Ample inventories pressure Asian LNG prices, while TTF stays supported by scheduled maintenance in Norway and Algeria; geopolitics remain the key factor for swings

Ample inventories pressure Asian LNG prices, while TTF stays supported by scheduled maintenance in Norway and Algeria; geopolitics remain the key factor for swings

Market & Trading Calls

European TTF front-month price outlook: Stable as reductions in aggregate supply, mainly driven by heavy maintenance in Norway and Algeria, will be balanced by strong wind generation across NWE, although geopolitical developments will continue to pose a significant risk to our outlook.

Asian LNG front-month price outlook: Slightly bearish, as ample NE Asian LNG inventories continue to cap upside, with sentiment pressured by a mild November temperature outlook and steady Pacific supply. Taiwan’s stronger gas-for-power demand offers some support, but not enough to offset the bearish rollover.

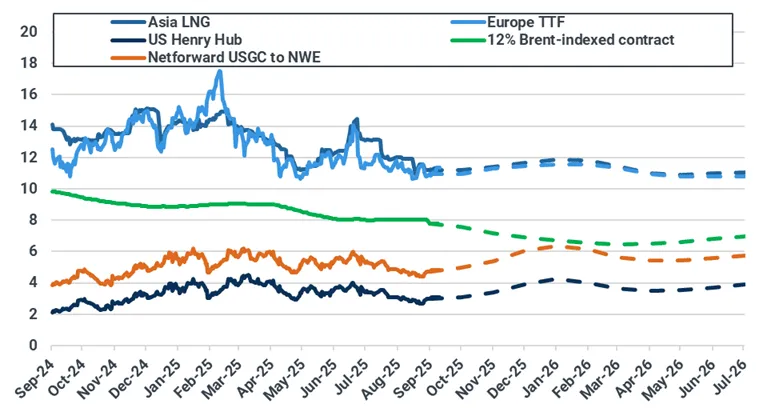

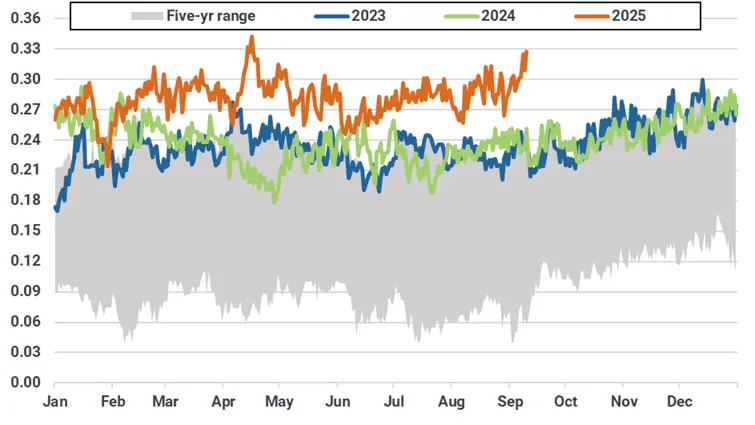

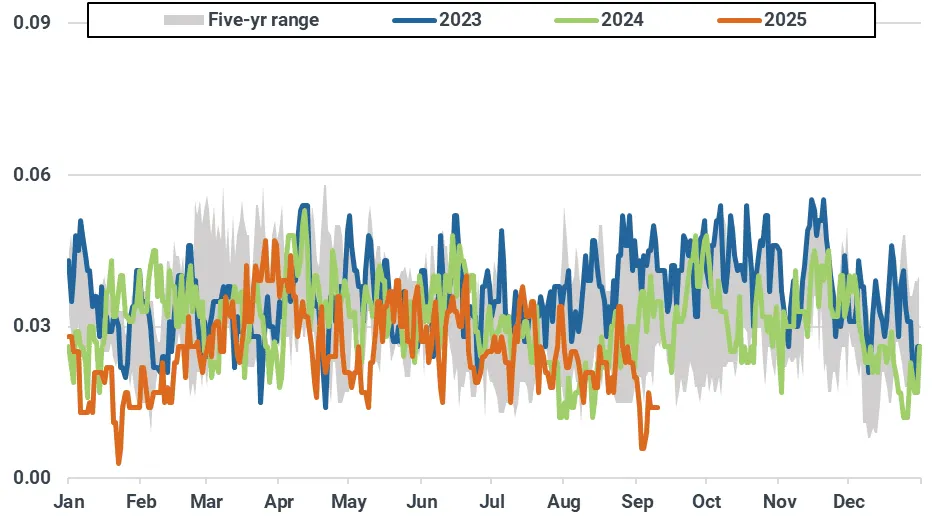

Asian LNG – TTF spread outlook: Slightly narrower as stable TTF contrasts with further downside risk in Asian LNG. The spread narrowed by $0.29/MMBtu to -$0.03/MMBtu on 10 September.

US Henry Hub front-month price outlook: Steady as weak near-term demand and large storage injections countered the technical factors that propelled prices above $3.00/MMBtu over the last two weeks.

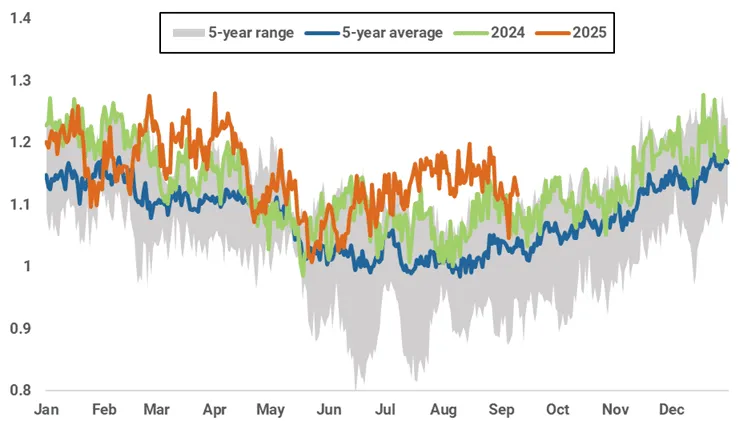

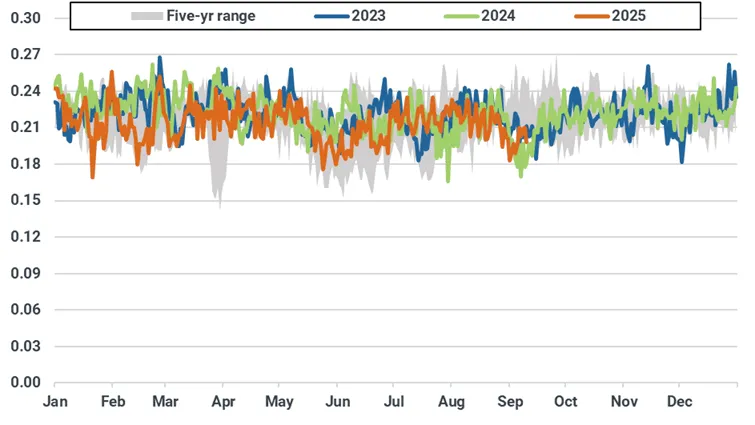

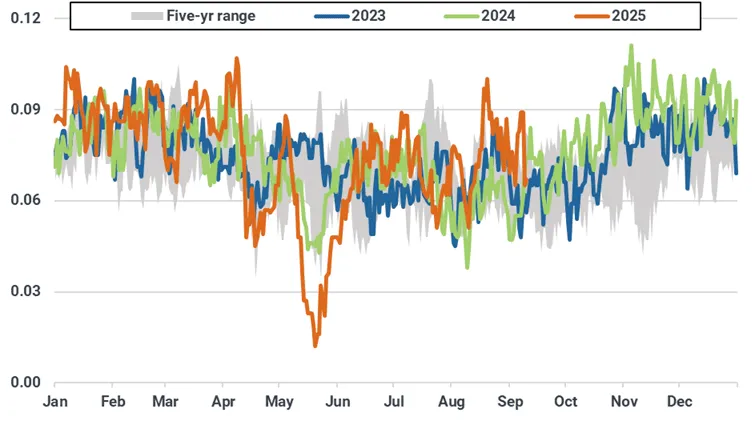

Key natural gas and LNG front-month prices ($/MMBtu)

Asian LNG-TTF front-month spread ($/MMBtu)

Europe: TTF stable as strong renewable generation and overall weak demand balance lower supply

European TTF front-month prices increased to $11.37/MMBtu on 10 September, up $0.40/MMBtu from $10.97/MMBtu on 3 September. The rise was mainly driven by geopolitics, with news about EU-US talks aiming to increase pressure on Russia, possibly through additional sanctions on Russian companies and secondary tariffs on countries purchasing Russian oil and gas. Additionally, Israel’s attacks on Qatar targeting the Hamas leadership drew market attention to the Middle East, which was closely monitoring any signs of escalation.

On the fundamentals side, bearish market indicators limited any further gains from geopolitical events including a third unloading of Arctic LNG 2 volumes at Beihai port in China, muted EU gas demand, EU UGS levels approaching 80%, higher LNG imports w/w, and Norwegian maintenance progressing as initially scheduled.

For the week ahead, Kpler Insight maintains a stable outlook for the TTF front-month contract as we expect bearishness stemming from strong renewable generation to be balanced by a gradual decline in temperatures and reductions in aggregate LNG and pipeline supply.

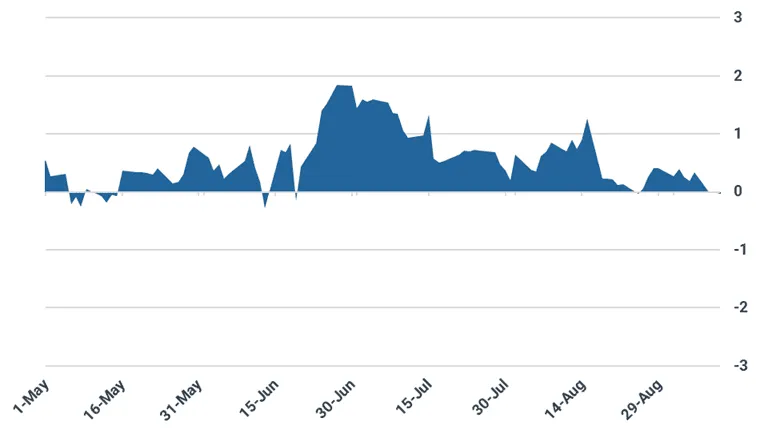

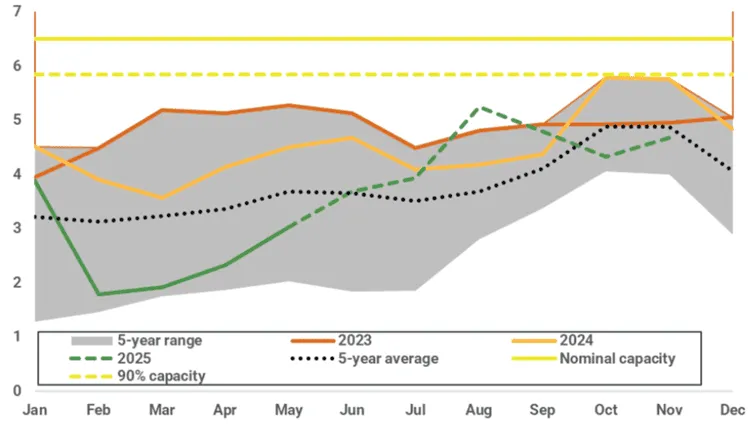

From the supply side, EU pipeline imports fell by 7.3% w/w to 2.8 bcm driven by lower imports from Norway (- 0.24 bcm w/w) and Algeria (- 0.09 bcm w/w) as heavy seasonal maintenance continues in both countries. UK exports to the continent increased as Norwegian flows into Easington rose in the last few days.

Norwegian daily net pipeline flows to the EU (bcm)

Ongoing maintenance in Algeria mainly affects flows to Italy, while exports to Spain remain high. Currently, flow patterns suggest a lighter-than-expected maintenance season in Algeria, but we anticipate flows to Spain will decrease within the next two weeks.

Algeria daily net pipeline flows to the EU (bcm)

Looking into next week, EU-27 net pipeline imports are expected to decline further as Norwegian & Algerian maintenance continue. In addition, planned maintenance works at the BBL pipeline will contribute to the reduction of UK flows into the continent.

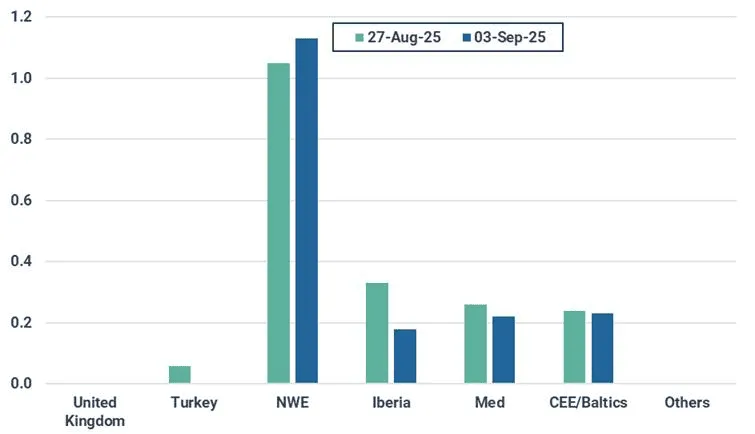

European LNG imports fell by 9% w/w to 1.8 mt, driven by decreased imports in Iberia and the Med region. The drop was mainly driven by increased maintenance in Spain along with weak domestic demand trends, high domestic UGS levels, and market players in Italy opting to increase intra-European pipeline imports to cope with the loss of pipeline imports from Algeria. Looking ahead, we expect LNG volumes to slightly reduce next week as planned maintenance will take place at several terminals in Spain and Germany’s Brunsbüttel will start operating at limited capacity from 17 September.

EU-27 weekly LNG imports by region (mt)

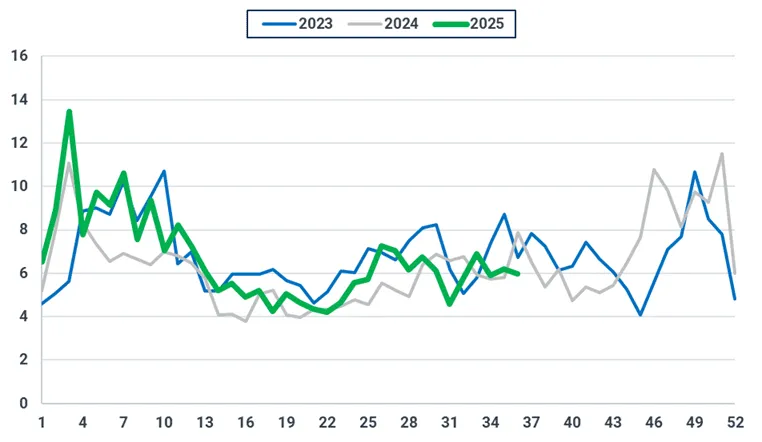

On the demand side, EU-24 gas-fired generation decreased by 4% w/w to an estimated 5.9 TWh, mainly due to strong wind generation surpassing small increases in overall power demand. Looking ahead, with forecasts indicating above-average renewable generation in the coming days, especially in NWE, we expect reductions in gas-fired generation across the EU.

EU-24 weekly gas-fired generation (TWh)

Average forecast temperatures for selected European countries (°C)

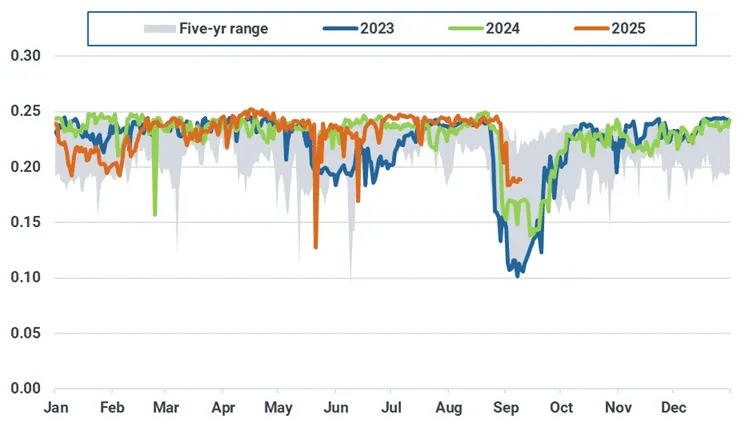

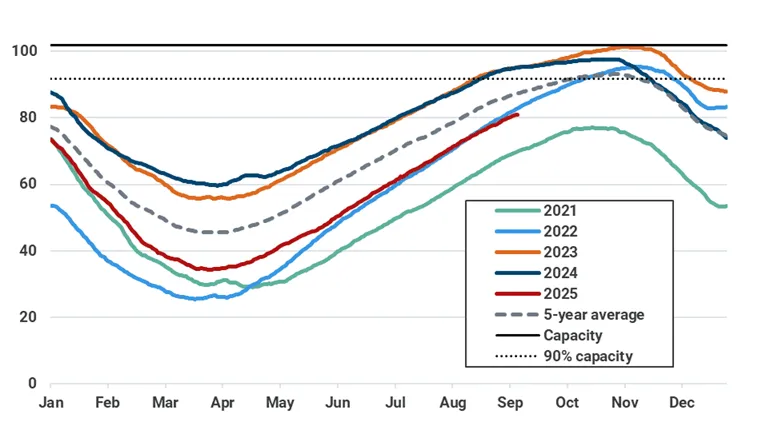

EU-27 underground gas stocks stood at 79.7% on 9 September, 6.7 percentage points below the five-year average. Net injections slowed down as pipeline imports reduced w/w as a result of increased maintenance in Norway and Algeria. Looking into next week, we expect net injections to continue decelerating and only start ramping up after 20 September when capacity of several assets in Norway will be gradually added back online.

EU-27 underground natural gas inventories (bcm, left) as of 9 September

Asia: Ample LNG stocks and mild heating outlook weigh on prices into November rollover, offsetting stronger Taiwan gas-for-power demand

Asian LNG rose $0.11/MMBtu w/w to $11.34/MMBtu on 10 September, tracking European TTF geopolitical risk despite muted Asian demand.

Asian LNG prices are expected to be slightly bearish into next week as ample LNG inventories and mild November temperatures in Japan/Korea curb heating demand. Pacific supply eased w/w ahead of planned maintenance but remains above 5-yr averages, while Taiwan’s gas-for-power uptick too modest to shift prices.

Gas-for-power demand in Northeast Asia is set to remain elevated into next week with temperatures across the region trending above 5-year norms. Ongoing monsoons continue to cap temperatures and limit cooling demand in South and Southeast Asia.

Forecasted average temperatures for Asian countries (°C)

In Japan, May METI gas-for-power demand slipped 0.2 bcm y/y to 3 bcm, slightly above expectations. May utility stocks rose to 2.8 mt, offsetting stronger power demand. Major utility LNG stocks fell 0.2 mt w/w to 1.81 mt by 7 September, now 0.3 mt below the 5-yr avg, reflecting reduced deliveries amid higher nuclear availability. Implied LNG inventories are set to climb seasonally to 2.7 mt in October and 2.8 mt in November, capping spot demand. Fundamentals remain bearish, though a sustained September heatwave could trigger brief drawdowns and short-lived price support.

Japan implied LNG inventory for power utilities forecast (mt)

In South Korea, implied South Korean LNG inventories remain well above 5-year averages, easing from August highs to 4.8 mt by end-September and 4.3 mt by October, before modestly rebuilding to 4.6 mt by end-November. Ample stocks keep supply secure into Q4 winter heating season, capping upside for Asian LNG spot prices.

South Korea implied LNG inventory forecast (mt)

In China, August gas imports hit 11.85 mt (16.1 bcm), including 5.5 mt (7.5 bcm) pipeline gas, up 5% y/y (Preliminary Customs). Kpler trimmed September LNG demand by 0.15 mt to 6.9 mt on stronger pipeline inflows; October–November outlook steady, leaving near-term sentiment bearish amid high inventories. Despite recent CNPC–Gazprom plans to boost Power of Siberia 1 capacity to 44 bcm/y, Kpler does not expect additional volumes to reach China before 2027.

China’s pipeline gas imports by month (bcm)

China implied LNG inventory forecast (%, mt)

In Taiwan, MOEA reported record July gas demand at 3.2 bcm, up 0.6 bcm y/y, driven by 2.7 bcm gas-for-power burn. This reflected a 1.4 TWh y/y rise in gas-fired generation, offsetting coal and nuclear declines, and exceeded prior estimates on weaker renewables and softer coal output. With higher gas load factors, Kpler raised Taiwan’s 2025 LNG demand forecast by 0.3 mt to 23.9 mt (+4–5 cargoes in Q4 2025), though October–November impact remains limited and near-term outlook bearish.

Historical and projected power generation y/y changes by fuel type (TWh)

Elsewhere, India’s LNG demand outlook remains unchanged, with Kpler Insight updating its methodology to a sector-based approach that keeps Q4 2025 steady at 6.4 mt, as elevated spot prices continue to limit both industrial and power consumption. In Bangladesh, May gas demand slipped to 2.3 bcm, down 0.1 bcm y/y and below expectations, as high spot LNG prices and an early monsoon reduced power and non-power use. The September–December LNG import outlook is steady at 2 mt. Both markets remain stable, with no change to near-term price expectations.

India gas demand forecast by sector (bcm)

US Henry Hub: Rising prices stumble on weak demand and robust storage injections

US Henry Hub front-month prices settled at $3.03/MMBtu on 10 September, down from $3.07/MMBtu on 3 September. Prices continued rising throughout last week as falling production and technical factors provided upward support despite a bearish storage print and relatively mild national demand. However, during trading on Wednesday, the bullish winds propelling prices upward began to falter, with weak near-term demand and a sizable storage print on the horizon. Additionally, an early end to pipeline maintenance on the NGPL system and reduced feed gas deliveries into the Sabine Pass and Calcasieu Pass LNG facilities injected some looseness into the market. Henry Hub ultimately fell $0.09/MMBtu on Wednesday from the Tuesday settlement of $3.12/MMBtu.

US domestic gas consumption by sector (bcf/d)

Weather forecasts for the coming week show broadly above-average temperatures across much of the country, though warmer conditions in the shoulder season do not typically spur to a significant uptick in cooling demand. Natural gas-fired power consumption is likely to remain in the 30-40 Bcf/d range in the coming days. With near-term demand looking decidedly weak, Kpler Insight expects Henry Hub prices to remain near $3.00/MMBtu over the next 7 days.

Forecast of cooling degree days

US dry gas production fell to 105-106 Bcf/d over the last week, with upstream operators shutting in wells in tandem with the seasonal decline in cooling requirements. Over the last few years, advances in drilling and completion have enabled producers to more flexibly bring wells on and offline while still maintaining downhole integrity. This has allowed producers to increase supply during higher price and demand periods and curtail volumes when conditions are less favorable. Kpler Insight expects production to average near 105 Bcf/d for the coming week.

The US injected 55 Bcf into underground storage for the week ending 29 August, coming in on the lower end of consensus, but still far above the 5-year average level of 36 Bcf. Despite cooling degree days being well below the 5-year average during the reporting period, lower renewables generation required higher dispatch from natural gas-fired power facilities. Another robust storage build is forecast for the week ending 5 September, with Kpler Insight expecting the US to inject 57 Bcf into underground storage.

US underground gas stocks (bcf)

LNG Supply: Global exports to remain stable into next week despite lower Australian and Malaysian volumes; Russia delivers third Arctic LNG 2 cargo

Global LNG exports rose by 0.61 mt w/w to 8.06 mt last week, up from 7.45 mt the week prior. The increase was largely driven by higher output from the US (+0.43 mt w/w) and Qatar (+0.24 mt w/w), outweighing lower output from Australia (-0.15 mt w/w), Malaysia (-0.09 mt w/w), and smaller aggregate reductions from other countries.

Global LNG exports (mt, 10-day moving average)

In the Atlantic Basin, US LNG exports hit record levels, reaching 2.4 mt last week. Most US liquefaction plants saw w/w increases, especially Cove Point (+0.12 mt) and Calcasieu Pass (+0.07 mt). However, a drop in US LNG exports is expected next week due to lower feedgas volumes at Sabine Pass since 7 September, when the facility recorded its highest feedgas flows in four months. The decline is probably caused by maintenance on one of the terminal’s pipeline feeders.

US LNG exports (mt, 10-day moving average)

Exports from the Yamal LNG facility have increased by 0.07 mt w/w, returning the export trend to seasonal averages and confirming the end of the maintenance period. Four vessels have loaded at the terminal since last week, with all expected to unload at terminals in NWE, according to Kpler data.

Yamal LNG exports (mt, 10-day moving average)

Nigerian LNG exports recovered slightly by 0.07 mt w/w, but are still far from levels seen in August. Only one cargo was exported last week on the Yari LNG, currently on its way to Asia. Another vessel, the LNG Sokoto, entered the berth on 9 September and is currently loading cargo. Despite this, we anticipate Nigerian exports to remain well below August levels for the next couple of weeks based on expected port calls at the terminal in the comings days.

Nigeria’s LNG exports (mt, 10-day moving average)

Similarly, Algerian exports increased slightly by 0.05 mt w/w, but remain below seasonal trends. The overall underperformance mainly stems from lower exports from the Bethioua terminal, with only one cargo loaded last week into the Ougarta LNG carrier, compared to the usual two or three observed during August, suggesting possible issues at the terminal. However, we expect exports from the terminal to continue recovering in the coming days, with the vessels Lalla Fatma N'Soumer, Berge Arzew, and Tessala scheduled to dock at the terminal next week.

Algerian LNG exports (mt, 10-day moving average)

In the Pacific Basin, Australian LNG exports are set to decline w/w to 1.3 mt as scheduled maintenance impacts several plants, with the largest reductions at Chevron’s Gorgon (-0.14 mt) and Wheatstone (-0.21 mt). Despite country-level exports remaining above five-year ranges this week, Kpler Insight expects September volumes to fall by 3.3 mt y/y, driven by intensified summer maintenance and feed gas constraints at the North West Shelf.

Australia’s LNG exports (mt, 10-day moving average)

Malaysia’s LNG exports are set to decline by 0.3 mt w/w at 0.28 mt, driven by decreased output from the 29.3 mtpa Bintulu complex. While 10-day moving averages remain broadly in line with 5-year ranges, loadings have slowed following increased security measures to LNG infrastructure, with 5 cargoes idling close to the plant at the time of writing, though exports are expected to stabilize into next week.

Malaysia’s LNG exports (mt, 10-day moving average)

China’s 6 mtpa Beihai terminal has received a third cargo from the sanctioned Arctic LNG 2 project, delivered as of 9 September by the Zarya , as Novatek officially confirms the start of shipments. The next discharges are expected from Buran, Iris and Arctic Vostok, latter of which completed an STS transfer at the Koryak FSU on 30 August. A further loading from Train 1 is anticipated from the Christophe de Margerie, currently transiting the Northern Sea Route after discharging at Koryak on 6 September.

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Research & analysis driven by proprietary data