Non-Russian buying frenzy fuels Dubai gains, OSP hikes

Executive Summary

Source: ICE, CME, Argus Media

Market & Trading calls

Americas:

- Bearish US crude supply as steadily declining upstream activity keeps a lid on output over the remainder of the year.

- Bullish on US market structures in August amid tighter balances, but a lengthening in the US balance thereafter will increasingly pressure regional grades.

- Bearish on ANS crude differentials as an end of pipeline and field maintenance keeps ANS output on an upward trend in August and September.

Europe and Africa:

- Bearish on Johan Sverdrup differentials amid increasing sour competition into Europe and approaching maintenance season

- Neutral-to-bearish on Atlantic light sweet differentials with Forties quality to become lighter in the next trade cycle, weighing on competing grades

- Slightly bearish on crude import volumes to Nigeria's Dangote refinery in Aug-Sep, after inflows hit record highs in July.

Middle East - Asia - Russia:

- Bullish on India’s Middle East crude demand, as state refiners ramp up purchases to hedge against potential supply disruptions amid geopolitical uncertainty.

- Neutral to moderately bullish on China’s Russian crude imports: teapots remain constrained by tight import quotas, while state-owned refiners are holding off pending policy clarity.

- Neutral on Dubai backwardation, with rising OPEC supply and incoming arbitrage barrels expected to offset firm Indian demand for non-Russian alternatives.

Americas: Declining US shale supply not enough to keep US balances tight

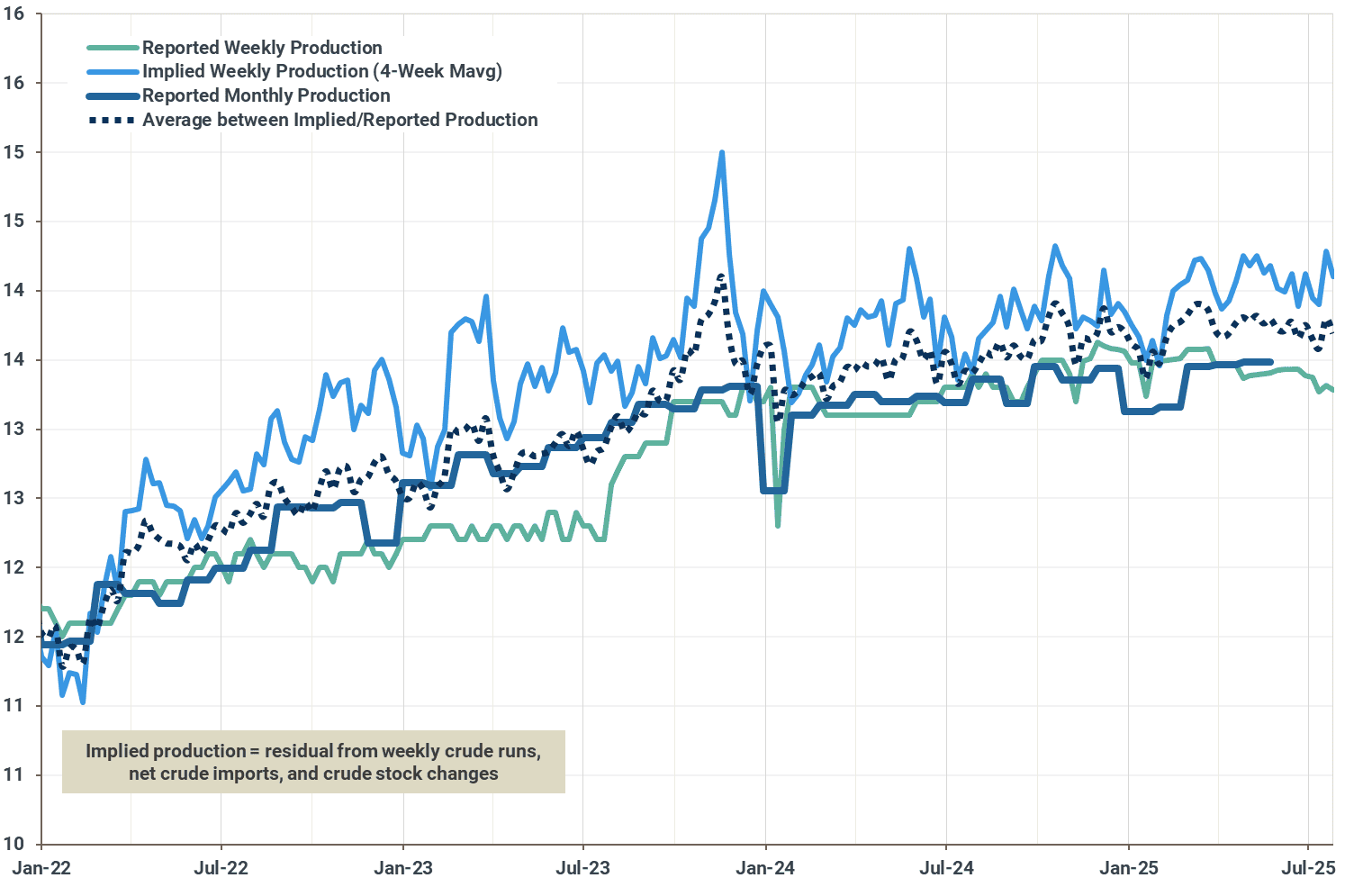

Weekly US crude supply nears 1-year lows

The EIA's weekly estimates showed US crude supply falling to near one-year lows, with output averaging only 13.28 Mbd in late July. While the EIA's weekly figures can often be volatile and diverge from official monthly data, the sustained low readings suggest that output remains under pressure.

This trend aligns with our view that production will face increasing pressure over the remainder of the year, driven by accelerating natural declines in aging fields and a slowdown in upstream activity. The oil rig count exemplifies this slowdown, having fallen to 410 from 482 a year ago. Major producers like Diamondback Energy have corroborated this assumption, noting on a recent earnings call that the shale producer dropped four rigs in Q2 and expects US shale supply to peak at current price levels. Uncertainty regarding the impact of US tariffs and sanctions on oil markets, as well as the unwinding of OPEC+ production cuts will keep a lid on US upstream activity, painting a bearish picture for US shale supply in 2026.

Reported and implied US crude supply figures, Mbd

Source: EIA

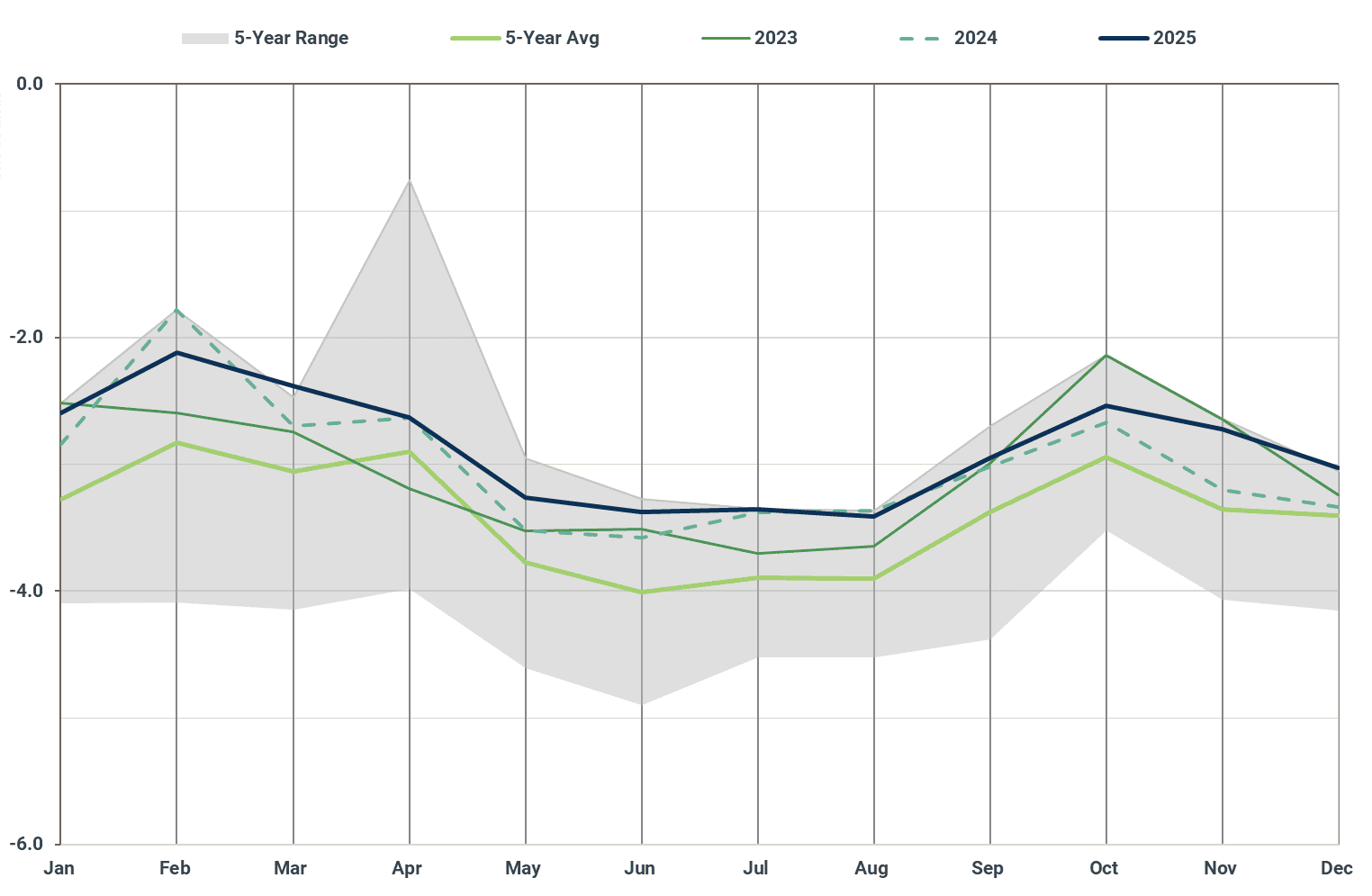

US crude stocks remain tight amid robust demand

US crude stocks remain tight, with inventories settling at 424 Mbbls in late July, representing a decline of 5 Mbbls versus year-ago levels and remaining below the 5-year range. Considering that US crude demand is expected to remain robust at around 16.8 Mbd in August, inventories could test lower levels in the near future. This is expected to keep regional market structures supported for the time being, with M1 versus M2 spreads for WTI, Mars, and LLS currently hovering just shy of a $1/bbl premium.

It should be noted, however, that the US crude balance is expected to lengthen strongly over the remainder of the year, largely on the back of lower crude throughput levels, which will pressure regionally produced grades and will help regional refiners replenish depleted inventories. We currently estimate that the US crude balance will remain around 200 kbd above year-ago levels in September and October.

US crude and condensate balance, Mbd

Source: Kpler

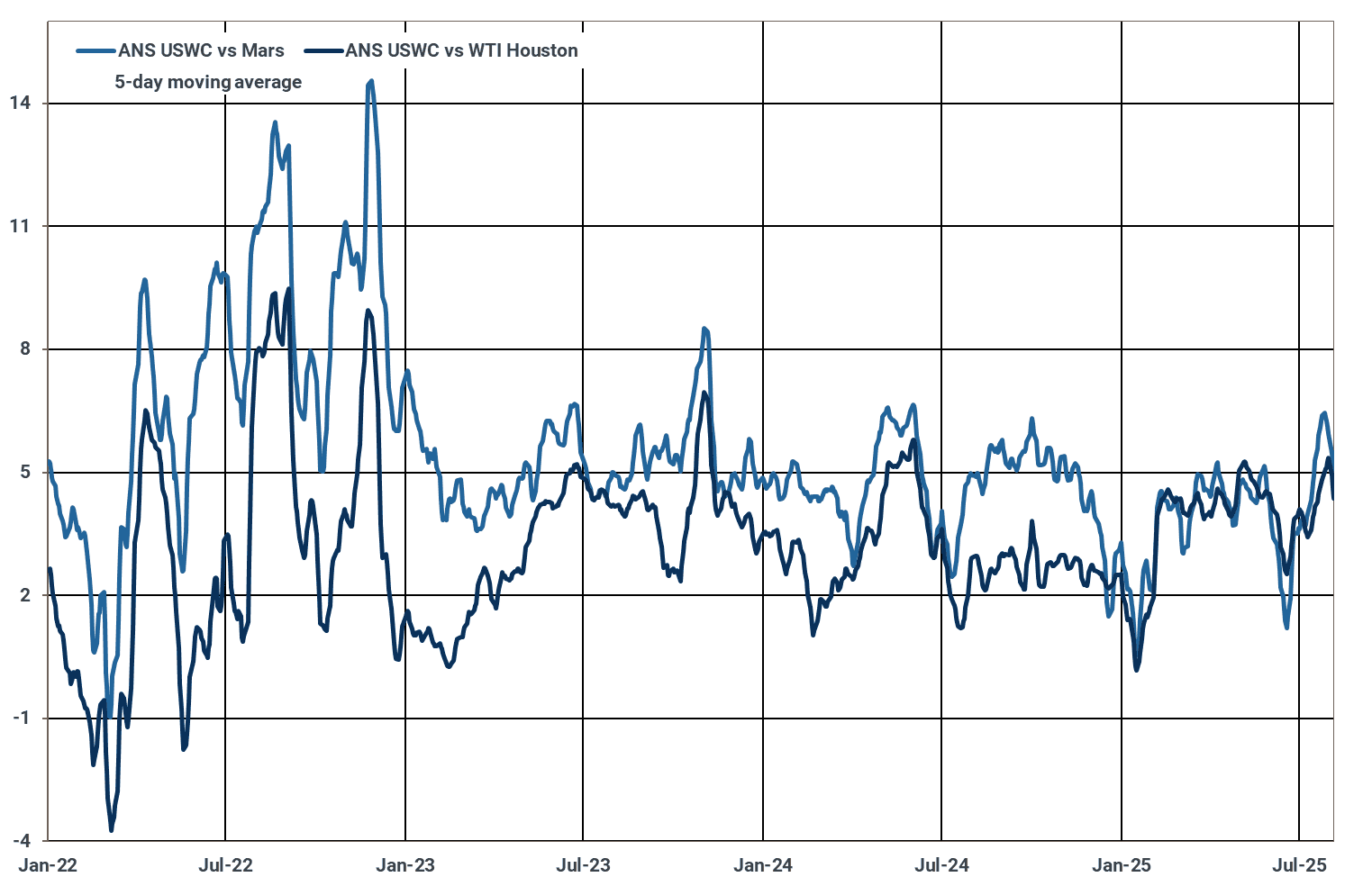

End of Alaskan field and pipeline maintenance to weigh on ANS differentials

While Alaska North Slope (ANS) differentials have been holding steady recently, with a cargo for October delivery to the US West Coast exchanging hands at a premium of around $3/bbl versus Brent (Argus Media), downward pressure is mounting. This pressure stems from a supply rebound in Alaska as well as an expected seasonal dip in US West Coast crude demand over Q4.

While maintenance work on the Trans-Alaska Pipeline (TAPS) has temporarily constrained ANS flows, forcing operators such as US independent Hilcorp to reduce output from Prudhoe Bay—the single-largest source of ANS, supply has been rebounding from the multi-year lows (hit lowest since 2026) seen in mid-July. Lower supplies from Alaska have partly helped draw down US West Coast crude inventories to a four-month low of just over 46 Mbbls in late July.

As supply normalizes through August and September, it will collide with seasonally weaker Q4 demand on the US West Coast. Values are also being pressured by a softening in European demand for crudes from Brazil and Guyana, which may increase their availability on the West Coast (flows via this route hit 230 kbd in July, a 14-month high).

ANS crude differentials, $/bbl

Source: Argus Media

This week’s Americas-related Market Pulse Reports:

- Transatlantic Freight Surge Widens WTI-Brent, Reshaping Arbitrage

- Record supply from Brazil and US lengthen global balances

Atlantic Basin: Local heavy sours pressured by Saudi OSPs

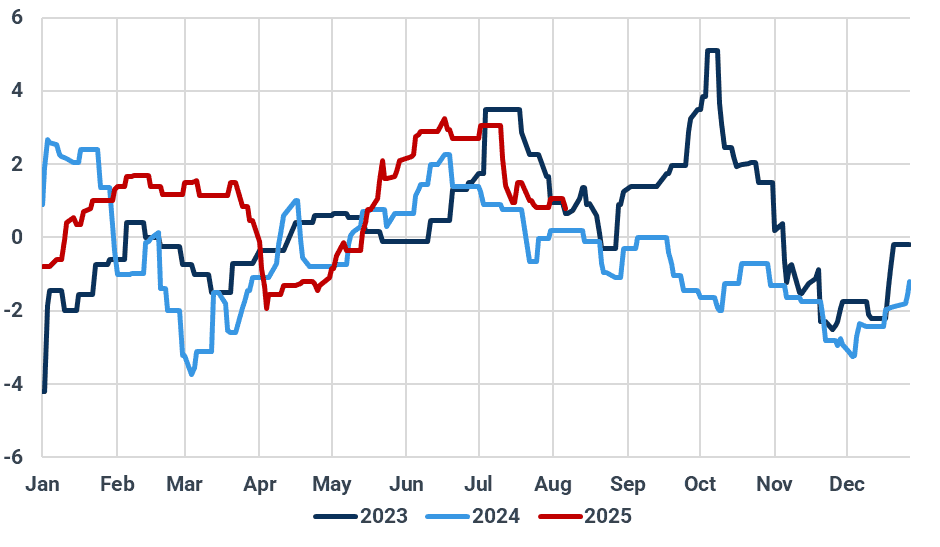

Johan Sverdrup pressured by OSPs and easing product tightness

Differentials for Norway’s Johan Sverdrup crude have continued their sharp decline, falling to a two-month low this week under pressure from multiple bearish factors.

The medium sour grade’s value has now fallen by over $2.20/bbl since early July, according to Argus Media. A key headwind has been the steeply backwardated Brent market structure, which heavily penalizes any delay in selling prompt-loading barrels and forces sellers to aggressively discount offers.

Furthermore, a major pillar of support for the grade has been removed. During Q2, a global tightness in residual fuel oil, which is needed by refiners to maximize clean product output, boosted demand for high-yield grades like Johan Sverdrup.

With this tightness now resolved, the grade has lost a key selling point. The most direct blow, however, has come from the Middle East.

This week, Saudi Aramco cut its official formula prices for all September-loading crude exports to Europe by a sharp $1.30/bbl. This move significantly increases competition for Johan Sverdrup in its core Northwest European market.

With all these headwinds, the grade will likely need to price even lower to maintain its competitive edge against newly discounted Saudi barrels, especially as the region heads into the autumn maintenance season.

Johan Sverdrup fob Mongstad differential to Dated Brent, $/bbl

Source: Argus Media

North Sea physical wobbles with tariff talk

Dated Brent prices edged lower on the week, settling below $70/bbl after a drop of over $3/bbl, according to Argus Media. The underlying weakness was most evident in the forward structure, with the balance-month August Dated-to-Frontline (DFL) contract dropping to its lowest level in nearly three months on August 5.

The DFL, a key barometer of prompt physical market health, reached around $1.25/bbl (Argus Media), a bearish signal indicating softening refiner appetite for spot barrels.

This has been linked to fresh uncertainty after the US imposed new tariff threats on India related to its continued purchasing of Russian crude, muddying sentiment for physical flows.

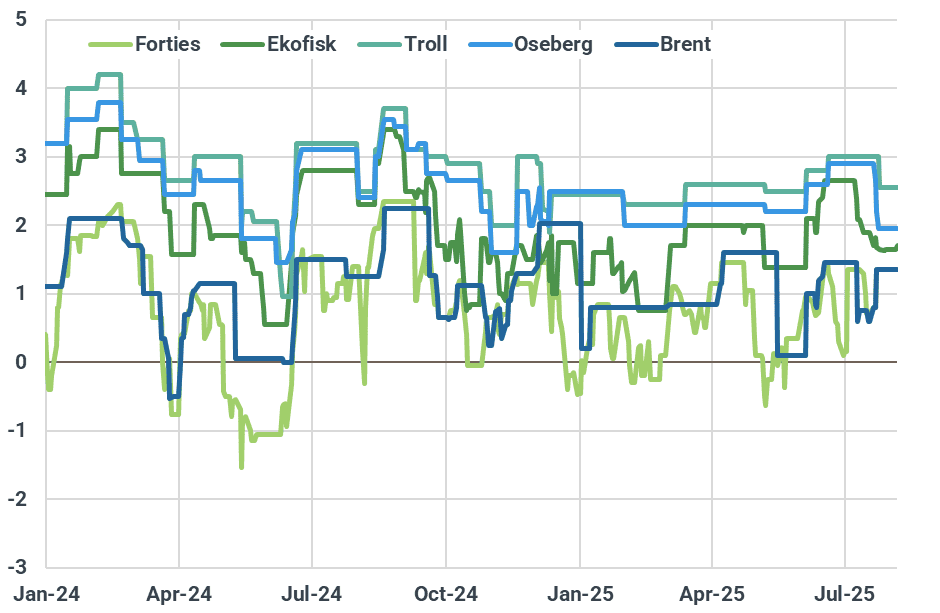

Looking ahead, the market is bracing for the planned three-week maintenance at the Buzzard field in mid-August. The shutdown will reduce August loadings of Forties to just four cargoes. Crucially, the absence of Buzzard’s heavier, sourer crude will make the remaining Forties blend lighter and more akin to WTI. This quality shift could paradoxically cap demand for other light sweets like WTI or Ekofisk as direct substitutes, as refiners specifically seeking a heavier component will have to look elsewhere.

BFOET crude differentials. $/bbl

Source: Argus Media

Crude diversification at Nigeria’s Dangote refinery intensifies

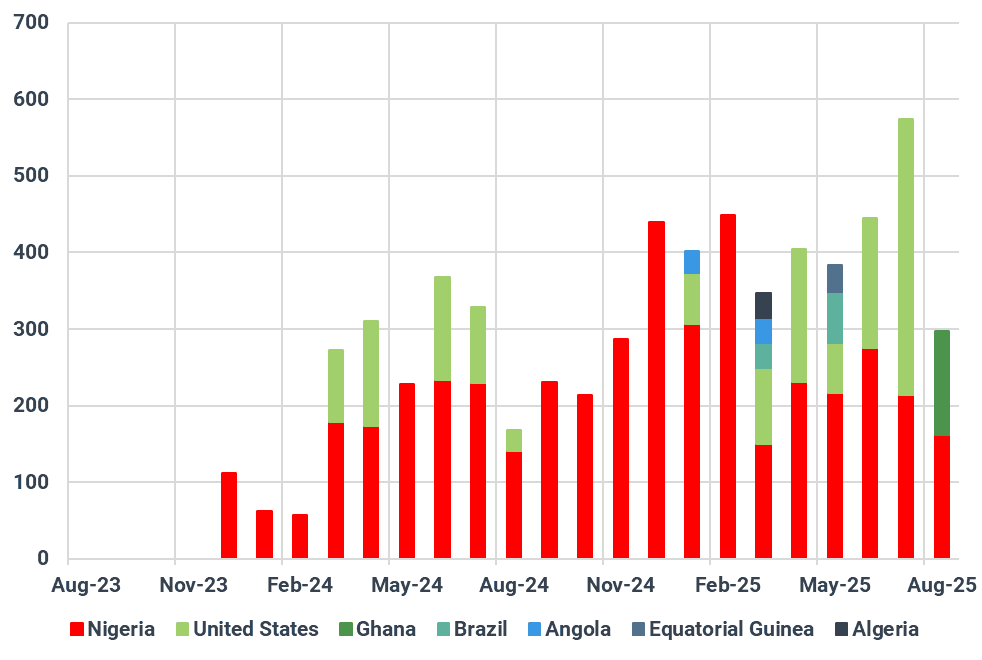

As shown on the Kpler platform, crude deliveries to the Dangote refinery surged to a record-high monthly volume of 570 kbd in July. Approximately 60% of these arrivals consisted of light sweet crude from the US, while the remaining 40% was made up of Nigerian grades. This marks the first time that US crude has overtaken Nigerian supply in Dangote’s import mix, a shift driven by ongoing challenges in securing domestic barrels and the cost competitiveness of WTI. In early August, a notable milestone was reached with the arrival of a 900 kb Suezmax carrying Sankofa crude from Ghana—the first time Dangote has imported Ghanaian crude. Sankofa, a medium sweet crude, is heavier than the typical light sweet slate processed at the refinery. It is comparable to other medium sweet grades that have been received to date, such as Brazilian Mero and Tupi, and Angolan Pazflor. This diversification highlights Dangote’s flexibility to process lower API grades. Looking ahead, Dangote is expected to continue sourcing from a mix of West African and US grades, supplemented by domestic barrels including Amenam, Bonny Light, and Escravos. Crude inflows suggest the refinery is running at elevated levels. Based on observed inventory builds and market intelligence, we estimate that current operations are around 445 kbd, representing 68% of total capacity, up from 400 kbd (60%) in Q1. Throughput is expected to remain near these levels over the coming months, with a dip to around 400 kbd anticipated during December–January maintenance. If no major technical issues arise, runs could climb to 600 kbd by the end of next year. At these higher throughput levels, the refinery is projected to produce up to 280 kbd of gasoline, up significantly from the current 150 kbd. This ramp-up is expected to place substantial downward pressure on Nigerian gasoline imports, which already dropped to record lows in June, forcing European refiners to seek alternative buyers.

Dangote refinery crude imports, kbd

Source: Kpler

This week’s Atlantic Basin-related Market Pulse Reports:

- US crude overtakes Nigerian barrels in Dangote's import mix

- Quality issue in Azeri BTC stream resolved, favouring price rebound

Middle East and Asia: Non-Russian crude chase lifts Dubai market, OSPs

Indian SOEs rush to secure non-Russian crude amid Trump tariff threat

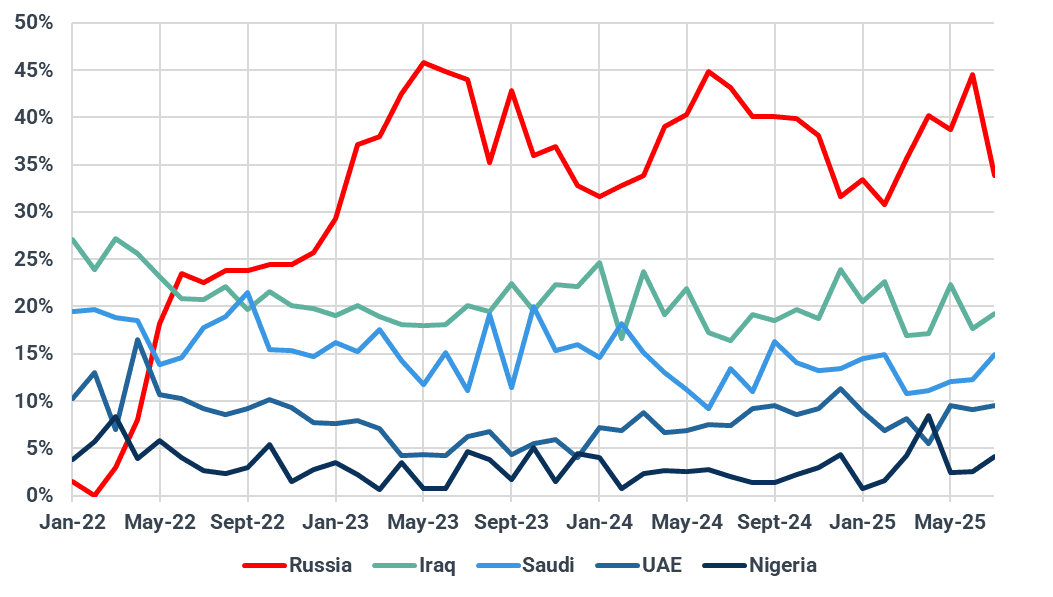

Trump’s order to hike US tariffs on India by additional 25% over its Russian oil purchases has thrown the Indian oil market into disarray, prompting refiners to issue more tenders for September-October delivery non-Russian barrels in a bid to hedge against potential supply disruptions. IOC snapped up a hefty 4.5 mb of US WTI crude in a recent tender, bundled with 0.5 mb of Canada’s WCS and 2 mb of Abu Dhabi’s Das, according to media reports. Other state-run refiners, including BPCL and HPCL, also picked up a handful of September-arrival Murban cargoes and are actively scouting for additional Middle Eastern and US barrels. These procurements underscore Indian refiners’ urgency to lock in prompt barrels, as they typically begin seeking mid- to late-October delivery cargoes in late July or early August.

At the same time, the Indian government dismissed the US threat, saying it has not instructed refiners to halt purchases of Russian oil. India’s imports of Russian crude slumped 25% m/m in July to a five-month low of 1.57 mbd, driven largely by reduced procurement from state-run refiners. As a result, Russia’s share in India’s total seaborne crude imports dropped to 34% last month from 45% in June, while volumes from the Middle East—particularly Saudi Arabia and Iraq—and the US saw an uptick. Nonetheless, at least 45 mb of Russian crude is still en route to India. Among the inbound cargoes is the Aframax tanker Guanyin, carrying Urals to Sikka, which was added to the US sanctions list on July 30. It remains unclear whether the cargo, currently anchored off Port Said, will be redirected to other buyers or transferred via STS to a non-sanctioned vessel before reaching India.

Share of key suppliers in India’s total crude/co imports, %

Source: Kpler

China has limited capacity to soak up the Russian crude glut

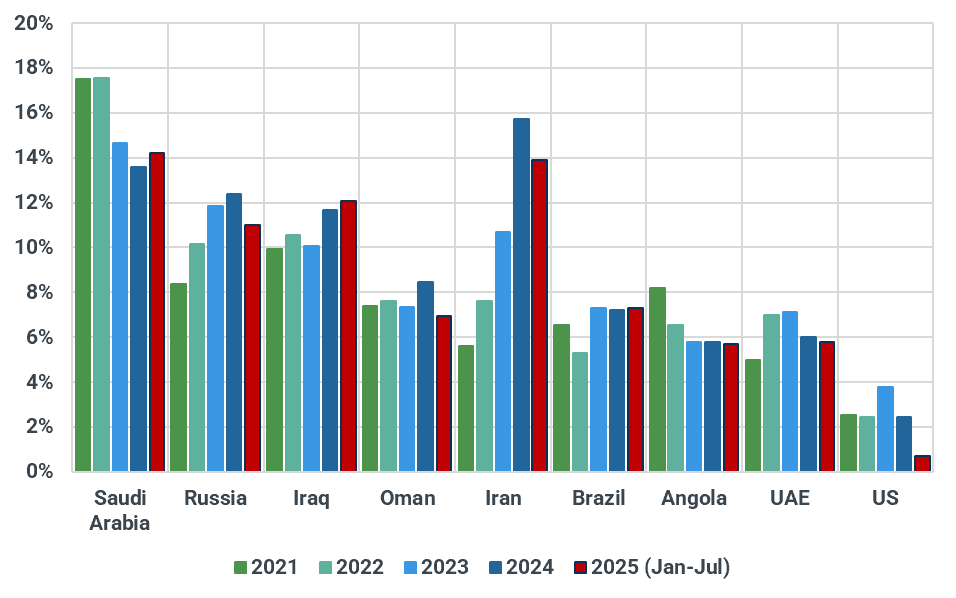

While Indian refiners have scaled back purchases of Russian crude, Chinese buyers have seen a growing wave of September-loading offers in recent days, amid a perceived oversupply of Russian barrels in the market. Several market participants told Kpler that more Urals cargoes are being offered in China at slightly softer levels, though buying interest remains muted. Although Trump’s salvo appears primarily aimed at India amid ongoing tariff negotiations, Chinese state-owned refiners—whose exposure to US sanctions is greater and compliance obligations stricter than those of their private peers—are also holding their breath, awaiting clarity on the future of Russian oil purchases. Currently, China only takes one to two cargoes of Urals each month, mostly supplied to state refiners.

If Trump moves forward with punitive tariffs or even sanctions targeting buyers of Russian oil, Chinese state-owned refiners are expected to pause procurement, mirroring the cautious stance already taken by their Indian counterparts. They briefly stepped away from Russian barrels in March in response to tighter US sanctions. That said, unless Beijing issues a directive for all firms to halt purchases—which remains highly unlikely given its consistent dismissal of unilateral US sanctions—China’s independent refiners may become one of the few remaining outlets for Russian crude. However, under current feedstock structure, refinery run rates, and crude import quota constraints, Chinese teapots have only limited appetite to absorb additional barrels—even in the event of a Russian price collapse. We estimate the potential maximum intake from independents in Shandong, Liaoning, and Hebei at around 300–400 kbd, which would also require them to replace all non-Iranian feedstocks with Russian crude.

Meanwhile, Iranian crude prices have continued to soften in China, with Iran Light now assessed at around -$4/bbl versus ICE Brent on a delivered basis—down from roughly -$3.3/bbl a month ago—as Chinese teapots see little incentive to place new orders amid high inventories and tight import quotas. Market participants told Kpler that teapots have used up their crude import quotas at a faster pace in the first seven months of this year compared to the same period in 2024.

Shares of key suppliers in China's seaborne crude oil imports, %

Source: Kpler

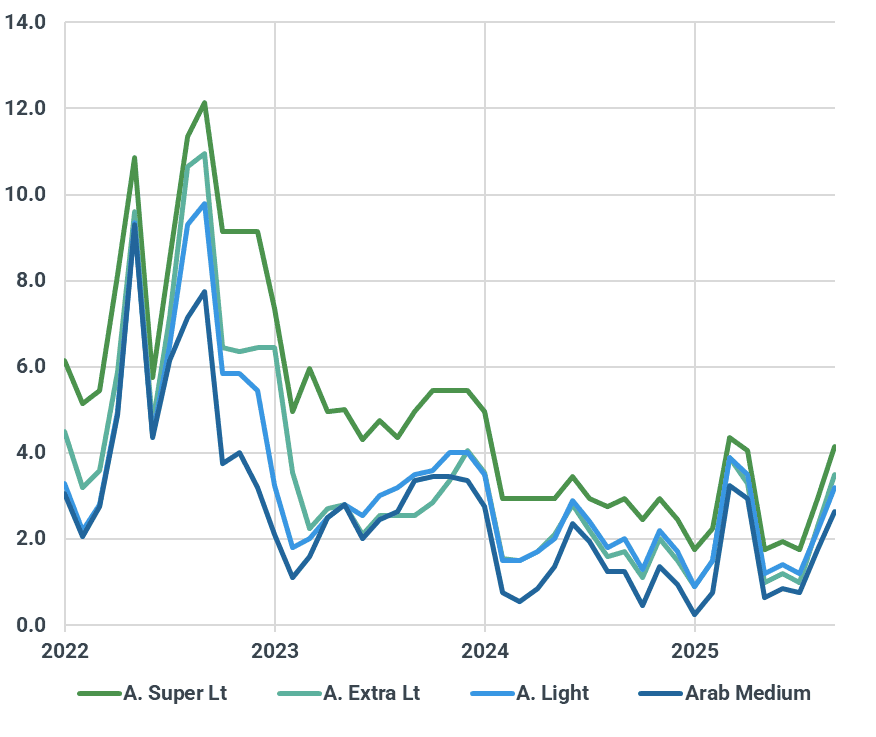

Saudi lifts Sept OSPs to ride the non-Russian barrel chase

Saudi Aramco has raised the OSP for its flagship Arab Light crude in Asia by $1/bbl for September-loading cargoes, setting it at $3.2/bbl above the Oman/Dubai average. The hike follows a $1.1/bbl widening in the Dubai M1-M3 spread in July and sits at the upper end of market expectations. While firm middle distillate cracks offer some support, the price hike reflects Aramco’s confidence in demand as Asian refiners—particularly in India, and to a lesser extent China—actively seek medium sour alternatives to Russian crude amid Trump’s vow to penalize buyers of Russian oil. That said, Saudi barrels are now pricing above other Middle Eastern grades such as Upper Zakum and Oman in the spot market, likely prompting some Chinese refiners to moderately trim their term liftings as ample supply follows the acceleration in OPEC+ production. Indian refiners, by contrast, may be inclined to take on additional Saudi barrels to cover prompt demand, as refinery run rates are also expected to ramp up with the end of the monsoon season.

The state oil giant raised the OSP for Arab Extra Light by $1.2/bbl to $3.5/bbl above the Oman/Dubai average, the highest in six months, signalling Saudi Aramco’s intent to capitalize on a tightening light sour market in Asia, as ADNOC is set to cut Murban exports and prioritize supply to its Ruwais refinery. As mentioned earlier, Indian state refiners have been ramping up purchases of Middle Eastern light grades such as Murban and Das, while buying interest from countries like Japan and Thailand also remains firm. However, a narrowing Brent-Dubai EFS has improved the economics of arbitrage cargoes for Asian refiners, prompting buyers in South Korea and Brunei to secure at least 3 mb of October-delivery CPC Blend. This renewed interest in Atlantic Basin barrels may cap gains for light crude grades in the region.

Meanwhile, the price hike for heavier grades such as Arab Heavy was more modest at $0.7/bbl, widening the light-heavy differential to $1.9/bbl, up from the $1.5–$1.7/bbl range seen in recent months. This suggests Saudi Arabia will ramp up exports of heavy crude as domestic crude burn demand tapers off with the end of the summer season.

Saudi OSPs to Asian clients (vs Oman/Dubai average), $/bbl

Source: Saudi Aramco

This week’s Middle East and Asia-related Market Pulse Reports:

Trump targets Russian resolution by ratcheting up tariffs on India

OPEC+ Raises Oil Production, Ends First Tranche of Voluntary Cuts

Urals discount into India widens as demand drops

India Faces Strategic Crossroads Amid EU Sanctions and U.S. Tariff Threats

See why the most successful traders and shipping experts use Kpler

Get research & analysis driven by proprietary data