Natural gas and LNG: Top 5 market drivers for 2026

This article was first posted on Kpler Insight on 7 January.

The global gas market is undergoing a significant period of transition, shifting from the tight market conditions that have prevailed since 2022 toward a phase of oversupply. From a fundamental perspective, the LNG market balance is projected to loosen in 2026, largely driven by a substantial increase in LNG supply. As the market finds a new balance, global gas prices are expected to drop to compress margins for US LNG offtakers; however, not to the extent that US cargo cancellations become necessary. Alongside these supply dynamics, we anticipate a gradual return to more traditional trade routes. LNG vessels could potentially resume transit through the Suez Canal, contingent on sustained peace between Israel and Hamas. Such developments would ease shipping bottlenecks and improve delivery flexibility. Nevertheless, uncertainty will remain a defining feature of the market. The outcome of Russia-Ukraine peace negotiations continues to represent a key source of risk, as a resolution—or lack thereof—could influence the potential return of Russian gas and LNG to the global market. 2026 is set to be a transitional year, characterized by ample LNG supply, shifting trade flows, and persistent geopolitical uncertainty, requiring market participants to carefully navigate both risks and opportunities. In this piece, we outline the top 5 things to watch out for in this market in 2026.

1. The 2026 LNG supply wave: how big and how fast?

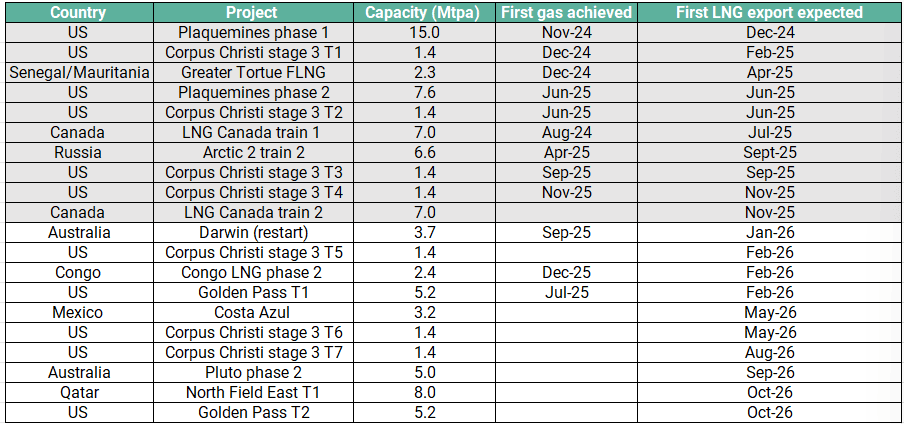

Approximately 37 mtpa of new liquefaction capacity is slated to come online in 2026, adding to the 51 mtpa of capacity that entered service in 2025 (including Plaquemines phase 1).

The new projects, as outlined in the table below, are expected to come online steadily through the year, resulting in a sustained increase in LNG supply, particularly from the Atlantic basin. Kpler Insight currently forecasts global LNG supply to rise by over 46 mt in 2025 to 475.3 mt. However, given regular delays associated with LNG developments, close monitoring of commissioning timelines and ramp-up profiles will be critical in determining the magnitude of supply growth in 2026.

The two biggest projects starting up next year are the 15.6 mtpa Golden Pass LNG facility in the US and the first 8 mtpa train of Qatar’s North Field East (NFE) expansion, but the timelines of these two projects are also the most in flux. Golden Pass has suffered delays due to its original EPC contractor, Zachry, declaring bankruptcy while NFE’s construction timeline is uncertain, with rumours of possible delays beyond our currently forecast start-up date of October 2026. Pluto LNG Phase 2 in Australia could also suffer delays due to the possibility of strike actions by workers at the project.

New liquefaction capacity additions by project and start-up year

Source: Kpler Insight

2. Ukraine peace scenario: implications for European gas balances and global LNG flows

Despite recent progress toward a potential peace deal between Russia and Ukraine, we believe significant uncertainty remains before any agreement is finalised. Key unresolved issues include borders, security guarantees, and the future involvement and commitment of both the EU and the US. Against this backdrop, Kpler Insight’s base case assumes the following:

- Kpler Insight does not expect a return of Russian pipeline gas flows via Ukraine or through any previously lost routes. Instead, our view is that the EU will pass legislation in early 2026 mandating a phase-out of Russian pipeline gas and LNG imports, with full implementation expected in 2027. This would further open the door to US LNG into Europe, despite subdued aggregate gas consumption across the continent and tightening margins for US exporters.

- The end of spot purchases of Russian pipeline gas and LNG in 2026 would have a limited impact on global LNG markets and European supply. Uncommitted cargoes from Yamal are expected to find alternative destinations, including Turkey and Egypt.

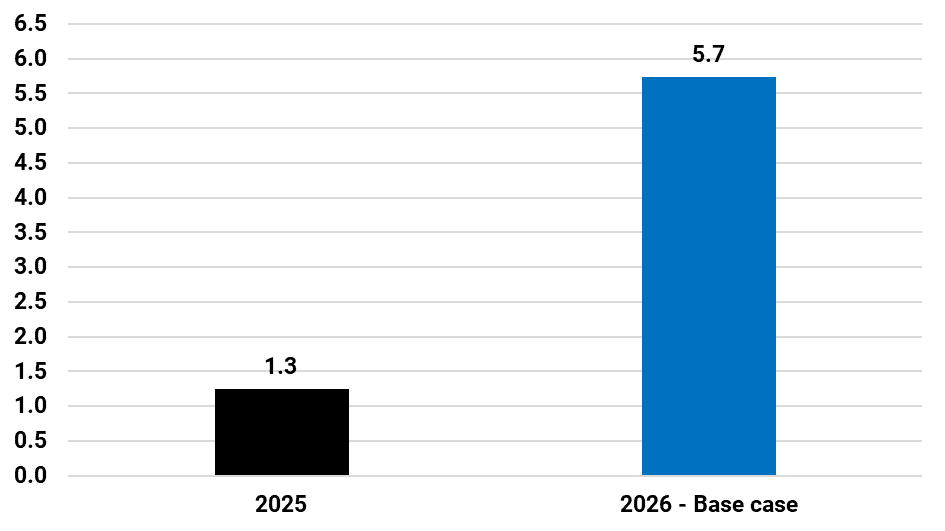

- Our current forecast assumes no sanctions relief, capping Arctic LNG 2 exports at 5.7 Mt in 2026 or nearly 45% utilisation of its two trains.

- Ukraine is expected to continue relying on EU gas imports while the conflict persists. A peace deal would reduce this dependence, as domestic production could be sustained at higher levels following an end to attacks on gas infrastructure.

One of the key potential market movers is the scope for a lifting of sanctions on Russian LNG projects. However, Kpler Insight’s base case does not assume this outcome, given lingering uncertainty around negotiati

Annual Arctic LNG-2 exports, including 2026 forecast (Mt):

Source: Kpler Insight

3. Cheaper gas, new demand? Will opportunistic consumption revive in Asia and Europe in 2026?

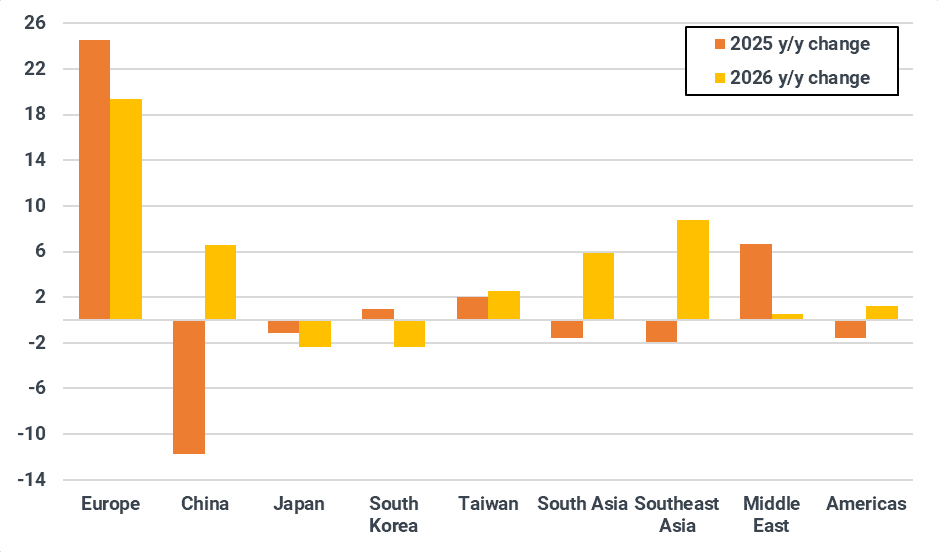

Asian opportunistic spot demand is likely to revive in 2026, particularly in China and India. As additional global LNG supply pressures Asian spot prices to below $10/MMBtu on average in 2026, margins could widen enough to incentivise spot LNG procurement, supported by expanding Chinese storage capacity. Kpler Insight’s base case forecasts 73 mt of Chinese LNG demand in 2026, with 2 mt upside potential should prices fall by a further $1/MMBtu, mainly from transport and industrial users. India’s LNG demand is expected to increase by 5 mt to 29.3 mt in 2026 under our base case forecast. India is also expected to display demand elasticity to prices, with potential to add around 0.3 mt for every $1/MMBtu drop, driven largely by industrial fuel switching and to a lesser extent by the city gas and power sectors.

