Moving metal: navigating costs, congestion, and carbon in the aluminium supply chain

The aluminium supply chain uses both dry bulk carriers and containership freight to move raw materials and products from producer to consumer. This leaves it open to two, sometimes divergent, sets of freight market fundamentals.

Dry bulk carriers are employed to ship bauxite from mines to refineries, as well as alumina for further processing. Aluminium products are generally carried on containerships, although the high cost of container freight has occasionally pushed them onto small dry bulk carriers.

There has been a divergence in the dry bulk freight market this year, with larger Capesize (100k+ dwt) vessels outperforming the smaller ships. Capesizes have enjoyed an average earnings premium of +32% to the smaller Panamax (68,000-99,999 dwt) in the year-to-date. This compares with a long-term average of only +12%.

Alongside iron ore, Guinean bauxite exports to China are a key driver of Capesize market strength, with shipments up by 36% y/y to 96.90 Mt over January-August. Volumes are about to start ramping up again following a lull during the rainy season (May-October), and a strong pace of trade is expected, despite policy-driven uncertainty in the Guinean mining sector. By contrast, lower Pacific coal trade has weighed on earnings for sub-Capesize vessels.

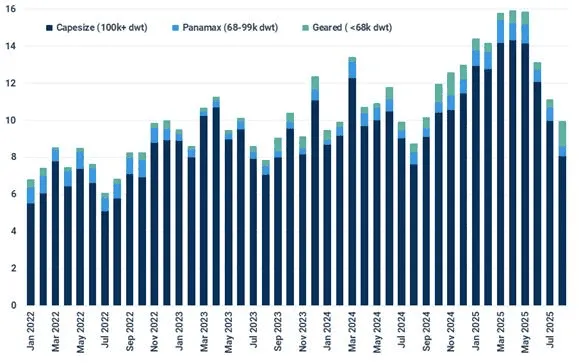

Guinean bauxite trade is dominated by Capesize cargoes to China (Mt)

Source: Kpler

The containership market has been shaken by macro trends linked to trade tariffs and threats to global economic prosperity. Efforts by shippers to front-run tariffs generated volatility and market spikes, although overall earnings are still lagging behind 2024. The FBX Global Container Index is down by 27% y/y in 2025 to date.

Containership earnings would be lower still were it not for the tightening effect on tonnage supply of vessels being forced to reroute around the Cape of Good Hope instead of sailing through the Red Sea. The sinking of two dry bulk carriers (Magic Seas and Eternity C) in July, plus subsequent attacks on shipping, have reinforced the risks of this route.

Rerouting imposes additional costs on charterers with a Shanghai-Rotterdam voyage using the Cape of Good Hope, 30% longer and an extra eight days voyage time (at 17 knots) compared with the Red Sea route, with a consequent increase in carbon emissions. Without the supply-tightening effect of the Red Sea crisis, the surge in containership deliveries in 2024, when a massive 430 ships totalling 2.87 million TEU of capacity were delivered, would have resulted in lower costs for charterers and reduced earnings for owners.

Dry bulk carriers are more willing to run the Red Sea risk. We have observed an upturn in dry cargo volume through the region since the start of the Russian Black Sea wheat export season. These are primarily cargoes for countries in the Middle East and East Africa, and sailing around the Cape of Good Hope would not be economical.

We do not expect a normalisation of trade through the Red Sea in the short or medium term.

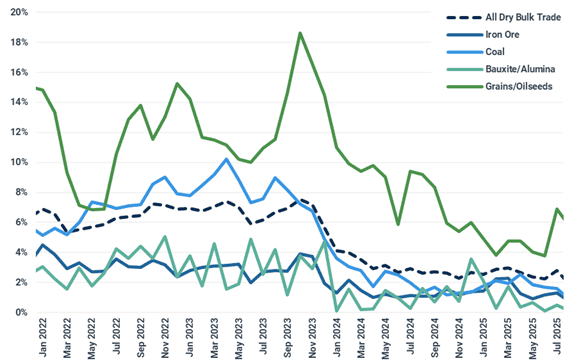

Seaborne dry bulk trade via Red Sea/Suez Canal: upturn in grain shipments (% total trade)

Source: Kpler Insight

Capesize dry bulk carrier earnings are set to firm, with smaller bulkers lagging behind. This will see higher costs on West Africa-China bauxite trade, but Panamax shipments into Europe will not see the same uplift. Nor will alumina shipments utilising geared vessels.

An unusually high 21% of the dry bulk carrier fleet is due for five-year special surveys in 2026 (reflecting the surge in deliveries in 2011). This will tighten supply and support earnings. Again, the Capesize fleet will be the most affected. An increase in newbuilding deliveries in 2025, projected at 558 vessels (43.40 Mdwt) compared with 400 (28.55 Mdwt) in 2024, will partially compensate.

The containership market will see policy-driven volatility, but costs should remain below the highs of 2022 and 2024. Earnings should see support from fleet inefficiencies in 2026 as US port fees on Chinese-linked vessels encourage ships to either call at Canadian and Mexican ports and then rail containers to the US, or limit US port calls to key terminals such as Long Beach. Either will increase congestion and delays at these ports. However, from 2027, a surge in newbuilding deliveries will see a new wave of large vessels hitting the water. This jump in supply will put downward pressure on earnings.

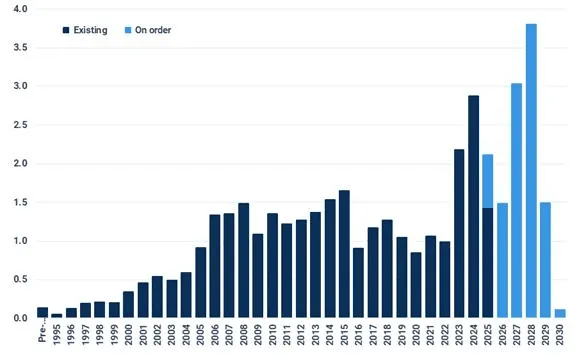

Containership newbuilding deliveries set to surge from 2027 (TEU)

Sources: Kpler Insight, Braemar

See why the most successful traders and shipping experts use Kpler

Gain clarity on dry bulk flows, rates & fundamentals to navigate market shifts precisely