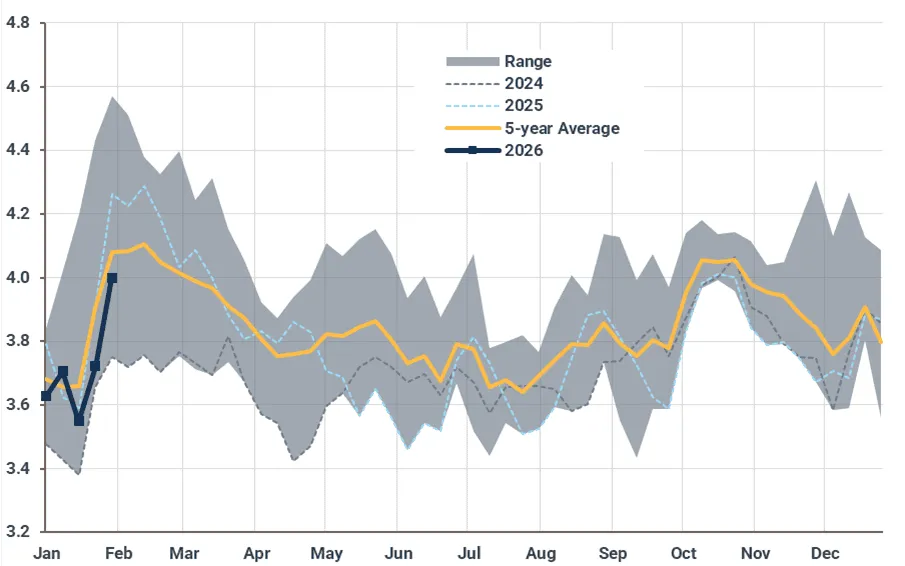

USGC ultra-low sulfur diesel (ULSD) cracks excluding RVO declined by $3.75/bbl (-13%) w/w, while RVO-included cracks fell by $3.50/bbl (-10%), giving back most of the gains from the prior two weeks. Implied diesel demand rose by 240 kbd w/w and by 280 kbd on a 4-week average basis (EIA). Colder temperatures this past weekend should continue to lift heating oil consumption. US diesel inventories drew 5.6 Mbbls in the week ending January 30. Stronger demand alongside lower production is likely to pull stocks lower, keeping diesel cracks healthy in the coming weeks.

US implied diesel demand (Mbd, 4-week average)

Source: EIA

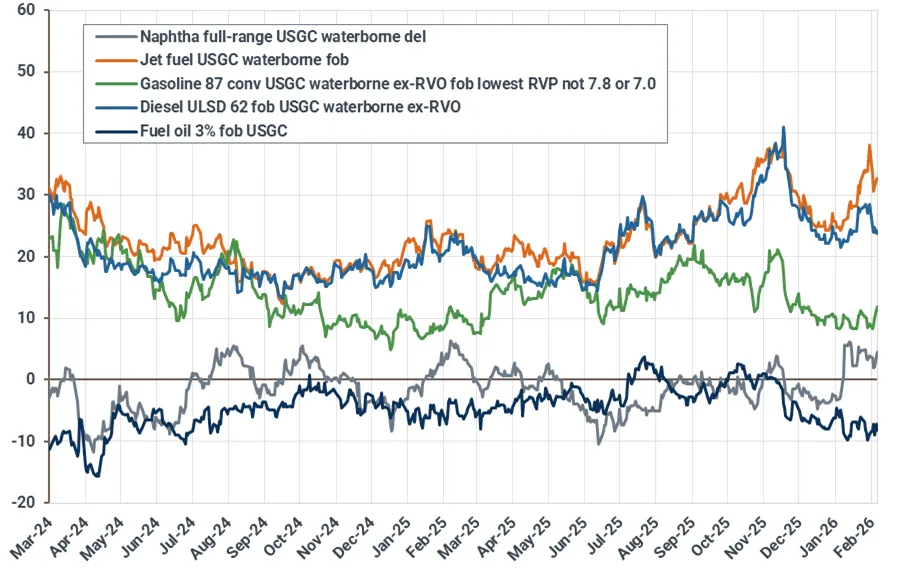

USGC jet fuel cracks declined by $2.65/bbl (-8%) w/w, while the regrade rose by $1.10/bbl to an average of $7.80/bbl. The regrade has strengthened materially since January, pointing to more constructive jet fuel fundamentals. US implied jet fuel demand remains the highest in the past five years, while kero/jet exports reached a multi-year January high since 2019 (EIA). Inventories have moved back within the five range and are broadly in line with year-ago levels. The regrade is likely to remain firm in the near term, although further upside may be limited.

USGC jet regrade – Jet fuel USGC waterborne FOB vs diesel ULSD 62 FOB USGC waterborne ($/bbl)

Source: Kpler calculations based on Argus Media data

USGC high sulfur fuel oil (HSFO) cracks increased by $0.55/bbl w/w to an average of -$7.90/bbl, which was $0.90/bbl lower m/m. Venezuela crude exports to the US more than doubled m/m to 280 kbd in January, a level last seen in late 2024. Greater heavy crude availability ensures internal coker feed, while rising coker offline capacity toward March is likely to further reduce US HSFO/HSSR imports and keep pressure on HSFO cracks.

USGC cracks (excluding RVO) based on Mars month 1 ($/bbl)

Source: Kpler calculations based on Argus Media data

USGC cracks (including RVO) based on Mars month 1 ($/bbl)

Source: Kpler calculations based on Argus Media data

Europe & FSU: Margins eke out marginal gains

Benchmark European refining margins moved marginally higher over the reporting week across the complexity spectrum, in both NWE and the Med. Refinery maintenance activities in the Med are already at a near peak and will remain relatively intense until late-March. By contrast, turnarounds in NWE are negligible at this point and are set to gradually rise from late-February onwards, reflecting different periods of tightness for the two key European regions. At any rate, refining margins should improve over the next couple of weeks as total core refined product balances tighten in the wider region.

NWE Refining Margins ($/bbl)

Source: Kpler based on Argus Media

Med Refining Margins ($/bbl)

Source: Kpler based on Argus Media

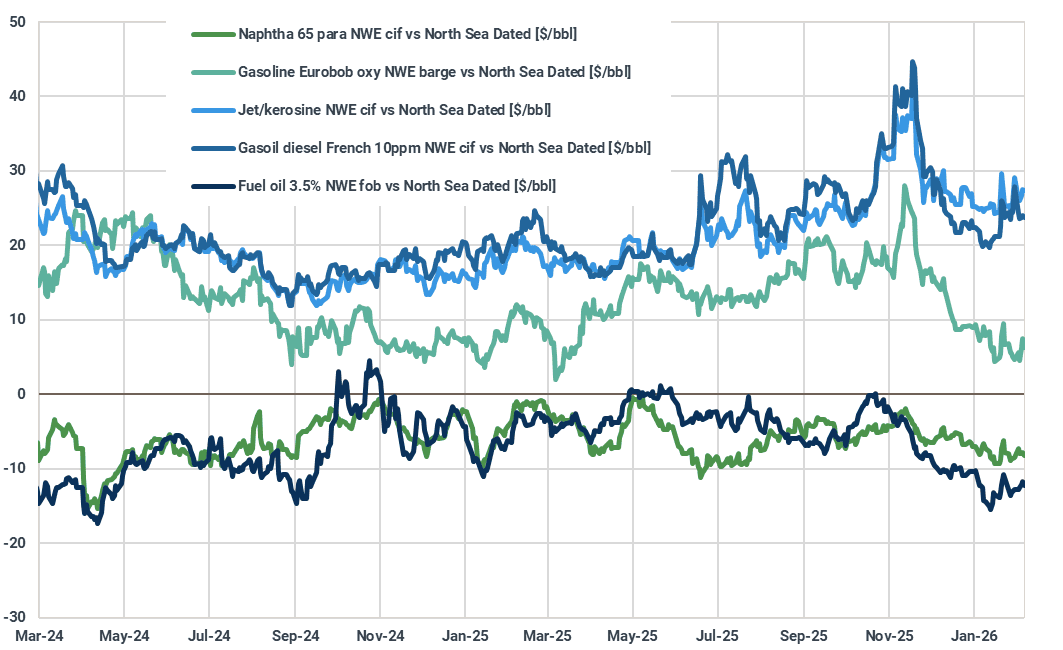

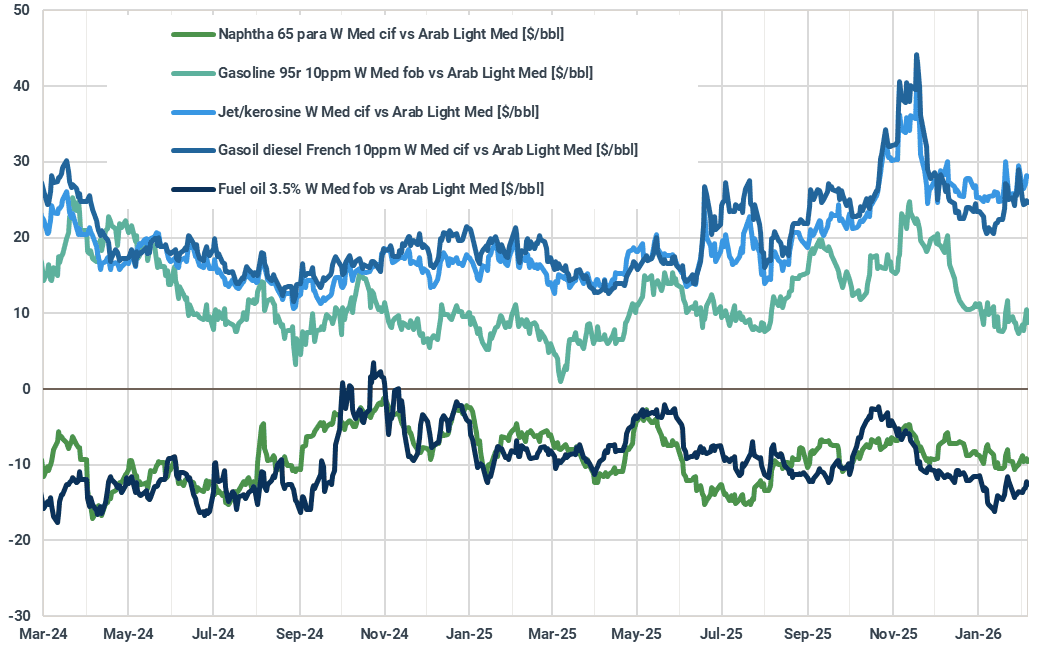

Naphtha cracks added some $0.50/bbl w/w, in both NWE and the Med. Simple margins remain pressured, especially in the former region, keeping supply in check, while demand-side support stems from improved gasoline blending demand. That said, Russian refinery runs are recovering, with West African naphtha imports surging therefrom. In terms of cracking demand, flexi-units continue to favor butane (and propane) over naphtha as a feedstock, while ethylene imports from the US have been rising as of late. With these offsetting factors at play, we maintain our neutral view on naphtha cracks.

Gasoline cracks increased by some $2.00/bbl in both key European regions. Domestic consumption is slowly rising from the seasonal January lull, whereas supply is taking a step lower. EU-27 + UK + Norway gasoline exports have room to pick up, with Brazil possibly offering additional opportunities thanks to favourable price signals from the domestic flex fuel vehicle market, where ethanol has been losing competitiveness lately. That said, total European gasoline exports are still hovering below the multi-year range and they will remain structurally impaired despite prolonged technical mishaps at Dangote, keeping the upside to cracks capped, despite improving fundamentals at home.

Gasoil/diesel cracks shed almost $2.50/bbl w/w in both key European regions. Some of the initial uncertainty about the implementation of EU Article 3ma seems to have been dissolved, with Jamnagar-origin cargoes set to arrive later this month. As such and coupled with prospects of increased suppliers of summer-spec gasoil into Europe in the coming weeks, we should see a moderate recovery in EU-27 + UK + Norway gasoil/diesel imports. By contrast, rare reverse arbitrage cargoes are heading from Europe to PADD-1 amid the lingering effects of cold weather conditions in the US, and coupled with tightening balances in Europe, we remain bullish about cracks. Meanwhile, the European regrade improved by some $2.00/bbl over the reporting week, amid firm aviation demand. When also considering subdued jet/kero imports to EU-27 + UK + Norway, a positive regrade should be maintained but a narrowing is possible should gasoil rally on PADD 1 tightness or geopolitical tensions.

HSFO cracks were up by some $1.00/bbl w/w across the two key European regions. Higher outflows from the US and arrival of heavy material from Venezuela in NWE are pointing to rising imports in February. With bunkering demand taking a hit following the adoption of the RED III rules, we do not foresee much upside to HSFO cracks in the near term.

NWE Cracks ($/bbl)

Source: Kpler based on Argus Media

Med Cracks ($/bbl)

Source: Kpler based on Argus Media

East of Suez: Clean cracks roll over, dragging margins lower

Singapore: refinery margins ($/bbl)

Source: Kpler using Argus Media Pricing

Singapore refining margins lost ground over the past week, tracking the broader pullback across clean product cracks. The regulatory ambiguity around the EU’s 18th sanctions package that had underpinned global middle distillates prices appears to have dissipated, following confirmation that Reliance cargoes have discharged into the EU after the January 21 deadline, according to Argus.

