Kpler Arbitrage | The Arb View: Eastbound arbs open as heavy sour diffs slide

Dubai structure is holding firm, supported by India’s lower Russian intake and replacement buying, including Dar and Venezuelan cargoes. Atlantic Basin light sweets remain soft into Europe’s maintenance window, and high WAF-to-China freight is still keeping eastbound arbs shut. The standout is LatAm heavies: weaker diffs have lifted the Napo arb to Asia from ~$7 to ~$9/bbl in two weeks, reopening a real eastbound outlet.

Executive summary

Arbitrage Values (16/02/2026 07:30 UTC)

Source: Kpler

Trading calls

- Neutral Dubai M1M3. Displaced Russian Urals will provide support to spot MEG while low risk of disruption in the Strait of Hormuz caps the upside.

- Bearish Brent Dubai EFS. As European crude demand softens amid spring maintenance while CPC flows remain fairly consistent.

Middle East & Asia: Dubai’s Structure Holds as India Rebalances Crude Intake

Dubai’s prompt structure held firm last week, with the 2-month spread trading at an average of $0.80/bbl. The support is still largely India-driven. In January, Russian crude imports slipped to 1mbd, the lowest since 2022, and with roughly 300kbd of primary distillation at Nayara set to go offline, imports should edge lower again going forward. That steady step back from Urals keeps the pool of replacement barrels tight and supports prompt MEG spot grades, even if outright Dubai pricing remains capped as the risk of disruption tied to US–Iran talks remains low.

What stands out is how India is filling the gaps. Earlier this month, Reliance received a rare cargo of Sudanese Dar (API 25, Sulfur 0.1%). On our arbs dashboard, the grade lands competitively into Jamnagar and suits complex runs with healthy middle distillate yields. At the same time, around 6mb of Venezuelan crude has been fixed for April arrival, reportedly by IOC and HPCL. Heavier inflows like that usually support demand for blending components, which helps explain Dubai’s resilience and can lend support to Atlantic Basin light sweets, although the Brent–Dubai EFS likely needs to soften further for those longer-haul trades to materialise.

That being said, we expect the Brent-Dubai EFS to narrow further this week. While there’s a clear physical support under Dubai, the Brent leg looks softer as CPC flows normalise and Europe moves deeper into maintenance. With the April Brent-Dubai EFS averaging around $1.6/bbl this week, the more natural adjustment remains through Brent drifting lower rather than Dubai pushing materially higher.

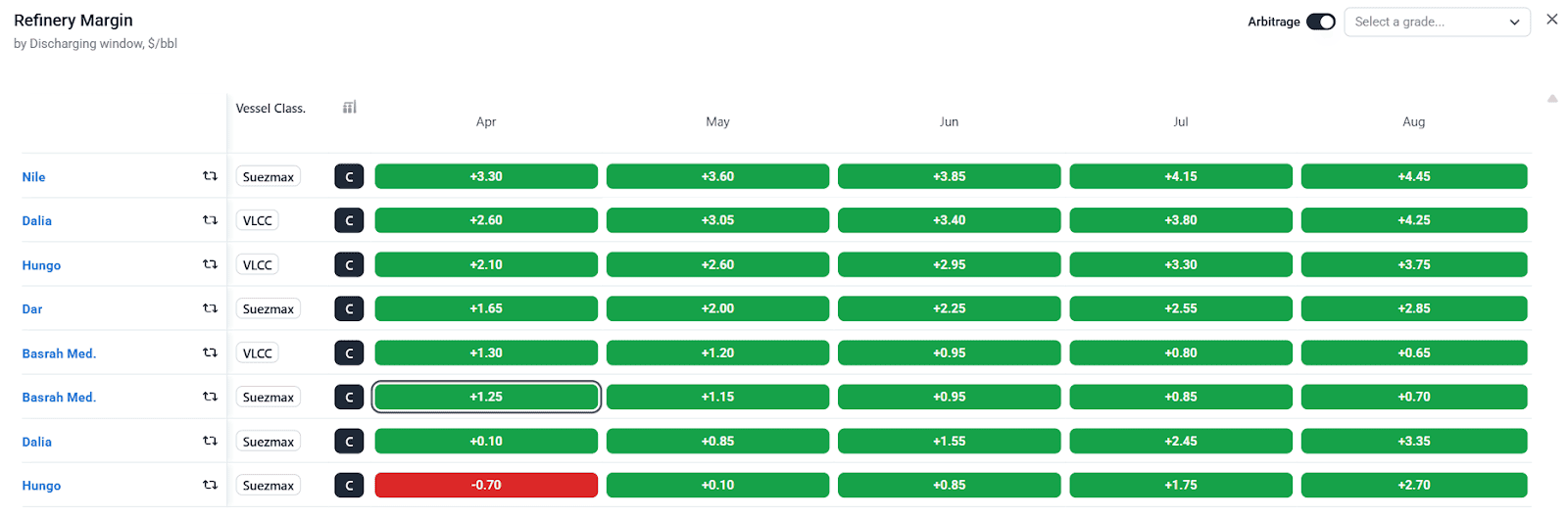

Arb values for selected medium grades into WCI

Source : Kpler

Atlantic Basin: Freight and maintenance weigh on Atlantic light sweets

The setup hasn’t shifted much week on week, but it’s becoming harder for Atlantic light sweets to hold their ground. European options have widened as CPC loadings recover and push more barrels back into the Med, taking the edge off alternatives like Azeri Light and nearby regional grades. With spring maintenance ramping up, prompt buying interest is thinning, so the basin is rebalancing through softer differentials rather than a fresh bid for barrels.

WAF assessments are still feeling the squeeze from both sides. VLCC rates to China have climbed to around $106,000 per day from roughly $76,000 two weeks ago, compressing long haul economics just as Dangote’s RFCC issues reduce regional pull for WAF barrels. To this end, even with the expected narrowing of the EFS, freight needs to ease for buyers to justify increasing purchases. In the meantime, we’ve seen the impact through a steady erosion in diffs, with many Agbami, Bonny Lt ad Qua Iboe losing around $0.20/bbl over the past week, while eastbound arbs remain largely shut on freight.

As mentioned in our previous report, India remains the swing factor as the March cycle develops. Grades such as Agbami and Nemba screen reasonably against current blending economics, but freight is still the gatekeeper. Unless rates ease materially, clearing is likely to continue through pricing adjustments rather than a meaningful reopening of Asia-bound flows.

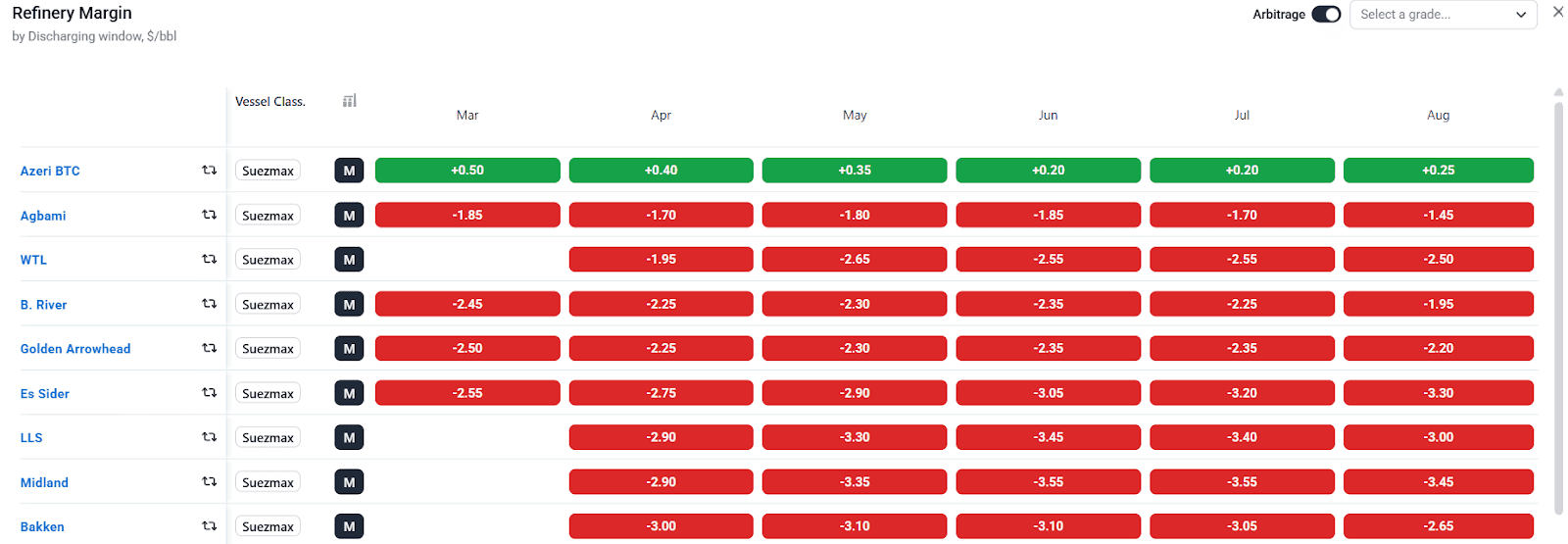

Light sweet arbs to MED

Source : Kpler

Americas: Heavy sour glut pressures LatAm diffs

Latin American heavy sour diffs are at multi-year lows as the USGC weakens into maintenance. Napo is now around $12/bbl below Brent futures, the softest since mid-2023, while Castilla is near record discounts of roughly -$9/bbl to Brent. Oriente has moved the same way, showing a broadly weaker heavy sour market.

The downward pressure is largely coming from the USGC. Venezuelan barrels moving through newly permitted channels are competing directly with Colombian and Canadian grades, and last week’s Venezuelan arrivals only added to prompt length, with cargoes discharging into systems like Valero’s Port Arthur and PBF’s Chalmette, plus some volume heading into commercial storage. With US and European maintenance limiting crude runs into late Q1, refiners have little reason to stretch for extra sour barrels. Differentials are doing the clearing, and the pressure should persist until runs recover.

Where it gets more interesting is the shift in eastbound economics. Two weeks ago, the Napo arb into Asia was closer to $7/bbl on a Suezmax; it is now nearer $9/bbl versus Oman, largely driven by the sharp move lower in LatAm differentials. That $2/bbl swing starts to make the East a credible outlet again, potentially into storage hubs such as Chiba, which could siphon off part of the USGC overhang. For now, the market is still clearing through weaker differentials, and any recovery will likely depend on refinery runs picking up or consistent eastbound flows emerging.

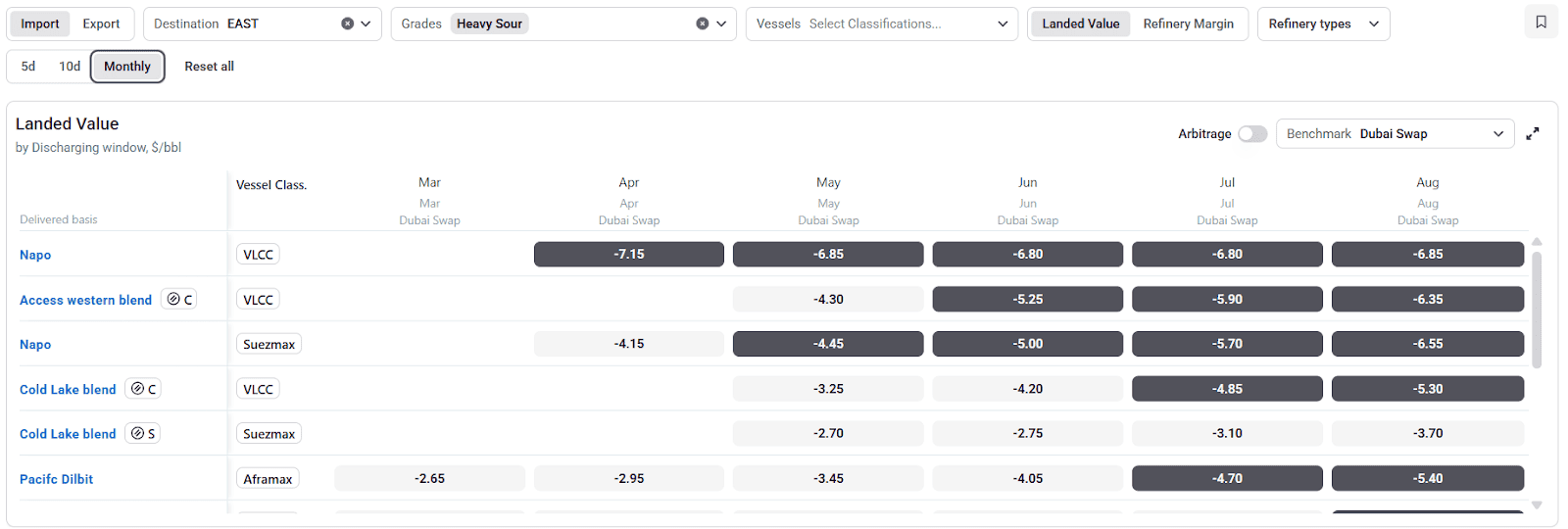

Heavy sour landed value to Eastern Asia

Source : Kpler

Kpler Arbitrage

Kpler’s Arbitrage platform turns complex freight, quality, and benchmark data into simple, actionable arbitrage insights so you can discover value windows, rank opportunities, and build scenarios confidently. With Arbitrage you can:

- Compare delivered crude values by region and freight cost

- Quantify refining margins and route profitability

- Spot open arbitrage opportunities quickly

- Breakdown value drivers like FOB differentials, spreads, and freight

- Model scenarios with custom market inputs

See why the most successful traders and shipping experts use Kpler