European natural gas outlook 2026

Market & Trading Calls

Call to action: New S&D breakdown of European LNG import forecast

As part of its continual modelling efforts for S&D, Kpler Insight has unveiled a new breakdown of its European LNG forecast, with data now available for Northwest Europe, Southern Europe and Rest of EU-27 (UK and Turkey remain separate).

Kpler Insight is now also breaking down domestic consumption by sector for the above regions at a country level.

Market & trading calls for 2025 and 2026

European TTF price outlook: Stable as the 2025 forecast was slightly lowered by $0.05/MMBtu to $12.06/MMBtu due to lower November prices and above-average temperatures expected in December. However, our price call for 2026 prices is ▼bearish m/m, after lowering it by $0.31/MMBtu to $9.81, due to the expectation that Atlantic supply will remain plentiful, a downward revision to Northeast Asia demand, and domestic European demand is forecast to remain weak. Increasing expectations of a potential peace deal between Russia and Ukraine also contributed to the bearishness.

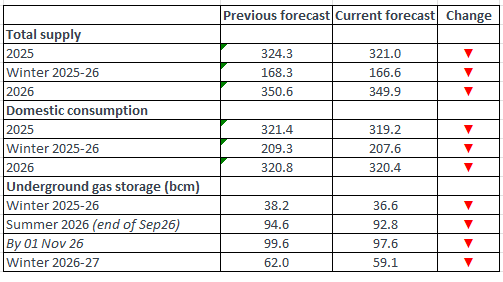

EU-27 natural gas balance (bcm)

Source: Kpler Insight

EU-27 gas supply forecasts

Domestic gas production forecast

EU-27 domestic gas production rose m/m, reaching approximately 3.2 bcm in October 2025, (+3% y/y), mainly caused by a rise in Dutch output.

Kpler Insight expects domestic production in 2025 to reach 38.4 bcm (+4% y/y) and 38 bcm in 2026 (-1% y/y), broadly unchanged from our previous forecast. Q1 2027 is set to reach 9.9 bcm, marking a 1.8% increase q/q, as the Neptune Deep field in Romania is expected to start ramping up in 2027. While the exact start date is yet to be confirmed, first gas is tabled for early 2027.

Shell has stated it is ready to substantially increase its investment in Italy if the government unlocks long-delayed drilling permits. The company currently invests about €500 million annually in the country, and has stated that with new permits it could double production at the Val d’Agri field and also increase output at the under-utilized Tempa Rossa site. Last year, Shell managed approximately 16% of Italy’s domestic natural gas output.

Gas production in selected EU-27 countries (bcm)

Source: Eurostat, Kpler Insight

Kpler Insight is incorporating biomethane production data for France, Denmark, Austria, Spain and Germany in its gas production data and forecast.

_____________________________________________________________________________________

Pipeline gas import forecast

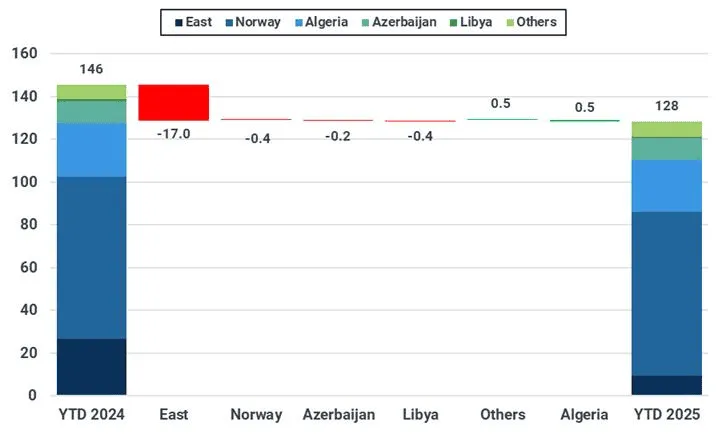

EU-27 net pipeline imports declined to 11.4 bcm in November 2025, down 2% m/m and 12% below last year. The monthly drop was due to weaker net imports from Algeria (-4% m/m), Azerbaijan (-6% m/m), Norway (-1% m/m), and the East corridor (-15% m/m). The declines more than offset increases in net UK flows to the EU for the month (+41% m/m).

Lower flows from Algeria and Azerbaijan were likely due to maintenance works planned by SNAM, which restricts available capacity at the Mazara del Vallo, Gela, and Melendugno IPs for one month, between 11 November – 11 December.

The slight drop in Norwegian flows occurred primarily on the back of the cold snaps that strengthened the NBP-TTF spread during the second half of the month. That said, mild weather conditions during the first two weeks of November favored flows UK flows to Belgium via the interconnector.

Regarding the East corridor, exports to Moldova increased m/m in line with our expectations as the winter season continues to unfold in the region. Pipeline exports to Ukraine also edged higher, notably as some limited flows went through Romania via one of the Isaccea IPs, likely as part of Route 1 bookings.

YTD (January–November) EU-27 net pipeline imports reached 128 bcm, 12% lower y/y. Aside from the loss through the East corridor, declines in Norwegian, Azeri, and Libyan volumes have also contributed to the drop, outweighing incremental gains in flows from the UK and Algeria (see chart).

January-November net pipeline flows to the EU-27 y/y change, by supplier (bcm)

Source: Kpler Insight. “Others” include net aggregates from the UK, Switzerland, Serbia, and other minor flows. Exports to Ukraine and Russian supply are included in the East category.

Looking ahead, as the year comes to a close, Kpler Insight projects a 12% y/y decline in net pipeline flows to 140 bcm in 2025. Despite the net loss of volumes, the European pipeline system has been remarkably resilient throughout the year, particularly in adapting to the loss of Russian pipeline gas supply via Ukraine that led to a significant reconfiguration of flows, especially across the CEE region.

For 2026, Kpler Insight expects net pipeline imports to increase slightly to 142 bcm. Higher supply is anticipated from the expansion of the Trans Adriatic Pipeline (TAP) starting in January 2026, which will lift Azeri exports to the EU by roughly 1 bcm y/y. We also expect to see marginal increases in flows from Norway, the UK, and stable imports coming from North Africa.

These gains are expected to be partly offset by lower flows through the TurkStream pipeline, as the EU plan to phase-out Russian gas leads to reduced utilisation. Ongoing negotiations around a potential peace deal between Russian and Ukraine seem to be slowly progressing. In our view, even if a deal is achieved, we believe the phase out of Russian gas will remain in place as this will be in the interest of US LNG exports. As for Ukraine, the country will try to avoid becoming a transit route for Russian gas in the near future.

_____________________________________________________________________________________

LNG import forecast

Europe

For this report’s LNG forecast, Kpler Insight continues to employ a hybrid forecasting method that combines a new bottom-up modelling approach for European gas consumption. This approach uses sets of linear and machine-learning-based regression models to estimate sectoral and total gas consumption in each country within the EU-27 region. We are also adding granularity and are now estimating LNG imports into Northwest Europe, Southern Europe, and the rest of EU-27*. You can find our latest breakdown in the S&D excel file here.

European LNG imports (EU-27 + UK + Turkey) strongly rose to 11.9 mt in November, up from 10.6 mt in October – the highest level recorded this year. This was on the back of significantly higher volumes into Turkey (and to a lesser extent, the UK), as LNG was increasingly used to balance the Turkish domestic grid. We forecast total European LNG imports to end at 127 mt in 2025, up 25 mt (25%) y/y, solidifying the role LNG plays in replacing the Russian pipeline gas lost on 1 January and serving as a key element for refilling UGS facilities. In 2026, we expect higher LNG availability, mainly from the US, to boost Europe’s LNG imports, which we forecast will reach 145 mt for the year, an increase of 18 million tons (19%) over 2025.

Northwest Europe

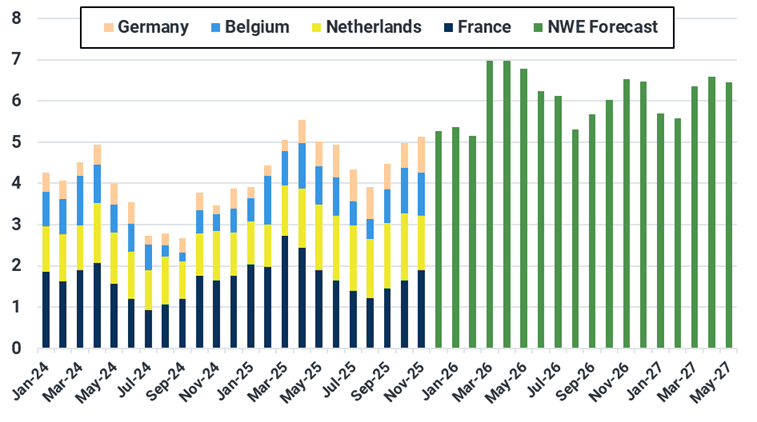

NWE November imports came in at 5.14 mt, 0.3 mt lower than initially expected. For the year 2025, imports are set to reach 57.1 mt (+28% y/y), as we forecast December volumes to remain high to meet seasonal end-of-year gas demand. For 2026, we see total LNG imports in the region reaching 73.6 mt (+29% y/y), in order to replenish storage during the injection season and support exports to the CEE region. Additional regasification capacity set to come online throughout the year in Germany, Belgium, and the Netherlands will help accommodate these extra volumes, while domestic consumption across NWE is also set to increase by 1.7% on average y/y. However, the commissioning date of Germany’s 3.7 mtpa Stade FSRU terminal remains a downside risk to this forecast, having recently been delayed again to Q2 2026.

Northwest Europe imports, 18m forecast (mt)

Source: Kpler Insight. This includes GER, FRA, NLD, BEL.

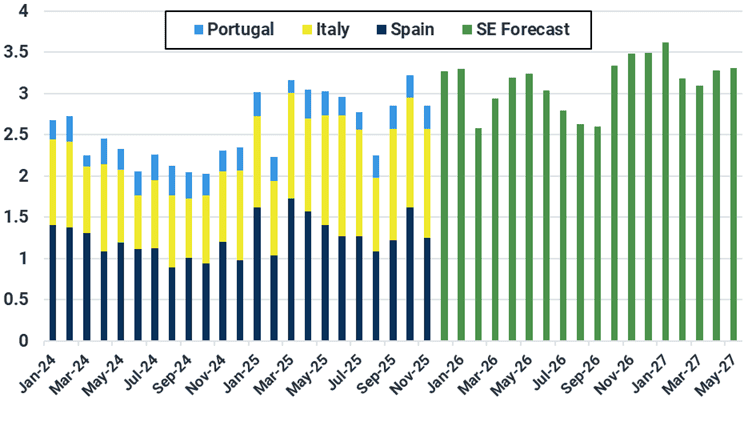

Southern Europe

November LNG imports into Southern Europe reached 2.85 mt, 0.4 mt lower than expected after a 2.5-year record high in October. For 2025, total LNG imports are set to end at 27.6 mt (+25% y/y), driven by increased domestic gas demand in Spain and Portugal following April’s power blackout, and Italy’s expanded regasification capacity aimed at replacing curtailed Russian pipeline supply.

In 2026, LNG imports are forecast to be 34.6 mt (+6% y/y). The growth will be driven by slightly higher gas consumption in the Iberian Peninsula y/y, particularly in Spain (1.8% up y/y), and stable regional pipeline supply. Regarding regasification capacity, only Italy is set to see a 1 mtpa expansion at Rovigo in January. Furthermore, the 2.8 mtpa Toscana terminal is scheduled to remain offline for the whole month of October due to planned maintenance, thus limiting Italy’s import capacity.

Southern Europe imports, 18m forecast (mt)

Source: Kpler Insight. This includes ESP, ITA, POR

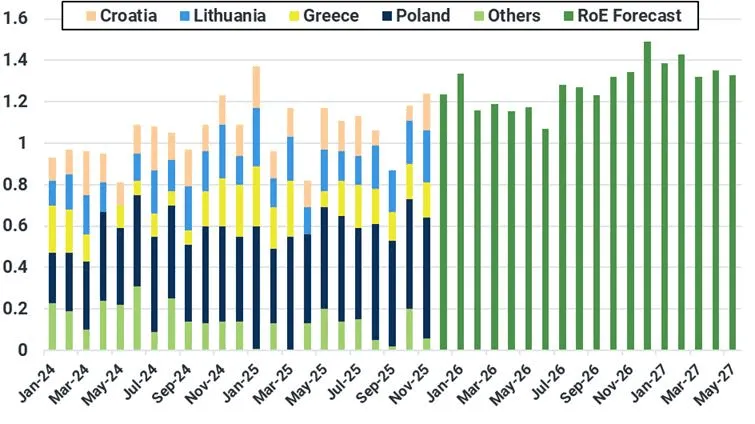

Rest of EU-27, UK and Turkey

Imports into the rest of the EU (RoE) reached 1.24 mt, spurred by higher imports into Croatia while Finnish volumes fell to just one cargo last month. 2025 imports are set to reach 13.4 mt (+10% y/y). For 2026, this is forecasted to increase by 12% to 15 mt, as higher regasification capacity in Croatia (recent 3mtpa expansion at the Krk terminal) alongside expected increases in pipeline capacity (Greece-Bulgaria and Croatia) will facilitate additional LNG imports. Some of these volumes may also serve Southeast Europe and the Ukrainian market.

Rest of EU-27 imports, 18m forecast (mt)

Source: Kpler Insight. This includes POL, GRE, LTU, HVR, FIN, MLT, SWE.

LNG imports into the UK and Turkey rose sharply in November, reaching 2.65 mt, mainly driven by Turkey (+0.91 mt m/m). Going forwards, Kpler Insight forecasts Turkish and UK LNG imports to increase during their seasonal demand period (typically Q1 and Q4 of each year), reaching 21.5 mt (+28% y/y) for this year and 19.5 mt for 2026. This will again be mainly driven by Turkey, who has signed multiple long-term supply agreements in recent weeks in its effort to become a regional gas hub and serve its own increased domestic demand.

Storage and LNG infrastructure developments

Poland’s Swinoujscie terminal has completed its first commercial loading of LNG onto a bunkering vessel following an expansion that added a second jetty and a third storage tank, increasing regasification capacity to 8.3 bcm/yr and enabling service for small and medium vessels. The terminal is also certified to handle bioLNG and biomethane for use as marine fuel.

Germany’s Stade terminal has been delayed to Q1 2027 after DET and HEH resolved a long-running dispute over the terminal’s incomplete superstructure. A new agreement signed on 14 November transfers responsibility for finishing the work to DET, allowing inspections and construction to restart. However, the Energos Force FSRU was reportedly being sub-chartered elsewhere — suggesting that the unit might not be available in time for the previously expected start-up.

The Höegh Gannet FSRU returned to Brunsbüttel on 24 November after completing two months of technical upgrades at the Fayard shipyard in Denmark. Upgrades included installing catalytic converters to meet German emissions rules and rotating the funnel outlets to reduce noise for nearby residents. DET also used the vessel’s absence to advance work on the new Jetty West and perform maintenance on existing port facilities.

The Toscana terminal completed its first auctions for small-scale LNG services, becoming the first Italian facility to offer loading for small carriers. All twelve 7.5k cbm slots for November 2025–November 2026 were fully allocated, reflecting strong market interest. The service enables LNG delivery to ships or coastal storage sites and follows the terminal’s commissioning of small-scale capabilities after the Mediterranean’s designation as a sulphur emission control area.

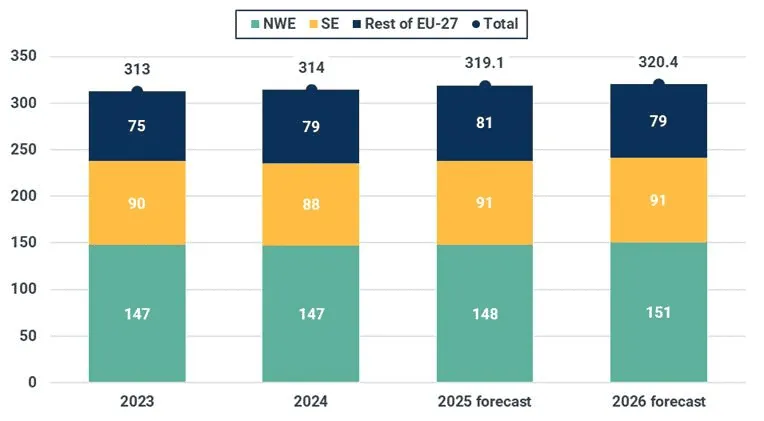

EU-27 gas demand forecast

EU-27 gas demand is estimated to have risen to 32.6 bcm in November, up 23.5% m/m but 6.3% lower y/y. The monthly increase aligns with typical seasonal patterns as winter demand ramps up. However, the year-on-year decline was driven primarily by weaker industrial consumption, particularly in Germany, and lower gas-for-power demand. Although a strong cold spell in the second half of the month temporarily lifted distribution demand, it was insufficient to offset milder temperatures earlier in the month and higher wind generation compared to last year, both of which reduced the call on gas in the power sector.

Looking ahead, Kpler Insight forecasts EU-27 gas consumption to reach 319.1 bcm in 2025, up 1.5% y/y but 2.3 bcm (-0.7%) below our previous outlook. The downward revision reflects expectations of higher-than-normal temperatures across much of the continent, particularly in the first half of December, when anomalies of 2–4°C above seasonal norms are possible depending on the region. On the power side, slightly below-average wind generation in Germany, offset by near-normal output across the rest of Northwest Europe, provides only limited upside for gas-fired generation. Lower gas prices may encourage some recovery in industrial demand, though the effect remains modest, as distribution and power demand continue to be the main drivers during the winter months. For 2026, we keep our consumption outlook broadly unchanged. EU-27 demand is now projected at 320.4 bcm, up 0.4% y/y and only 0.4 bcm lower than our previous forecast.

EU-27 annual gas consumption and forecast by region (bcm)

Source: Kpler Insight

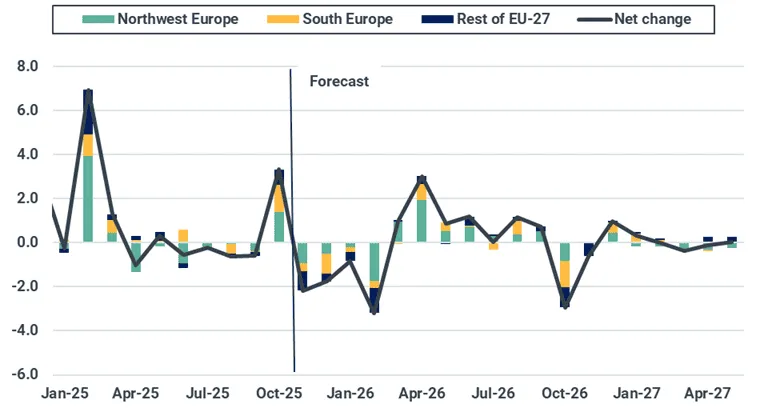

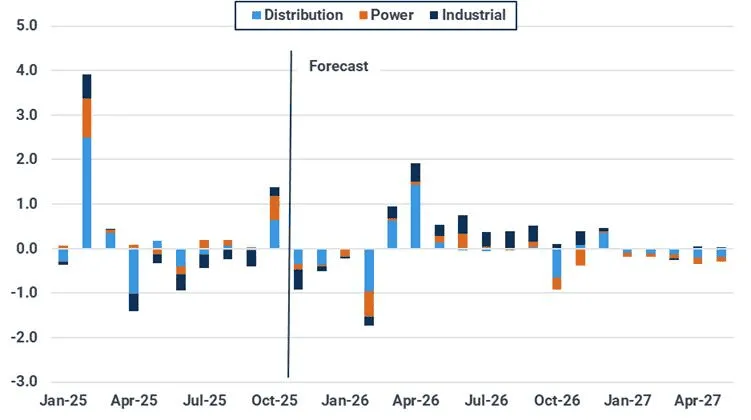

EU-27 y/y historical and forecast change in annual gas consumption by region (bcm)

Source: Kpler Insight

Northwest Europe

Looking at the regional breakdown, total gas consumption in Northwest Europe is estimated to have reached 16 bcm in November, up 4.3 bcm m/m but 0.9 bcm lower y/y. Milder temperatures in the first half of the month more than offset the impact of the late-November cold spell, which lifted distribution demand but not enough to reverse the annual decline. For 2025, Kpler Insight forecasts Northwest European demand to edge up to 147.7 bcm, an increase of 0.9 bcm (+0.6% y/y). The modest rise is driven by higher distribution and gas-for-power demand in February and October, when unseasonably cold conditions and episodes of low wind generation increased the call on heating and gas-fired generation.

In 2026, demand is expected to rise further to 150.6 bcm (+2% y/y), largely on the back of stronger industrial consumption. We forecast industrial demand to increase by 4.7% to around 59.8 bcm, supported by lower TTF prices (see price section), which should incentivise gas use in price sensitive markets like the Netherlands and Germany. These gains, together with marginal increases in distribution demand, outweigh continued declines in the power sector as expanding wind and solar capacity further displace gas-fired generation.

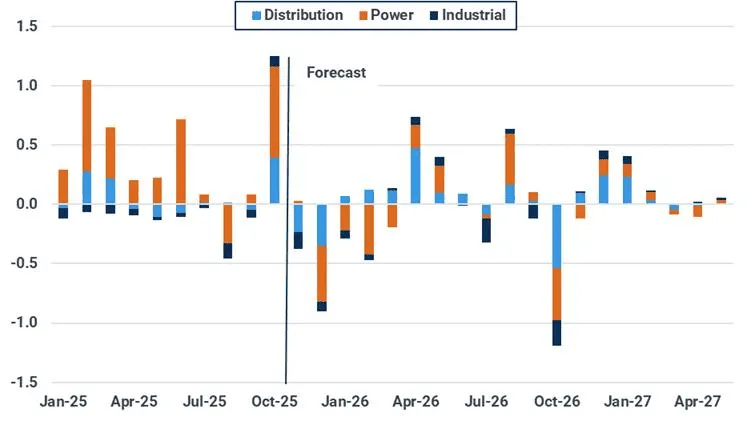

Northwest Europe y/y changes in sectoral gas consumption, historical and 18m forecast (bcm)

Source: Kpler Insight. Northwest Europe includes BE, LU, NL, FR and DE.

South Europe

In Southern Europe, total gas consumption is estimated to have reached 8.5 bcm in November, up 0.8 bcm m/m but 0.3 bcm lower y/y. The decline was driven by softer distribution and industrial demand, mirroring the dynamics observed in Northwest Europe, where milder early-month temperatures and weaker industrial activity offset gains later in the month. Looking ahead, we forecast Southern European demand to rise to 90.5 bcm in 2025, an increase of 2.1 bcm (+2.4%) y/y. The growth is led by a 10% y/y increase in gas-for-power demand (+2.8 bcm), reaching an estimated 30.5 bcm. The largest contribution comes from Spain (+1.9 bcm y/y), where gas-for-power demand strengthened markedly following the large-scale blackout event in April.

For 2026, total demand in Southern Europe is expected to remain broadly stable at 90.7 bcm (+0.2% y/y). We project gas-for-power demand to edge down by 1.2% y/y to 30.2 bcm, reflecting lower winter demand as temperatures normalise toward the five-year average and the impact of the Spanish blackout becomes fully absorbed into the region’s power mix. Industrial consumption is also forecast to decline slightly by 1.3% to 27.1 bcm, as lower TTF prices are not fully transmitted into the Italian PSV market due to the hub’s premium, limiting the demand response relative to Northwest Europe. These reductions are largely offset by a 2.7% increase in distribution demand.

Southern Europe y/y changes in sectoral gas consumption, historical and 18m forecast (bcm)

Source: Kpler Insight. Southern Europe includes IT, ES, and PT.

EU-27 underground gas storage forecast

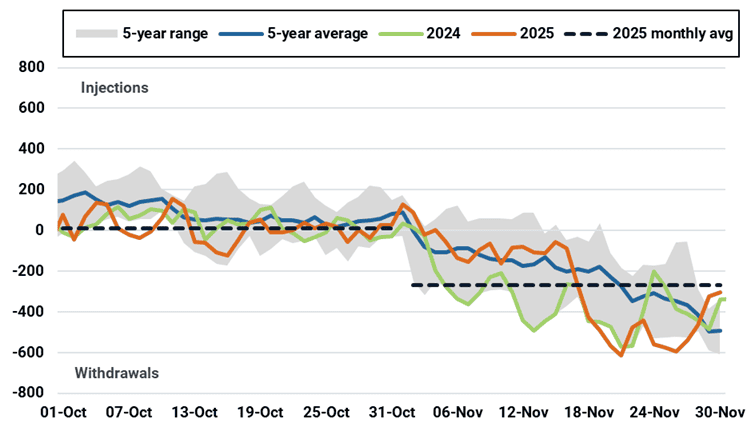

The EU-27 ended November 2025 with underground storage levels at 76.8 bcm, or 75.4% full. This is around 10 percentage points lower y/y. Withdrawals in November averaged -255 mcm/d. This pace is 45 mcm/d below the five-year average but remains significantly lower than the -333 mcm/d withdrawal rate recorded in November 2024. Withdrawals were muted through the first half of the month, as stable pipeline and LNG supply largely met demand. However, rates accelerated sharply in the second half of November when a cold spell lifted both heating needs and gas-for-power demand across the bloc.

EU-27 daily storage injections/withdrawals since October (mcm/d)

Source: AGSI+, Kpler Insight

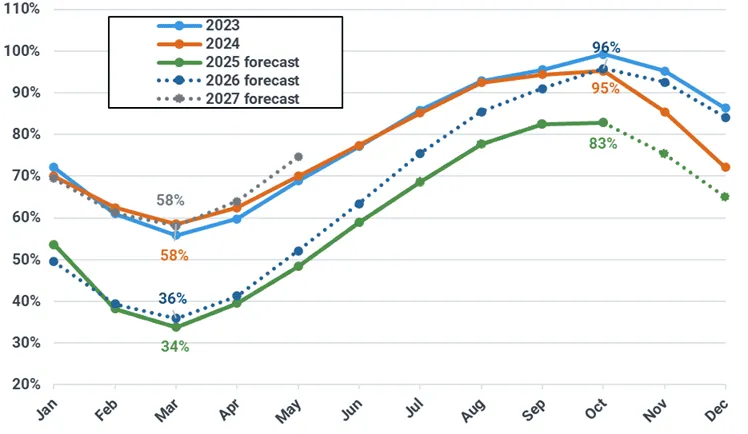

Kpler Insight expects EU-27 storage levels to end the 2025–26 winter at 36% full, 1.5 percentage points below our previous estimate of 37.5%. The downward revision primarily reflects reduced expectations for LNG imports in December 2025 and January 2026, notably in Northwest Europe, alongside slightly lower net pipeline inflows, both of which increase the call on storage. However, with ample LNG supply forecast to reach the EU over summer 2026, supported by expanded export capacity in the Atlantic basin and lower TTF prices y/y, EU-27 stocks are projected to reach 96% by 1 November 2026 and to exit the 2026–27 winter at around 58% full.

EU-27 underground gas storage levels (%)

Source: AGSI+, Kpler Insight

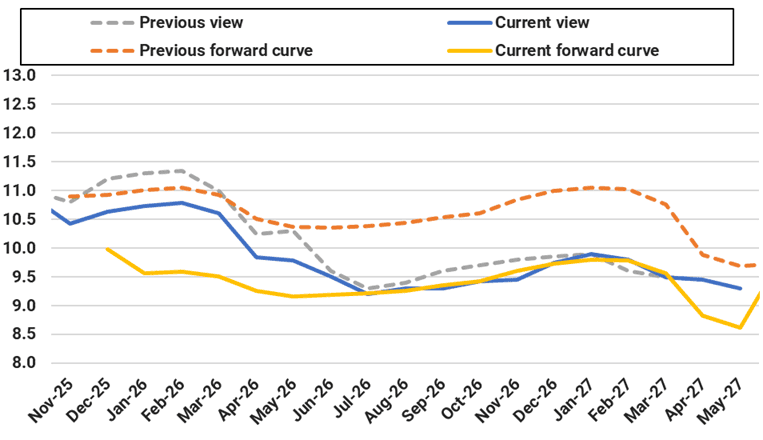

European TTF price forecast

European TTF front-month averaged $10.43/MMBtu in November – a $0.45/MMBtu decline from the $10.88/MMBtu average in October. Prices mostly fell throughout the month, as warmer than expected temperatures coupled with plentiful LNG and pipeline supply contributed to the bearish pressure. Rising freight rates and increased competition with Turkey added some bullish pressure towards the middle of the month, however optimism on peace discussions to end the war in Ukraine capped these gains.

Kpler Insight has slightly lowered its 2025 European TTF forecast by $0.05 to $12.06/MMBtu ($1.15/MMBtu higher y/y). This reflects a lower-than-expected November price due to abundant supply and perceived progress in negotiations toward a potential peace deal between Ukraine and Russia. Additionally, above-seasonal temperatures expected for December are likely to keep gains in check for the month. We have also reduced our average price forecast for 2026 by $0.31/MMBtu to $9.81/MMBtu, reflecting weaker demand in Northeast Asia next year, which will lead to less competition for increasing LNG supply in the Atlantic Basin. Additionally, sluggish gas demand in the EU, whose economy is expected to grow only modestly in 2026, will help keep prices in check. We expect the decline in prices to result in a stronger injection season compared to summer 2025, with UGS storage levels projected to reach 96% capacity by 1 November 2026.

Average monthly European TTF price with forecast ($/MMBtu) vs. previous monthly report

Source: Kpler Insight

Excel dataset

Premium subscribers to Kpler Insight’s Natural gas package receive access to an Excel dataset detailing 18-month ahead forecasts on US and European supply-demand balances and price forecasts. You can request access to the latest natural gas monthly balances Excel dataset here.

See why the most successful traders and shipping experts use Kpler

Kpler Insight: Get the analysis that matters