In Europe, we expect LNG demand in 2026 to rise by 18 Mt to 145 mt. This increase does not factor in a material recovery in gas consumption. Kpler Insight anticipates that EU-27 gas consumption will remain subdued in 2026, rising just 0.4% y/y to 320.4 bcm, with limited support from lower prices, which will induce a modest recovery in industrial gas demand in Northwest Europe, and only a marginal uplift in gas-for-power demand, mainly for cooling during the summer in Southern Europe. The rise in European LNG demand is rather a reflection of high storage injection needs as we expect the EU-27 UGS levels to end the 25-26 winter period at slightly lower levels than last year. In addition, the EU’s ample regasification and underground storage infrastructure will serve as a source of market flexibility to accommodate higher LNG supply from the Atlantic basin, mainly from the US.

Year-on-year change in LNG demand by region (Mt)

Source: Kpler Insight

4. Back to Suez? Implications for freight and LNG trade in 2026

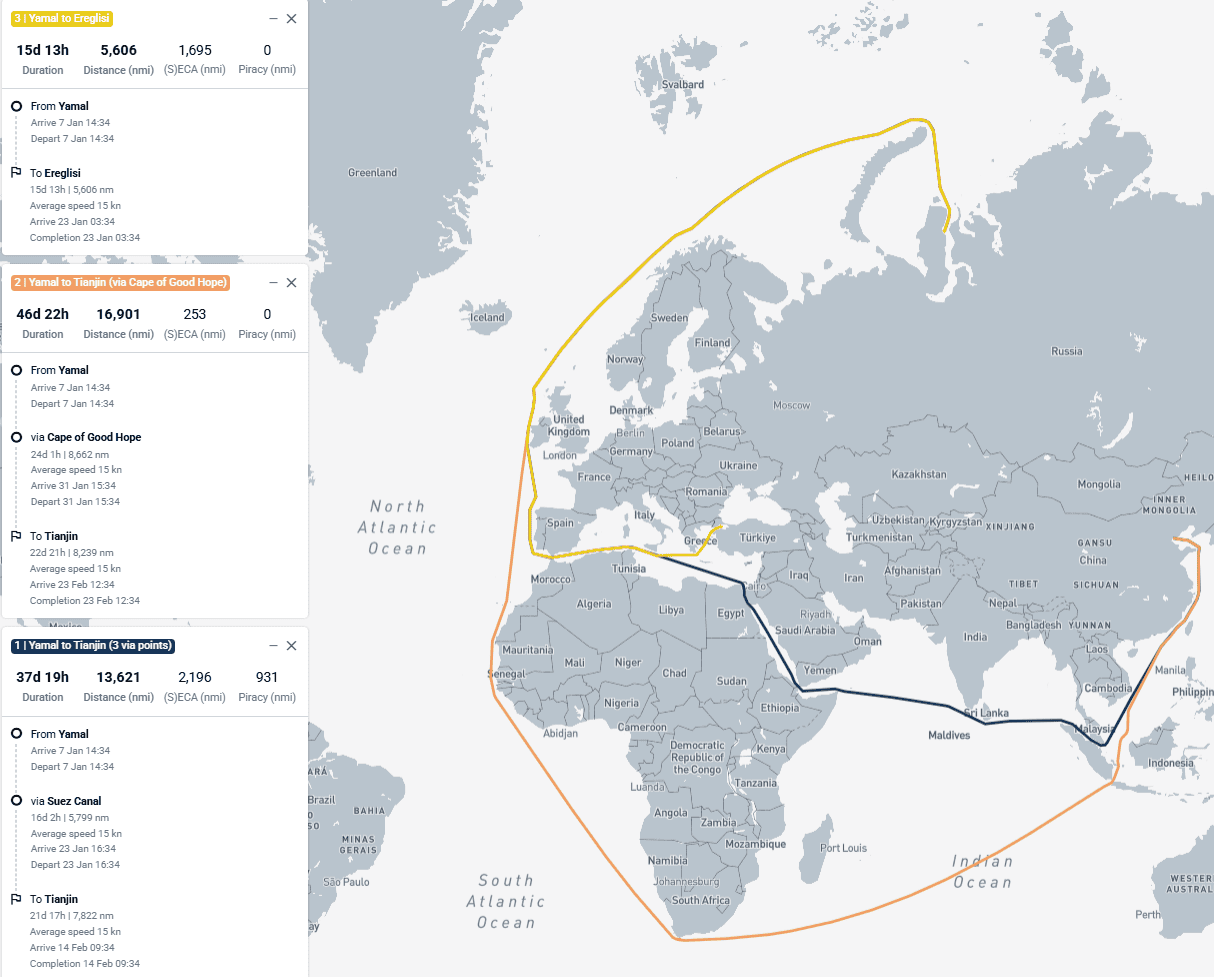

Following the first transit of a laden LNG vessel (Zarya) via the Suez Canal at the end of November, expectations are rising for a resumption of this major trading route in 2026. In our view, its full reopening will depend primarily on sustained progress in the peace plan between Israel and Hamas, as a credible and lasting peace deal would likely reduce the risk of attacks and thus lower insurance costs for vessels crossing the route.

Until recently, the Canal was used only for LNG imports into Egypt and Jordan. The crossing of the Zarya vessel, loaded with an Arctic LNG 2 cargo that was discharged at the Beihai port in China, signals that vessels transporting Russian LNG could continue using the route in 2026, particularly when the NSR is closed. A full reopening of the Suez Canal will not be a game-changer for US LNG exports heading to Asia, as voyage times are similar via the Cape of Good Hope. However, it would provide much more flexibility for exports of Russian LNG heading to Asia during winter, and for Qatari exports serving European clients.

Voyage time comparison for Yamal LNG exports to Asia via Suez Canal and Cape of Good Hope

Source: Kpler

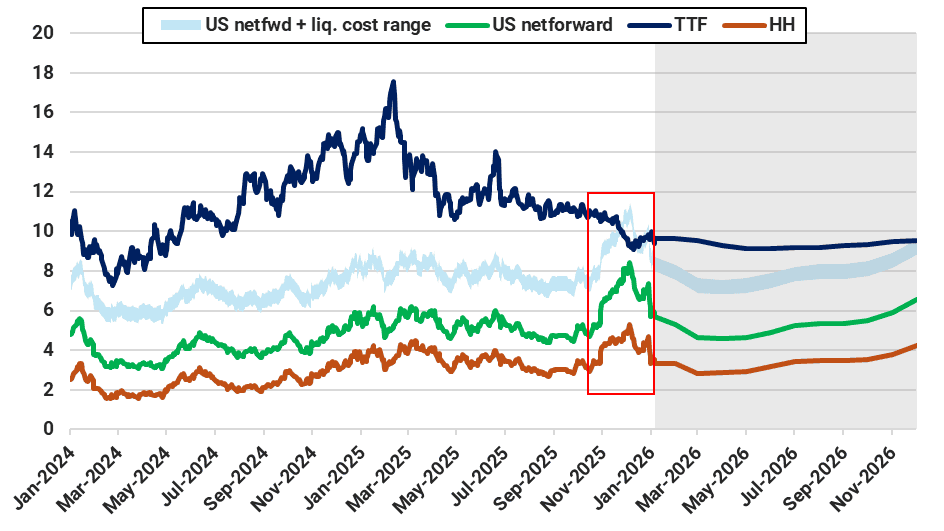

5. Margins under pressure: US LNG exporters and portfolio players in 2026

The TTF-Henry Hub spread tightened to multi-year lows in December 2025 and, together with elevated Atlantic Basin freight rates at the time, squeezed margins for US LNG exporters and portfolio players.

While this has raised concerns around the future profitability of US LNG exports, Kpler Insight does not expect US cargo cancellations in 2026, instead, we anticipate that lower margins will likely accelerate optimisation as exporters and portfolio players adapt to a new economic reality of lower TTF prices, and LNG exports playing an increasing role in shaping Henry Hub prices, particularly in times of peak domestic demand in the US.

TTF, Henry Hub, and US netforward prices and forward curves ($/MMBtu)

Sources: ICE, NYMEX, Spark Commodities. Netforward USGC to NWE calculation is 115% Henry Hub contract plus shipping and regasification costs into Gate (Spark Commodities).

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler