Tariffs and macro risks recalibrate crude demand down by 200 kbd for remainder of 2025

Executive Summary

Americas:

- Bullish on Argentina's light-sweet supply, with output in the Vaca Muerta hovering at record highs. Rising output has helped lift exports to multi-month highs, with recent pipeline capacity expansions incentivizing further production growth in the years ahead.

- Bearish on Venezuelan crude exports, which have dropped to a 6-month low in March as PDVSA revoked multiple crude loading authorizations, tightening US heavy crude markets in Latin America and Canada.

- Bullish on WCS Hardisty differentials amid a restart of the Keystone pipeline, with uncertainty surrounding Venezuelan crude flows keeping exports via the TMX pipeline at record highs.

Atlantic Basin:

- Bullish on Norwegian crude supply with Johan Sverdrup and Johan Castberg output to remain steady

- Bearish on Russian flows as lower OSPs and Indian monsoon season may weigh on exports through Q2

- Neutral on European sour crude imports with weaker economic activity being offset by Buzzard outage over the summer

Middle East and Asia:

- Bearish on Middle Eastern June OSPs amid OPEC+ crude supply in May/June, depressed Singapore product cracks, and the goal to regain market share in Asia

- Bearish on Asian buying of CPC Blend as pricing of light sour Murban becomes more competitive

- Bearish on Iranian crude exports despite nuclear talks happening between US and Iranian envoys on Saturday

Highlights

S&D highlights

Our latest revisions incorporate the impact of US tariffs and the US-China trade war on oil demand. These point to a looser crude market outlook, with the 2025 balance shifting from a mild deficit (-6 kbd) to a surplus of +273 kbd.

On the demand side, China’s crude intake was revised down by an average of 160 kbd through July, reflecting peak maintenance and softer refining sentiment amid rising trade tensions. South Korean refinery runs were reduced by 160–200 kbd in March–April due to a mix of planned and unplanned outages.

Elsewhere, Singapore demand was lifted by 180 kbd in May as expected maintenance was deferred, while Canadian and Russian runs were revised higher in line with updated maintenance schedules. U.S. crude demand remains largely unchanged.

Russian supply was revised down by nearly 100 kbd from March as the country implements additional OPEC+ compensation cuts. Ecuador saw a ~80 kbd decline after a pipeline rupture forced a shutdown and widespread production halts. Iraqi output was lowered by 70 kbd in March amid falling exports and reduced direct crude burns.

In contrast, Libya’s supply was revised up by nearly 110 kbd on the back of strong export flows. Saudi and UAE output revisions were mixed: March and April saw modest downward adjustments, but both are expected to increase production from May as OPEC+ accelerates its phased unwind. Venezuela’s supply outlook improved slightly following an extension granted to Chevron, with average output revised up by 60 kbd in Q2–Q4, though a year-end decline remains likely.

Global crude and condensate balances, kbd

Source: Kpler

Crude production revisions March 2025:

- Russia output has been revised down by nearly 100 kbd from March onward, reflecting expectations of additional reductions under the country’s updated compensation cut commitments

- Ecuador supply was revised down by approximately 80 kbd in March following the temporary shutdown of the SOTE pipeline. A landslide on 13 March ruptured the line, spilling around 3,800 bbl of crude. Petroecuador subsequently declared force majeure, halted operations, and shut in production. Several private and international producers also suspended output

- Libya output has been revised up by nearly 110 kbd in 2025, supported by strong crude export flows in recent months and reinforced by our negative balancing factor, indicating higher production levels

- Iraq crude production for March has been revised down by approximately 70 kbd, driven by lower-than-expected direct crude burns, as confirmed by official data, and a 190 kbd m/m decline in crude exports last month, while refinery runs remained stable

- Saudi Arabia output was revised down by 20 kbd in March and 40 kbd in April, but increased by 120 kbd for both May and June, reflecting expectations of higher production as OPEC+ moves to accelerate the unwinding of voluntary cuts

- UAE crude supply was revised down by 65 kbd in March, aligning with official data. Looking ahead, output is projected to increase by 40 kbd in May and 70 kbd in June, as the country accelerates its incremental additions to the market

- Venezuela production has been revised up by an average of 60 kbd from Q2 through Q4, following the extension granted to Chevron—currently producing around 220 kbd—to continue operations until 27 May (previously set to expire on 1 April). As a result, our base case now assumes a total production decline of 180 kbd by year-end

Production revisions, kbd

Source: Kpler

Refinery crude demand revisions March 2025:

- China crude demand has been revised down by an average of 160 kbd from February through July, with the spring maintenance season peaking in May as nearly 2.1 mbd of refining capacity goes offline. Going forward, crude demand expectations remain muted amid escalating Sino-US trade tensions, which should weigh on oil demand and drive refiners to reassess operational strategies despite Beijing’s signals of future economic stimulus

- Canada refinery runs have been adjusted up by 110 kbd in March and 90 kbd in April, reflecting alignment with official weekly data and updated maintenance schedules

- Greece crude intake was lowered by an average of 60 kbd from March through August, driven by ongoing maintenance at the Elefsina refinery, which began in March and is expected to continue through July. Further downward pressure stems from the delayed restart of MOH Corinth’s 140 kbd CDU, which has been offline since September. As a result, Greece’s available refining capacity is estimated at around 300 kbd for Q2 compared to a total nameplate capacity of 530 kbd

- South Korea refinery throughput was revised down by 160 kbd in March due to major planned maintenance, with roughly 500 kbd of capacity offline. April runs were lowered by an additional 200 kbd following unplanned maintenance at S-Oil’s Onsan refinery, where the 170 kbd Vacuum Distillation unit was offline during the first half of the month. These revisions are also corroborated by continued crude inventory builds observed across both March and April

- Singapore crude demand was increased in April and by 180 kbd in May, returning to normal levels as the ExxonMobil PAC refinery is no longer expected to undergo maintenance next month, as opposed to earlier projections

- Russia refinery runs were increased by 70 kbd in May and 100 kbd in June, as most downstream units are expected to complete spring maintenance and return online in the upcoming weeks

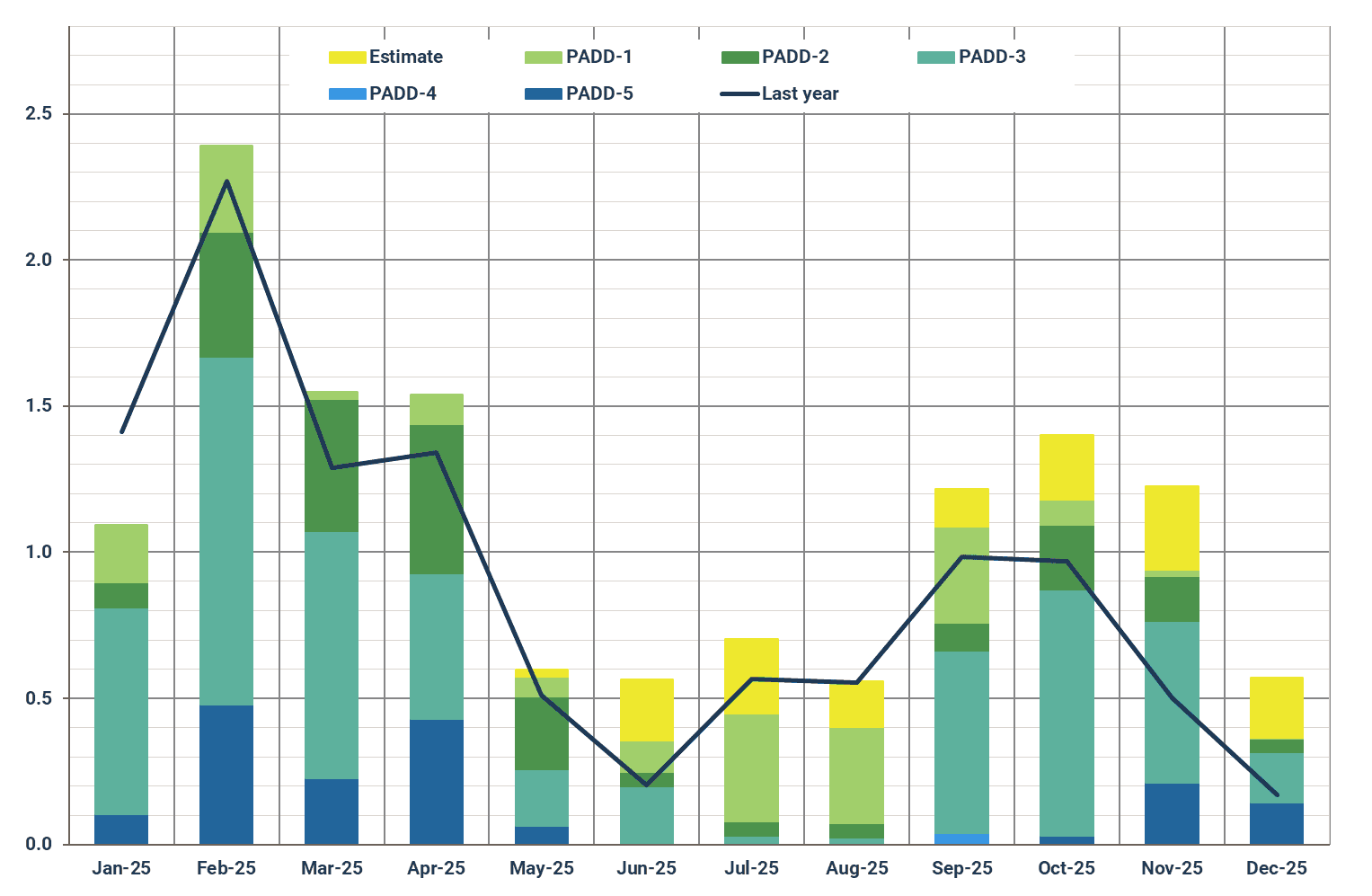

- US refinery throughput was revised from Q2 through Q4 2025, following alignment of PADD-level runs with planned maintenance schedules, refinery closures, and seasonal patterns. Overall, crude demand remains largely unchanged, with only a marginal downward revision of 15 kbd over the period

Global refining maintenance & outages, kbd

North West Europe refining maintenance & outages, kbd

Russia refining maintenance & outages, kbd

Asia Pacific refining maintenance & outages, kbd

US refinery maintenance & outages by PADD, Mbd

Source: Kpler estimates based on various industry and media sources

Chart of the Month

While Q1 crude demand revisions were relatively modest at -125 kbd, our outlook for the rest of 2025 has deteriorated. We now see global demand lower by an average of 204 kbd from April through December, reflecting macro headwinds and geopolitical uncertainty.

The upcoming U.S. “Liberation Day" tariffs have added fresh downside risks. While the 90-day delay suggests the move may serve as a negotiating tool to address the U.S. trade deficit, the broader implications are clear: weaker sentiment, delayed industrial projects, and reduced travel activity are expected to weigh on refined product demand.

In line with this, we’ve revised down our GDP forecasts for the U.S. and key Asian economies. China remains an exception, where we still expect the government to meet its 5% growth target, but even there, oil demand is taking a hit. Overall, we’ve lowered our 2025 global products demand growth forecast by 295 kbd to 502 kbd y/y.

Asia accounts for the largest share of the downward revision, led by China (-60 kbd), South Korea (-39 kbd), and India (-30 kbd), highlighting the region’s sensitivity to both economic policy shifts and external trade pressures.

Crude demand revisions for April-December 2025, kbd

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions - backed by the most accurate oil price predictions two years running.

Unbiased. Data-driven. Essential.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data