With that uncertainty unwinding, the distillate complex lost one of its key bullish supports, and margins across upgrading configurations moved lower. Coker margins against Basrah Medium fell by $1.54/bbl w/w, FCC margins versus Dubai declined by $0.90/bbl, and hydrocracker margins against Dubai slipped by $0.76/bbl over the same period. Simple refinery margins held up relatively better, easing by $0.44/bbl w/w, as the relative resilience in 380 CST HSFO cracks provided a partial floor to the downside.

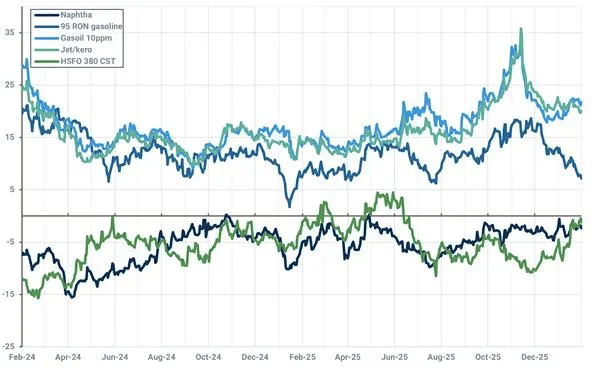

Singapore naphtha cracks rose by $0.34/bbl over the week, standing out as the lone outlier in an otherwise bearish clean products complex. The strength was driven by a combination of factors, including a relatively lighter cracker maintenance schedule this month and economics that continue to favor naphtha use at flexi-feed steam crackers. Even so, the upside looks fragile. Resurgent Russian naphtha exports are expected to rebuild regional supply over the coming weeks, which should cap any further gains and keep cracks under pressure.

Singapore 95 RON gasoline cracks fell by $1.61/bbl over the week, reflecting a softer spot market where Indonesia – the region’s single largest importer – has remained notably circumspect ahead of the typical Ramadan stockpiling season. The recent mechanical completion at the Balikpapan refinery has allowed the country to reduce its reliance on imports and instead lean more heavily on domestic blending.

Singapore ULSD cracks fell by $0.71/bbl over the week, while jet/kero cracks declined by a steeper $1.09/bbl w/w. The pullback reflects a market where the EU sanctions risk premium is beginning to unwind, with underlying fundamentals no longer justifying the earlier strength. The recent turn in Chinese oil product export economics – now strongly positive for both distillates – is also set to drive a sharp increase in gasoil and jet/kero exports, adding fresh pressure to the regional spot market. At the same time, healthy inflows into the region have pushed Singapore distillate inventories to nine-week highs, removing any residual impetus for further gains.

Singapore HSFO cracks rose by $0.77/bbl over the week, reflecting persistent supply concerns tied to geopolitical flashpoints in Venezuela and Iran. The strength in cracks has also been reinforced by tightening regional balances, with recent draws in onshore stocks and a parallel reduction in floating storage pointing to firmer spot conditions. That said, the rally looks vulnerable. Weakness across West of Suez fuel oil markets is likely to incentivize incremental Middle East cargoes to flow East, rebuilding regional supply and easing Singapore HSFO cracks in the weeks ahead.

Singapore product cracks ($/bbl)

Source: Kpler using Argus Media Pricing

Charts

USGC: Gross Refinery Margins Forecast ($/bbl)

Source: Kpler

NWE: Gross Refinery Margins Forecast ($/bbl)

Source: Kpler

Med: Gross Refinery Margins Forecast ($/bbl)

Source: Kpler

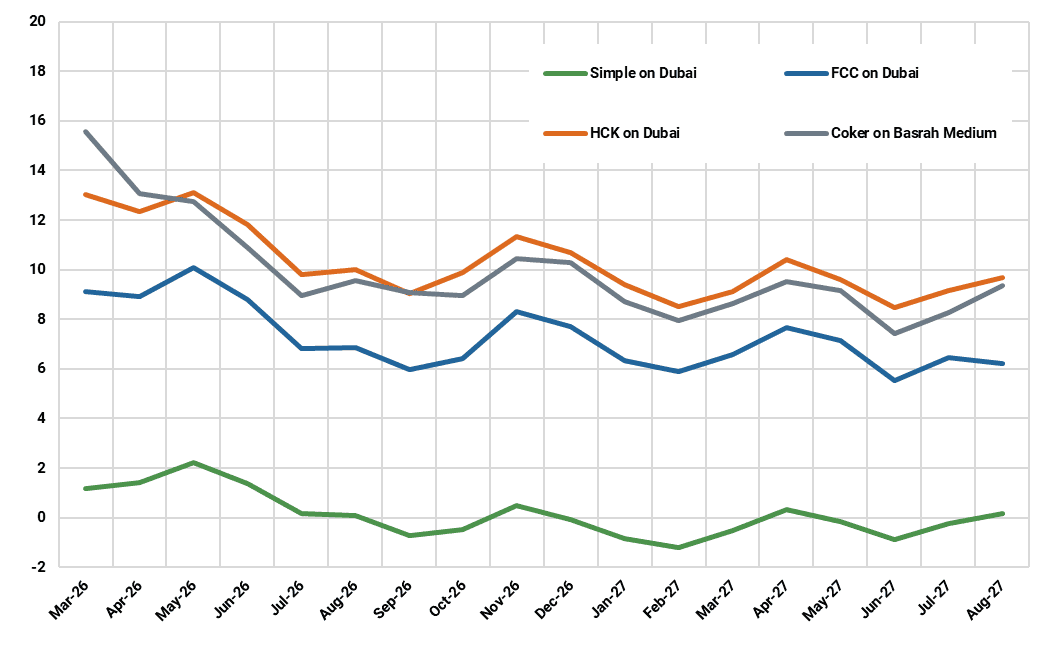

SG: Gross Refinery Margins Forecast ($/bbl)

Source: Kpler

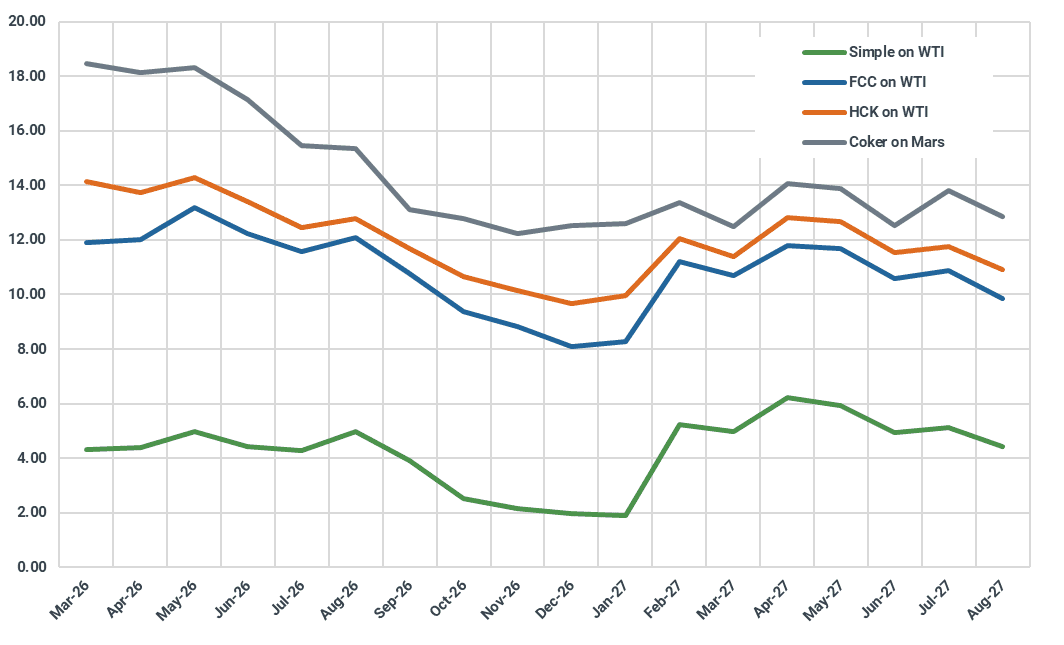

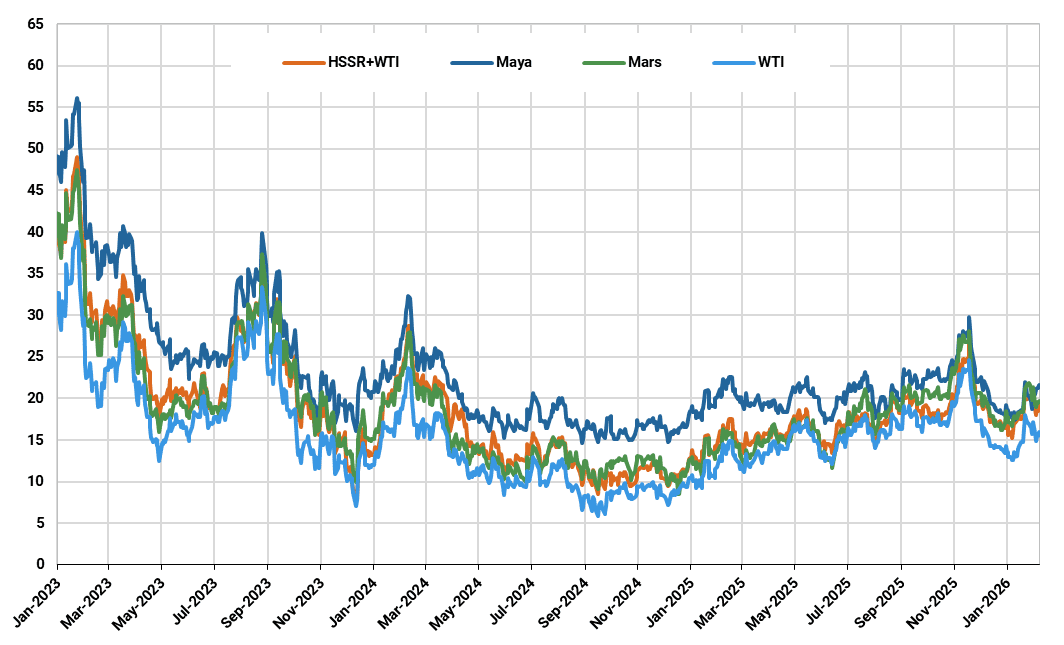

USGC: Coker conversion refinery margins for different feeds ($/bbl)

Source: Kpler based on Argus Media

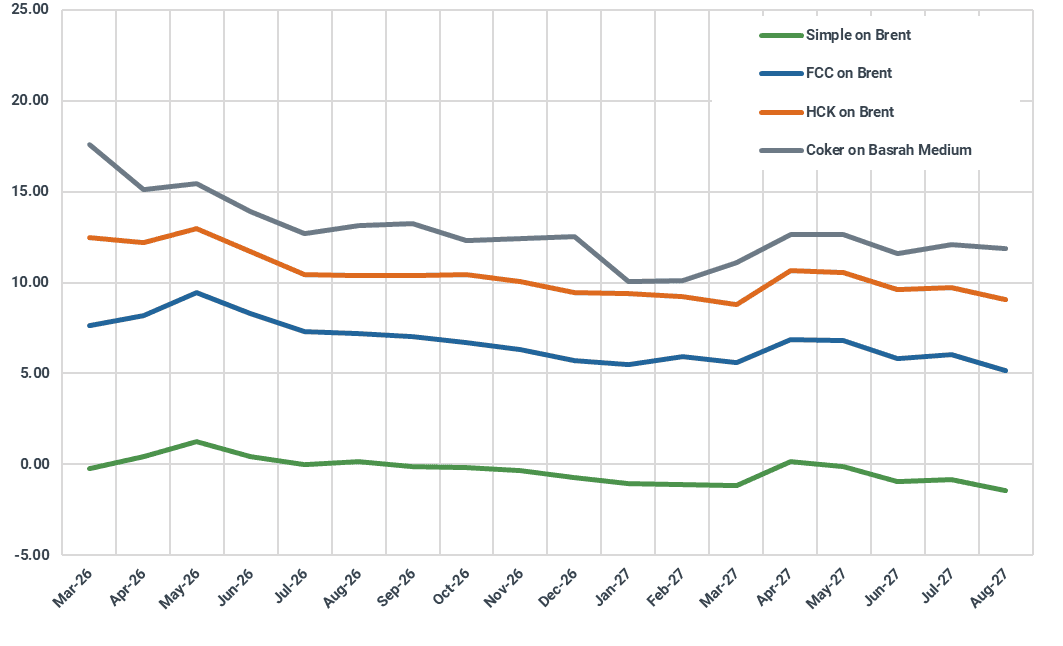

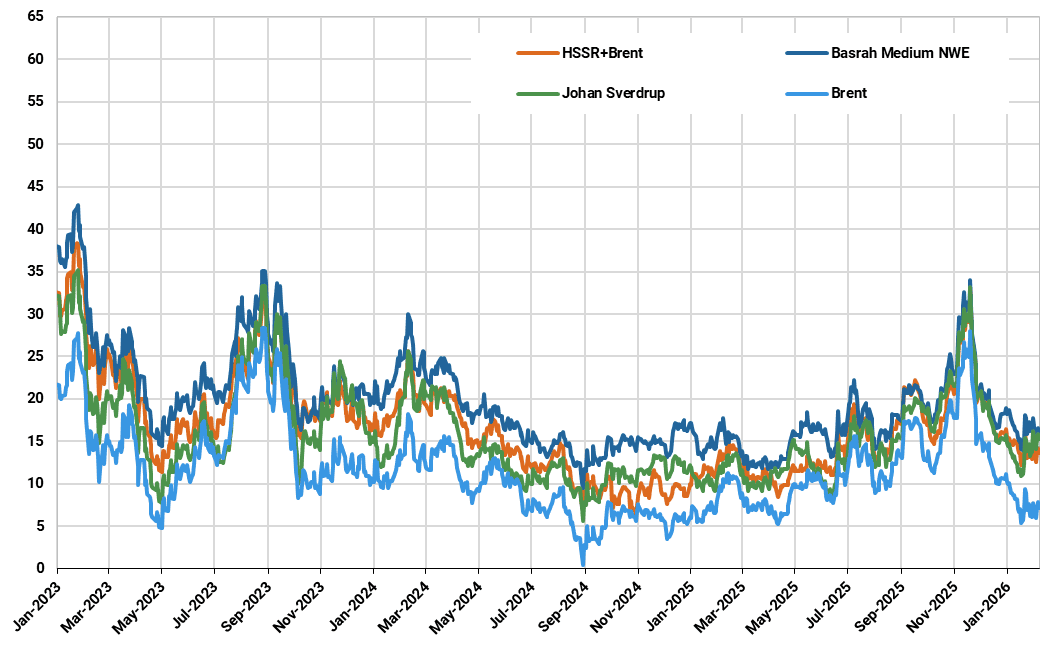

NWE: Coker conversion refinery margins for different feeds ($/bbl)

Source: Kpler based on Argus Media

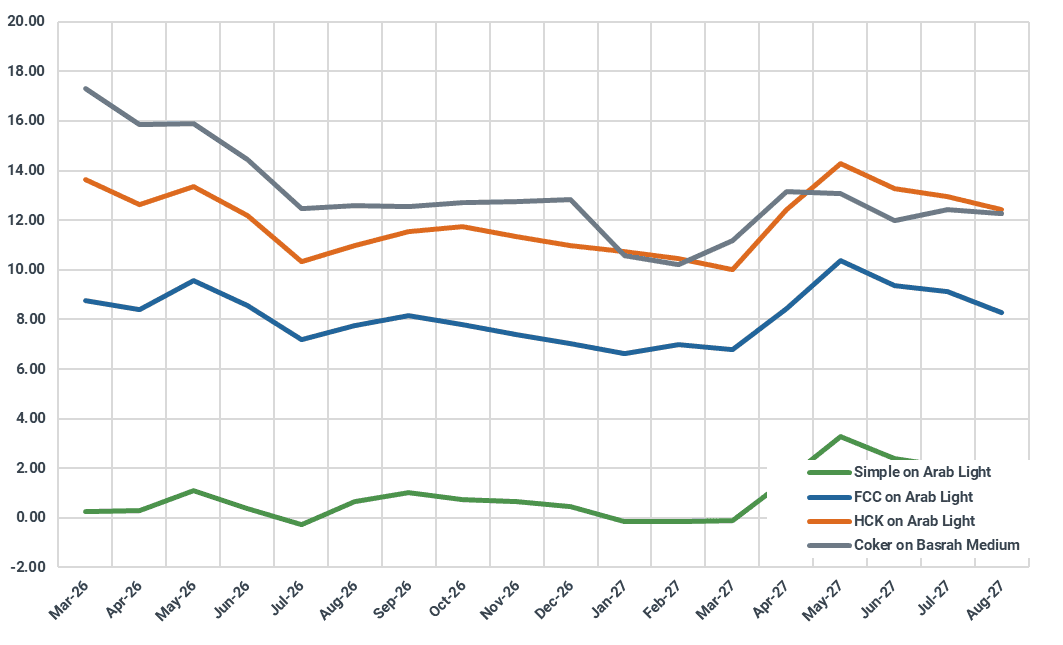

Med: Coker conversion refinery margins for different feeds ($/bbl)

Source: Kpler based on Argus Media

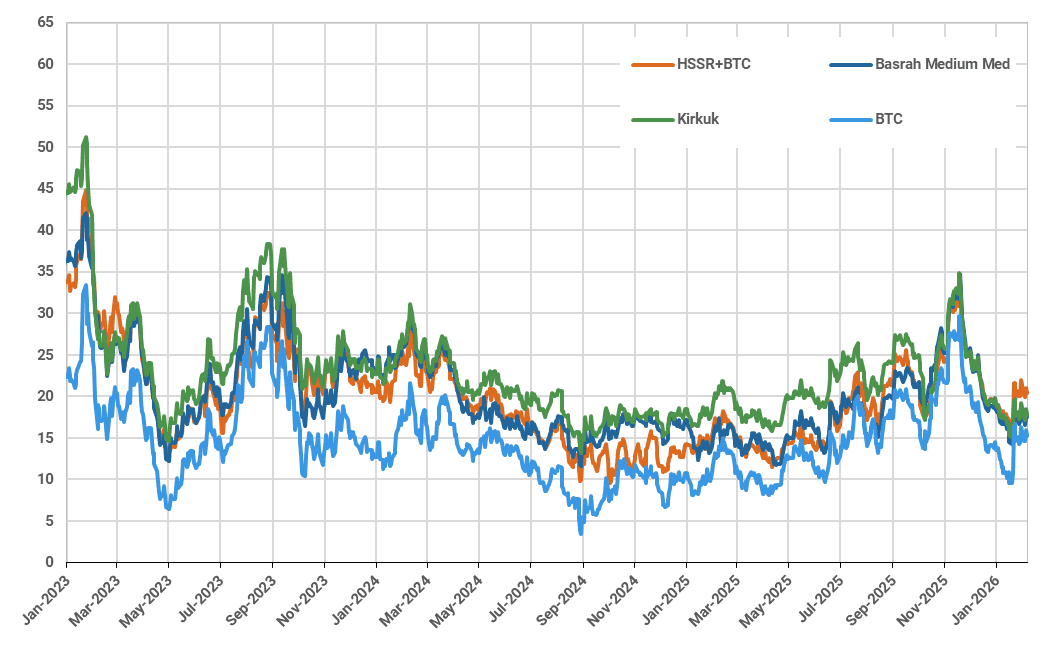

SG: Coker conversion refinery margins for different feeds ($/bbl)

Source: Kpler based on Argus Media

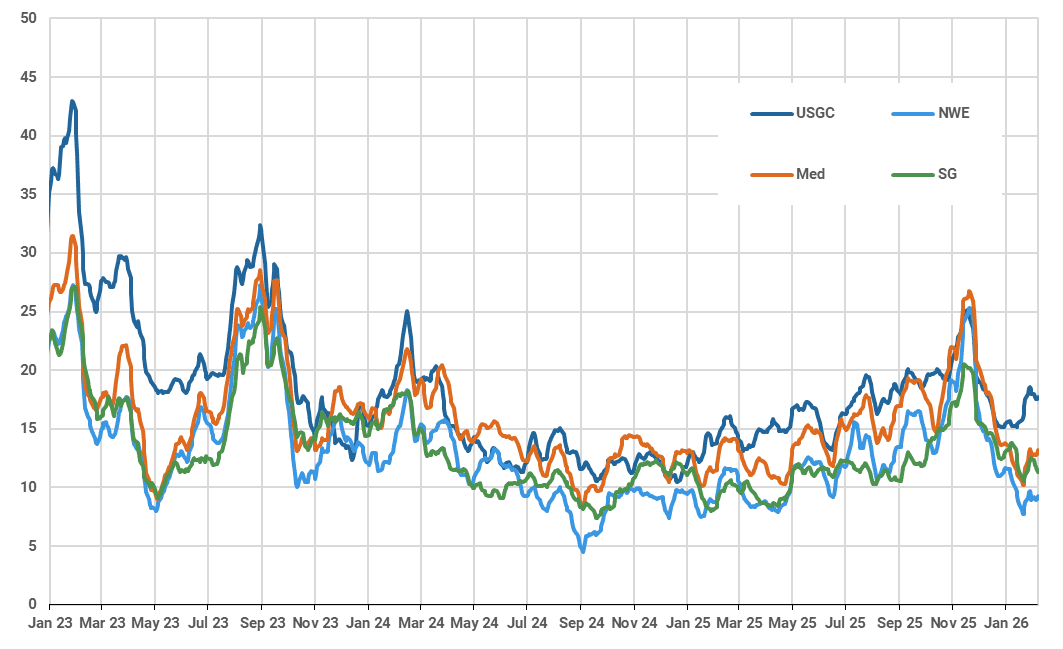

Refining Margins Complexity weighted (5DMA, $/bbl)

Source: Kpler based on Argus Media

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler