Rosneft and Lukoil sanctions are live: how India, China and Turkey adapt rather than exit

Russian crude exports face a sanctions-induced crossroad as its market pivots, with demand from key importers, including India, China, and Turkey, falling strongly in late November.

Executive summary

Following the US Treasury’s 23 October announcement of sanctions on Rosneft and Lukoil, the 21 November wind-down deadline has now passed. Based on recent observations, since the announcement of the sanctions, a visible but temporary reduction in Indian, Chinese and Turkish imports is likely as flows reorganise.

Unless more expansive secondary sanctions are introduced, India and China will continue to buy Russian oil. The reasons are multiple: the geopolitical and economic dimensions are both essential. Political leaders from China, India and Turkey, will not want to be seen as bending down to US sanctions. At the same time, Russian barrels remain highly cost-competitive, and workarounds to maintain flows are likely to emerge. In particular, buyers may increasingly pivot to non-sanctioned Russian entities and opaque trading channels.

Market & Trading Calls

- Russian differentials to face wider discounts vs Dubai/NSD as Rosneft/Lukoil supply is rerouted through second-tier sellers and opaque structures. The already wide discount of more than $22/bbl for Urals to NSD for FOB Med/Baltic cargoes, >$6/bbl Urals DES India and >$4/bbl ESPO DES Shandong (Argus Media) are likely to remain elevated or widen intermittently.

- Mildly bullish time spreads and flat price as a temporary 1.2–1.4 mbd disruption is possible in the short-term.

- Russia-India: 800 kbd at risk in the short-term. Indian refiners are pivoting to non-designated Russian entities, opaque trading channels, and alternative suppliers across the Middle East, West Africa, and the Americas. Complex logistics, STS transfers near Mumbai, and mid-voyage diversions underscore Russia’s adaptive response. As long as broader secondary sanctions are not enforced, India will continue importing Russian barrels, albeit through increasingly indirect and less transparent means.

- Russia-China: 300-400 kbd at risk in the short-term. Independent refiners require fresh quotas and sharp discounts in the medium-term to return to sourcing Russian barrels. However, state-owned companies are generally conservative on sanctions risk. Sharp Russian grade differentials will be required to entice Chinese buying again. Pipeline imports are unlikely to decrease due to energy security concerns.

- Russia-Turkey: 180 kbd at risk in the short-term. Tupras and SOCAR are likely to act cautiously: sourcing barrels from non-sanctioned Russian entities while reassessing the trade-off between using cheap Russian feedstock. The decision to prioritise access to the EU product market or access to cheap Russian barrels will determine future flows into Turkey.

The geopolitical lens

With the new sanctions on Rosneft and Lukoil coming into force today after the 30-day wind-down period, there is little reason to expect major demand-side shifts from China, India, or Turkey. For both geopolitical and economic reasons, these countries will continue buying Russian crude. Their economies rely on affordable barrels, and none of these governments are inclined to let Western sanctions dictate their energy security choices.

That said, the form of their engagement with Russian supply is likely to evolve. Governments in all three countries will nudge their refiners to minimise visible exposure. They won’t want their state-owned or flagship refiners buying directly from Rosneft or Lukoil if that creates compliance or reputational risk. The workaround is simple and already well-tested: continue buying Russian crude, but through intermediaries. If the barrels are supplied via third-party trading entities, entities that can credibly show they are not Rosneft/Lukoil, then refiners can keep accessing discounted supply while limiting the appearance of sanctionable contact. This is a trend that has already started with new sellers emerging such as Tatneft, RusExport, MorExport or Alghaf Marine DMCC (see Middle East-Asia-Russia section of this month's Crude Oil Barrel report).

The new structure not only preserves their flows, but it also benefits the buyers. The sanctions have already pressured Russian prices downward, and a shift to more opaque, intermediated transactions will likely deepen those discounts. As long as Moscow reorganises its export apparatus quickly, i.e., it gets its house in order so Rosneft and Lukoil are not the named suppliers, these three markets stand to enjoy better margins. It will take a couple of months for the supply chain to reorganise itself, but it probably will, eventually.

There is also a clear political dimension. Xi, Modi, and Erdoğan all cultivate an image of strong, autonomous global leaders. None of them will want to be seen as publicly aligning with a US-led sanctions regime.

