East/West divergence to deepen into Q1

Market & Trading Calls

LPG:

- West of Suez: We decreased our outlook for Mont Belvieu and NWE propane beginning in Q2 2026, as US production has beaten our high expectations and US-China normalization appears unlikely before H2 2026, keeping pressure on prices in the West. For butane, we made more minor adjustments, decreasing our spring 2026 Mont Belvieu outlook amidst strong US production and upcoming Middle East Supply.

- East of Suez: We lowered our Far East propane outlook modestly beginning Q2 2026 as extended US-China trade disruption means plentiful US supply for Japan and South Korea where demand prospects are weak. We also decreased our Middle East outlook for propane and butane for spring 2026 as increasing regional supply and a strategy to defend market share will offset growing cylinder demand in the East.

Naphtha:

- We nudged our January 2026 NWE crack forecast higher m/m to show a smooth backwardation through the curve, but West of Suez cracks will only find support from export demand in Q1 and for much of 2026 as cracking, blending demand continue to soften.

- We moved December to February Singapore crack slightly higher m/m as attacks on Russian refineries continue. Asian cracks will find support in H1 2026 from China’s rising import requirements, lingering refinery maintenance in the Middle East and only a slow recovery in Russian output.

- E/W spread will remain above seasonal norms and year-ago level through Q1 2026, but there is downside risk to our view if operating rates cuts at ex-China crackers deepen more than anticipated.

Gasoline:

- Slightly bearish WoS cracks, as the end of refinery maintenance and easing demand dictate a lengthening of gasoline balances, pressuring cracks.

- Nonetheless, tighter European balances on a y/y basis, depressed US inventories, and pockets of demand in the Atlantic Basin point to stronger than usual cracks going to year-end.

- Bullish EoS cracks, backed by fundamentals pointing to prolonged tightness well into 2026.

- Solid Indonesian buying and depressed Chinese exports continue to support Singapore cracks via limited regional cargo availability, although the recent closing of the transpacific arbitrage will partly offset this.

Middle Distillates:

- EU and sanctions enforcement tightens the barrel: the regulatory backdrop locks in a firm, scarcity-driven start to the year despite somewhat poor demand and seasonally higher stocks.

- Geopolitical downside risk remains material: a genuine easing in Ukraine-Russia tensions would render sanctions concerns moot and rapidly unwind the embedded risk premiums.

- Singapore prices to ease: rising South Korean runs and Chinese refiners adapting to sanctions have softened what had been a tight spot market.

Fuel Oil:

- WoS HSFO markets pressured by weak feedstock demand, ample crude and fuel oil supply.

- Crashing NWE VLSFO cracks poised for reversal on shifting production incentives.

- Optimism builds for Asian VLSFO markets as balances gradually tighten.

- Asian HSFO markets pressured into Q1 by ample supply and limited seasonal demand although record-low Russian exports will limit the downside.

Trades of the Month

- A long NYMEX heating oil position stands out as the best trade. PADD 1 stocks remain chronically below five-year averages and will need to price higher to pull barrels away from NWE just as the EU’s new sanctions come into force and USGC refineries head into Q1 maintenance.

- With gasoline blending waning and petchem demand weak while refineries increase runs post-maintenance, M1 NWE naphtha cracks should moderately soften.

- Cautiously bullish on Asian VLSFO spreads on tightening balances although repeated delays to Malaysia's Pengerang refinery RFCC restart would U-turn upward momentum.

LPG: Growing US length and delayed US-China trade talk dim 2026 outlook

West of Suez

Propane prices rose in the West since our last report as seasonal heating demand picked up and new US export capacity came online. Butane prices climbed in the US amid gasoline blending and export demand, while prices fell modestly in Northwest Europe (NWE) as gasoline tightness eased.

