US–India trade deal reshapes India’s crude buying pattern

India appears to be winding down April-arrival Russian crude purchases while ramping up Venezuelan cargoes, alongside spot Middle Eastern and WAF supplies, with the US trade deal beginning to take effect.

Market Calls

Executive Summary:

Americas

- Cautiously bearish heavy crude differentials, which have faced downward pressure from an oversupplied market, with sweet-sour spreads widening.

- Expect wider sweet-sour spreads to incentivize US refiners to run a heavier crude diet over the remainder of Q1.

- Optimistic regarding a buildup of US crude stocks, which rose by 8 Mbbls in early February as US refinery maintenance kicks in and imports remained robust.

Europe and Africa

- Slight increases in Russia’s crude supply over the next months, with March levels still remaining below the OPEC quota at 9.33 Mbd.

- Increase expected for Uganda’s medium sweet crude supply from mid-2027 onwards, assuming that construction of the EACOP pipeline concludes until early 2027.

- Delayed ramp-up expected for Namibia’s crude oil production to 2033 considering that FID on Venus has not been taken yet.

Middle East and Asia

- Mildly bearish on heavy crude differentials in Asia, as the tap appears to be opening for Venezuelan crude into India, potentially capping refiners’ demand for other heavy grades.

- Bearish on Urals prices in Asia, as steeper discounts will be needed to pull India back on economic grounds and to displace Iranian barrels in China.

- Bullish on Saudi crude exports to China in March, as lower OSPs have enhanced competitiveness against other suppliers.

Americas: Wide sweet-sour spreads incentivises heavier crude diet

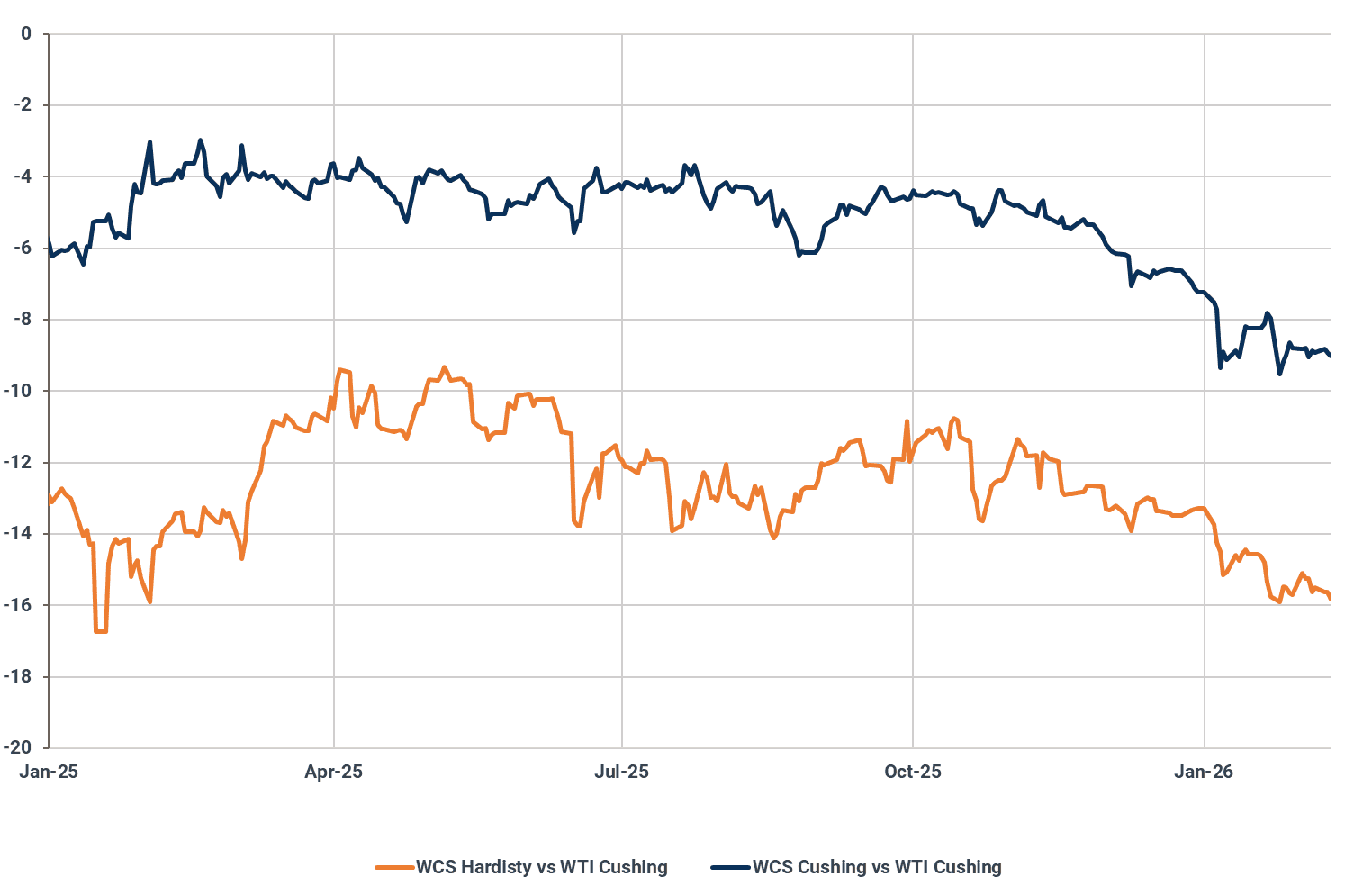

Heavy sour differentials hit multi-year lows

America's heavy sour crude differentials are under renewed pressure as Venezuelan barrels return to the US Gulf Coast, intensifying competition in an already well-supplied market. The redirection of Venezuelan flows to the US has coincided with robust crude production from Canada's oil sands in Alberta, where output continues to set new highs. Even in the US Gulf—traditionally a key clearing point for medium-grade production—non-shale supply remains resilient, with Gulf output hovering at multi-year highs above 2 Mbd. The result is a crowded slate of heavier and medium-sour barrels competing for limited refinery demand.

Pricing signals reflect this oversupply. Ecuador’s Napo has recently fallen to $15–$16/bbl discounts versus May NYMEX WTI, its weakest level since May 2023, with Colombia’s Castilla sliding to a record discount of around -$9.50/bbl to May ICE Brent, underscoring intense competition for US Gulf placement. In Canada, WCS Hardisty differentials have eased further, in line with our prior view, as ample Albertan supply tightens Enbridge Mainline capacity and reinforces regional imbalances.

Looking ahead, downside risks persist over the remainder of Q1. Rising Mainline apportionment—reaching 12% for heavy crude in February—alongside limited relief via TMX, signals that excess supply will continue to weigh on regional grades. At the same time, US refinery maintenance is approaching its seasonal peak, with February crude demand expected to average 15.6 Mbd, down roughly 500 kbd month-on-month. As refinery runs soften and balances lengthen, heavy sour differentials are likely to remain under pressure before any meaningful recovery emerges later in the quarter.

WCS Hardisty crude differentials versus WTI, $/bbl

Source: Argus Media

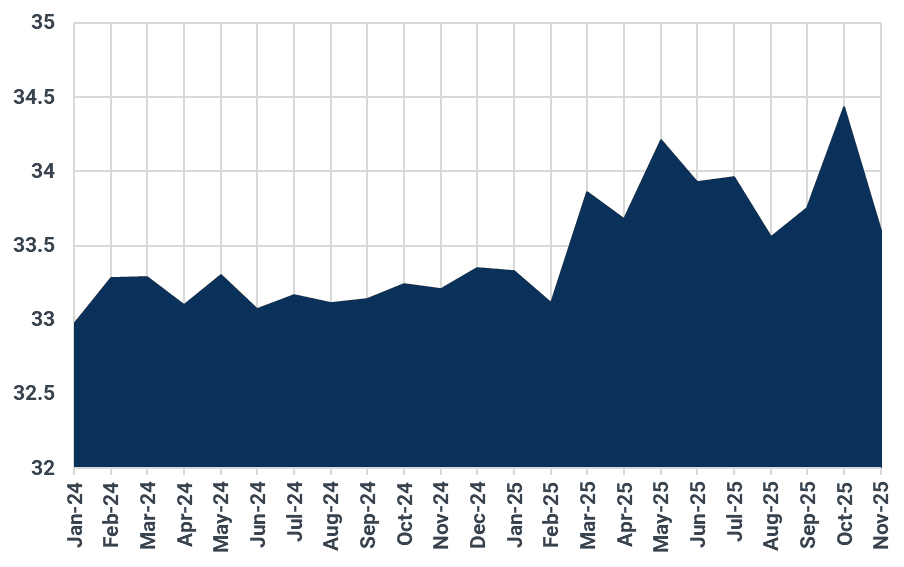

Ample heavy supply to lead to a heavier US crude diet

US refiners are actively increasing heavy sour intake as discounted barrels improve crude slate economics. Valero, Phillips 66, and Marathon Petroleum have all purchased Venezuelan crude under the US-administered sales process, signaling a structural shift toward heavier grades.

Notably, Phillips 66 confirmed it can process up to 250 kbd of Venezuelan crude across its system, which includes the 265 kbd Sweeny and 264 kbd Lake Charles refineries, and is currently maxing out heavy supplies to capture favourable discounts, according to the firm's CEO Mark Lashier.

Valero is also ramping up Venezuelan runs and can process substantially more than the 240 kbd the firm handled pre-sanctions, supported by expanded coking capacity at its 380 kbd Port Arthur refinery. While Marathon has secured Venezuelan cargoes for its 606 kbd Garyville plant, with sour crude now accounting for 50% of its feedstock, up from 47% in Q4 2025, the refiner mentioned that it will stick primarily to Canadian and Mexican grades moving forward.

As sweet–sour spreads widened through late 2025, refiners signalled higher heavy intake—a trend that is now weighing on the average API gravity of US crude runs and is likely to persist as long as heavy discounts remain attractive.

US crude intake by API gravity, degrees (°)

