Milder temperatures in Europe, high LNG inventories in China and steady LNG supply to weigh on global gas prices next week

Market & Trading Calls

European TTF price outlook: Bearish as lower-than-average forecasted temperatures across most of the continent and slightly increased pipeline imports are expected to extend loose fundamentals into next week. The ongoing EU-US trade negotiations pose a risk to this price call with the looming 1 August deadline for potential US tariff increase on EU goods.

Asian LNG Price Outlook: Bearish as robust Chinese LNG inventories, a mild weather outlook in South Korea, and steady Pacific supply week-on-week continue to outweigh modest demand gains, reinforcing downward pressure on prices.

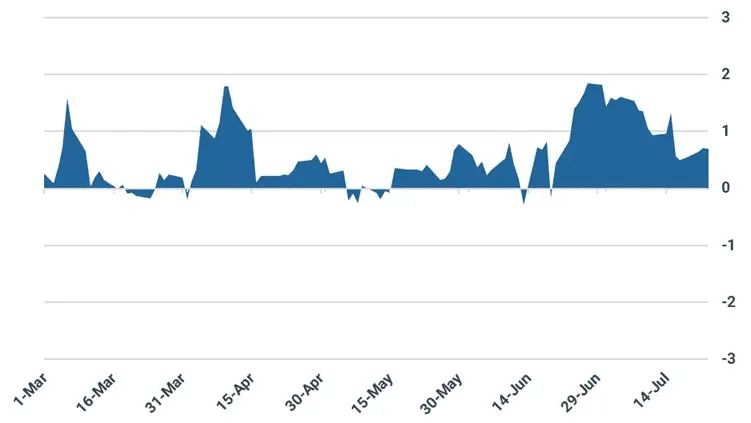

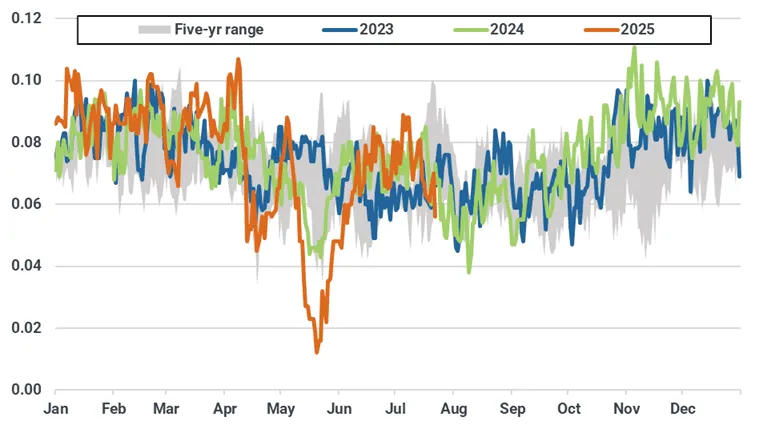

Asian LNG – TTF spread outlook: Stable as both indices are expected to fall in tandem. The spread widened to $0.7/MMBtu on 23 July from $0.57/MMBtu on 16 July.

US Henry Hub price outlook: Bearish as a cooler start to August and higher gas production put significant downward pressure on prices.

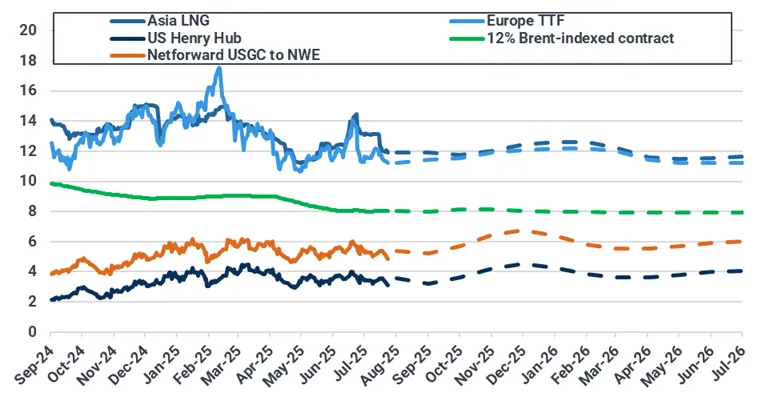

Key natural gas and LNG front-month prices ($/MMBtu)

Source: ICE, NYMEX, Spark Commodities. Brent-indexed price represents 12% slope of 90-day moving average of Brent contract. Netforward USGC to NWE calculation is 115% Henry Hub contract plus shipping and regasification costs into Gate (Spark Commodities).

Asian LNG-TTF front-month spread ($/MMBtu)

Source: ICE, Kpler Insight

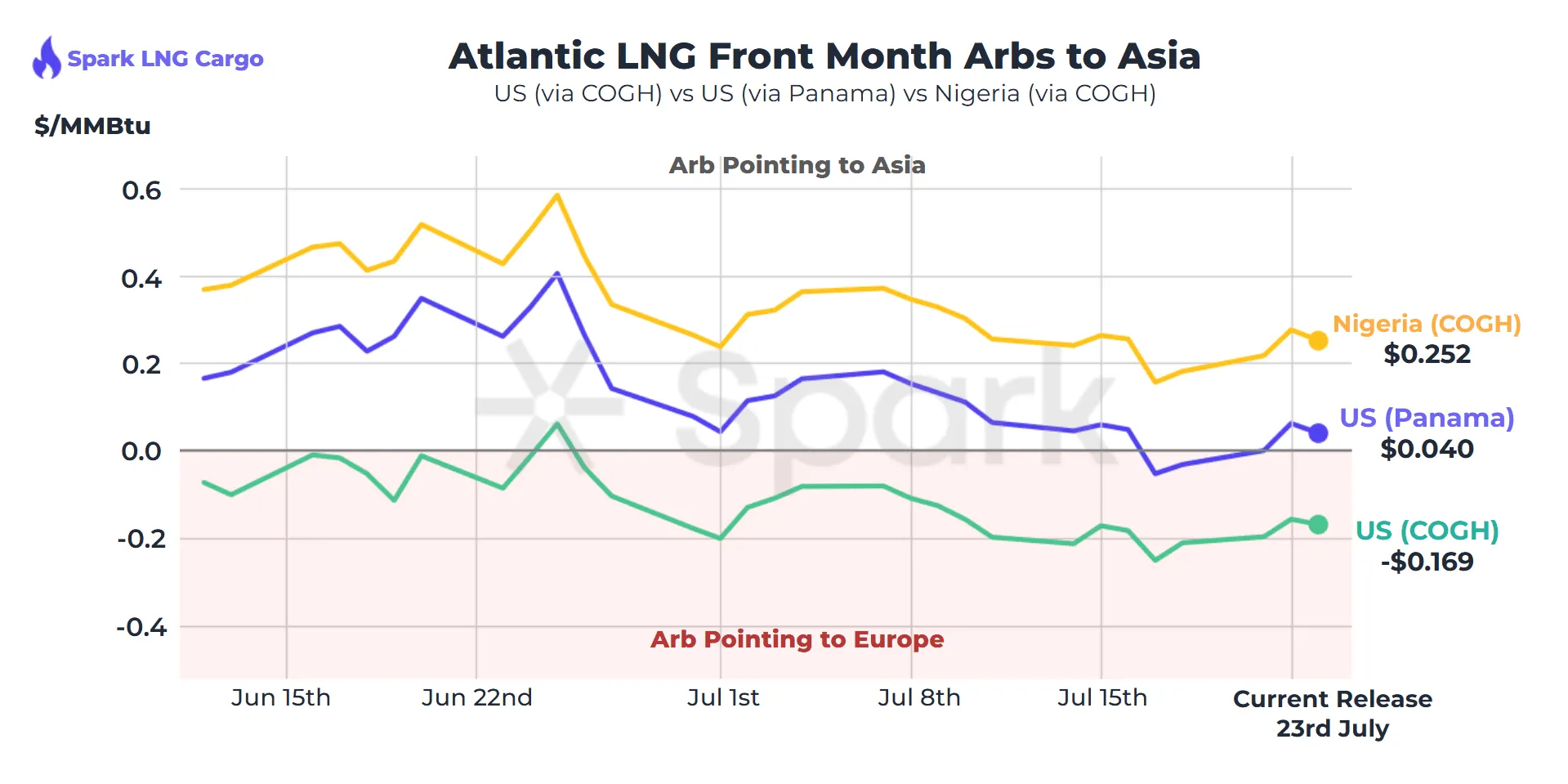

Atlantic basin LNG front-month arbs ($/MMBtu)

Source: Spark Commodities, incorporating ICE-listed Spark Freight and Spark Cargo products. For a full M+12 forward curve and netback cost breakdown, contact Spark at info@sparkcommodities.com.

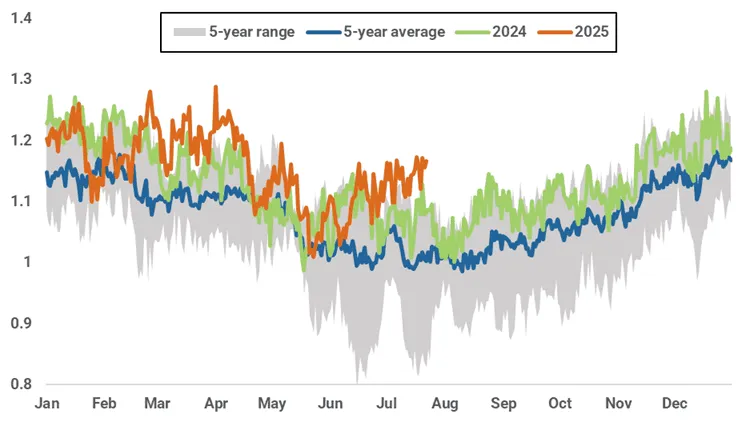

Europe: Lower temperatures and robust supply to prolong TTF’s bearish momentum

European TTF front-month prices declined w/w by $0.6/MMBtu (-5.1%) to $11.24/MMBtu from $11.84/MMBtu on 16 July. The gradual decrease was driven by higher LNG imports w/w and robust pipeline imports outweighing a slight increase in gas-fired generation at the EU level.

Looking ahead, Kpler Insight expects TTF front-month prices to fall due to lower-than-average forecasted temperatures across most of the continent and slightly increased pipeline imports. Moreover, the narrowing of the Asian LNG–TTF spread seen in recent days could allow Europe to increase imports in the coming days. A risk to this price call is posed by the ongoing EU-US trade negotiations as the 1 August deadline for a US tariff increase on EU goods approaches (despite cautious optimism as a similar deal was reached with Japan yesterday).

Diving into supply-side fundamentals, EU pipeline supply fell by 1.3% w/w to 3.48 bcm. The decrease was caused by brief outages at the Kollsnes and Nyhamna gas processing facilities and a compressor failure at the Troll field in Norway. Despite maintenance, Norwegian and UK flows to the EU remain higher than at this time last year, partly due to a widening NBP discount to the TTF. Similarly, TurkStream’s output is currently higher than in 2024, helping offset recent slight declines in Azeri flows to the EU. For next week, Kpler Insight expects a slight increase in pipeline gas supply as most maintenance works in Norway are expected to end on Friday.

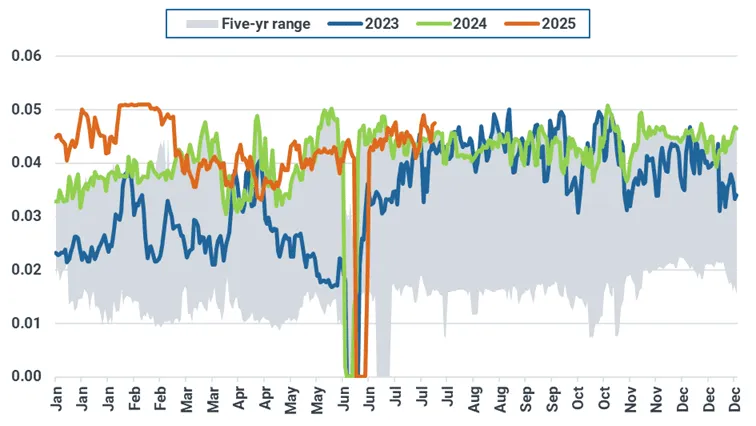

Turkstream’s daily pipeline flows to the EU (bcm)

Source: ENTSOG, Kpler Insight

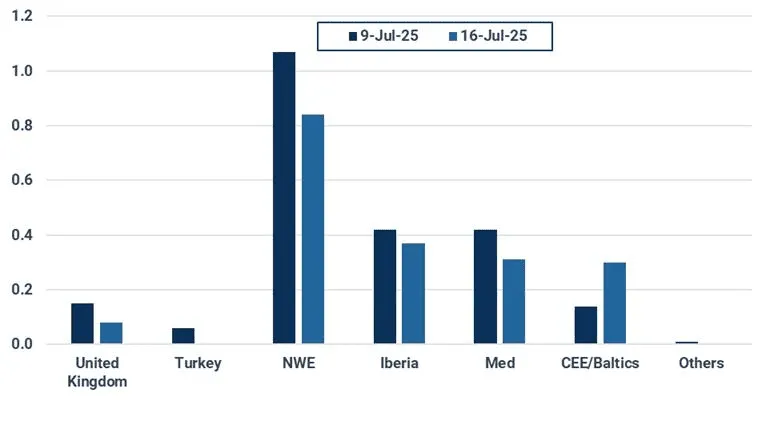

European LNG imports fell by 16% w/w to 1.9 bcm. The decrease was primarily driven by reduced Belgium’s weekly imports, the lowest recorded since January, outweighing significant gains in other parts of NWE and the Baltic region. For next week, we expect LNG imports to rise slightly due to the recent narrowing of the Asian LNG-TTF spread as well as higher hub prices in Spain, Italy, and Germany.

EU-27 weekly LNG imports by region (mt)

Source: Kpler Insight. Data represents week commencing 02 and 09 July. NWE=FR, BEL, NL, GER. Iberia=ESP, POR. Med=ITA, HVR, GRE. Baltics/CEE=FI, LT, POL. Others=SWE, MT.

On the demand side, EU-24 gas-fired generation increased by 10% w/w to an estimated of 6.8 TWh, mainly due to lower solar and nuclear generation amid slightly higher power demand. With temperatures in most of Europe forecast to decline below seasonal averages, we expect gas-fired generation to fall next week.

EU-24 weekly gas-fired generation (TWh)

Source: Kpler Power, Kpler Insight.

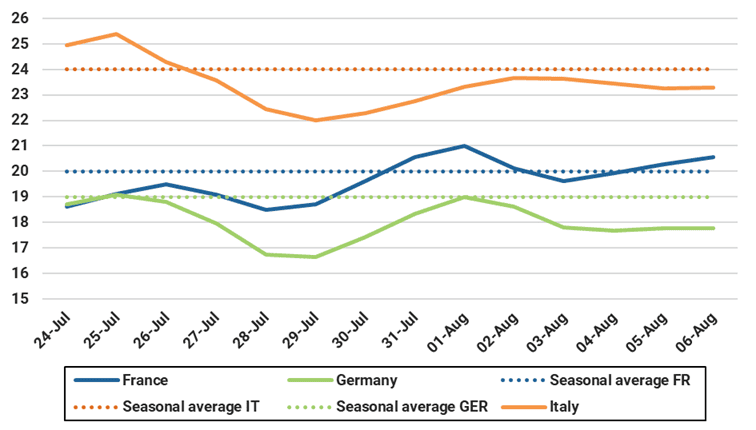

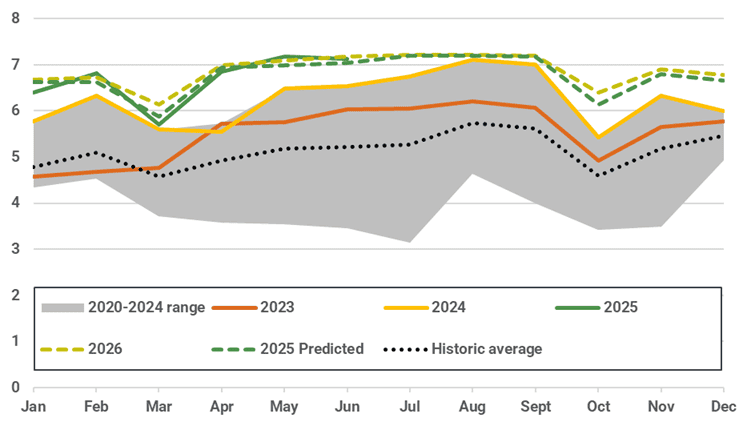

Average forecast temperatures for selected European countries (°C)

Source: Kpler Power. As of 23 July 00:00 UTC.

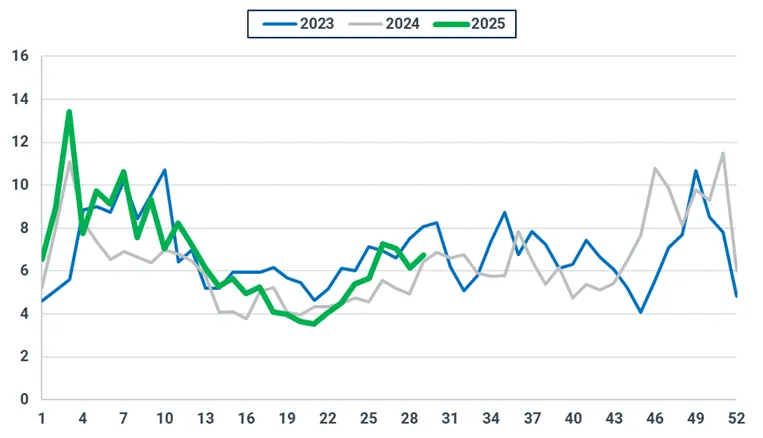

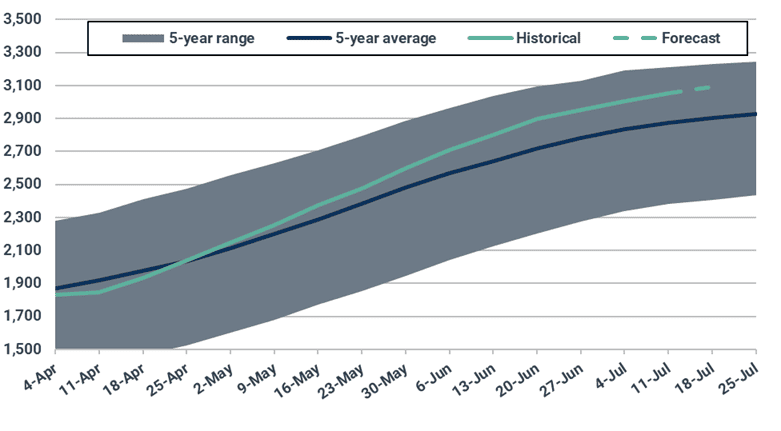

As of 22 July, EU-27 underground gas stocks were 65.7% full (compared to 83.1% last year and the 5-year average of 74%), increasing by 2.1 percentage points w/w. Despite the gradual widening in net cumulative injections relative to the 5-year average at the EU level, different subregional trends continued to develop in recent weeks. For instance, while Austria and Germany have been showing an acceleration in storage injections, driven mainly by higher supply and relatively weak domestic demand, a slowdown is occurring in parts of NWE, notably in the Netherlands, France, and Belgium. Next week, we expect injections to accelerate as lower temperatures spread across the continent and supply is anticipated to remain robust.

EU-27 net cumulative gas storage injections (bcm)

Source: GIE, Kpler Insight. Latest date as of 22/07/25.

Asia: Prices continue to fall amid robust Chinese LNG inventory, steady Pacific supply, and milder temperature expectations in South Korea

Asian LNG prices fell to $11.93/MMBtu on 24 July, down $0.48/MMBtu w/w, as weak demand along with rising Pacific basin supply, exerted downward pressure. Despite persistent heat in Japan and South Korea, spot activity remains subdued.

Bearish sentiment persists for Asian LNG prices next week, with continued strong Chinese inventories, mild South Korean 3-month temperature outlook, and steady Pacific supply outweighing modest demand gains. South and Southeast Asian spot LNG demand is expected to stay muted next week as monsoon conditions curb power needs and prices remain above affordability thresholds.

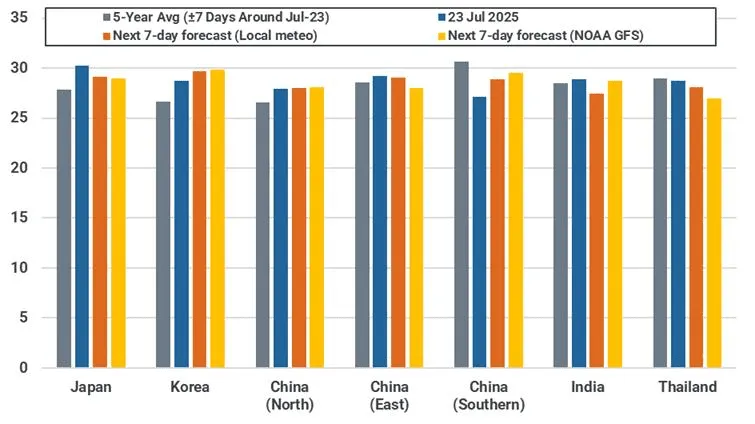

In the week ahead, temperatures across Japan, South Korea, and North China are expected to stay above 5-year averages, sustaining cooling demand momentum through the end of July. In contrast, monsoon-driven rainfall continues to lower temperatures across South and Southeast Asia, while Typhoon Wipha is keeping East and Southern China cooler, both factors weighing on regional gas-for-power demand.

Forecasted average temperatures for Asian countries (°C)

Source: Meteostat, Kpler Insight. As of 24 July 2025 00:00 UTC. Population-weighted average temperature of selected major cities across a country is shown for both historical and forecast.

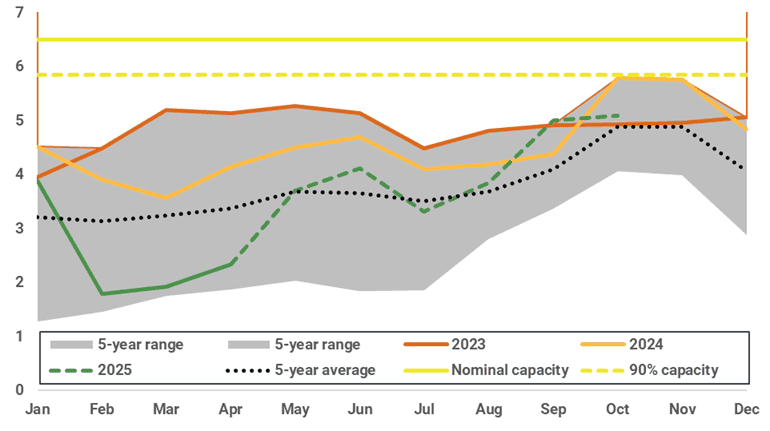

As of 20 July, LNG inventories at major Japanese utilities rose by 0.05 mt w/w to 1.92 mt, as increased rainfall from Typhoon Nari tempered heat and reduced power demand. Looking ahead, a slightly hotter September–October outlook from the Japan Meteorological Agency (JMA) prompted a modest upward revision of 0.1 mt to Q3 demand, but it won’t trigger additional spot demand as term cargoes should cover restocking needs. Kpler Insight forecasts inventories reaching 2.2 mt in August and 2.3 mt in September. The latest US tariff deal also bears no impact on demand expectations, as Japan’s GDP growth forecast remains unchanged at 0.6% for 2025.

Japan implied power sector LNG inventory forecast (mt)

Source: METI, Kpler Insight *Note: Implied power sector LNG inventory includes both major power companies and smaller utilities or independent power producers.

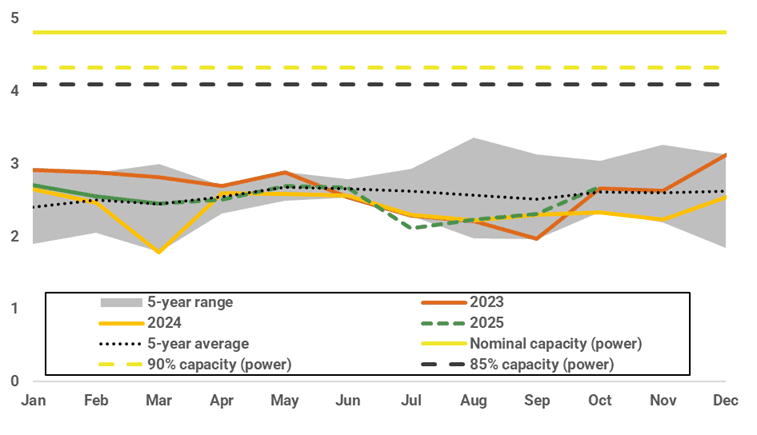

In South Korea, the latest Korea Meterological Agency (KMA) 3-month outlook reaffirms mild conditions for August–September and assigns just a 40% chance of above-normal temperatures in October. As our base case already assumes CDDs in line with the 5-year average from early August, the July–October LNG demand forecast remains at 13.2 mt, with LNG inventory projections unchanged. Lower gas-for-power burn will support stock rebuild, with inventories expected to reach 3.8 mt in August, 5.0 mt in September, and 5.1 mt in October—reinforcing a bearish prompt outlook.

South Korea implied LNG inventory forecast (mt)

Source: KESIS, Kpler Insight

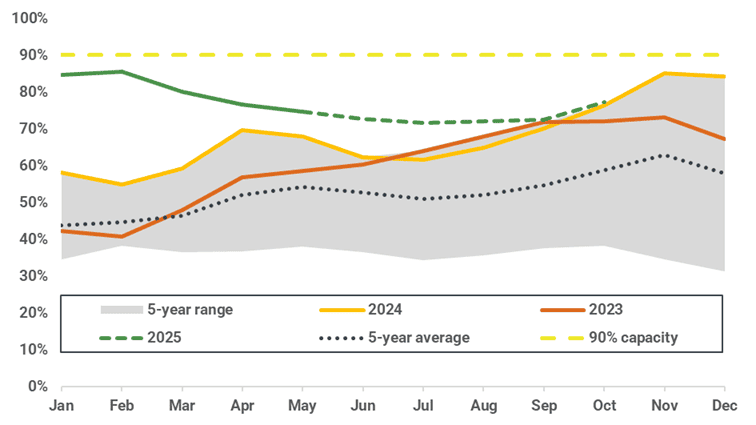

Despite an upward revision to prompt LNG demand in China, Asian spot prices remain under pressure as high LNG inventories and weak spot activity continue to dominate market sentiment. June pipeline imports came in below preliminary estimates, prompting a +0.2 mt upward revision to 2025 LNG demand, slightly lifting Q3 demand. The impact on spot LNG prices remains limited, on the back of robust inventory levels and muted spot market activity.

China implied LNG inventory forecast (%)

Source: Kpler, Kpler Insight

China’s pipeline gas imports by month (bcm)

Source: China Customs, Kpler Insight

US: Henry Hub plummets as supply surges and weather models shed cooling degree days

Henry Hub front-month prices settled at $3.08/MMBtu on 23 July, down substantially from $3.60/MMBtu on 16 July. Going into last weekend, prices appeared to be holding strong above $3.50/MMBtu as a forecast hot end to July lent some bullish energy. However, market sentiment veered sharply into bearish territory come Monday.

Revisions to the US and EU weather models over the weekend now show a much cooler first week of August, with the US model losing nearly 10 CDDs. Though hot weather is still forecast for the next few days, market players are looking firmly beyond July and into early August. The northeast, Midwest, and western US are now all expected to experience below-average temperatures in early August. Additionally, an uptick in natural gas production over the last week saw output climb to nearly 107 Bcf/d, contributing to the bearish overtones. Rig counts also added to this sentiment, with a w/w increase and the Haynesville notably adding three rigs. These factors combined led to front month prices settling at $3.33/MMBtu on Monday, down $0.23/MMBtu from Friday. Henry Hub continued to tumble on Tuesday and Wednesday as both fundamentals and technicals remained suffused with bearish sentiment.

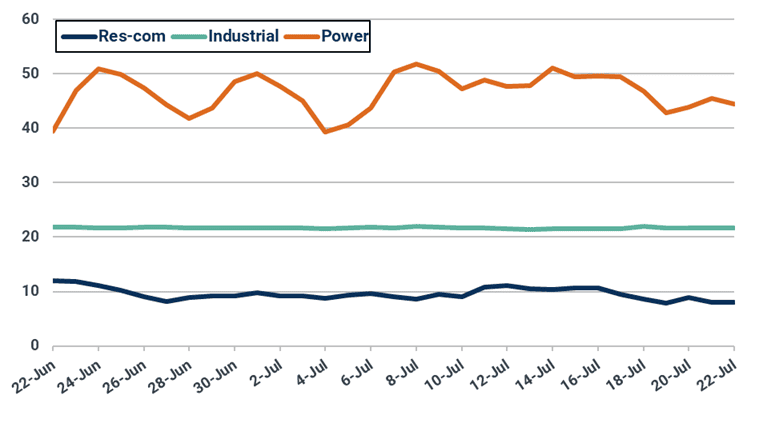

US domestic gas consumption by sector (bcf/d)

Source: EIA

Temperatures are projected to increase across the Lower 48 over the next few days, with triple-digit highs forecast for the entire southern half of the country. Despite this broad swath of heat, gas-fired power generation is unlikely to reach the record levels seen last summer. Though demand may slightly exceed the 50 Bcf/d mark, as it did during the late-June 2025 heat wave, robust renewables generation is expected to cut into gas burns, especially in Texas. Erratic price behavior is likely over the next week as the market contends with bearish August weather forecasts, strong gas production, bargain buying, and the roll off of the August futures contract on 29 July. Kpler Insight expects prices to rebound slightly towards $3.30/MMBtu over the coming week.

Forecast of cooling degree days

Source: National Weather Service

US dry gas production averaged roughly 106.5 Bcf/d over the last seven days, as producers pushed supply into the market on the eve of this week’s summer weather. Supply is likely to remain elevated over the next several days, though if prices continue to retreat, producers may be inclined to reduce output. Kpler Insight expects production to average near 106 bcf/d over the next week.

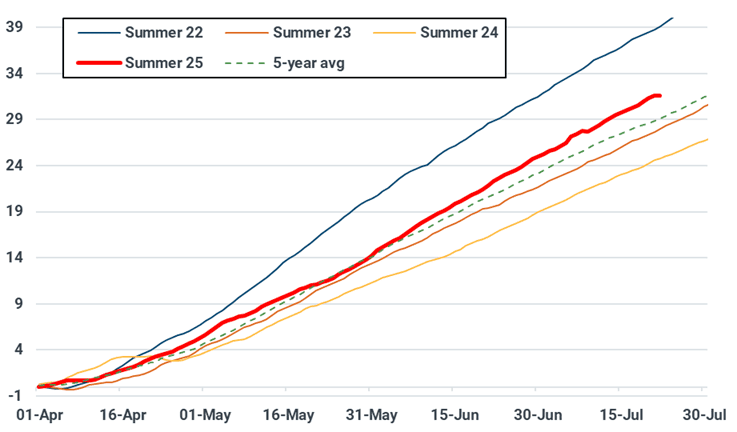

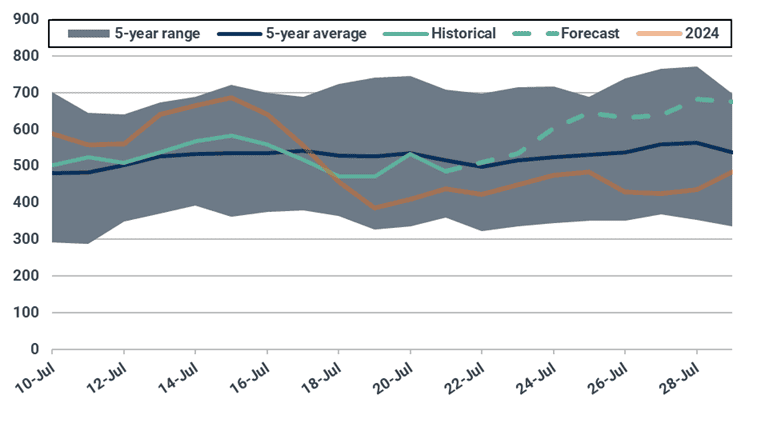

The US injected 36 Bcf into underground storage for the week ending 11 July, roughly in line with consensus. Relatively strong gas-fired power demand last week is expected to have led to a relatively modest storage build. Kper Insight forecasts a net injection of 38 Bcf for the week ending 18 July.

US underground gas stocks (bcf)

Source: EIA, Kpler Insight

LNG Supply: Exports to remain stable this week, increases expected next week as maintenance wraps up in the US, Norway, and Australia

Global LNG exports held steady at 8.03 mt last week, with higher supply from Nigeria (+0.17 mt w/w) and Russia (+0.10 mt w/w) due to the return of the 10.8 mtpa Sakhalin 2 post-maintenance, offsetting a reduction in exports from Indonesia (-0.10 mt w/w) and Malaysia (-0.09 mt w/w).

Looking ahead, Kpler Insight expects no major change in global LNG supply availability this week. However, next week, global LNG exports could increase with the US’ 2.5 mtpa Elba Island currently restarting from maintenance, Australia’s 9 mtpa APLNG returning to full service from 24 July and Norway’s 4.2 mtpa Hammerfest scheduled to end maintenance on 29 July. Rising exports from new North American projects – Plaquemines and LNG Canada - could further boost exports towards the end of the month.

Global LNG exports (mt, 10-day moving average)

Source: Kpler

In the Pacific basin, Russian supply from the 10.8 mtpa Sakhalin 2 plant has returned to typical levels following maintenance that started in mid-June. The return to full output increases LNG availability to northeast Asia, in particular Japan, which offtakes approximately 50% of exports.

In Australia, brief maintenance at the 9 mtpa APLNG facility, which began on 18 July, is expected to conclude by 24 July. The next major maintenance rounds are scheduled at 7.8 mtpa Gladstone LNG starting 9 August, and at 8.9 mtpa Ichthys beginning 18 August. Separately, Kpler continues to track developments at the Barossa gas field, which is expected to begin first gas production in Q3 2025, providing backfill for the 3.7 mtpa Darwin LNG project—offline since November 2023 due to feedstock shortages. Project operator Santos reported in mid-July that the project was 97% complete.

Meanwhile, Malaysia’s 10-day moving average exports have declined, primarily due to lower volumes from the 29.3 mtpa Bintulu plant. Market participants attribute the drop to a minor instrumentation issue, which is expected to be resolved shortly. In addition, the 1.2 mtpa PFLNG 1 facility in Sabah has not exported a cargo since 4 July, likely due to ongoing maintenance.

Elsewhere in the Pacific basin, the first 7 mtpa train at LNG Canada has been consistently producing at a rate of one cargo per week, with potential to ramp up to two cargoes this week. All exports to date have been directed to Northeast Asia, with one cargo delivered to Japan and two to South Korea.

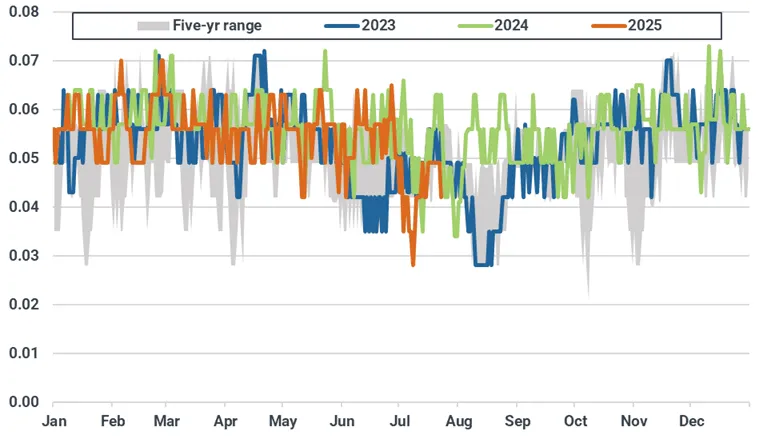

Malaysia’s Bintulu LNG exports (mt, 10-day moving average)

Source: Kpler

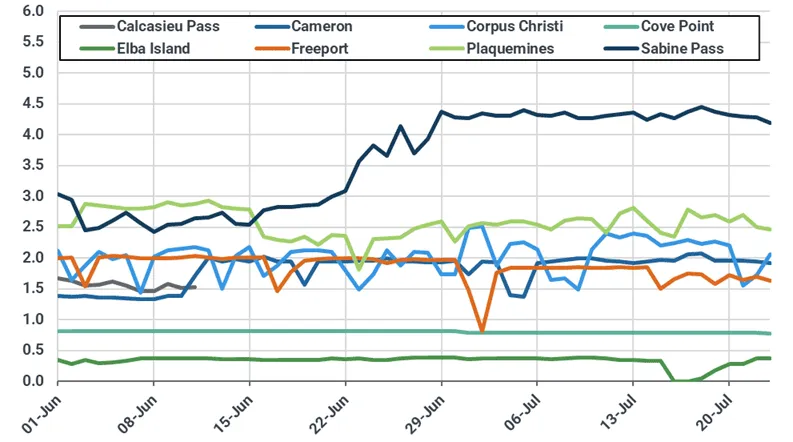

In the Atlantic basin, the 22 mtpa US’ Plaquemines plant has been cleared to introduce hazardous fluids into block 14 of 18, paving the way for further export growth in Q3. Meanwhile, the 2.5 mtpa Elba Island plant has seen its feedgas flows recover following a short period of planned maintenance which took the entire plant offline (see chart below).

US LNG feedgas deliveries by plant (bcf/d)

Source: Williams, Cheniere, Sempra, Boardwalk, Kinder Morgan, Berkshire Hathaway

Exports from Russia’s 17.4 mtpa Yamal LNG remain below typical seasonal levels, likely due to ongoing maintenance, which is hampering deliveries to both Europe and China. Meanwhile, Norway’s 4.2 mtpa Snohvit plant is expected to resume production on 29 July, with four ballast vessels currently waiting offshore. Elsewhere, the UAE’s 5.8 mtpa Das Island plant remains underutilised based on 10-day moving averages, equivalent to 1 of 3 trains offline.

Russia’s Yamal LNG exports (mt, 10-day moving average)

Source: Kpler

Want market insights you can actually trust?

Our analysts are updating Insight in near real-time, delivering critical intelligence on trade flows, pricing shifts, and geopolitical risk.

Updates are live across oil, LNG, and cross-commodity sectors.

Request access here.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data