US–India trade fallout: What’s at stake for commodities?

This article assesses India’s imports from the US and evaluates the feasibility of replacing these supplies in the event of retaliation.

Washington has threatened to add another 25% tariff on India effective August 28, on top of the 25% tariff effective from August 1. Goods affected include textiles, footwear, gems (especially diamonds), and jewelry, as well as marine products (especially shrimp). Notably, pharmaceuticals are currently exempt. India could therefore, together with Brazil, face the highest US tariffs of up to 50%.

This measure aims to penalize India for continuing to buy Russian energy commodities, most importantly crude oil. So far, the Indian government has refrained from issuing any directive to halt Russian crude imports, a stance supported by robust import flow data. Nevertheless, Indian refiners have already issued more tenders for non-Russian crude for September–October delivery.

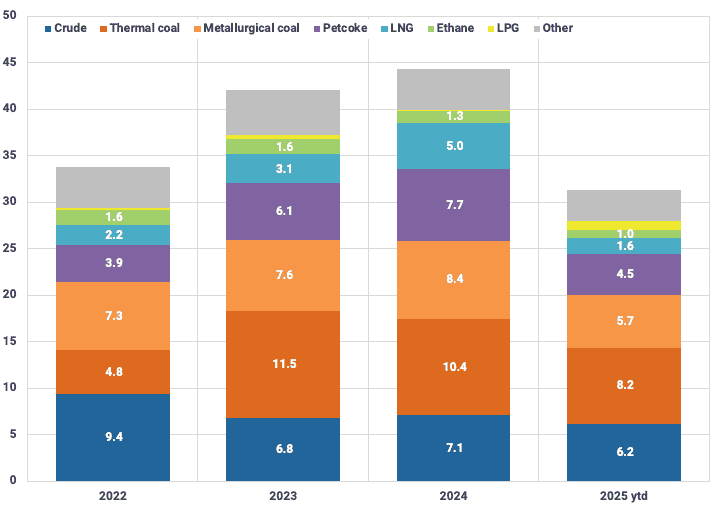

India’s commodity exports to the US are minimal, including 53 kbd of blending components in 2024 or occasional seasonal gasoline flows to the US West Coast. However, at 44.3 Mt in 2024, Indian imports of US commodities are significant. For comparison, China, the largest recipient of seaborne US commodities, imported 90 Mt in 2024.

Which US commodities does India import, and in a hypothetical scenario of Indian retaliation, could these supplies be replaced with alternative sources?

Indian imports of US commodities (Mt)

Source: Kpler

Crude

Among the major commodities, India has the lowest reliance on US crude, which held a 3.0% share of total Indian imports last year, totaling 150 kbd (excluding Canadian grades exported via the US Gulf Coast). In 2025 year-to-date, volumes have increased to 210 kbd, with the vast majority consisting of light sweet grades such as Midland. On the other hand, the 80 kbd flow of Canada’s heavy sour Cold Lake Blend exported via the US would likely not be affected should India aim to retaliate against the US tariff measures. Light sweet US crude could be substituted by Middle Eastern Murban and Umm Lulu, which are slightly sourer but comparable in density. In general, Indian refiners favor distillate-heavy grades, which could also incentivize a shift away from gasoline-rich WTI and Midland. In terms of refining economics, replacing non-discounted US barrels is more feasible than substituting cheap Russian crude. Indian buying of medium sour US grades such as Mars and Poseidon halted in early 2023 amid tightening global availability of heavy molecules (Russia sanctions, OPEC+ production cuts) and US refiners scrambling to source replacements.

LNG

At 18.8% of total Indian 2024 imports, US LNG (5 Mt) plays a significant role in India’s energy mix, even though the 2025 year-to-date share has already dropped to 10.8%, driven by greater purchases from the UAE and Oman. Retaliatory action on LNG by New Delhi remains unlikely given the country’s price sensitivity and high exposure to flexible US spot cargoes. Nevertheless, elevated LNG stocks in OECD Asia and China, coupled with steady Pacific Basin supply, could facilitate sourcing of non-US volumes in Q3. Additionally, Indian LNG consumption has declined year-to-date, primarily due to elevated spot prices driving fuel switching in the industrial sector—a trend expected to persist into H2—combined with lower cooling demand following an early monsoon. Also, in 2026, new LNG supply targeting the Asian market will come online (Canada LNG 2, Qatar NFE expansion, phase 2 of Australia’s Pluto LNG) and could trigger price decreases closer to India’s affordability levels.

Coal and petcoke

Compared to US LNG, India’s imports of US thermal coal (10.4 Mt in 2024, 6.4% of total imports) account for a smaller share. Major global miners have refrained from production cuts this year, as they remain able to absorb lower prices, while high inventory levels and reduced blending needs are currently dampening Indian import demand. Nevertheless, should India aim to lower its US exposure in response to Washington’s tariffs, potential replacement volumes are not easily available, considering that India imports a special grade, Northern Appalachian coal. This high CV and high sulfur grade is available at a discount to other grades and mostly used by India’s cement industry.

The US plays a larger role in metallurgical coal exports to India (8.4 Mt, 12.3% share). While India’s post-monsoon restocking demand and improved steel production point to rising import needs, Australian and Russian production capacity would likely be sufficient to replace US metallurgical coal, even though provisions from Trump’s “Big Beautiful Bill” could increase the competitiveness of US coal in coming years.

On the other hand, the US is by far the world’s largest exporter of seaborne petcoke (64% of the global total in 2024). Saudi Arabia, Oman, and Venezuela follow far behind and would struggle to replace US volumes (7.8 Mt in 2024, 52% share) in the Indian market, especially as the US-China trade war may increase China’s demand for non-US petcoke. This limited replaceability would likely undermine the cost competitiveness of petcoke in India and could further encourage Indian buyers to turn to non-US thermal coal.

Petrochemical feedstocks

The US is the world’s only major exporter of ethane, while Reliance is India’s sole significant importer (63 kbd in 2024). Should trade tensions between India and the US escalate, replacements for US ethane would be difficult to obtain. In addition, modifying ethane crackers to run on LPG is not feasible in the short term, as it would require massive investment and dramatically alter both output mix and economics. On the other hand, the burgeoning US-India LPG trade, which reached an unprecedented 159 kbd in July 2025, could come under pressure should India retaliate, as Middle Eastern supply is closer in proximity and a better match for India's more evenly split propane and butane demand than the propane-heavy US exports.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Get research & analysis driven by proprietary data