Oil prices fly on geopolitics, but fundamental risks lurk beneath

While geopolitics remains the main driver of oil prices, the underlying supply surplus remains a key risk that could turn against price bulls once fundamentals return to centre stage.

Key takeaways:

- Supply-side issues in the West of Suez tightened the global balance to ~1 mbd in January, from a previously forecast surplus of ~2 mbd.

- This front-end tightness does not alter the structural surplus, with average oversupply in Q1 still estimated at around 2.2 mbd.

- The buildup of sanctioned barrels on the water and China’s stockbuilding has inflated the headline surplus, but the effective balance length is still assessed at around 1.5–1.6 mbd.

- Global oil on water (excluding sanctioned barrels) and ex-China onshore inventories remain well above Q1 2025 levels, pointing to continued weakness in fundamentals.

The high volatility seen so far in 2026 underscores the increasingly critical role geopolitics plays in oil markets—not only by shaping sentiment and flat prices, but also by redirecting cargo flows and overshadowing economic considerations. From Venezuela, to Iran, and now India’s trade deal, oil pricing has become increasingly detached from underlying balances.

With prolonged supply disruptions linked to CPC Blend production and loading issues, alongside weather-related outages in the US and Algeria and lower Venezuelan output following the earlier US blockade, our global crude oil and condensate balance for January has tightened sharply, from around 2 mbd of oversupply projected last year to about 1 mbd. As some supply-side constraints gradually ease, the average supply surplus is expected to widen to around 2.2 mbd in the first quarter.

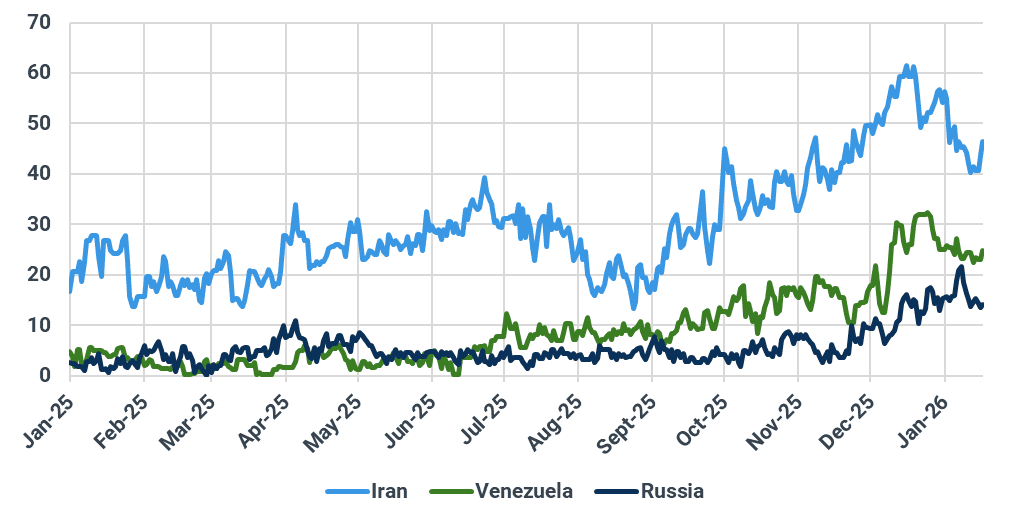

Indeed, we should not lose sight of barrels that fail to reach the commercial market due to sanctions—namely Iranian and Russian crude, as Venezuelan oil has largely returned to commercial channels following recent US actions. Kpler data shows Iranian floating storage currently stands at around 45 mb, down sharply from a peak of 61 mb in early January, though still double the level seen over the same period last year. Meanwhile, Russian floaters have hovered near 15 mb in recent days, easing from about 21 mb in late January. That said, these unsold sanctioned barrels account for roughly 200–300 kbd in the headline surplus but have limited impact on benchmark prices and spot market dynamics.

Iranian, Venezuelan, Russian crude oil floating storage, mb

Source: Kpler

Taking China’s stockbuilding into account, the remaining supply overhang would narrow further. Market chatter suggests the country aims to add around 140–160 mb over a 12-month period, or roughly 100 mb over nine months, ending in March 2026—equivalent to about 360–380 kbd. While Kpler cannot independently confirm the mandate, our data shows that China’s onshore inventories, including both commercial stocks and the SPR, rose by around 120 mb between April 2025 and January 2026, roughly 392 kbd.

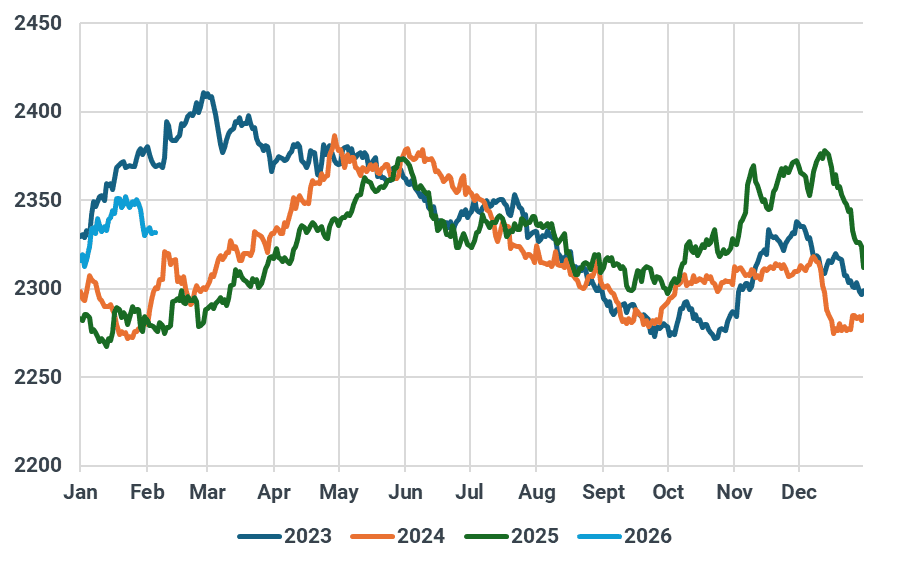

However, excluding Iranian, Russian, and Venezuelan crude—given that sizable volumes shipped before January remain sitting on the water in Asia—global oil on water now stands at around 900 mb. This is down sharply from a peak of about 995 mb in November, but still above levels seen over the same period in 2025, reflecting rising output from Middle Eastern OPEC+ producers.

Meanwhile, global ex-China onshore inventories also built in January and are expected to rise further over the next two months, as refineries in the US and Europe enter a heavy maintenance season. That said, while the effective supply surplus reflected in market-accessible barrels may be smaller than headline figures—likely around 1.5–1.6 mbd in Q1—it still points to a notable oversupply and would continue to weigh on oil prices, pressures that have recently been masked by fears of a potential military conflict between the US and Iran.

Global ex-China onshore crude oil inventory, mb

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler