India unlikely to rapidly drop Russian oil, despite Trump remarks

Recent remarks by Donald Trump on October 15, suggesting India would reduce Russian crude imports, are likely pressure tactics linked to trade negotiations rather than a reflection of an imminent policy change. Russian barrels remain deeply embedded in India’s energy system for economic, contractual, and strategic reasons. Kpler data shows no visible sign of a reduction, with October imports tracking around 1.8 Mbd. Any adjustment is likely to be symbolic rather than structural.

Key takeaways

- No policy shift evident: Recent remarks by Donald Trump suggesting India will cut Russian oil imports appear to be political posturing, with no official confirmation from New Delhi.

- Flows remain robust: Kpler data shows no sign of a slowdown. Indian imports of Russian crude are tracking at a strong 1.8 Mbd so fair in October, provisionally up 250 kbd from September.

- Economics still compelling: Russian crude remains structurally vital for India, accounting for roughly 34% of its total imports and offering compelling discounts that are too significant for refiners to ignore.

- Market shrugs off threat: The oil market is exhibiting "pricing fatigue" to such threats. The back end of the Brent curve is weakening in anticipation of a supply glut, not a disruption, signaling that traders do not see a credible risk to Russian flows to India.

- Politics to determine Indian intake mix: Ultimately, it is likely to be a political decision that decides the fate of Russian oil flows to India. Given India's balanced foreign policy stance, any block of imports seems unlikely at this time.

Recent comments by Donald Trump suggesting India is poised to reduce or halt its imports of Russian crude should be viewed as a political pressure tactic rather than a signal of a concrete policy shift. There has been no official statement from the Indian government to directly support this claim, with a spokesman also claiming no knowledge of a discussion between Trump and Modi yesterday.

On the contrary, Kpler data shows that India’s intake of Russian oil remains robust, with October flows tracking at approximately 1.8 Mbd, an increase of around 250 kbd from the previous month (though the current month data is subject to revision). Russian barrels maintain their position as the largest single source of crude for India, with a market share of roughly 34%. This underscores the deep economic and structural reliance that is unlikely to be unwound by political rhetoric alone.

The rationale for India’s continued procurement is clear. Even with narrower discounts than in 2023, Russian barrels remain one of the most economical feedstock options available to Indian refiners, due to landed discounts and high GPW margin outputs from grades such as Urals. The landed India price for Urals reached parity to Dated Brent earlier this month, up from around $6-7/bbl discount in early September. Furthermore, the country's energy system is now structurally integrated with Russian supply through term deals, established supply chains, and optimised refinery configurations.

Delivered-India crude differentials to North Sea Dated, $/bbl

Source: Kpler based on Argus Media data

Replacing Russian barrels is technically possible on paper, but politically and economically fraught

More barrels could flow from the Middle East, Latin America, and the US; similar to India’s pre-2022 crude slate. Indian refineries can handle diverse crude grades, so the technical constraint is minimal. But whether New Delhi is ready to make that shift is another matter. The reality is that cutting Russian imports would be difficult, costly, and risky. Russia still supplies around 30-35% of India’s crude. Substitution would require rapid scaling from multiple suppliers, at higher costs (freight, weaker discounts). If margins compress or retail prices rise, the result could be inflation, political backlash, and weaker refinery profitability. Higher-cost crude could also worsen domestic operating budgets and put pressure on refiner credit lines.

Refiners will therefore look to squeeze every dollar of margin unless directed by New Delhi. While there has been a stronger push for diversification, contracts for Russian crudes are typically signed 6–10 weeks before arrival. Rewiring all that takes time. In practice, Indian refiners are gradually broadening their baskets, not to replace Russia in the short term, but to enhance energy security and flexibility.

Alternatives like Iran or Venezuela remain entangled in sanctions, complicating substitution unless the US explicitly relaxes restrictions. So, whether India reduces its dependence will depend heavily on the strength of US pressure and how much volatility India is prepared to absorb. For now, the Russia–India oil partnership remains intact and central.

India has consistently pursued an independent foreign and energy policy, balancing economic interests with diplomatic relationships. A sudden shift away from Russian crude would undermine its energy security strategy and is unlikely unless formal US secondary sanctions, similar to those on Iran, are imposed.

At this stage, it’s improbable that India will implement structural cuts purely to satisfy US and EU political pressure. If Washington intensifies pressure, Indian refiners could make a token reduction — on the order of 100–200 kbd — to demonstrate diversification and appease Western partners. However, these cuts would likely be symbolic rather than transformative.

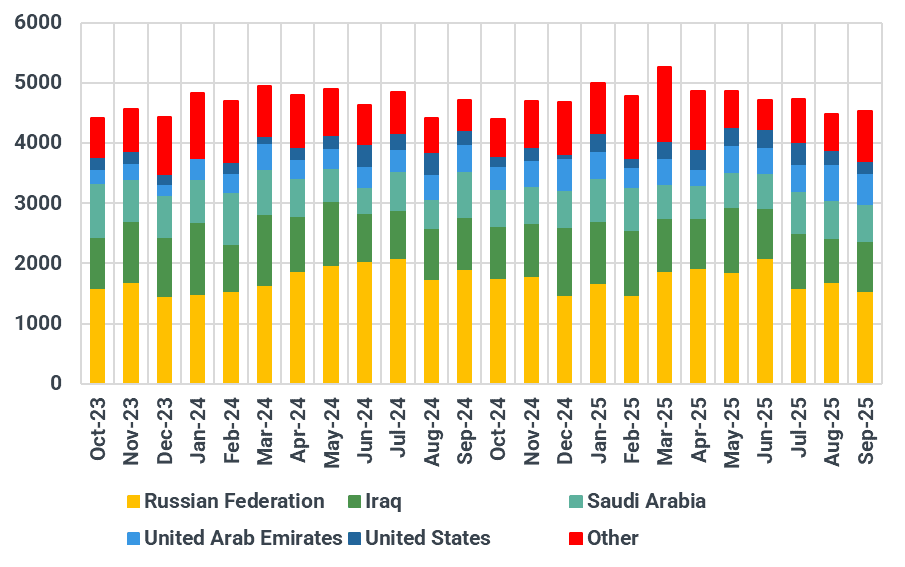

India crude and condensate imports by origin, kbd

Source: Kpler

Can India import high volumes from the US?

Linked to the trade talks rhetoric is the question that President Trump also desires more buyers of US crude. India has limited upside to take US material, around 400-500kbd, due to US grades facing higher outright and transportation costs, along with compatibility challenges with Indian refining systems. India’s refinery system’s attempt to diversify has meant that imports of US crude have averaged 295 kbd so far in 2025, an increase from 199 kbd in 2024.

India imports of US crude by year, kbd

Source: Kpler

Financial markets shrug off this headline, again

The broader oil market appears to agree that the threat to these flows is not credible. There is significant "pricing fatigue" regarding this topic, and the market’s structure indicates that traders are more concerned about a potential supply glut than a disruption. Both ICE Brent flat price and prompt structure have been muted regarding the headlines, with greater focus further down the curve.

The December 2025-2026 strip is hitting its lowest levels since June, with the prompt six month ICE Brent strip near year-lows. Therefore, price remains the key driver for any meaningful reduction in India's Russian imports, even in the face of continued external pressure.

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Research & analysis driven by proprietary data