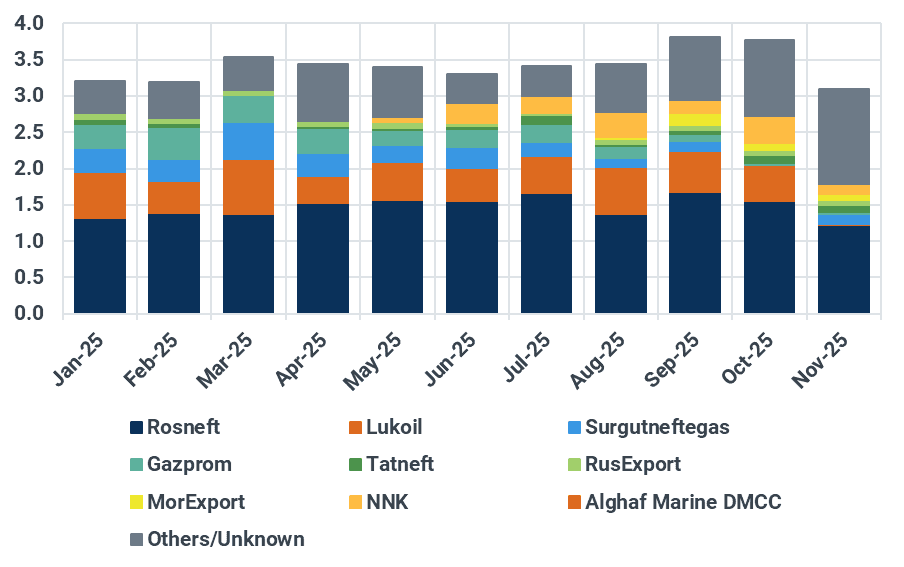

New sellers emerge as Moscow reorganises its supply chain

In the short term, Russian oil discharges are likely to dip as Rosneft- and Lukoil-linked barrels are temporarily sidelined during the market’s adjustment phase. We believe that in an extreme case, 1.2–1.4 Mbd of flows could be at risk while buyers, traders, and shippers reassess exposure. However, this disruption should prove temporary. As alternative sellers such as Tatneft, Rusexport, Morexport, and Alghaf Marine expand their trading footprint and take over the commercial role previously played by Rosneft and Lukoil. Russia’s exports should largely re-normalise, with volumes gradually reappearing through these new channels. The structure will become more intermediated, but the barrels will still find their way to market.

Russia seaborne oil exports by sellers, Mbd

Source: Kpler

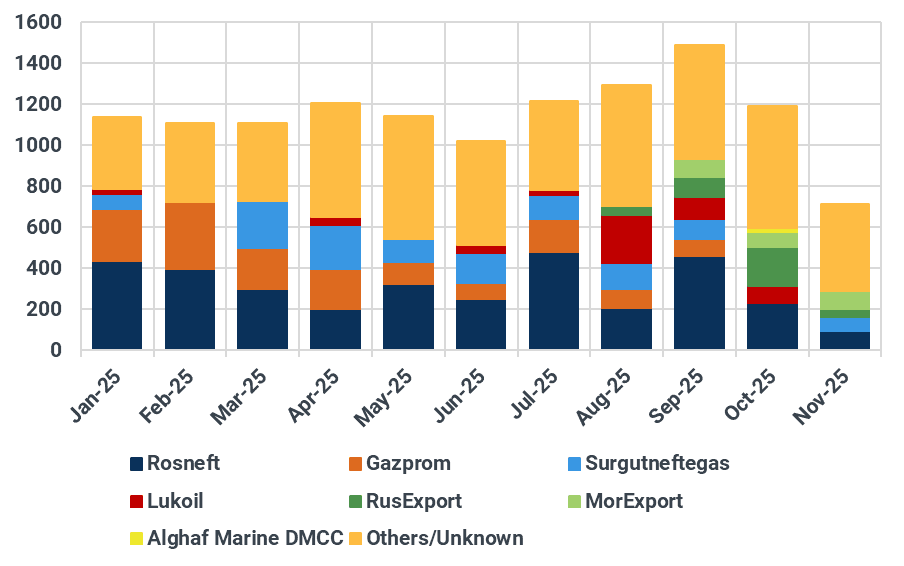

Impact on Russian crude flows to India

Before the 21 November wind-down deadline, India’s crude imports from Russia have remained very strong (around 1.8–1.9 Mbd) as refiners continued to prioritise the most economical barrels ahead of the sanctions’ cutoff. After today's deadline, flows are likely to decline noticeably in the near term, because of the uncertainty and perceived risk related to sourcing barrels from Rosneft or Lukoil. Based on our current understanding, no Indian refiner other than Nayara’s already-sanctioned Vadinar facility is likely to take the risk of dealing with OFAC-designated entities, and buyers will need time to configure contracts, routing, ownership structures, and payment channels.

With crude linked to these entities now effectively treated as a “sanctioned molecule,” Indian refiners (aside from Nayara) are expected to pause direct purchases after 21 November. As a result, a noticeable drop in Russian crude flows to India in the near term is likely, particularly through December and January. Loadings have already slowed since 21 October, though it is still early for definitive conclusions given Russia’s agility in deploying intermediaries, shadow fleets, and workaround financing.

Refiners will likely proceed more cautiously, relying on unsanctioned traders, blended barrels, and more complex logistics to minimise OFAC exposure. Russian supply will not disappear but will increasingly move through opaque channels.

Recent tanker activity suggests a notable shift in Russian crude trading behaviour, marked by mid-voyage diversions between India and China and Ship-to-Ship (STS) transfers at unusual locations such as off Mumbai’s coast, far from the typical transfer zones near the Singapore Strait.

Does India receive crude from other, non-sanctioned Russian companies, and can these producers legally step in to replace the sanctioned volumes? Yes, India does receive Russian crude from suppliers other than Rosneft and Lukoil, and those flows remain legal, for now. The sanctions announced by the U.S. target specific companies (Rosneft, Lukoil, and their majority-owned subsidiaries), not all Russian oil or all Russian producers. This means that crude supplied by non-designated Russian entities or independent traders using non-sanctioned intermediaries can still be legally purchased by Indian refiners, as long as no sanctioned entity, vessel, bank, or service provider is involved.

In other words, Russian oil itself is not sanctioned; the suppliers are. That is why non-designated producers can legally step in to fill part of the gap created by the Rosneft/Lukoil restrictions.

However, there are two important caveats:

- Operational risk rises, even for non-sanctioned suppliers, because OFAC can expand designations, and traders/banks/insurers may reduce exposure to avoid secondary sanctions.

- Volumes may not fully replace Rosneft/Lukoil barrels in the near term, since those two dominate Russia’s export blend slate and logistics.

Therefore, non-sanctioned Russian producers can fill the breach, but not perfectly and not without risk, especially if Western pressure increases or sanctions widen beyond specific entities

In the longer term, the trajectory will depend on how strictly santions are being enforced and secondary sanctions are being introduced. Tighter enforcement would suppress volumes further, while lighter-touch implementation could allow some recovery through intermediaries.

Some Indian refineries are very complex in setup, so replacing Russian volumes does not have any technical impact; it will only reduce margins for some. To compensate for softer near-term Russian arrivals, Indian refiners are expected to increase intake from a broader mix of suppliers, including from the Middle East (Saudi Arabia, Iraq, UAE, Kuwait), Brazil and broader Latin America (Argentina, Colombia, Guyana), West Africa , North America (U.S., Canada). Freight costs on long-haul routes will cap substitution potential, but the overall import basket is likely to widen.

Russian oil exports to India by sellers, kbd

Source: Kpler

Impact on Russian crude flows to China

The decline of Russian loadings comes amid lower exports to other countries, including China and Turkey, where flows are trending well below the levels seen in previous months. Russian seaborne loadings of crude and condensate to China are currently averaging less than 800 kbd, which represents a decline of around 400-500 kbd month-on-month and would mark the lowest level since February 2022.

While some of this decline can be attributed to higher freight rates, bad weather restricting loadings, and lower import quotas, Chinese refiners remain cautious. This includes independent refiners, with total seaborne exports of Russian crude to Shandong averaging ~600 kbd so far this month, which would represent the lowest level since July 2024.

Chinese independent refiners are awaiting fresh import quota allocations for the new year to resume purchases of barrels from multiple sanctioned sources (Iran and Venezuela included). State-owned Chinese refiners are treading more cautiously and could take the lead from how Indian state-owned refiners proceed with sourcing Russian barrels once logistical workarounds are found and the ‘dust settles’ on these current sanctions.

Nonetheless, Chinese refiners have significant optionality with open arbitrages for West of Suez grades flowing East, suggesting that a clear lack of sanctions enforcement and continued sharp Russian grade discounts would be needed to boost flows to state-owned entities in the medium term.

China also imports ~800 kbd of Russian crude via the ESPO and the Kazakhstan-China pipeline. While seaborne imports are likely to decrease in the short-term, piped imports are unlikely to decrease due to energy security concerns as the oil feeds China's northwestern regions, where refineries would have to stop activity if imports are stopped.

Russian oil exports to China by sellers, kbd

Source: Kpler

Impact on Russian crude flows to Turkey

Just like Indian and Chinese refiners, both Tupras and SOCAR will stay on the cautious side in the short-term and look for cargoes that are supplied by non-sanctioned Russian companies. Three shipments are currently headed to Turkey and will arrive after the 21 November deadline. Two of them are being sold by Tatneft and the third one by Rusvietpetro.

With the clarification around the product stipulations involved in the EU's 18th sanctions package, both Tupras and SOCAR need to decide whether to prioritise access to the EU products market or to continue benefitting from high margins due to cheap Russian barrels. With Russian FOB Urals trading at a >$22/bbl discount to NSD (Argus Media), and Turkish gasoil exports declining, refiners may selectively absorb Rosneft or Lukoil barrels. However, they are more likely to buy crude from non-sanctioned entities in the short-term, given what we have seen in the most recent data (see below).

Russian oil exports to Turkey by sellers, kbd

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Kpler Insight: Get the analysis that matters

.jpg)