Source: EIA

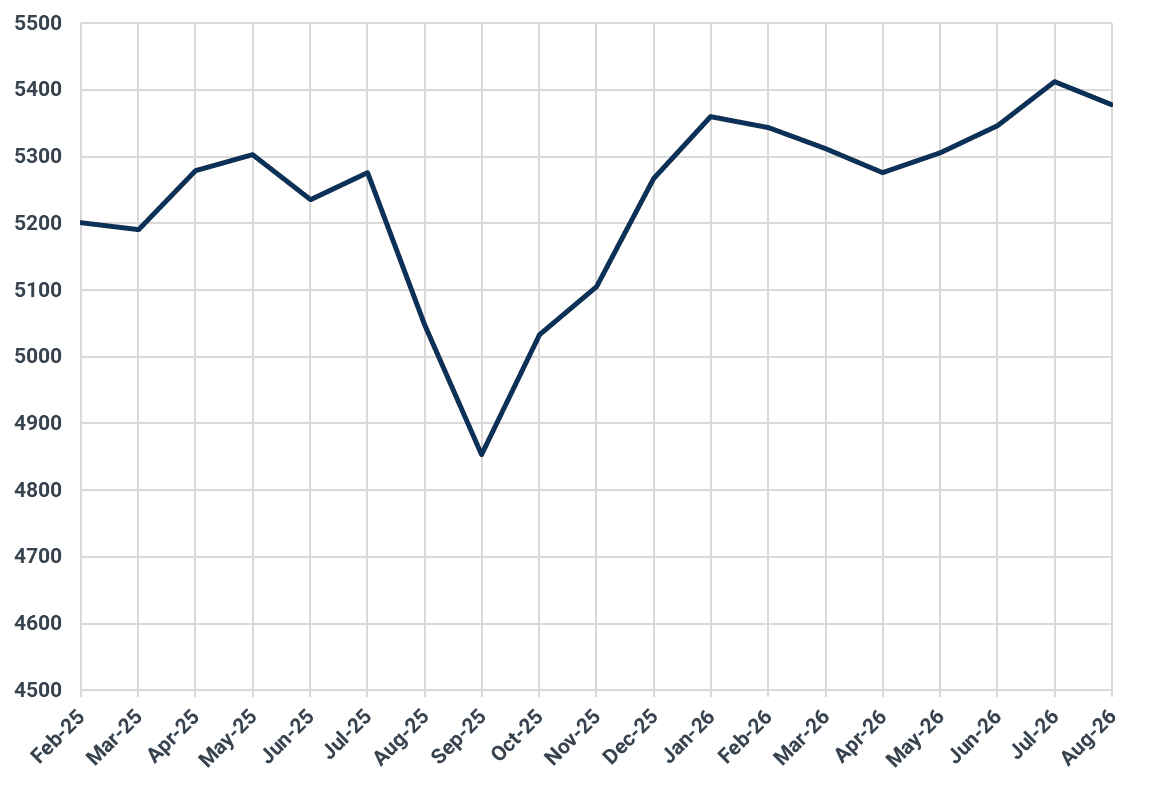

Seasonal US refinery maintenance lifts US crude stocks

The onset of the US refinery maintenance season is keeping overall balances longer, as crude demand softens against still-elevated supply. According to the latest weekly EIA data, US crude stocks rose by over 8 Mbbls to 429 Mbbls in early February, underscoring the impact of lower refinery runs and robust inflows.

Crude and condensate seaborne imports into the US Gulf averaged 1.4 Mbd in the week beginning 26 January—the highest weekly level since May last year—while higher Canadian availability continues to reinforce supply.

At the same time, primary distillation offline capacity is set to average around 300 kbd more than January levels at around 1.1 Mbd, according to IIR, before easing to 700 kbd in March. While this is temporary, balances are likely to remain elevated versus prior years into spring, even as US shale output gradually moderates.

US crude and condensate balance, Mbd

Source: Kpler

Atlantic Basin: Uganda could join the ranks of oil producers in 2027

Slow recovery in Russia’s upstream and downstream sectors after drone strikes

Russian crude supply continues to struggle. Crude-only output fell by 90 kbd m/m in January to a three-month low of 9.24 Mbd, with production expected to edge up only slightly to around 9.3 Mbd this month. We see Russia underproducing its OPEC target again in March, with crude output set to average 9.33 Mbd, below its quota of 9.574 Mbd. Notably, crude held in floating storage has declined over the same period, easing from multi-year highs of about 19 Mbbls in late January to roughly 14 Mbbls by mid-February.

Downstream operations are likewise recovering only slowly from outage-related disruptions. Offline refining capacity has fallen sharply from nearly 1.5 Mbd in December to below 700 kbd in January and around 390 kbd in February (IIR), allowing crude intake to rebound to 5.3–5.4 Mbd in January, the highest level in the past year.

Product exports also strengthened, rising to a two-year high of 2.49 Mbd in January, heading mainly to Turkey, China, Brazil and Singapore. Despite these gains, refinery runs remain below five-year averages, reflecting continued operational caution and lingering maintenance constraints. We expect crude runs to broadly hold near current levels in Q1, with limited upside due to ongoing outage risks and maintenance backlogs.

Russia refinery runs outlook, kbd

Source: Kpler

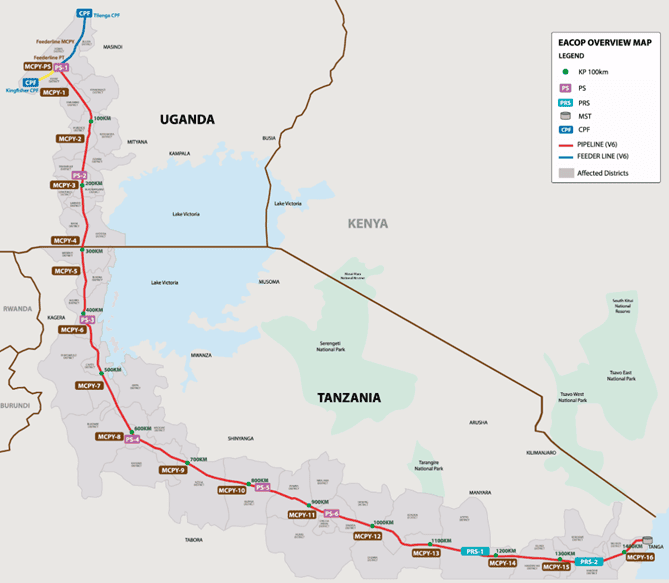

We expect first oil at Uganda’s 230 kbd Lake Albert oil development in 2027

Uganda’s upstream expansion appears to be gathering momentum. According to statements by Uganda National Oil Company (UNOC) chief executive Proscovia Nabbanja, the 230 kbd Lake Albert crude oil development remains on track for commissioning by July. Drilling at the Tilenga and Kingfisher fields—operated by TotalEnergies and CNOOC, respectively—is reportedly ahead of schedule. Nabbanja added that plateau production could be reached within two years, implying output of 230 kbd by mid-2028, with production sustained for five to six years.

While this outlook reflects optimism from project partners—TotalEnergies (56.67%), UNOC (15%), and CNOOC (28.33%)—we remain more cautious. With land acquisition along the full pipeline route reportedly completed, construction of the East African Crude Oil Pipeline (EACOP) is still only about 62% complete. Given the project’s history of delays, financing challenges, and environmental opposition, further setbacks remain possible. As a result, we currently expect production to begin ramping up from Q3 2027, with nameplate capacity of 230 kbd potentially reached by mid-2029. The crude produced is expected to be a medium sweet grade (30–34° API), low in sulfur but waxy in nature—one of the key reasons EACOP is being developed as a heated pipeline to ensure steady flow.

The East Africa Crude Oil Pipeline Route

Source: EACOP

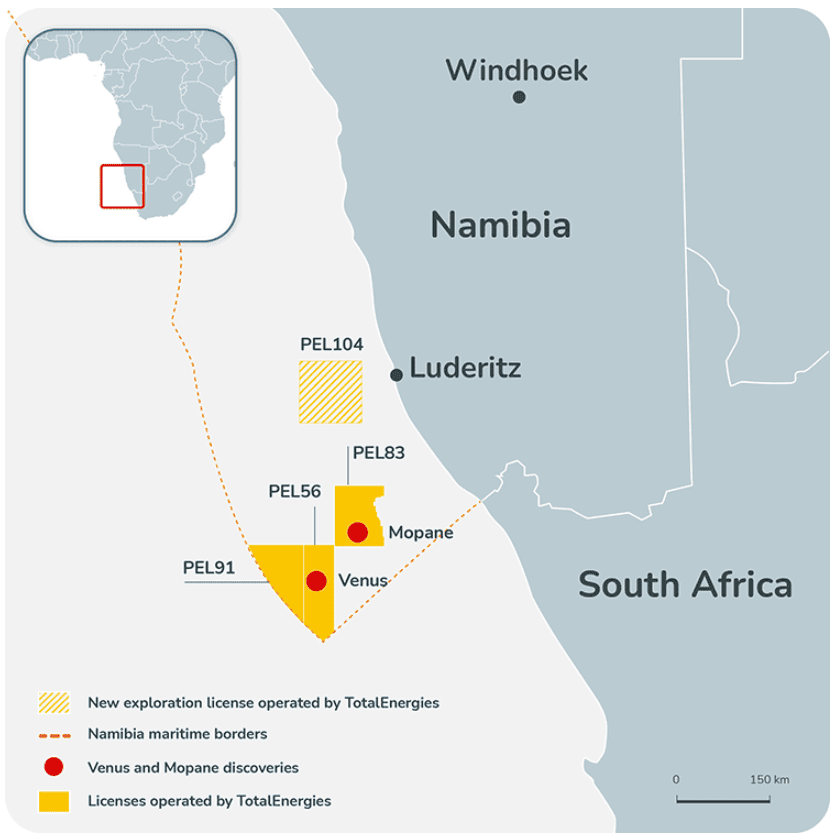

Still no FID on Namibia's Venus discovery - we expect delayed ramp-up in 2033

Namibia’s two flagship offshore oil projects—Venus and Mopane—continue to advance, though they remain at different stages of development. Venus, operated by TotalEnergies, is the more mature project, with appraisal largely completed and a development concept in place. Project partners are working toward the conditions required for a final investment decision (FID) in 2026, with first oil targeted toward the end of the decade. Mopane, which also recently came under TotalEnergies’ operatorship following a transaction with Galp, is at an earlier stage, with a multi-well appraisal campaign planned for 2026 to further delineate resources ahead of development decisions.

In early February, TotalEnergies announced that it had signed agreements to acquire a 42.5% operated interest in the offshore PEL104 exploration license from Eight Offshore Investments Holdings and Maravilla Oil & Gas. Subject to regulatory and partner approvals, the company said it would become operator of the block alongside Petrobras, Namcor, and Eight. However, the Namibian government subsequently stated that it would not recognise the transaction, arguing that the parties failed to comply with legal requirements by not formally notifying authorities or obtaining prior ministerial approval.

Reflecting slower-than-expected project progress, we have pushed our forecast for Namibia’s crude supply ramp-up from 2030 to 2033, as neither Venus nor Mopane has yet reached FID. We now expect production to rise to around 150 kbd in 2033, increase to 230 kbd in 2034, and approach 300 kbd by 2036.

Namibia offshore fields

Source: TotalEnergies

Middle East and Asia: India adjusts crude buying pattern following US trade deal

Urals weakens as India pulls back; China unlikely to take up the slack

Urals prices softened further in Asia as India reportedly slowed—if not entirely paused—the procurement of April-arrival cargoes amid uncertain policy guidance from New Delhi. No public confirmation or directive has been issued by the Indian government to refiners on whether the country will move away from energy trade with Russia following the trade deal with the US to lower tariffs. Nonetheless, sanctioned Nayara Energy is scheduled to take its 400 kbd Vadinar refinery offline for maintenance in April, a move that will significantly reduce India’s demand for Russian crude. Against this backdrop, Urals discounts widened to -$11.9/bbl against Dated Brent on a delivered-India basis from -$11/bbl last week, marking the weakest level since June 2023, according to Argus Media data.

Offers for Urals are expected to soften further in China, as sellers can rely only on independent refiners to absorb cargoes shunned by India. March-arrival Urals is currently trading at around -$11/bbl against ICE Brent, broadly in line with Iran Light at roughly -$10.5/bbl. However, China’s seaborne imports of Russian crude already hit a record 1.72 mbd in January—even without participation from state-owned refiners—suggesting that any additional buying appetite is likely to be limited.

That said, unless Urals prices fall meaningfully below Iranian crude, it is unlikely that China’s independent refiners will materially increase their purchases of Russian oil. Depending on whether India’s pullback from Russian crude proves to be a short-lived dynamic or a structural policy shift, this could lead to a build-up of Russian floating storage in the near term and potentially force Moscow to cut oil production over the long run.

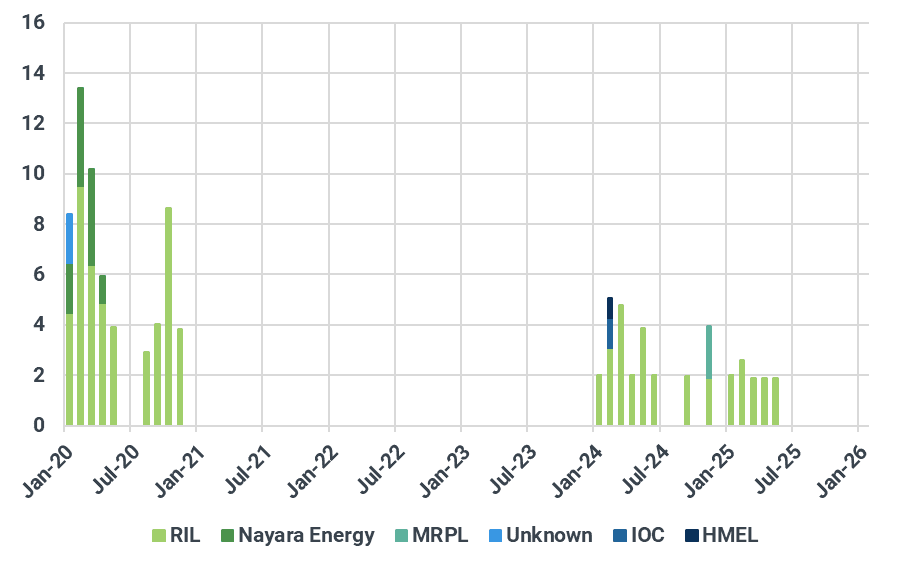

India's imports of Venezuelan crude by buyer, mb

Source: Kpler

India likely lines up 8 mb of Venezuelan crude from trading houses

India is ramping up purchases of Venezuelan crude following the US issuance of a general license lifting most trade restrictions. Privately owned Reliance is believed to have secured two VLCC cargoes for April delivery, while IOC and HPCL jointly purchased 2 mb, with BPCL also heard to be taking a further 2 mb, also for April arrival. The deals were concluded with Vitol and Trafigura at around -$6 to -$6.5/bbl against ICE Brent on a delivered basis, although it remains unclear whether the pricing is linked to the May or June Brent contract.

While Reliance had been a regular buyer of Venezuelan crude both before and during US sanctions on the Latin American producer under a special waiver, IOC had only taken one cargo previously. Neither BPCL nor HPCL has bought Venezuelan crude before, although the Bina, Kochi and Vizag refineries are equipped to process heavy grades such as Merey.

That said, it remains to be seen whether Indian refiners will sustain this buying momentum, as it will hinge on economics and crude availability—both of which are partly shaped by procurement interest from US Gulf Coast refiners. At present, Merey is assessed at around $2/bbl cheaper than Canada’s Cold Lake into India. With Latin American crude differentials sliding sharply on an FOB basis, Merey is likely to follow suit to compete for USGC demand and/or move east in search of outlets in India.

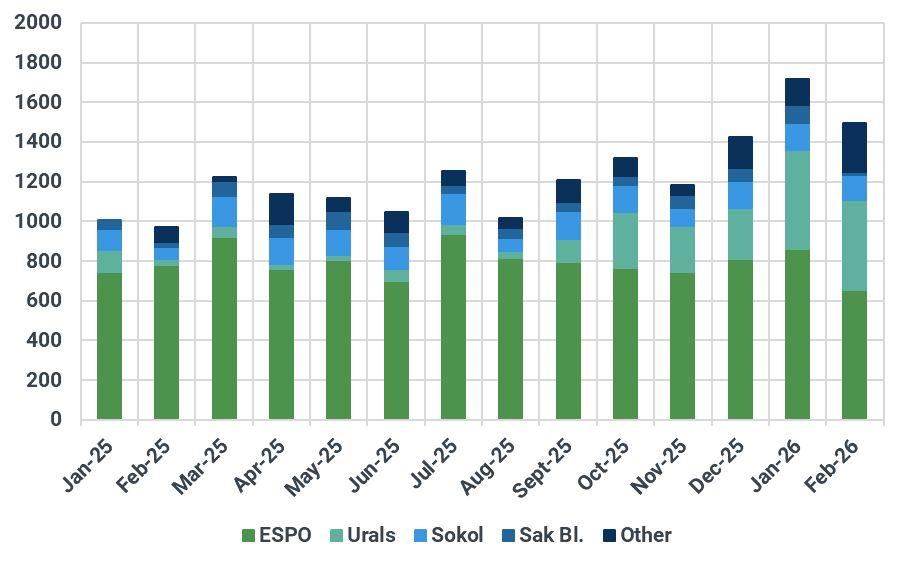

China's imports of seaborne Russian crude by grade (as of Feb 11), kbd

Source: Kpler

China keeps March-loading Saudi crude liftings elevated

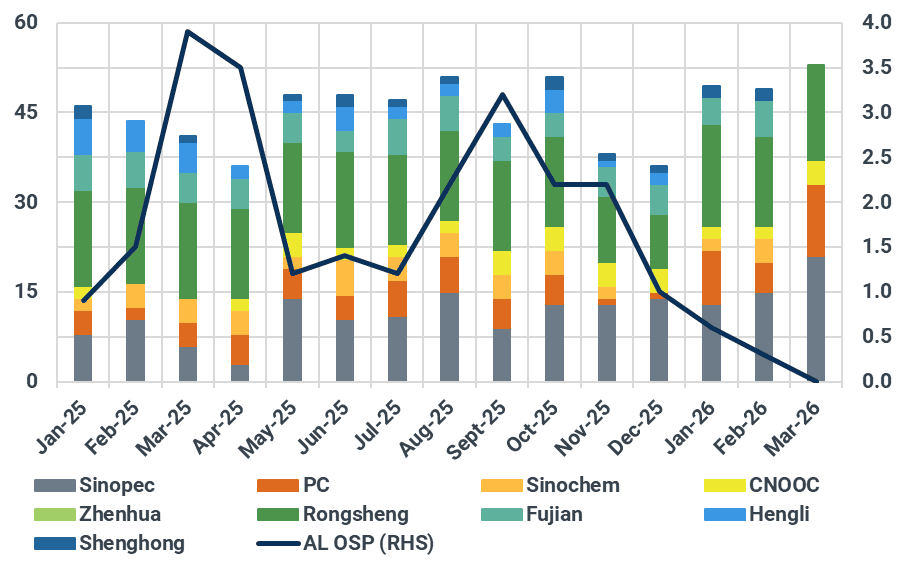

China is likely to receive at least 53 mb of March-loading Saudi crude, according to market participants—the highest level in at least two years. While allocation details remain unclear at the time of writing, market talk suggests volumes could reach as high as 60 mb, with Sinopec taking around 20 mb.

China’s liftings of Saudi crude stayed elevated in recent months, as Saudi Aramco trimmed OSPs and made its offerings economically attractive relative to other suppliers. Aramco cut the March Arab Light OSP by $0.30/bbl m/m to parity with the Dubai/Oman average for Asian buyers, the lowest level since December 2020. This leaves Arab Light around $0.30–$0.40/bbl cheaper than Abu Dhabi’s Upper Zakum. Against a backdrop of elevated freight rates, Arab Medium—whose OSP was lowered by $0.40/bbl m/m—is assessed to be at least $2/bbl cheaper than Brazil’s Tupi for April arrivals.

Therefore, although refiners are set to enter heavy maintenance from late April, state-owned firms appear willing to snap up large volumes of attractively priced feedstock, potentially for stockbuilding. Argus Media data show that Chinese refiners purchased at least 33 mb of Brazilian crude for April delivery, below the December peak of 42.7 mb, but still above the 27–30 mb range seen in April–May last year.

China's liftings of Saudi crude by firm, mb; Arab Light OSP vs Oman/Dubai avg, $/bbl

Source: Kpler, Saudi Aramco

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler