Oil products demand outlook for 2025 and 2026 (Update)

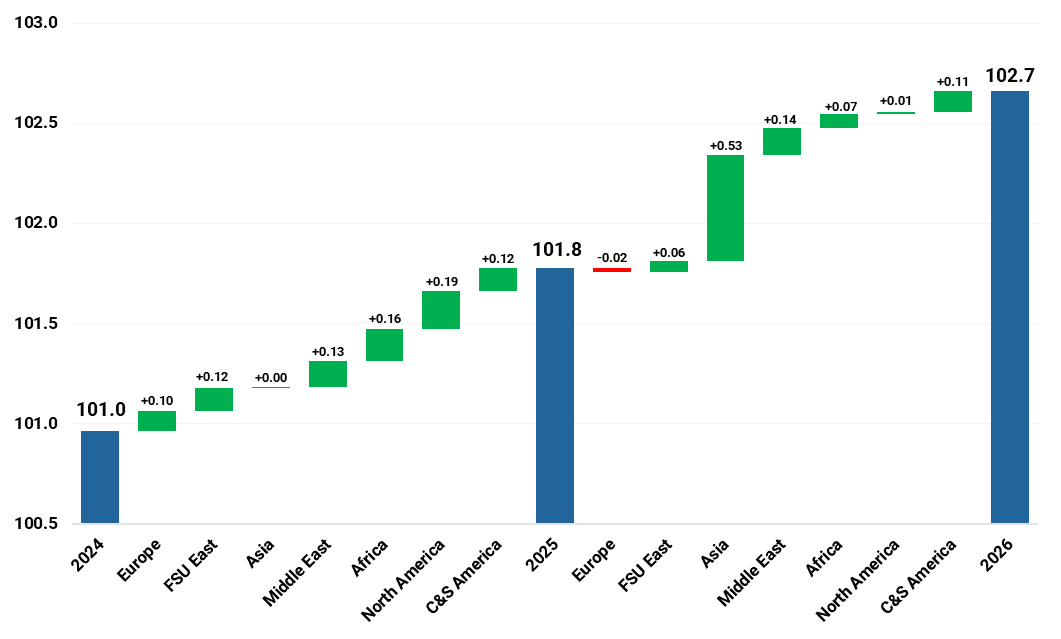

Global oil product demand (excl. ethane) is now forecast to grow by 0.84 mbd y/y in 2025 and by 0.88 mbd in 2026. The latest data shows sluggish demand across key economies. With consumer confidence subdued and renewables continuing to gain market share, a sharp rebound remains unlikely. This update outlines regional growth projections and the primary factors shaping the outlook.

Global oil products demand (mbd)

Source: Kpler, based on observed statistics; estimates from June 2025 onward.

Europe: Light ends demand will remain under pressure due to weak steam cracking margins and elevated energy costs. The closure of Italy’s remaining crackers is contributing to a sharp contraction in naphtha demand this year. In 2025, rising gasoline and jet fuel consumption, supported by robust hybrid and gasoline vehicle sales, is expected to offset declines in naphtha and fuel oil. However, by 2026, diesel demand is set to return to structural decline following a temporary boost in 2025 from fuel oil substitution under the new Mediterranean ECA. As a result, total oil demand growth in the region is projected to turn negative.

FSU East: Russian transport fuel demand is expected to maintain a steady growth trajectory, supported by the limited near-term penetration of electric vehicles and renewable fuels.

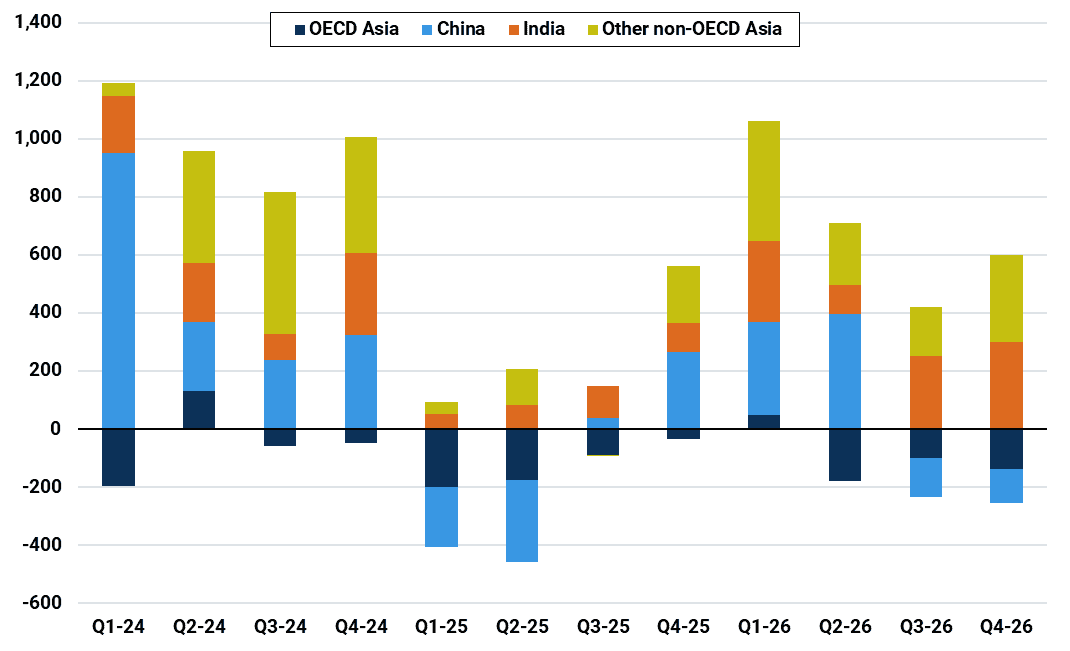

Asia-Pacific: Liquids demand in Asia-Pacific is expected to see no y/y growth in 2025. Several dynamics are at play:

- OECD Asia will remain on a downward trend. Light ends are impacted by persistent overcapacity linked to China’s recent petrochemical expansion. Slowing economic growth, an ageing population, and continued gains in vehicle efficiency are weighing on domestic fuel demand, especially diesel.

- China is projected to register a decline in total product demand this year. LPG has been particularly hit by ongoing US-China trade tensions. Gasoline demand is starting to fall due to rising EV adoption, a trend expected to continue through 2026. Diesel faces similar pressures from the growing use of LNG and electric trucks.

- India is experiencing disappointing growth at 1.7% y/y, reflecting the country’s structurally lower oil intensity compared to China during its 2000s expansion. Naphtha and other product categories are set to post meaningful declines.

- Southeast Asia, particularly Vietnam and the Philippines, is seeing a broad-based slowdown. Diesel demand is notably weak, and overall regional growth will be limited in 2025.

Assuming a more stable global economic and trade environment, demand in Southeast Asia is expected to recover in 2026. Chinese LPG demand could rebound with the ramp-up of new PDH plants, especially if accompanied by an improved trade deal with the US. This would support a healthier environment for naphtha-fed cracker utilization. These developments, alongside stronger jet fuel and fuel oil consumption, should help offset ongoing declines in gasoline and diesel, returning Chinese total product demand to positive growth in 2026.

Asia total oil products year-on-year demand change (kbd)

Source: Kpler, based on observed statistics; estimates from June 2025 onward.

Middle East: Product demand is expected to grow steadily. Significant fuel oil declines are not anticipated before 2027, by which time Saudi Arabia’s Vision 2030 energy transition targets—50% renewables and 50% gas—begin to materialize.

Africa: Strong growth is forecast for 2025, driven by diesel and LPG, supported by fuel substitution under the Med ECA in North Africa and ongoing economic expansion. Industrial activity and infrastructure development remain key contributors. However, growth in 2026 will be constrained by a sharp drop in Egyptian fuel oil demand as new FSRUs come online.

North America: Demand growth in 2025 will be led by LPG, rising by 110 kbd y/y due to strong heating demand during Q1 on the US East Coast. Jet/kero demand is also expected to grow by 60 kbd, supported by low aircraft fleet renewal rates and sustained growth in air traffic. These gains will be partially offset by declines in gasoline and diesel demand, down 15 kbd and 30 kbd respectively. In 2026, gasoline consumption is set to fall further as fuel economy standards tighten, while tariffs are expected to weigh on freight activity, reversing the diesel gains seen earlier in 2025. As a result, total oil product demand is projected to remain flat y/y in 2026, before entering a decline in 2027.

C&S America: Brazil, and to a lesser extent Argentina, will continue to drive regional growth. However, overall expansion will remain modest as the region contends with tariffs and enduring structural challenges, including institutional inefficiencies, low labour productivity, and an underdeveloped manufacturing base—factors that continue to constrain its growth potential relative to other emerging markets.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Get research & analysis driven by proprietary data

.png)