The last gasp of a regime: the Israel/US coalition against Iran

US and Israeli forces struck Iran overnight and Trump has framed the operation in explicit regime change terms. This is the Islamic Republic's last gasp. Here you will find our full market analysis including price scenarios, Iran's narrowing retaliation options, and a breakdown of what is physically at risk, with Asia most exposed on crude, Europe critically vulnerable on jet fuel, and the sell the spike playbook at serious risk for the first time since the Arab Spring.

What We Know:

- US and Israeli forces struck Iran overnight in a significant escalation that has been anticipated for weeks

- Iran responded by hitting US military bases across the region including Bahrain's Fifth Fleet headquarters, Qatar's Al Udeid Air Base, bases in Kuwait and the UAE, and assets in Iraq, describing the strikes as an act of self-defence; a senior US official described Iran's response as ineffective

- Ali Shamkhani, former head of the Supreme National Security Council and close advisor to Khamenei, has been killed; unconfirmed reports also claim Khamenei himself and his son Mojtaba, widely seen as a key behind-the-scenes figure, have been killed as well

- President Trump has urged Iranians to take back their country, framing the operation in explicitly regime change terms

- Oil facilities near Kharg Island and Assaluyeh, where most of Iran's natural gas is processed, remain untouched

- Crude flat price is already up 9% over the last week

What We Expect:

- Brent to open $6-$10 higher on Sunday, consistent with the spike seen when Israel launched its bombing campaign in June 2025, with extreme volatility through the session as producers hedge into the rally and shorts scramble to cover

- Freight rates to continue rising as war risk insurance premiums spike or have gotten cancelled altogether, widening arbs and creating dislocations across physical markets

- The conflict to be measured in days or weeks rather than months given Iran's increasingly limited retaliation capacity (see below)

- The market will be laser focused on whether Iran shifts from military targets to energy assets; if it does, the $80 highs reached during the June 2025 twelve day war will be breached and the price impact beyond that depends entirely on how many barrels are disrupted and for how long

The playbook since Obama's Syria red line in 2013 has been to sell the spike; every geopolitical premium over the past decade faded as barrels kept flowing; the question this time is whether Washington is pursuing regime change rather than compliance, because a regime with nothing left to lose does not de-escalate, it goes scorched earth, and that is the risk the opening spike may not fully price

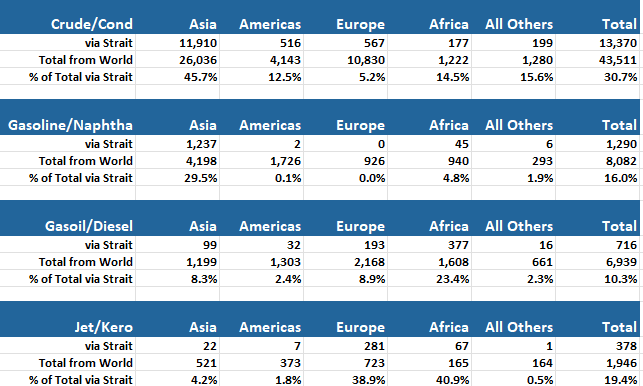

What is at Risk?

Seaborne Exports by Destination (kbd)

Source: Kpler

The Trade

Producers: Sell the spike Sunday on the open. The playbook from 2013 to today has been consistent, geopolitical premiums fade. Lock in prices while the premium is in the market.

Traders: When producers sell Dec 26/Dec 27 WTI into the spike, that selling will pressure the back end of WTI artificially due to hedging flow. Producer hedging blows out Dec 26 and Dec 27 WTI relative to Brent, creating a spread that has nothing to do with the underlying supply picture. When the hedging flow exhausts itself, that arb snaps back.

What makes this different from every event since 2013: Those events had no physical supply impact. The barrels kept moving. There have been reports that the strait has been disrupted and there is risk that Gulf export infrastructure will be targeted. Disrupting barrels puts the old playbook, “sell the spike” at risk.

Iran’s options are narrower than they appear

Iranian Foreign Minister Abbas Araghchi has not ruled out the possibility of continuing talks but said attacks must stop first. That is a significant signal from Tehran about where the regime believes it stands.

Beyond diplomacy, Iran's military options are constrained by a brutal irony: the most impactful retaliatory moves would accelerate the regime's own collapse.

Hitting regional oil infrastructure would push every neighbour currently calling for de-escalation firmly into the US and Israeli camp. Saudi Arabia, which was struck by Iranian missiles and had previously called for de-escalation, now faces direct pressure to respond, and any further Iranian strikes on Saudi soil risk pulling Riyadh formally into the coalition. While the Saudi-Iran relationship is meaningfully more diplomatic today than it was before the 2019 Abqaiq strike, this option is not zero but remains low probability. The cost to Iran of unifying the Gulf states against it is simply too high.

Closing the Strait of Hormuz is an even lower probability. It would raise oil prices temporarily but the US Military would dismantle Iran's ability to threaten the Strait within hours, making it a one-way door for Tehran with no strategic upside. It would also directly antagonize China, which imports 38% of its seaborne crude from the Mideast Gulf. Roughly 9 mbd of crude and condensate have no bypass route. Severing Iran's most important trading relationship at the moment it needs Beijing most would be self-defeating. Iran may use mines to raise the risk premium at the margins.

That leaves diplomacy as the only path with any prospect of preserving the regime. Araghchi's comments suggest Tehran knows this. The question is whether Trump wants a deal or a new Iran. His language so far suggests the latter.

Decapitation or Regime Change - Who Rises?

Two models, very different outcomes for oil.

Venezuela model: cut the head, leave the body: Remove leadership, redirect oil revenues to the Iranian people. Trump cited Maduro explicitly. Clean politically, but Iran is not Venezuela. Maduro's base was thin. The IRGC has 47 years of institutional depth. Remove Khamenei and you likely get an IRGC power struggle, not a pragmatic successor ready to deal. However, IRGC leaders are also businessmen. The regime’s decapitation could incentivise defections and actions towards a transition.

Total regime change: Trump's apparent preference: "Take back your country" is not the language of decapitation. It is the language of revolution. The most discussed successor in exile circles is Reza Pahlavi, who has built opposition coalitions and has meaningful relationships in Washington. Whether Iranians who rejected the monarchy in 1979 welcome it back under the pressure of a foreign military campaign is the central unknown. Trump has been unequivocal saying no boots on the ground. That means no stabilizing force if the transition fractures, and transitions in post-IRGC Iran will not be clean. A successful transition removes the entire conflict premium and places Iranian barrels back into the market as a non-sanctioned crude, adding supply at the margin just as the geopolitical risk premium unwinds. That is a significant double headwind for oil prices. A fractured succession with no coherent government is the opposite: premium stays, supply stays off, and the market has no counterparty to negotiate with.

Fundamental Flows

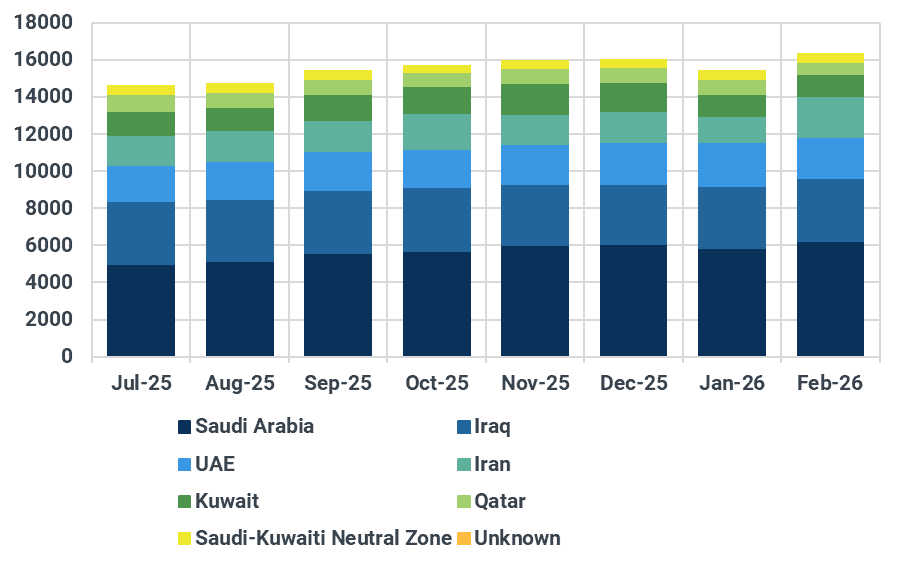

Despite elevated geopolitical tensions, the physical market,particularly in Asia, is increasingly well supplied with medium sour crude. Exports from the Middle East Gulf rose by 880 kbd m/m in February, reaching their highest level since August 2022. Regional producers have been pre-emptively maximising exports, similar to their strategy during the previous 12-day escalation episode, shipping as many barrels as possible before any potential disruption.

Mideast Gulf crude and condensate oil exports, kbd

Source: Kpler

Iranian crude loadings have surged by more than 800 kbd m/m to 2.2 mbd in February, marking a new high under sanctions. At the same time, combined shipments from Saudi Arabia, Iraq, Kuwait, and the UAE increased by 208 kbd m/m, despite higher domestic demand (+105 kbd m/m). The net effect is a growing concentration of medium sour supply directed toward Asia at a time when seasonal demand is about to soften, as the turnaround season reigns supreme.

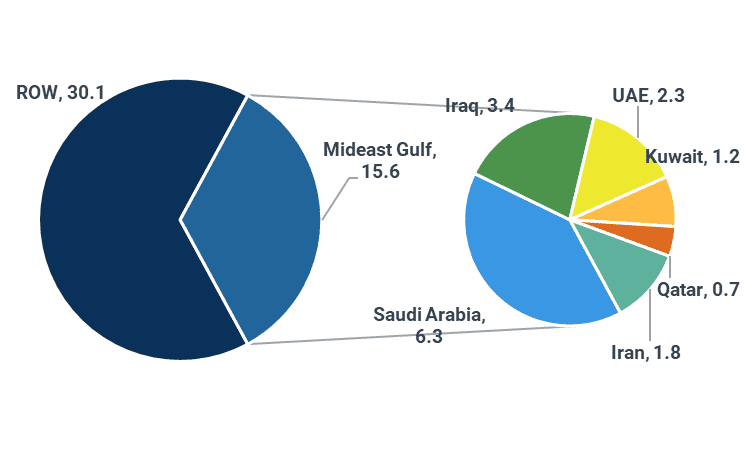

Seaborne global crude oil exports in 2026 ytd, including the Mideast Gulf share passing through the Strait of Hormuz, mbd

Source: Kpler

Duration scenarios:

Days: Qatar and Saudi were calling for an immediate halt this morning. But since these countries have been hit, that off-ramp may now be closed.

Weeks: Episodic retaliation against military targets. $8-12 premium holds.

Months: Succession struggle, IRGC factionalism, no coherent negotiating counterparty. Premium becomes structural.

See why the most successful traders and shipping experts use Kpler