China gas supply strength caps LNG demand growth

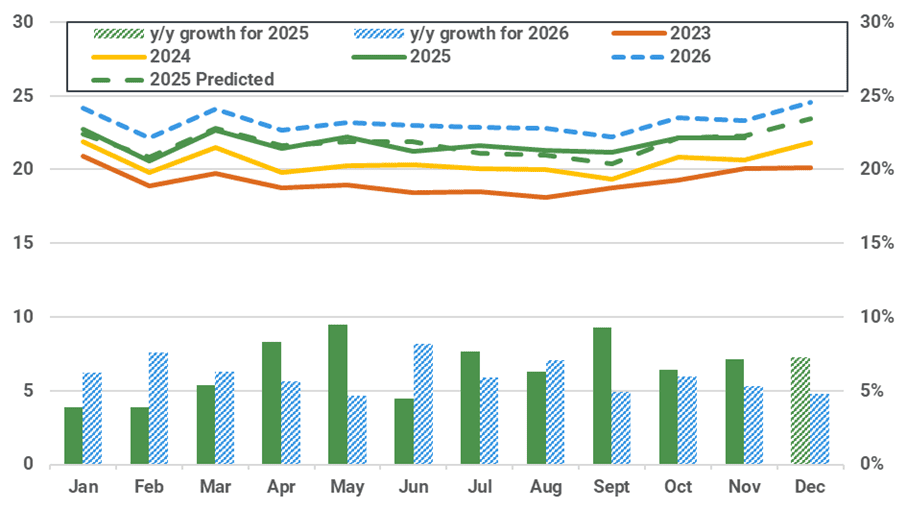

China finalised NBS data show continued strength in domestic gas production, with November output rising 7.1% y/y to 22.1 bcm, driven by faster-than-expected shale gas ramp-ups in the Sichuan Basin. Kpler Insight expects China’s total gas production to reach 263 bcm in 2025, largely in line with the14th Five Year Plan targets. Production is expected to increase further to 278.5 bcm in 2026, as stronger policy support from the 15th Five Year Plan proposal is likely to accelerate unconventional gas growth in Sichuan and Shanxi. Meanwhile, pipeline gas imports are expected to grow only marginally, constrained by limited new Russian capacity ramp-ups before 2027 and weaker flows from Central Asia. As stronger domestic gas supply largely offsets limited pipeline import growth, Kpler Insight has revised China 2026 LNG demand down by 0.6 mt to 73.9 mt, adding mild bearish pressure to Asian LNG spot prices in Q2-Q4 2026.

Market & Trading Calls:

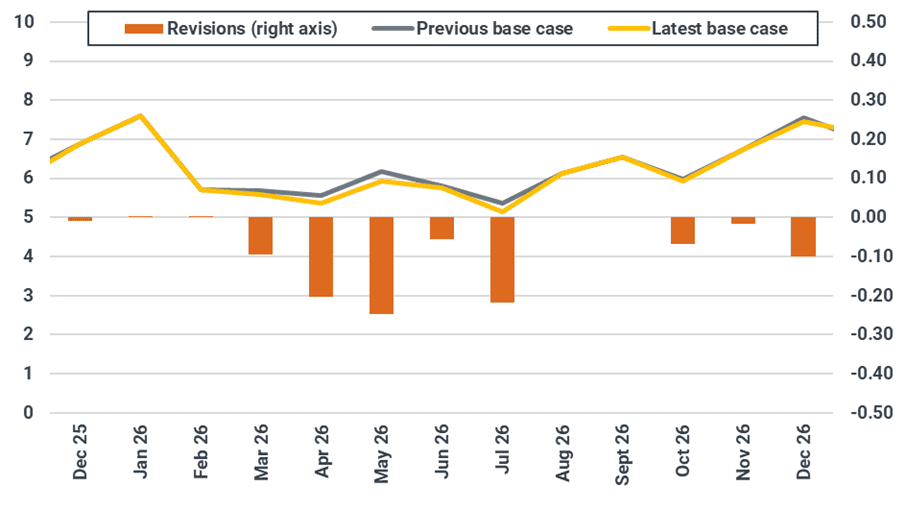

- China LNG demand: Decrease in 2026, as upward revisions to gas production in Sichuan and Shanxi largely offset the limited increase in pipeline imports, displacing around 0.6 mt of LNG demand in Q2–Q4 2026 and cutting the demand outlook to 73.9 mt.

- Asian LNG spot prices: Slightly bearish Q2-Q4, as downward demand revision is mainly concentrated during these periods.

Finalised data from China’s National Bureau of Statistics (NBS) confirm that domestic natural gas production rose 7.1% y/y in November to 22.1 bcm, slightly above the preliminary data. The stronger growth was primarily driven by higher-than-expected production in the Sichuan Basin, reflecting continued ramp-ups at PetroChina’s and Sinopec’s shale gas fields.

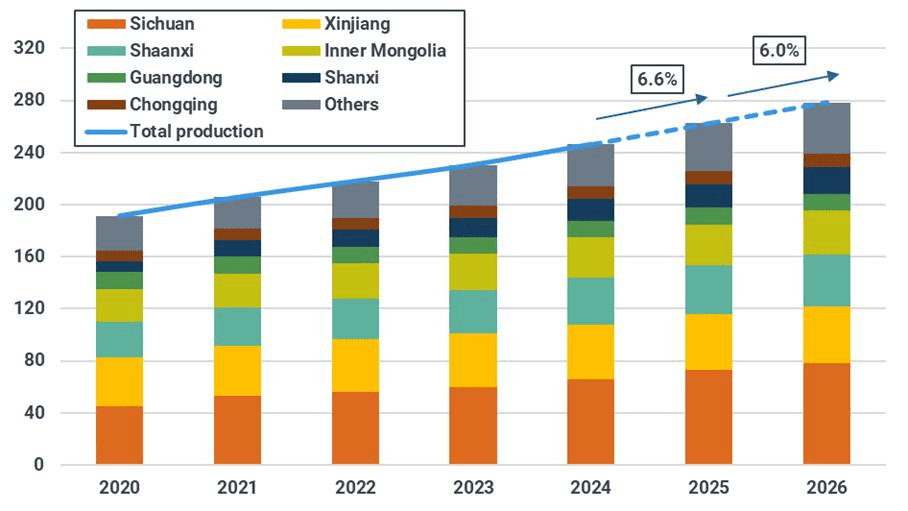

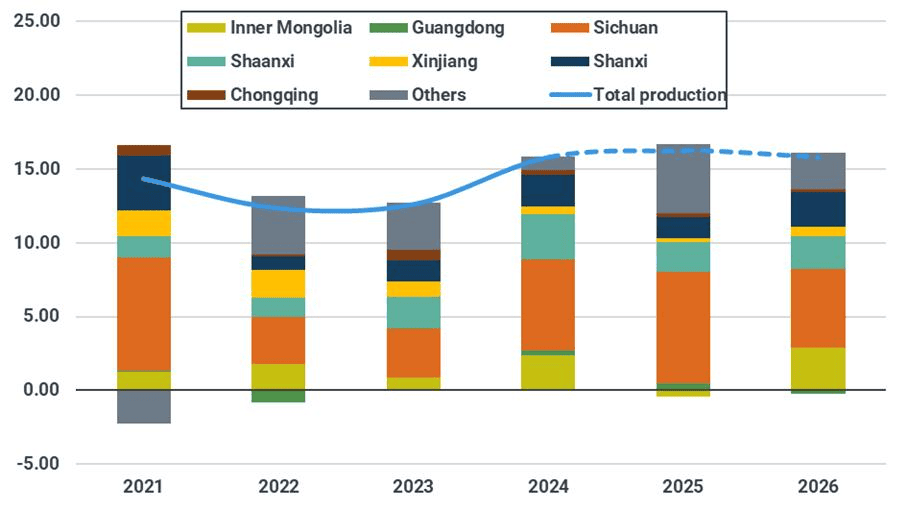

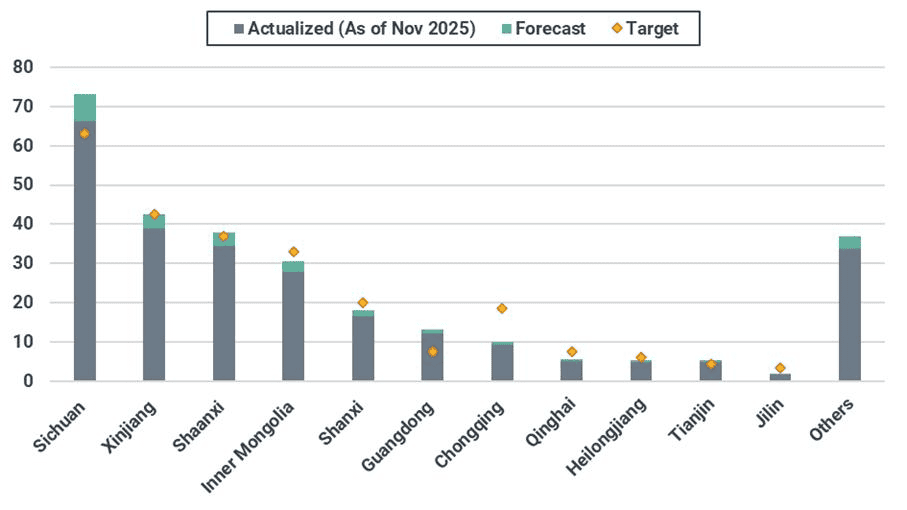

For 2025, Kpler Insight expects China’s national gas production to reach 263 bcm, up 16 bcm y/y and in line with previous estimates. Growth is mainly led by Sichuan (+7.5 bcm y/y), Shaanxi (+2.0 bcm) and Shanxi (+1.5 bcm), reflecting accelerated production of shale gas in Sichuan Basin and tight gas and coalbed methane in Shaanxi and Shanxi. Combined output from the Sichuan–Chongqing region is estimated at 83.3 bcm, exceeding the regional 14th Five-Year Plan (FYP) target of 82 bcm by 1.3 bcm. This is supported by rapid local shale gas development and the completion of the first section of the Sichuan East Gas Pipeline II, enabling more Sichuan gas for domestic consumption. Production in other provinces is expected to broadly align with respective targets.

Looking ahead, preliminary guidelines under China’s 15th FYP continue to emphasize “increase reserves, ramp up production” across most gas-producing provinces. Sichuan’s 15th FYP proposal points to continued efforts to develop a national shale gas base, while Shanxi maintains its focus on coalbed methane utilization. Although specific provincial gas production targets will only be finalized and disclosed in Q1 2026, the stronger policy focus on domestic energy self-reliance has prompted Kpler Insight to revise up its 2026 gas production forecast to 278.5 bcm, up 15.8 bcm or 6% y/y. The increase is driven by higher ramp-ups in unconventional gas in Sichuan (+5.4 bcm y/y), Shaanxi (+2.2 bcm) and Shanxi (+2.4 bcm), following Chinese New Year as industrial activity restarts beyond Q1 2026.

China monthly LNG demand latest forecast against previous forecast (mt)

Source: Kpler Insight

China monthly gas production forecast and year on year growth (LHS bcm, RHS %)

Source: NBS, Kpler Insight

China annual domestic gas production level by major province (bcm)

Source: NBS, Kpler Insight. Note: 2025-2026 are forecasts.

China annual domestic gas production y/y changes by major province (bcm

Source: NBS, Kpler Insight. Note: 2025-2026 are forecasts.

14th Five-Year gas production targets and forecast by province (Bcm)

Source: State Council of China, NBS, Kpler Insight

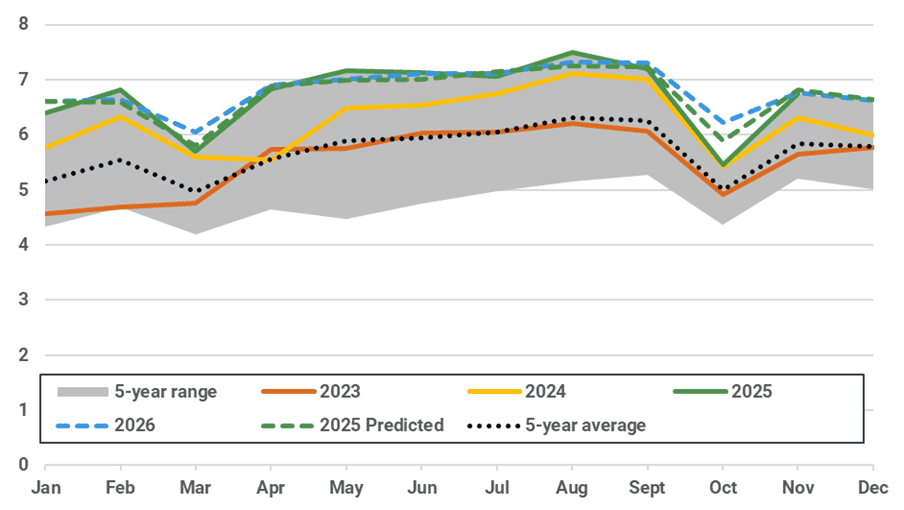

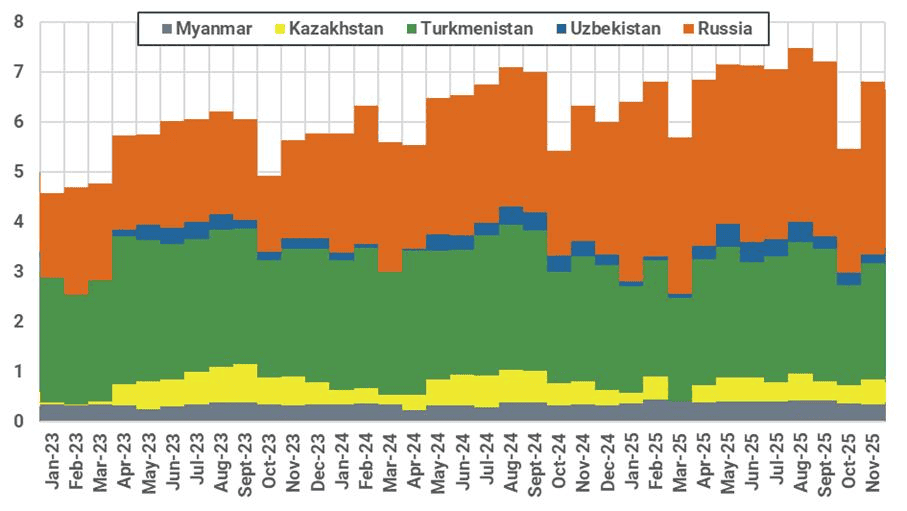

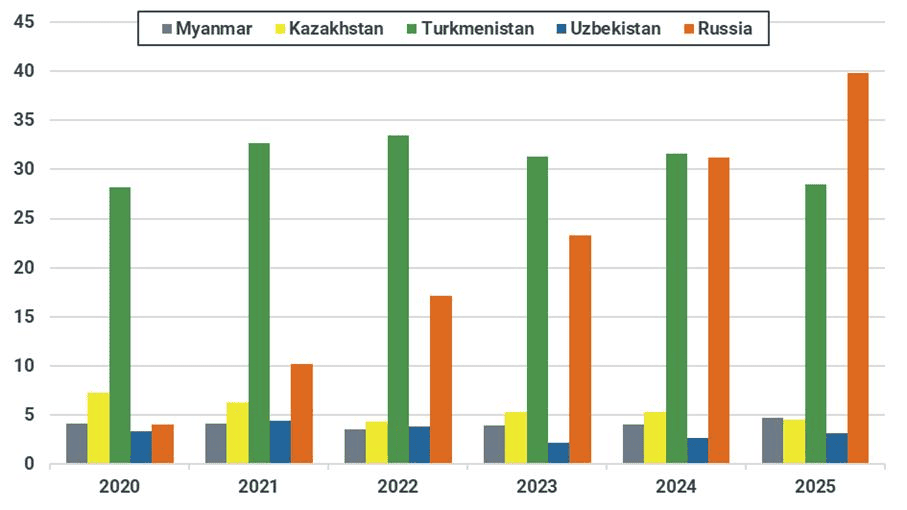

Finalised November Customs data show China imported 5 mt (6.8 bcm) of pipeline gas, up 0.5 bcm y/y. Russia’s Power of Siberia 1 (PoS 1) led imports at an estimated 3.5 bcm, up 0.8 bcm y/y, while Central Asian flows declined by around 0.3 bcm as exporters such as Kazakhstan and Turkmenistan diverted more gas to meet rising domestic demand, in line with our previous expectations.

For 2025, China’s pipeline gas imports are expected to reach 80.7 bcm, up 5.8 bcm or 8% y/y. Imports from Russia are projected to rise to 39.2 bcm, up ~8 bcm y/y, driven by the continued ramp-up of PoS 1. Myanmar pipeline supplies are expected to increase to 4.8 bcm, up 0.8 bcm y/y. In contrast, imports from Central Asia are forecast at 36 bcm, down 4 bcm y/y, as higher domestic demand in exporting countries diverts gas away for local consumption.

Looking ahead, Central Asian countries such as Kazakhstan and Turkmenistan continue to prioritize domestic energy security in 2026, keeping downward pressure on pipeline exports to China. Russian pipeline imports via PoS 1 have largely ramped up, while additional volumes from further ramp-ups or the Far East pipeline are unlikely to materialise before 2027, leaving limited headroom for further growth. Myanmar’s pipeline gas supply is expected to remain broadly stable y/y, as its main source, offshore Shwe gas field, is unaffected by Myanmar–Thailand border conflicts. Overall, Kpler Insight expects China’s pipeline gas imports to reach 81.7 bcm in 2026, marginally up 1 bcm y/y.

As upward revision in domestic gas production largely offsets the limited increase in pipeline imports, Kpler Insight has revised China’s 2026 LNG demand outlook down by 0.6 mt to 73.9 mt. The downward revision is mainly concentrated in Q2–Q4 2026, adding bearish pressure to prices during these periods.

China’s pipeline gas imports by month (bcm)

Source: China Customs, Kpler Insight

Estimated China pipeline monthly gas imports by country (bcm)

Source: China Customs, Kpler Insight *Note: Data from 2022/1/1 onwards are Kpler Insight estimates, as China Customs stopped publishing pipeline gas import volumes by country.

Estimated China pipeline gas imports by country between 2020 – 2025 (bcm)

Source: China Customs, Kpler Insight *Note: Data from 2022 onwards are Kpler Insight estimates, as China Customs stopped publishing pipeline gas import volumes by country.

See why the most successful traders and shipping experts use Kpler

Kpler Insight: Get the analysis that matters