Albertan wildfires threaten 700 kbd of supply, tightening heavy crude markets

Market & Trading Calls

- Bullish on near-term WCS Hardisty crude differentials as Albertan wildfires close in on major oil sands operations and shut-in production in early June.

- Bearish on medium crude diffs as OPEC+ accelerates unwinding for a third month, adding yet another 411 kbd in July, while strong refining margins likely approach a tipping point.

- Bullish on Atlantic Basin light sweet crude differentials in the near term amid rising summer crude demand, Ekofisk field maintenance and US shale supply declines.

Trades of the month

- Aramco July OSPs: Arab Light and Arab Extra Light are likely to be cut by $0.50–$0.70/bbl m/m in Asia, reflecting weaker fundamentals and the need to stay competitive against rival barrels. We expect a smaller cut of $0.30-$0.40/bbl for Arab Heavy considering strong fuel oil cracks. Arab Light OSPs into Europe and the US are likely to rise by $1.00-1.20/bbl and $0.10-0.20/bbl, respectively, reflecting the stronger market structure for medium sours in those regions.

- Long WCS Hardisty relative to Maya as heavy crude markets along the USGC remain almost unaffected from Albertan supply disruptions.

Price forecast: Dated Brent outlook cut to $58/bbl as structural surplus persists through mid-2026

We have revised our 12-month Dated Brent forecast to $57.7/bbl, more than $6/bbl lower than the previous projection, reflecting a structurally long market and continued macroeconomic fragility. Despite a softening in tariff rhetoric from the US administration, persistent policy uncertainty is stalling investment and weighing on consumption. The global growth backdrop remains too weak to support stronger crude fundamentals.

Global crude and condensate balances are set to average a surplus of nearly 600 kbd in 2025, up from 213 kbd a month ago. OPEC+ remains committed to unwinding its cuts, while non-OPEC+ production remains robust. However, US supply could begin to retreat as early as Q4 2025, under pressure from sustained low prices and average breakevens near $60/bbl. We now expect US crude output to fall by 200 kbd in 2026.

In the near term, rising domestic burn within OPEC+ will temporarily absorb July’s planned 411 kbd increase, keeping Brent supported into mid-summer. Lack of progress on the Russia-Ukraine front or in the Iran-US nuclear negotiations also prop up the geopolitical risk premium. But balances are set to lengthen sharply from August onward. Demand growth of just 205 kbd this year and refinery closures of 765 kbd leave little room for optimism. With no geopolitical supply shocks or demand surprises, Brent remains capped well into H1 2026.

Kpler Dated Brent Price Forecast, $/bbl

Source: Kpler, ICE

Chart of the Month: OPEC+ widens Brent-Dubai spread to stem West of Suez inflows into Asia

Two months into the phased rollback of 2.2 Mbd in voluntary OPEC+ cuts, the group is already seeing results from its strategic effort to rebalance regional flows. The Brent-Dubai EFS has widened significantly, climbing above $2/bbl for the first time since Oct. 2024, an essential move to curtail the competitiveness of Atlantic Basin grades into Asia, particularly amid the seasonal ramp-up in crude buying from regional refiners.

This structural shift was necessitated by the continued divergence in supply dynamics. In 2023, non-OPEC+ added 1.27 Mbd while OPEC+ (excluding exempt members) contracted by 480 kbd. In 2024, this divergence has only intensified: non-OPEC+ supply is up 780 kbd y/y, while OPEC+ volumes are down by 1.38 Mbd. That dynamic led the EFS levels near parity, enabling West of Suez flows to Asia to rise to nearly 9 Mbd by February and March, pressuring OPEC+ market share.

The group’s intervention has already reversed the trend. WoS-to-Asia flows have declined by over 2.7 Mbd since February, with LatAm and WAF exports down a combined 1.6 Mbd. Volumes of Kazakh crude flowing to Asia, despite Kazakhstan’s OPEC+ membership, collapsed from 363 kbd in April to zero in May. Meanwhile, the WTI-Murban spread on a CFR Asia basis moved from parity in April to $1/bbl in May, reflecting improved pricing leverage for Middle East producers.

While OPEC+ is looking to reinforce this trend with deeper curbs in July, two key variables may constrain further gains in the EFS: rising production from Brazil and Guyana, and persistent strong demand from Asian refiners returning from heavy maintenance. Nevertheless, the current trajectory underscores the effectiveness of OPEC+’s tactical recalibration.

West of Suez oil flows to Asia (Mbd, LHS) and Brent-Dubai EFS spread ($/bbl, RHS)

Source: Kpler, Argus Media

Heavy crude: Albertan wildfires are closing in on major oil sands operations, which is keeping heavy crude markets supported

Albertan wildfires are encroaching on oil sands operations, threatening supplies and contributing to tighter North American heavy crude markets. Currently, 53 active wildfires are reported in Alberta, with 32 considered out of control. Notably, the Caribou Lake Fire (LWF090), which recently expanded to 68,000 hectares, has closed in on key oil sands facilities, including Cenovus's Foster Creek and Christina Lake sites, MEG Energy's Christina Lake facility, and Canadian Natural Resources' Kirby and Jackfish projects. These operations collectively represent over 700 kbd of bitumen output, based on first-quarter data, translating to approximately 1 Mbd of marketable crude when blended. Cenovus Energy has already initiated a precautionary production curtailment at its Christina Lake facility on May 29, impacting an estimated 238 kbd of its output. While outages at MEG Energy’s Chistina Lake facility have not been reported, power outages have delayed the start-up of 70 kbd of production at the company’s phase 2B site.

This escalating wildfire situation across Alberta is injecting considerable uncertainty into Canadian heavy sour crude markets. Consequently, Western Canadian Select (WCS) prices at Hardisty have found support, with the benchmark's discount to WTI CMA tightening by approximately $1/bbl to trade near $8.50/bbl ahead of the July cycle. While supply outages are likely to boost near-term prices for regional heavy crude grades, an anticipated increase in Albertan oil sands supply in Q3 (in line with seasonality as field maintenance reaches its peak), coupled with a relatively flat US crude demand outlook and persistently weaker US HSFO cracks (currently hovering around $2/bbl), are expected to provide some headwinds, assuming supply disruptions do not accelerate.

Albertan crude differentials, $/bbl

Source: Argus Media

The primary beneficiaries of Alberta's ongoing supply disruptions are alternative medium to heavy grades typically processed by US West Coast refiners. This is because other consumers, such as US Midwest refiners, are unable to turn to alternatives due to pipeline constraints, even under a scenario where WCS Hardisty crude differentials appreciate strongly. A potential reduction in Alberta's crude supply will also partly curtail export availability and constrain flows via the Trans Mountain Pipeline (TMX). Exports to US West Coast refineries through TMX have already declined sharply, averaging only 100 kbd this month—half the volume observed in March—amid tariff uncertainties and stronger WCS Hardisty pricing. While a potential decline in demand due to a rise in WCS Hardisty prices may deter some buying, differentials are expected to remain robust over the coming weeks as supplies ease amid seasonal field maintenance and ongoing wildfire outages.

US West Coast refiners may turn to alternative grades, such as Ecuador’s Napo, with medium-density grades from the Middle East (like Basrah Medium), and Colombia’s Vasconia, likely to see a potential uptick in buying interest in PADD 5 as well. This is particularly relevant for Ecuadorean Napo, last assessed at a $9.35/bbl to $9.65/bbl discount to September ICE, making it $2.80/bbl cheaper than Cold Lake FOB assessments. This situation coincides with an expected rise in Napo availability. Petroecuador’s 110 kbd Esmeraldas refinery is reportedly experiencing operational difficulties following an earthquake on April 25, a development anticipated to weaken Napo's differentials as more crude becomes available for export. Utilization rates at the Esmeraldas refinery have reportedly averaged around 48% since May 10, potentially leading Petroecuador to offer more crude in its upcoming tenders. This dynamic is expected to keep Napo crude differentials under pressure, although a potential increase in demand from US West Coast refiners could provide some counterbalance.

Selected Latin American crude differentials, $/bbl

Source: Argus Media

Recent K-factors for Maya crude also signal prevailing tightness in US Gulf Coast heavy crude markets. Mexico's state-owned Pemex lifted Maya's June price adjustment factor (K) for this region by 60¢/bbl, an increase that notably contrasted with reductions applied to most other Mexican grades destined for the US Gulf Coast.

Despite some headwinds, including weaker US HSFO cracks and a relatively flat outlook for US crude demand in the months ahead, Maya prices are anticipated to remain largely range-bound for the time being. This expectation is primarily due to persistent near-term uncertainty surrounding Canadian heavy crude flows. The sideways price trend is foreseen even considering the recent decline in Canadian crude shipments to the US Gulf Coast, which averaged 440 kbd in March, down from nearly 500 kbd in October of the previous year (some of this decline remains in line with seasonality).

Maya crude differentials, $/bbl

Source: Argus Media

Medium crude: Growing downside risks as continued OPEC+ output acceleration adds supply, middle distillate cracks near tipping point

Middle Eastern medium sour crude benchmark Dubai softened in May, after eight OPEC+ members agreed to add 411 kbd of supply in June, the second consecutive month of accelerated production. The increase, although expected to result in lower crude exports than the headline figures imply, will primarily come from Saudi Arabia and the UAE, and is likely to consist of light and medium sour grades. As a result, the spread between front- and third-month Dubai narrowed by $0.54/bbl in May from the previous month. Over the weekend, the eight members unsurprisingly moved ahead with the decision to add yet another 411 kbd in July. That said, Saudi Aramco is expected to cut its July-loading Arab Light OSP by around $0.50-$0.70/bbl m/m — likely deeper than the Dubai structure adjustment—to reflect the OPEC+ decision and stay competitive.

Thanks to lower-than-expected OSPs over the past two months, Saudi medium crude appears cheaper than many spot cargoes—such as Oman, Tupi, and Djeno—for June and July delivery in Asia. This has prompted refiners, particularly in China, to increase liftings under term contracts and, to some extent, reduce their appetite for spot procurement. As more refining capacity returns from maintenance, which will put downward pressure on refining margins, the Dubai market is likely to face continued weakness during the June trading cycle, even though crude buying demand from refiners remains resilient and lower flat prices may spur some restocking.

That said, one potential supportive factor is Iran. If nuclear talks between Washington and Tehran fail to yield an interim deal and U.S. sanctions under the “maximum pressure” policy remain in place, China is expected to keep its Iranian crude imports below 1 mbd in June, around 500 kbd lower than the April level. The decline in cheap feedstock and potential weakening of margins could force Chinese teapots to cut run rates—if not shut down altogether—and, in turn, prompt state-owned refiners to ramp up crude purchases, primarily from the Middle East, as well as boost operations to capture greater market share.

Dubai M1-M3 spread, Brent-Dubai EFS, $/bbl

Source: Argus Media

In contrast to the softened market in Asia, medium sour crude in the Atlantic Basin strengthened in May, supported by solid refining margins and tighter supply. Since March, the Czech Republic has halted imports of Russia’s Urals crude via the Druzhba pipeline and has instead been receiving oil delivered to Italy’s port of Trieste, which is then transported through the Transalpine Pipeline. Kpler data showed that crude discharged at Trieste surged to a record high of 946 kbd in May, up 173 kbd m/m, with rising volumes of Norwegian Johan Sverdrup and Middle Eastern crude. Prices for Johan Sverdrup crude jumped to as high as $2.10/bbl over Dated Brent in late May, up from a discount of $1.20/bbl the previous month, and are expected to remain firm in June following a sharp drop in the July-loading program. Only 20 cargoes of Johan Sverdrup—equivalent to 684 kbd—are scheduled for shipping in July, marking the lowest monthly volume since February 2023.

Meanwhile, Johan Castberg, a medium sweet crude from Norway, finally reached the market in mid-May after several delays caused by weather conditions and technical issues. The first cargo was loaded on May 29 and appears to be headed to Rotterdam. Earlier market talk suggests that Spain’s Repsol may be the first buyer, likely for its 120 kbd La Coruna refinery. The new supply stream, together with rising Middle Eastern volumes, could cap the gains in European medium sour crude prices this month. At the same time, it’s worth noting that the increase in production quotas for Middle Eastern oil producers will also boost domestic refining activity, leading to higher middle distillate exports. This could exert downward pressure on gasoil and diesel cracks in Europe—the primary destination for those shipments—and, in turn, weigh on the region’s medium crude market.

Johan Sverdrup FOB diffs vs Dated Brent, $/bbl

Source: Argus Media

Medium sour crude in Latin America softened in May and continues to face growing downward pressure in the June trading cycle, as OPEC+ moves ahead with a third consecutive production increase in July—making Middle Eastern barrels more competitive against WTI- and ICE Brent-linked grades in the region. At the same time, Brazil brought online its newest FPSO—the 180 kbd Alexandre de Gusmão (Mero 4)—in the pre-salt Santos Basin in late May. This followed just days after Petrobras announced that FPSO Marechal Duque de Caxias (Mero 3) had reached its peak production of 180 kbd. Kpler currently forecasts Brazil’s crude output near record high of about 3.6-3.7 mbd in May and will reach 3.8 mbd in late Q3. The rising supply is expected to drive Brazilian crude prices lower, particularly as most cargoes are sold to Asia, where they frequently compete with barrels from Saudi Arabia and the UAE. In addition, elevated freight rates for shipping Latin American crude to China have further diminished the attractiveness of arbitrage cargoes. Brazilian Tupi is currently priced about $1.50/bbl higher than Oman crude for August delivery. As a result, China has likely purchased only 21 mb of August-loading cargoes, down from 26.5 million barrels in each of the previous two months, according to Argus Media.

Oman-Tupi diffs on delivered basis in Asia

Source: Argus Media

Light crude: European summer demand should support light crudes in the North Sea soon

North Sea physical market structures weakened sharply last month, with the NSD M1-M3 spread narrowing from an average of $2.38/bbl in April to just $0.64/bbl in May. Reflecting this, BFOET crude differentials also declined—Forties crude, for example, dropped from $1.45/bbl in mid-April to $0.40/bbl by mid-May. This decline was partly driven by June loading schedules indicating an 18% month-on-month increase in Forties exports, rising to 187 kbd this month. More broadly, bearish sentiment in Northwest Europe (NWE) was fueled by an oversupply of light crude, following a sharp rise in WTI and CPC Blend inflows in April—up 40% and 10% m/m, respectively. The situation was further exacerbated by the shutdown of the 150 kbd Grangemouth refinery in Scotland during May, which reduced UK refining capacity by 12% m/m last month (from 1.24 Mbd in April to under 1.1 Mbd in May, IIR), driving NWE crude demand down to 5.6 Mbd. Looking ahead, NWE refinery runs are expected to rebound to 5.78 Mbd in June and peak at 5.81 Mbd in July, supported by strong summer transport fuel demand. Refining margins are projected to remain firm in the coming weeks, helping to sustain crude demand for regional grades. Additionally, a tightening in supply is expected, with June loadings of Ekofisk set to hit a record low of 350 kbd due to maintenance activities. These tightening dynamics are already translating into stronger market structures: the North Sea Dated M1–M3 spread widened to $1.86/bbl by 30 May and BFOET differentials are also expected to rise in the near term.

BFOET crude differentials, $/bbl

Source: Argus Media

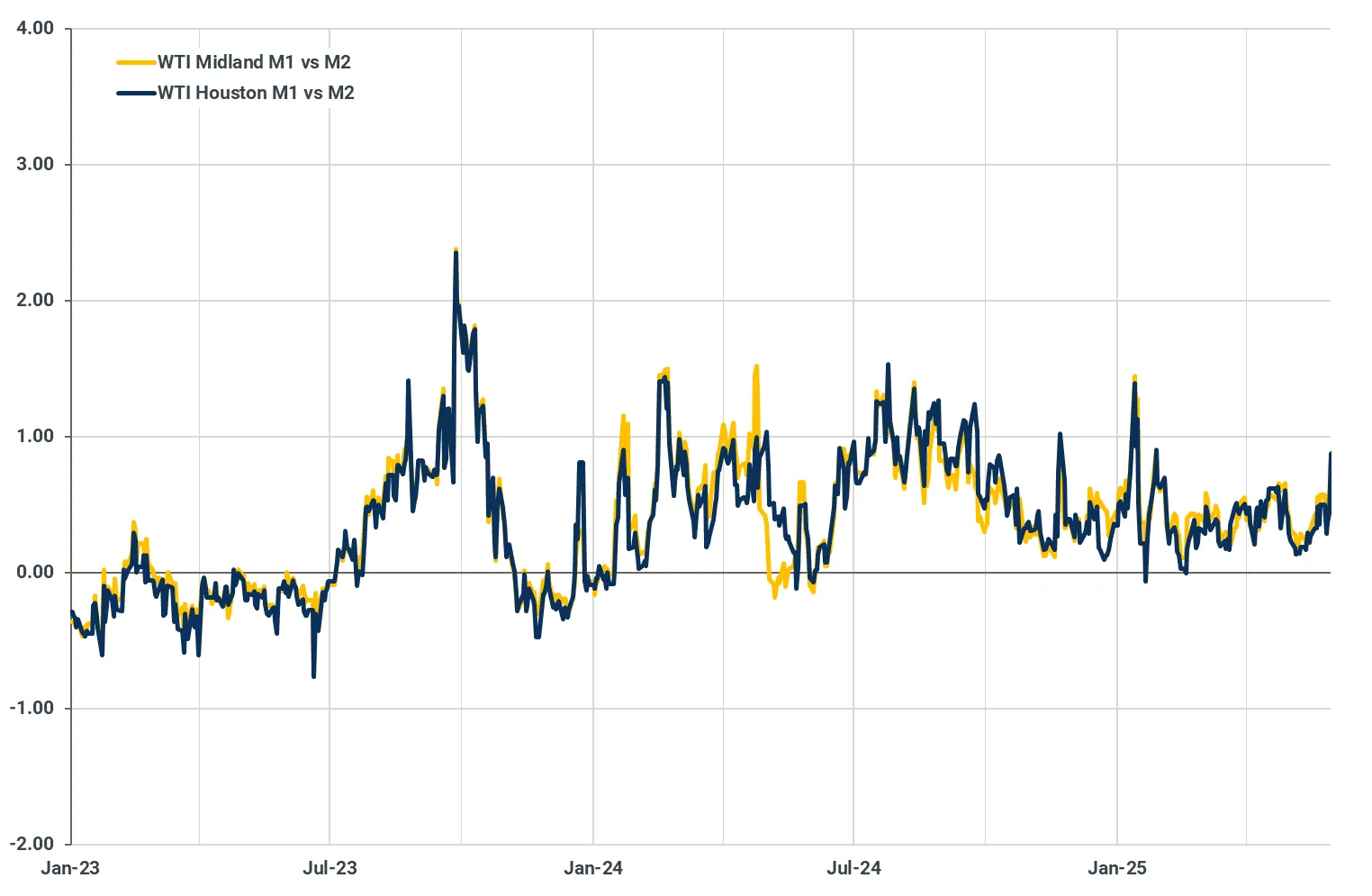

While WTI crude prices experienced a modest rebound in the latter half of May, they remain below the breakeven levels required for new well development across most U.S. shale regions. This persistent price weakness continues to weigh on upstream activity, as the average breakeven for new U.S. shale projects is trending in the mid-to-high $60s per barrel. Sustained prices below this threshold are likely to prompt significant operational cutbacks and a corresponding decline in production. This trend is already becoming evident, with the total U.S. oil rig count dropping by approximately 10% since early April, a multi-year low. Hence, we have downgraded our U.S. crude and condensate supply forecasts, with output now projected to average 13.34 Mbd in the second half of 2025 and 13.15 Mbd in 2026. Meanwhile, the WTI M1 vs. M2 spread faced downward pressure in early May due to softer European demand for June-loading cargoes, amid abundant regional supply of light sweet crude and elevated transatlantic shipping costs. However, the combination of seasonal demand, a tightening global crude balance, and anticipated declines in shale output is expected to bolster prompt WTI buying interest. This shift is already reflected in the M1-M3 spread, which climbed to $0.88/bbl on May 30—up sharply from $0.13/bbl at the beginning of last month.

US market structures, $/bbl

Source: Argus Media

Light crude grades from the Middle East—such as Murban and Arab Extra Light—have come under increasing pressure due to rising supply. Correspondingly, the spread between front-month and third-month IFAD Murban contracts narrowed significantly, dropping from $2.53/bbl in early April to just $0.53/bbl by early May. This supply growth is being driven not only by elevated OPEC+ production but also by a surge in competing light crude inflows from the Atlantic Basin and the Caspian region. On 31 May, eight OPEC+ members agreed to implement an additional supply increase of over 411 kbd starting in July, which is likely to exert further downward pressure on light crude prices in the Asian market. In response to softer fundamentals, we expect Saudi Aramco to lower its Official Selling Price (OSP) for Arab Extra Light by approximately $0.50–$0.60/bbl next month, mirroring the recent drop in Murban valuations. Such a move would present further headwinds for light crude exporters from regions like the North Sea, West Africa, and the United States, as competition for market share in an increasingly saturated Asian market intensifies. At the same time, reports emerged this week that Adnoc has cut the projected volumes of its Murban crude available for export in the August 2025-May 2026 period because of plans to increase processing of Murban at its Ruwais refinery. These dynamics should lend support to light sour grades in the region.

IFAD Murban M1-M3 spreads, $/bbl

Source: Kpler

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data