Strikes on Alba and EGA smelters enhance the possibility of $4,000/t aluminium

In retaliation for US and Israeli strikes on its steel facilities, Iran has struck Alba and EGA’s Al Taweelah smelters, placing half of GCC aluminium capacity at risk. Under two disruption scenarios, the damage to these facilities could result in potential production losses of between 1.13Mt and 1.79Mt in 2026. Should the conflict escalate to affect additional smelting capacity across the region, the global aluminium deficit would significantly deepen and push LME benchmark prices towards $4,000/t.

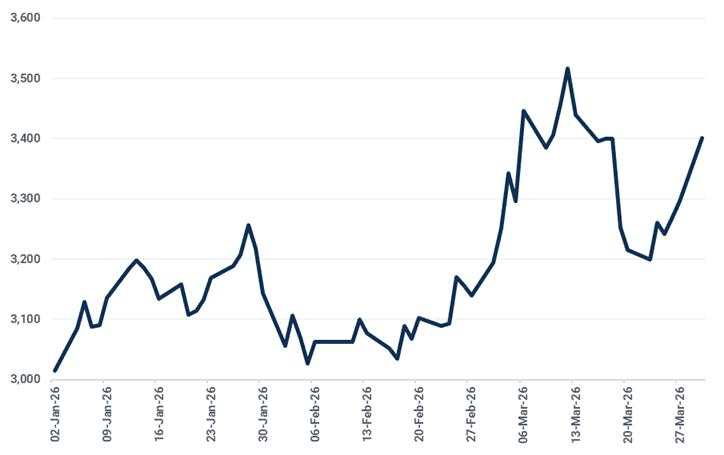

Half of GCC’s aluminium capacity attacked on 28 March

The escalation of hostilities in the Gulf has dealt a fresh blow to the global aluminium market. On 28 March, EGA’s Al Taweelah smelter (capacity: 1.50Mtpa) in the UAE and Alba’s smelter (capacity: 1.60Mtpa) in Bahrain were struck by Iranian missiles and drones. Together, the two facilities account for nearly half of the GCC’s aluminium capacity. The three-month LME aluminium contract rose 3.19% to $3,401/t on 30 March, near the four-year high of mid-March.

The LME aluminium benchmark jumped on 30 March following attacks on smelters ($/t)

Source: MarketView, Kpler Insight

Before the strikes, aluminium production and exports in some GCC countries had already experienced significant disruptions:

- Alba declared force majeure on 4 March for aluminium deliveries and announced on 15 March that it had initiated a controlled shutdown of 19% of capacity.

- EGA had already begun diverting exports through Omani ports and leveraging inventories held outside the UAE.

- Qatalum (capacity: 0.64Mtpa) had reduced output to around 60% capacity following cuts in gas supply from QatarEnergy.

What will happen if the attacked smelters are partly shut down? And if there is more to come?

We outline two scenarios to assess how the latest strikes could affect the production of EGA’s Al Taweelah and Alba smelters:

- In Scenario 1, moderate damage, both smelters cut running capacity to 50% until the end of Q3, and restart the rest 50% capacity from Q4. Combined production in this scenario could be reduced by 1.13 Mt in the whole of 2026, compared to the pre-war forecasts of 3.12Mt for the two smelters.

- In Scenario 2, severe damage, both smelters cut running capacity by 80% until the end of Q3, and restart the rest 50% capacity from Q4. Combined production in this scenario could fall 1.79Mt this year.

Alba and EGA’s Al Taweelah’s 2026 production in different capacity cut scenarios (Mt)

Alba

Source: Kpler Insight

EGA’s Al Taweelah

Source: Kpler Insight

Whether a production loss of 1.13 or 1.79Mt would significantly widen the projected global deficit, which had already been estimated at around 0.50Mt for 2026 prior to the outbreak of war on 28 February.

Why does Q4 2026 production remain low even if a restart is expected in both scenarios? Based on precedents from other smelter outages, we expect only around 20% of curtailed capacity to return in Q4 under a relatively optimistic case. The slow ramp-up reflects the technical challenges, as once the pots that hold the molten metal are cooled, particularly following an unplanned shutdown caused by physical damage, returning to full capacity would be a slow process. The process may be further delayed by difficulties in securing replacement equipment and components amid ongoing conflict-related disruptions.

What if more attacks are to come? If other GCC smelters, including EGA’s Jebel Ali (capacity: 1.20Mtpa), Ma'aden’s Ras AI Khair (capacity: 0.90Mtpa) in Saudi Arabia and Sohar (capacity: 0.40Mtpa) in Oman, are attacked and face partly or complete shutdown, global aluminium deficit could be pushed to over 2 or even or 3Mt, even as allowing for some demand destruction linked to the energy shock. Under such conditions, the LME aluminium benchmark could breach $4,000/t, although the durability of such levels would remain uncertain.

Securing enough alumina supply remains a big headache for GCC smelters

While the previous scenarios assume sufficient alumina availability to sustain reduced operations and enable future restarts, the reality is more challenging. Securing adequate supplies of both alumina and bauxite could become a critical constraint for GCC smelters, even in the absence of further Iranian attacks.

Although both Alba and EGA have managed to source limited volumes via alternative routes, these remain insufficient to meet mid and long-term operational requirements:

- EGA is estimated to have imported around 0.07Mt of alumina via Oman’s Sohar port in March, as Omani imports were abnormally high, with volumes 0.07Mt above the previous five-year average. However, this figure is well below its typical monthly requirement, particularly given that the disruption to bauxite imports, which averaged 0.46Mt over the previous 12 months, necessitates a higher alumina intake. To sustain the 2025-level output of 2.60Mt of primary aluminium, monthly alumina imports would need to reach 0.42Mt.

- Alba imported only 0.02Mt of alumina from Saudi Arabia’s Ras Al Khair in March, compared with the previous 12-month average of 0.24Mt per month from traditional suppliers. Even at reduced operating rates of around 20% capacity, this level of supply would fall well short of the estimated 0.15Mt monthly requirement. Potential overland imports from Saudi Arabia are expected to be very limited and will do little to fill the gap, as Saudi alumina production remains primarily to meet domestic demand.

Meanwhile, even if high overland transport costs are not the main consideration, the possibility of importing alumina via Saudi Arabia’s Red Sea ports to Alba, EGA or Qatalum remains low at this stage, as:

- Alumina is a fine, powdery, hydrophilic and highly abrasive material that requires enclosed high-throughput systems, re-handling/packaging and a moisture-controlled storage environment. Saudi Arabia’s Red Sea ports lack the equipment to import alumina in large volumes.

- Alumina has to compete with food and other necessities for port capacity and trucking resources, which are already stretched. GCC customs requirements are further complicating logistics.

- The Red Sea route itself is increasingly exposed to geopolitical risk, following the involvement of Iran-aligned Houthi forces in Yemen.

Market insights you can actually trust

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions. In times of conflict and geopolitical uncertainty, our real-time data keeps you ahead of supply disruptions and price volatility.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler