Middle East war disrupts dry bulk commodity trade as Hormuz shipping grinds to a halt

The war in the Middle East is disrupting shipping patterns and raising risks across multiple dry bulk supply chains. Pellet supply in the region is at risk as vessels avoid the Gulf, while steel imports may decline. In energy markets, LNG disruptions and tighter gas inventories could lift European coal demand, while petcoke flows through Hormuz face supply risks. Grain markets remain broadly stable but fertiliser trade through the Strait of Hormuz is increasingly vulnerable. Freight markets have seen higher bunker costs and war risk premiums.

Iron Ore & Steel: Middle East conflict threatens pellet trade and regional steel demand

- The Iran-US/Israel war is set to disrupt iron ore pellet supply in the Middle East and weaken regional steel consumption. Iran and Bahrain together accounted for roughly 18% of global seaborne pellet exports in 2025, and shipments from both producers are now at risk. On the steel side, Iran’s exports as well as imports into other Middle East Gulf countries face disruption, potentially weighing on construction and industrial activity across the region. China is also indirectly affected, as its pellet imports from the Middle East and its steel exports to the region will both decline.

- Shipping data already suggest a slowdown in raw material flows into the Gulf. Since the outbreak of hostilities on 28 February, no bulk carriers loaded with iron ore have been observed entering the Gulf to supply pellet plants and direct reduced iron (DRI) facilities. Several vessels previously bound for Gulf ports, including Cape Shangrila, HT Huang Shan, and William Oldendorff, appear to have diverted away from the region.

- Iron ore prices have so far shown limited reaction to the conflict and traded within a narrow range over most of the past week. Market sentiment improved after Beijing pledged on 5 March to stabilise the country’s struggling property sector, which lifted futures prices. The most traded DCE contract, May 2026, rose 1.40% w/w to 759 yuan/t on 5 March, while the SGX April 2026 contract gained 1.91% to $100.25/t at the time of writing.

- Global seaborne iron ore supply remains strong. Exports reached a year-to-date high of 34.30Mt in the week ending 1 March, well above the five-year average of 31.50Mt. In Guinea, two bulk carriers departed the port of Morébaya within the same week for the first time, likely reflecting improved rail capacity following the deployment of four additional locomotives since the third week of February.

- On the demand side, Chinese seaborne iron ore imports fell to 22.40Mt last week, the lowest level since April 2025. This was largely due to weather-related shipment disruptions from Australia and Brazil earlier in February. Nonetheless, with port inventories still at multi-year highs and steel production soft compared to the year-ago level, the Chinese iron ore market continues to be oversupplied.

Daily DCE and SGX iron ore prices ($/t)

Source: DCE, SGX MarketView, Kpler Insight

Coal: Hormuz Strait risk poses systemic threat to coal and petcoke markets

- The Qatar Ras Laffan LNG terminal’s force majeure has the potential to cause waves of disruption in the energy complex. The steep increase in gas prices opens up the possibility of coal-to-gas switching economics in Europe for the first time since 2022. Generation margins for European coal units have not yet turned positive, as power prices have not risen proportionally, but the bullish case is increasingly inventory-driven: EU gas stocks sit below seasonal norms and Atlantic LNG supply is tightening as Asian buyers compete for flexible cargoes.

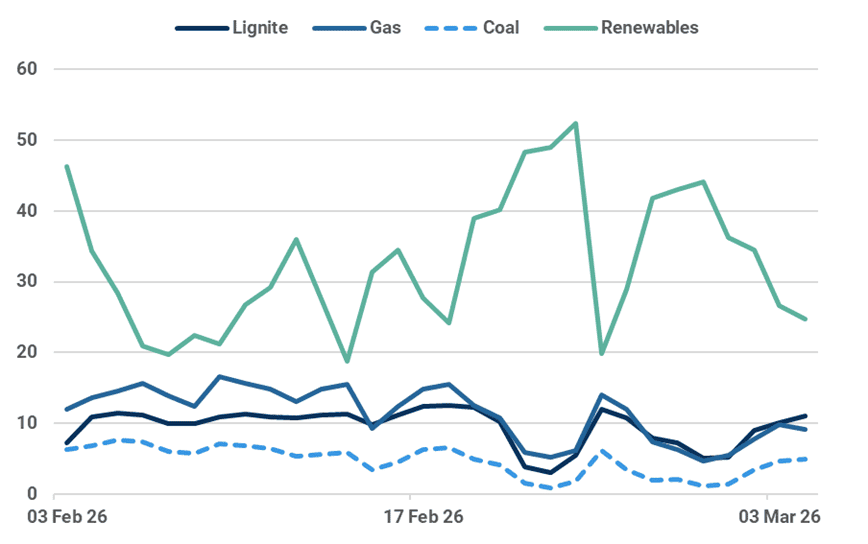

Germany renewable vs thermal generation (GW)

Source: Kpler

- In an aggressive switching scenario, European seaborne coal demand could rise by around 8 Mt y/y, approaching 30 Mt and reversing prior forecasts of a decline to the low 20s Mt. Germany and the Netherlands retain the most meaningful coal stacks, though Germany's upside is capped near-term by the Datteln 4 maintenance outage until 16 March. Gas burn uplift from coal switching will likely only materialise materially in the 2026-27 winter renewable output through summer will increase.

- Strait of Hormuz petcoke flows face separate disruption risk, with Saudi, UAE and Omani exports to India and China exposed. Indian cement producers, reliant on fuel-grade petcoke, face the sharpest supply risk and would be forced to source US petcoke at a premium or switch to coal.

- Australian premium hard coking coal prices fell sharply over the past week, with the PLV index dropping from by around $20/t w/w to the high $210s/t fob Australia. Escalating US-Iran tensions have pushed bunker fuel costs and are pushing freight rates higher, pressuring fob rates.

Grains & Oilseeds: Grain markets hold steady for now, despite raging conflict

- The blockade of the Strait of Hormuz cuts off access to the largest container ports in the region, threatening supplies of essential goods to the region.

- The volume of grain transported via the Strait of Hormuz is small compared to total trade. Corn through Hormuz accounts for less than 10% of global trade, while wheat and soybeans are less than 5%. However, for many Middle East Gulf countries, access is key in supporting domestic grain consumption. Over half of these shipments go to Iran. Iran’s wheat crop is near harvest and it could also import wheat and barley from Russia through the Caspian Sea, however, imports of corn, soybean and meals will suffer.

- For nitrogen and phosphorus, two of the three key nutrients for plant growth, around 25% and 10% of annual seaborne exports are transported via the Strait of Hormuz, respectively. Fertiliser prices have risen globally as a result. While growers may be covered for fertiliser in the short term, this could compromise yields for summer crops and 2027 harvests if access via the Strait of Hormuz remains constrained.

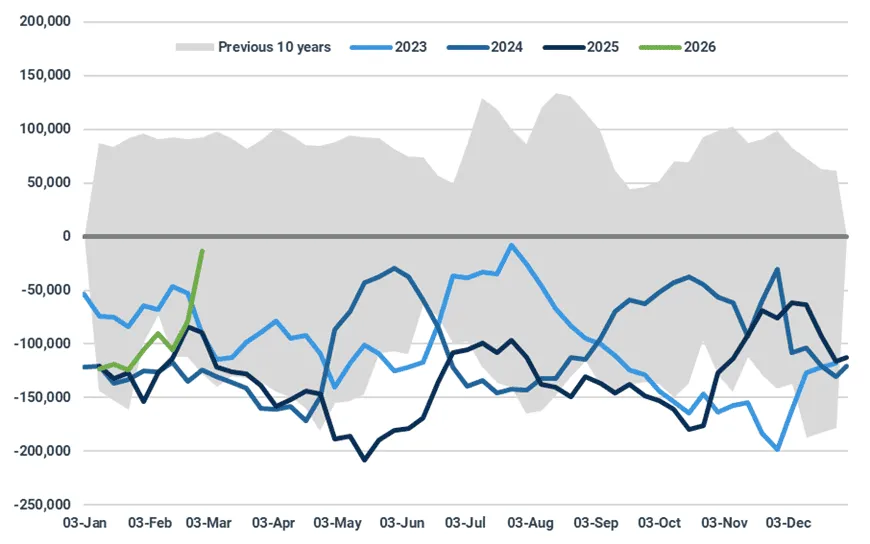

- Wheat markets rose last week as funds continued to close short positions. However, as more favourable weather conditions were forecast across western EU and the Great Plains, pressure on nearby CBOT wheat and MATIF milling wheat futures returned after both opened at multi-month highs on Monday.

Net position of funds for CBOT wheat (# contracts)

Source: Commodity Futures Trade Commission

- Novorossiysk, a major wheat-exporting Russian seaport, came under attack from Ukraine. It was reported that damage was caused to naval and oil facilities. Subsequently, Russia targeted a drone strike on a vessel transporting corn from the port of Chornomorsk. Odesa has also been subject to continued drone strikes from Russia, leading to power outages that limit the operational capacity for seaport terminals. Ukrainian corn exports were robust in February, however, the threat of further Russian attacks on vessels transiting through Ukraine’s maritime corridor could see shipments decline.

- Last week, the US EPA submitted its proposal for the 2026 and 2027 Renewable Fuel Standard renewable volume obligations. Not only are the proposed volumes for biomass-based diesel supportive, but the market viewed the progress towards the policy’s ruling as supportive too. The White House should take around 30 days to review the proposal and can ask for any revisions before the proposal will come into effect.

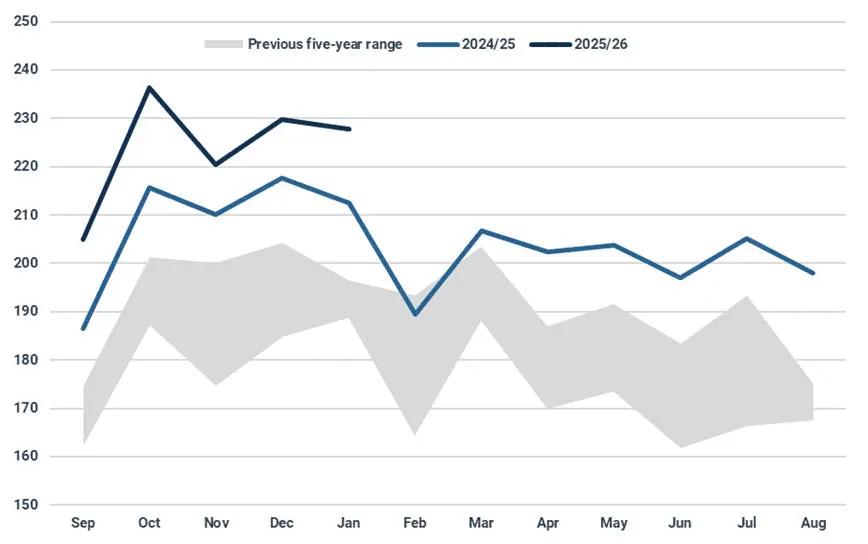

- US soybean crush continues to operate at a high utilisation rate, with January crush at 228 mbu. While 1% lower m/m, this was the largest soybean crush on record for the month of January. Board crush has remained firm despite the weakness seen in CBOT soybean meal as CBOT soybean oil reached new highs. As a result, front month CBOT soybean oilshare surpassed 50%, which has not been seen since August 2025.

US soybean crush (mbu)

Source: USDA

- By 28 Feb, Brazil’s soybean harvest was 42% complete, behind last year's pace of 48%. A short pause in rainfall last week had helped producers continue with the harvest, though heavier rains are forecast in the coming weeks. In Rio Grande Du Sol, recent rainfall has partially alleviated dryness concerns, though as the soybean crop is still yet to mature, additional rains are needed to prevent further productivity losses. Brazilian soybean exports lined up for March have already surpassed the 10 Mt mark with FOB offers continuing to show the US at a premium to Brazil.

Minor Bulks: War in the Gulf disrupts global aluminium supply chain

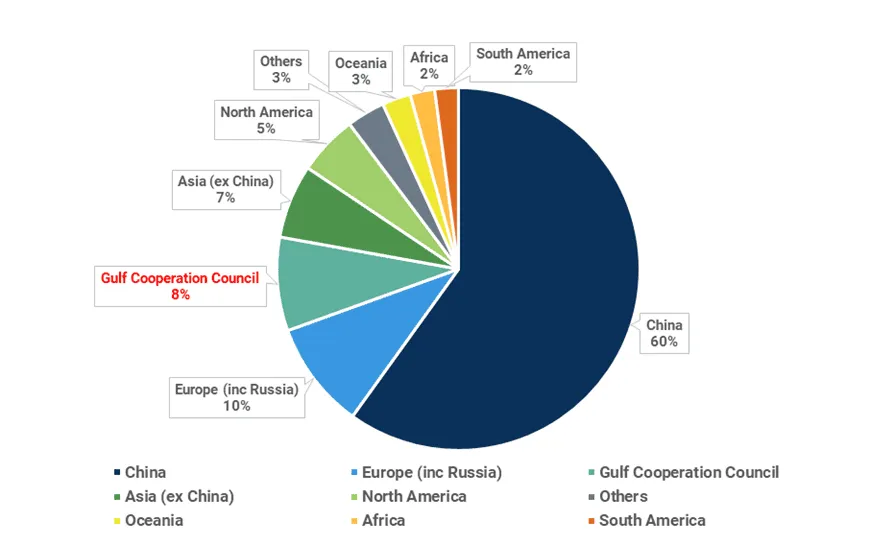

- The conflict involving Iran and the US/Israel is beginning to ripple through global aluminium markets, threatening nearly a tenth of worldwide production. Iran and the Gulf Cooperation Council countries together account for around 9% of global primary aluminium output, with Iran producing about 0.60Mt in 2025 and GCC producers 5.24Mt. Meanwhile, most of GCC countries’ aluminium production is exported to non-GCC countries and must transit the Strait of Hormuz, meaning that a prolonged disruption to the shipping corridor could significantly deepen the global supply deficit.

- The market has already reacted. The benchmark three-month aluminium contract on the London Metal Exchange rose 5.07% w/w to a record $3,335.50/t on 4 March, while regional premiums in both the United States and Europe also climbed to new highs.

- Operational strains are becoming increasingly visible. Qatar’s Qatalum and Bahrain’s Alba have both invoked force majeure in recent days. Qatalum, with a capacity of 0.636 Mtpa, began shutting down operations on 3 March after QatarEnergy halted gas supplies, and the smelter expects to cease production entirely by the end of the month. Alba, with a capacity of 1.623 Mtpa, said its declaration is directly related to the transit issues through the Strait of Hormuz. Both smelters rely heavily on imported alumina from outside the Gulf, making the conflict a risk not only for metal shipments but also for raw material supply.

- In Iran, around 80% of operating primary aluminium capacity is now at risk. The conflict has damaged the electricity infrastructure and curtailed access to alumina feedstock, of which the country produces only around 20% domestically. Although roughly two-thirds of Iranian aluminium output is consumed locally, potential export losses of around 0.20Mt would further tighten global supply.

The GCC countries accounted for over 8% in global primary aluminium production in 2025 (%)

Source: IAI, Kpler Insight

Dry Bulk Freight: War risk weighs, sub-Capesize earnings rally

- The outbreak of war in the Middle East prompted marine insurers to issue cancellation notices and revise terms of coverage. War risk premiums have surged, with numbers as high as 1.5% of hull value reported. Insurance coverage is available for ships in the MEG however, the very real risk of attack is discouraging vessels from transiting the Strait of Hormuz. At the time of writing, close to 280 dry bulk carriers (10k+ dwt) are positioned in the MEG, with a significant proportion stationary and taking shelter at anchorages and in ports.

- Transits through the Strait of Hormuz (in both directions) dropped from nineteen on 28 February to ten on 1 March and have since slowed almost to a halt, with a consequent buildup of vessels anchored at both ends of the waterway. Threats and actual attacks on merchant shipping by Iran prompted US offers to escort vessels through the Strait. However, we do not believe this to be a credible solution to the situation. The US does not have enough available military assets in position to implement this suggestion, and the pace of transits would still be well below peacetime.

- The Middle East Gulf accounts for 16-18% of global fertiliser exports, approximately 30Mtpa of seaborne grains/oilseed imports. Other major seaborne dry bulk trades include inbound bauxite and steel cargoes, and outbound iron ore pellet and aluminium shipments.

- Renewed threats to shipping from the Houthis, following the outbreak of the Iran-US/Israel war saw major container lines once again suspend voyages through the Red Sea. Dry bulk carrier trade through the waterway is also expected to fall. A return to Cape of Good Hope routes will boost ton miles and tighten vessel supply. We do not expect a normalisation of transit patterns through the Suez Canal in the medium term.

- The impact on dry bulk timecharter rates from the war in the Middle East was small. The benchmark indices have little to no coverage of the region in their constituent routes. However, the new Baltic Indian Ocean rates pushed higher. The S12 (Arabian Gulf-India) route jumped by $2,250/day w/w to the highest level since assessments began in December 2025 at $18,083/day on 4 March.

- By contrast, spot voyage rates jumped due to oil price-driven rises in the cost of bunkers. The price of VLSFO in Singapore is up by almost 30% w/w and demand for Singapore bunkering is set to climb due to disruption at Fujairah. The Capesize C14 (China-Brazil/West Africa round-voyage) timecharter rate rose by 2% w/w however, there was a 10% jump in the C3 (Tubarao-China) iron ore spot voyage rate. A similar bunker price-driven trend can be observed on fronthaul grain and Pacific iron ore routes.

- After slipping into reverse in recent days, the Capesize 5 TC average dropped by a net $907/day w/w to $26,765/day. There were net weekly increases in average Panamax, Supramax and Handysize earnings to $17,970/day, $17,600/day, and $14,748/day, respectively. However, sub Capesize markets have lost momentum in recent days and are likely to flatten or slip into reverse in the coming week.

- At 1.02, the average Panamax:Supramax earnings ratio dropped to the lowest since January on 5 March. The relative cheapness of Panamax compared to Supramax should favour the larger vessel for Indonesian coal chartering over the coming weeks.

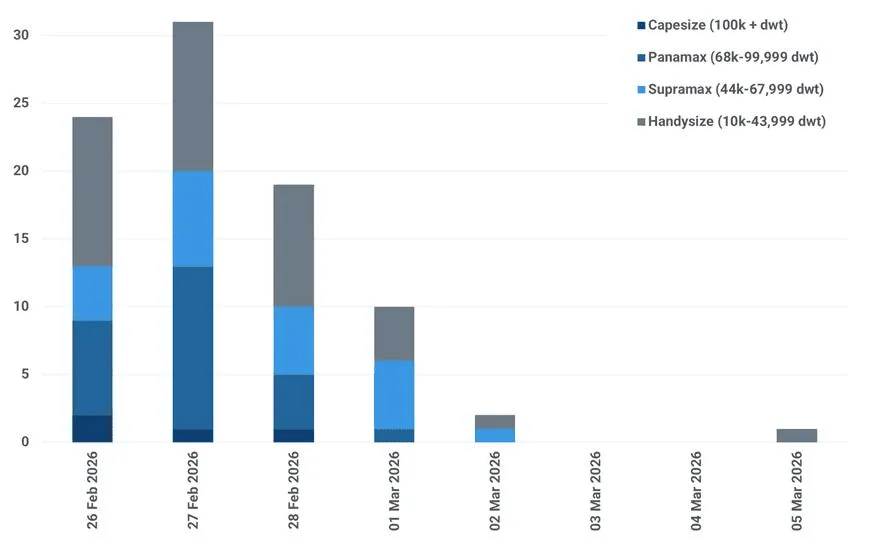

Dry bulk vessel transits SoH: no crossings occurred between 3 and 4 March (count)

Source: Marine Traffic

Key Dry Bulk Market Developments

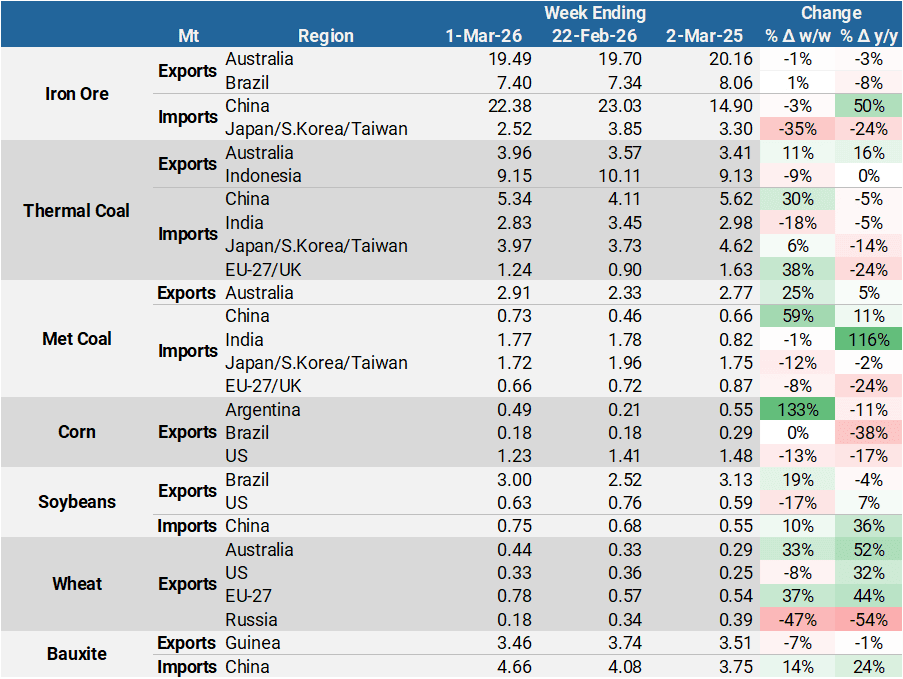

Dry Bulk Commodity Flows

Source: Kpler

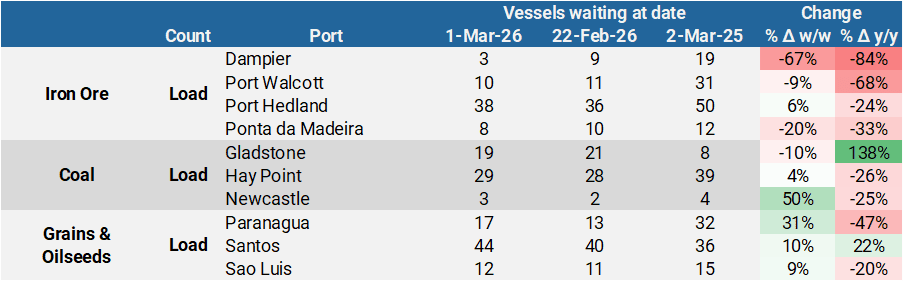

Dry Bulk Port Congestion

Source: Kpler

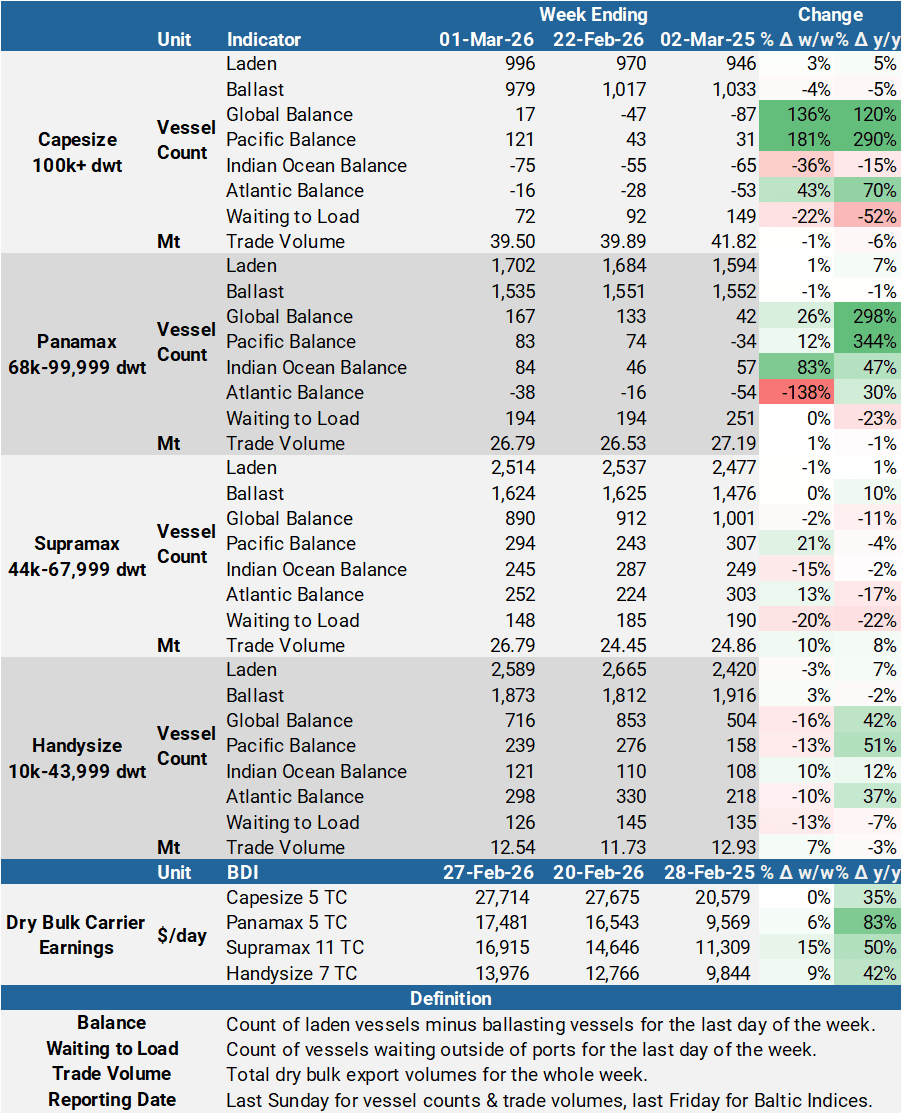

Dry Bulk Freight Metrics

Source: Kpler, Baltic Exchange

Market insights you can actually trust

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical dry bulk market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions. In times of conflict and geopolitical uncertainty, our real-time data keeps you ahead of supply disruptions and price volatility.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Get real-time market intelligence on how the Middle East conflict is reshaping dry bulk trade