India–US trade deal to reshape marginal crude flows, not displace Russian barrels

The India–US trade deal announced on 2 February is unlikely to trigger a near-term reduction in India’s Russian crude imports. Russian volumes are largely locked in for the next 8–10 weeks and remain economically critical for complex Indian refiners. Instead, the deal reinforces an ongoing diversification trend, with US crude emerging as the primary marginal winner and Venezuelan crude offering optional, non-structural upside. The adjustment is expected to be compositional rather than volumetric.

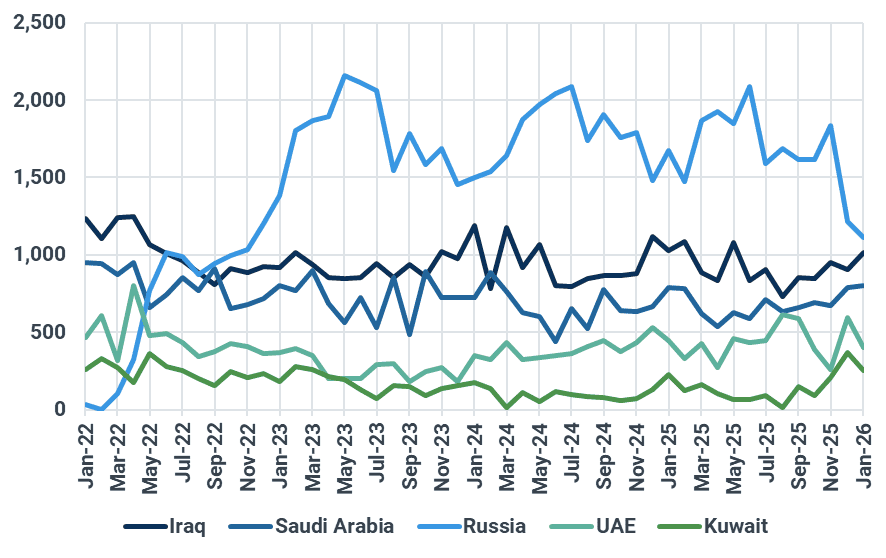

Russian crude flows to India seen continuing

Indian imports of Russian crude are expected to remain broadly stable in the ~1.1–1.3 Mbd (with upside risk) range through Q1 and early Q2, with cargoes for the first half of March largely fixed, logistics in place, and refinery economics continuing to favour discounted Russian grades. Despite a recent moderation in purchases (Higher Middle East crude volumes have offset declining Russian imports), India is unlikely to fully disengage in the near term, as an abrupt shift could disrupt refining economics and raise overall energy costs; while refiners are technically capable of operating without Urals and can process alternative grades, a complete move away would require careful management of commercial factors such as feedstock costs and margins, alongside broader political and diplomatic considerations. Redirecting demand entirely toward non-Russian suppliers would also intensify competition for available barrels, reduce supply flexibility in other importing regions, and place pressure on global crude differentials. Reliance Industries’ re-entry into the Russian crude market, with cargo(s) unloading on 1 February after a brief pause, underscores the continued commercial competitiveness of Russian barrels. With trade-related arrangements and bilateral mechanisms progressing, any policy-driven recalibration of Russian crude intake is likely to remain gradual rather than immediate.

As stated, price remains a key factor. Urals crude is being offered at discounts around $9/bbl to ICE Brent, some $4-5/bbl cheaper than where Venezuelan barrels are being shown (with WTI as a blend stock trading near parity to ICE Brent on a delivered-India basis).

Looking ahead, we do not anticipate any substantial further decline in Russian crude volumes into India from current levels. As outlined in our November note, imports have already moderated from a 2025 average of around 1.7 Mbd and are expected to stabilise broadly within the 1.1–1.5 Mbd range. A more pronounced reduction would likely require a clear policy shift by the Government of India, which appears highly unlikely given that energy security & economics remain a primary policy objective amid increasingly complex geopolitical dynamics shaping global oil trade flows.

Venezuelan crude: Optional, not transformational

Venezuelan crude could re-emerge as an supply source for some Indian refiners, given its compatibility with India’s complex refining systems. However, any volumes are likely to remain episodic, constrained by current processing economics, as discounts are less attractive compared with levels previously available to refiners, alongside ongoing considerations around sanctions compliance, insurance, and blending requirements. As a result, Venezuelan barrels are more likely to serve as a tactical pricing and negotiation lever against Russian grades rather than a sustained or structural replacement.

US crude: Marginal gains accelerate

US crude imports into India have remained strong in recent months and are expected to stay supported following the deal. US barrels could account for up to ~10% of India’s crude intake, largely displacing lighter West African grades rather than Russian crude. From a refinery optimisation perspective, refiners may also blend WTI with Venezuelan crude, creating a “dumbbell-shaped” yield profile that is well suited to India’s complex refinery configurations, allowing refiners to maximise middle distillate and residue upgrading margins. Overall, the ongoing adjustments in India’s crude sourcing are unlikely to materially alter refined product yields, as the underlying crude slate remains broadly unchanged. While incremental volumes may shift between suppliers, refiners are largely substituting like-for-like grades and optimising blends within existing specifications, allowing product yield structures to remain stable across the system.

India crude imports by origin country, kbd

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler