How low can it go: US shale price scenarios

US shale's vulnerability to price swings is rising as oil rig counts and drilled-but-uncompleted (DUC) well inventories fall, exposing supply to a potential 700 kbd drop by Q4 2026 if WTI maintains $50/bbl.

Key Takeaways

- US supply remains resilient near-term due to efficiency gains, masking price vulnerability.

- Kpler forecasts a temporary WTI dip into the $50s over the next 6 months, but a sustained $55/bbl scenario would add downward pressure to our supply outlook.

- A severe, sustained $50/bbl scenario—a view held by some agencies and banks like Goldman Sachs—would cripple US crude supply.

- Under the $50/bbl scenario, US rig counts could fall to 360, slashing US crude supply by 700 kbd by Q4 2026 as natural declines take over.

US crude and condensate supply has shown exceptional resilience despite WTI prices hovering near $60/bbl over the last months, which is below the average breakeven price for the average newly drilled well for many shale basins.

Kpler estimates that domestic supply currently remains at record highs. This view is supported by recent EIA data, which shows the implied and reported crude production figures rising almost continuously since July. Whilst the implied production figure should be taken with caution, given its volatility and overestimation of output, the upward trend implies that output has been rising over the summer months and likely has hit new highs in early October.

Reported and implied US crude supply, Mbd

Source: EIA

This supply strength stems from significant efficiency gains, which are successfully offsetting the decline in the active rig count. The Permian basin leads this trend, accounting for most of the drop in US drilling activity this year, with the active rig count in the Permian basin falling to only 250 currently, down 50 compared to the start of the year.

Active rig count by region, rigs

Source: EIA

A key efficiency metric is the rise in wells drilled per rig. This trend allows fewer rigs to maintain, and even exceed, previous activity levels in some key sub-basins, directly supporting robust production volumes.

New wells drilled per rig by region

Source: EIA

Concurrently, initial production rates from new wells are also increasing. This dual improvement in drilling efficiency and well productivity is keeping overall US output on a clear upward trend.

Production from newly completed wells by region, kbd

Source: EIA

Producers have faced heightened uncertainty from US tariff impacts, Washington's desire for low prices, and OPEC+ regaining market share, which has caused operators to scale back activity this year, creating downward risk to supply if prices fall further.

Whilst producers have partly relied on drilled-but-uncompleted wells (DUCs) to offset the decline in activity, this trend is likely to end as DUCs are hovering near extreme levels in some key shale basins. This is particularly true for the Bakken and Eagle Ford, where DUCs have fallen by around 25-30% so far this year to only 280 and 310 in September, respectively. This downward trend is unsustainable, unless drilling ramps back up - a scenario that is unlikely under the current price environment. Moreover, with producers unable to rely on DUCs, it makes US shale increasingly vulnerable to price fluctuations.

Kpler's 6-month forecast expects WTI to hover near $60/bbl. Whilst a temporary dip into the $50s is expected, we see fundamentals improving in 2H 2026 as non-OPEC+ supply growth peaks, which will support a price recovery. Therefore, a sustained $55/bbl WTI scenario would cause little change to our supply forecast. While current prices might stabilize activity, a $55/bbl environment would likely see the oil rig count fall to around 300, down from currently levels of around 320, with half of this decline originating in the Permian.

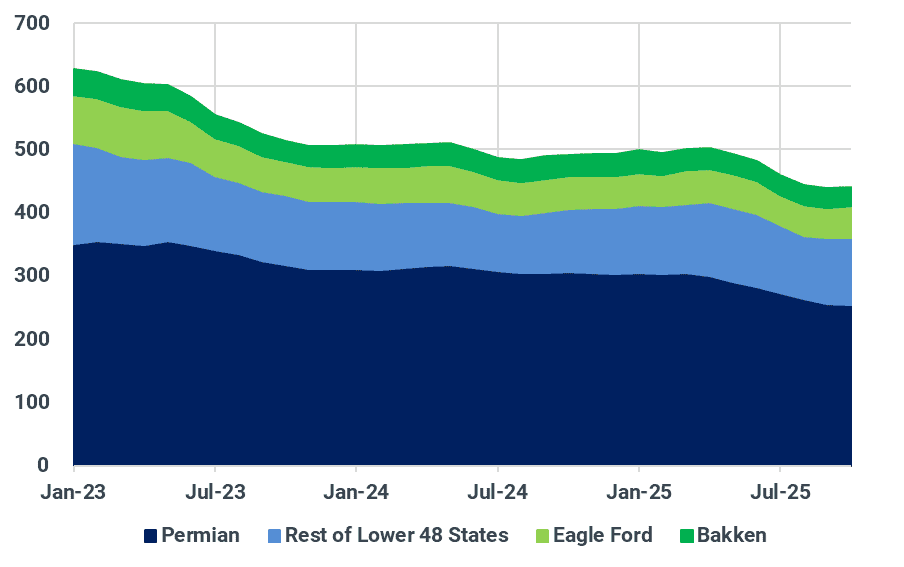

US crude supply price scenarios, Mbd

Source: Kpler

A more pessimistic $50/bbl WTI scenario tests the breakevens of larger producers. Although majors and large independents can operate below $50/bbl, this price level would enforce cautious activity for most. We see the US oil rig count falling to around 360-370 under this scenario, with around 30 of this decline coming from the Permian.

The average new Permian well produces around 1.6 kbd, according to the EIA's STEO report. A significant drop in the number of wells drilled would therefore weigh considerably on domestic crude supply. Our forecast expects output to reach around 13 mbd by December 2026 if WTI averages around $50/bbl continuously until the end of next year.

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Research & analysis driven by proprietary data