Next in line for demand losses: Africa transportation fuels

High import dependency on gasoline, jet fuel, and diesel from the Mideast Gulf, particularly in East and Southern Africa, combined with limited inventory buffers, could result in immediate demand losses. These losses are projected to peak at 260 kbd in May, assuming normal shipping conditions through the Strait of Hormuz resume by July.

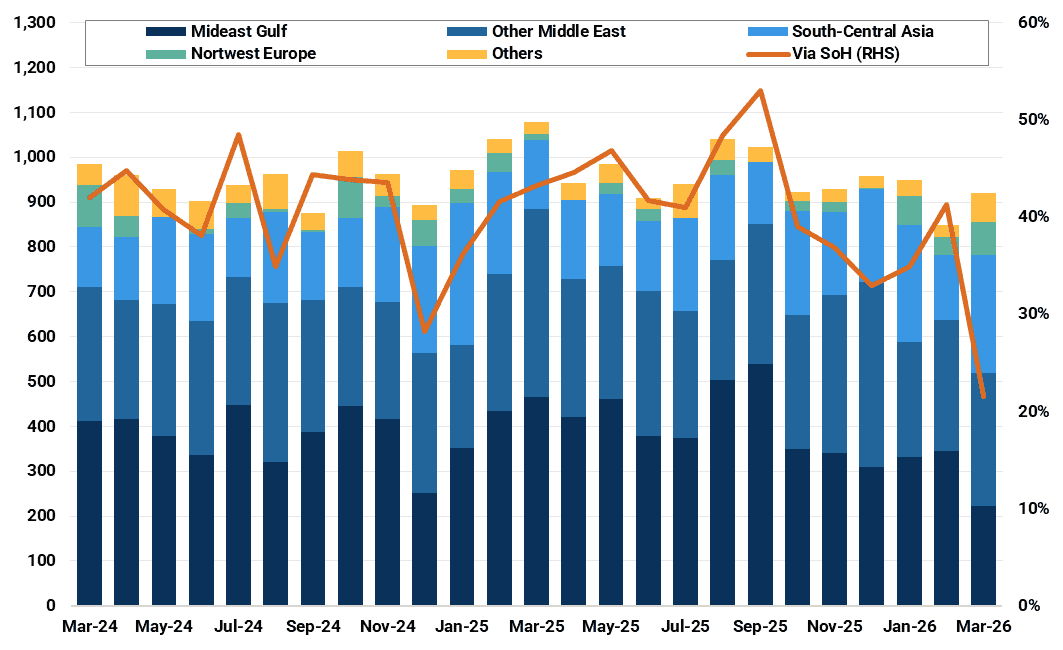

As we continue to update our Refined Products Balances for the April release, and following our previous analysis of demand losses in Asia-Pacific, we find that transport fuel demand in Eastern and Southern Africa is also highly exposed to disruptions in flows through the Strait of Hormuz (SoH) and to the broader implications of the ongoing US/Israel-Iran conflict. Indeed, imports of gasoline, gasoil/diesel, and jet fuel/kerosene routed through the SoH to East and South Africa accounted for an average of 42% of total inflows in 2025.

Eastern and Southern African gasoline, kero/jet and gasoil/diesel imports by origin (kbd)

Source: Kpler

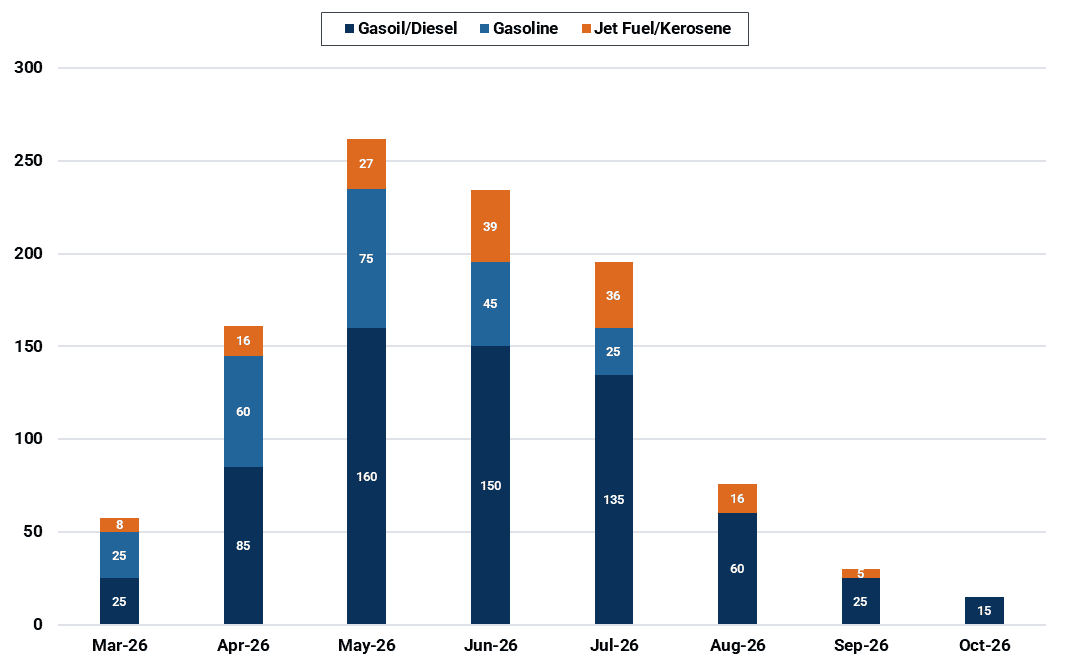

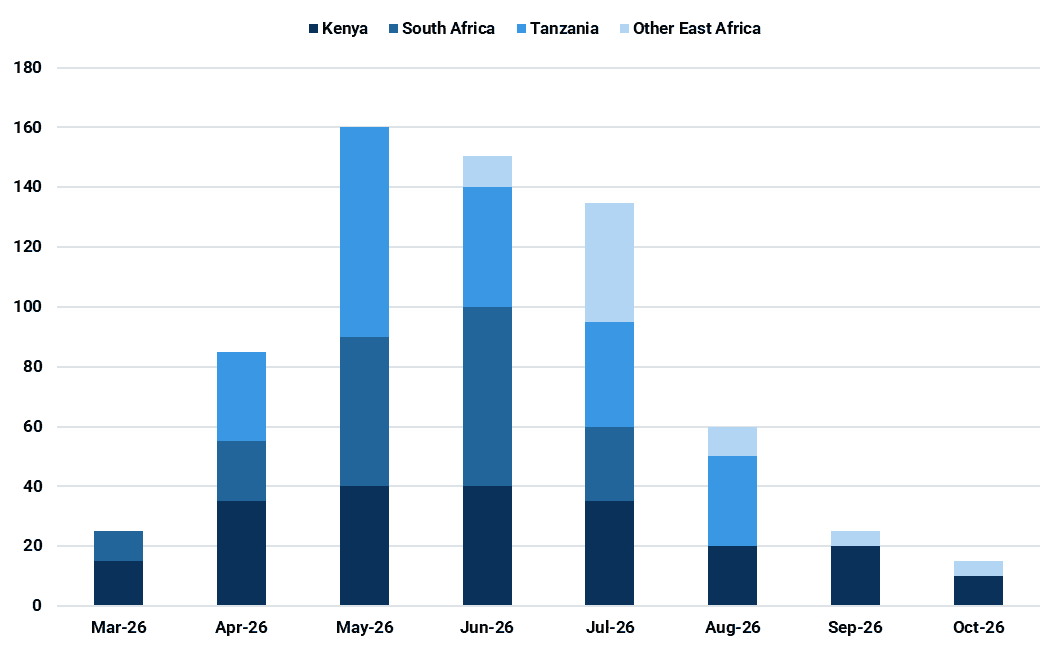

Under a de-escalation scenario for the reopening of the SoH, assuming attacks subside between April and May and allow for phased normalization of flows by July, transport fuel demand losses are expected to peak at 260 kbd in May. Losses remain elevated thereafter, not falling below 150 kbd over the April to July 2026 period, with gasoil/diesel bearing the largest share of the impact.

To estimate these losses, we apply a framework consistent with our Asia-Pacific analysis, conducting a country by country and product level assessment. This approach evaluates the extent of demand cuts required, under current supply and trade assumptions, to prevent inventories from falling below minimum operational thresholds.

Transport fuel demand loss in East and South Africa (kbd)

Source: Kpler

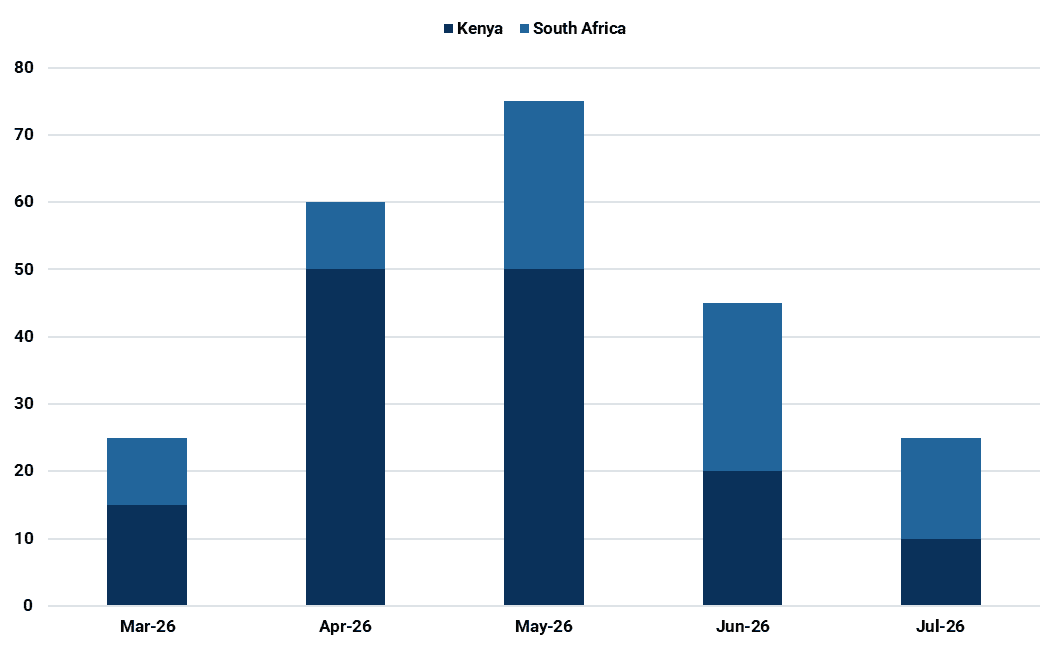

East and South Africa gasoline demand loss (kbd)

Source: Kpler

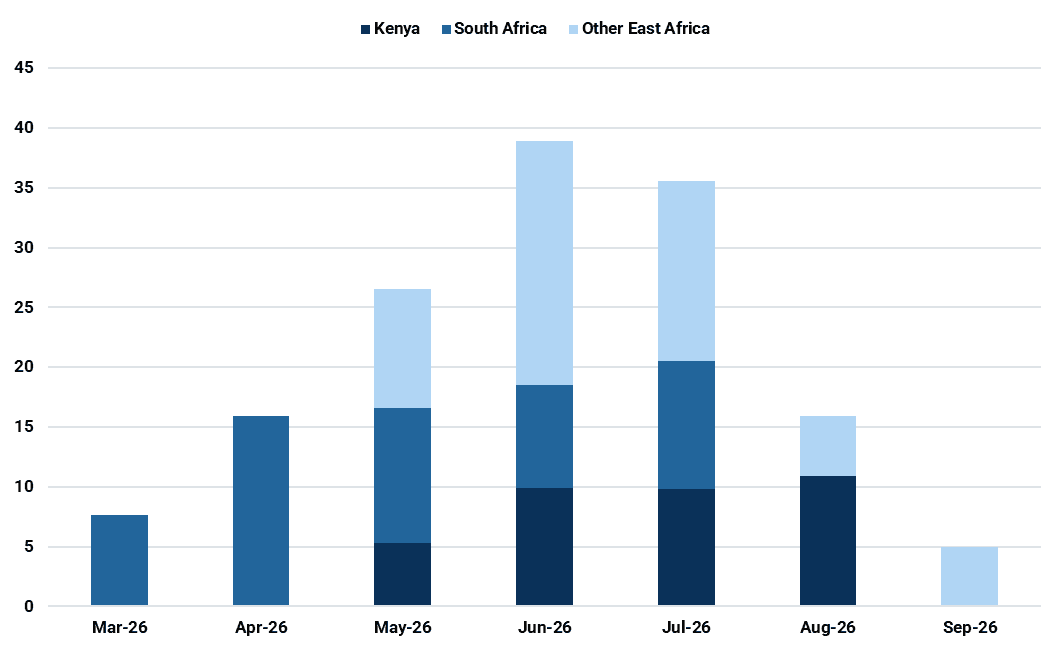

East and South Africa jet fuel/kerosene demand loss (kbd)

Source: Kpler

East and South Africa gasoil/diesel demand loss (kbd)

Source: Kpler

We have applied the following assumptions for aggregate transport fuel export reductions from key major hubs through July 2026:

- UAE, Kuwait, Bahrain: 50-90% export reductions

- Saudi Arabia: 20-50% export reductions

- Qatar: 60-95% export reductions

- Oman: 10% export reductions

An important distinction relative to Asia-Pacific is worth emphasizing. In the East of Suez, refinery run cuts, constrained crude availability, and the prioritization of domestic supply are major factors driving inventory stress and, ultimately, demand rationing and losses. In contrast, East Africa is fully import dependent, with no domestic refining capacity. While South Africa operates the Cape Town refinery and NATREF, with combined distillation capacity of 208 kbd, this is structurally insufficient to meet its own demand, let alone that of the landlocked markets it supplies.

Against this backdrop, and in the context of already limited storage buffers, the region’s exposure extends beyond reliance on uninterrupted product flows through the SoH. It is also directly tied to the extent and duration of refinery disruptions in the Middle East, as captured in our supply assessment. This reinforces the fragility of the current balance and introduces additional downside risk to the demand outlook, all of which will continue to be closely monitored.

Market insights you can actually trust

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions. In times of conflict and geopolitical uncertainty, our real-time data keeps you ahead of supply disruptions and price volatility.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

.png)