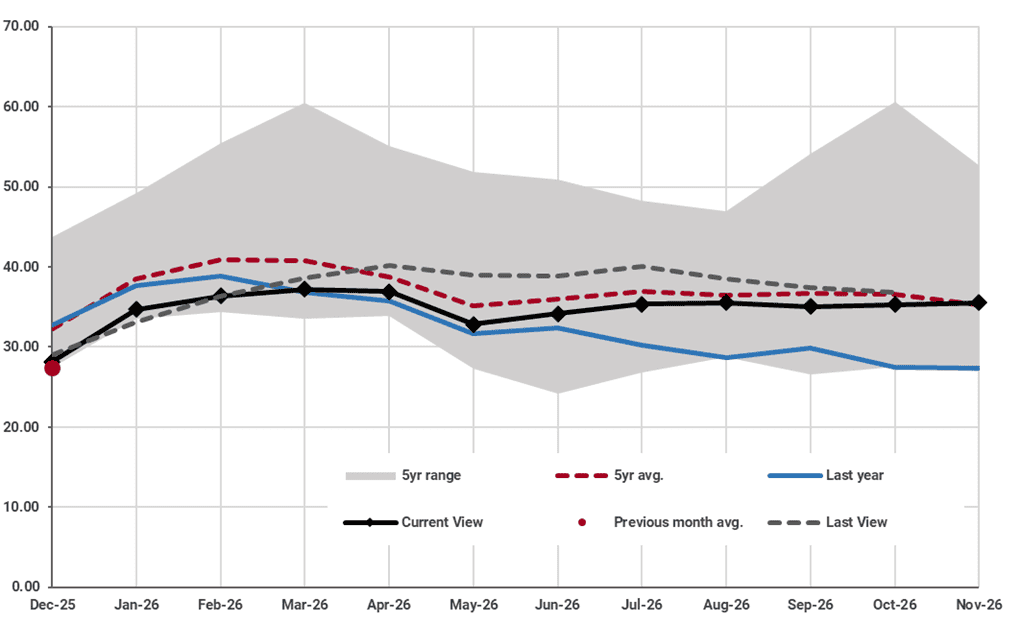

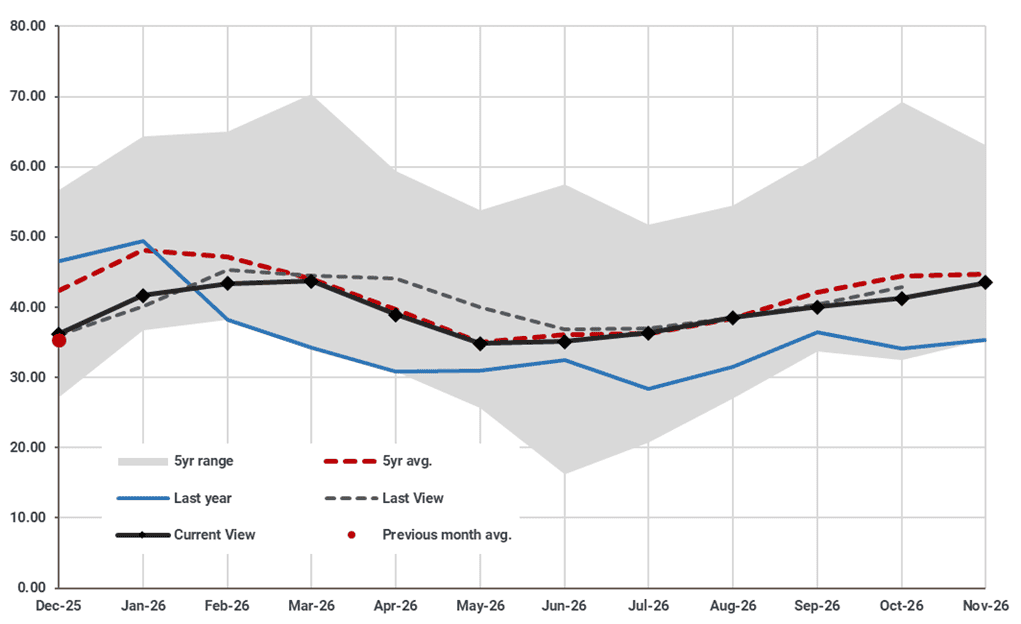

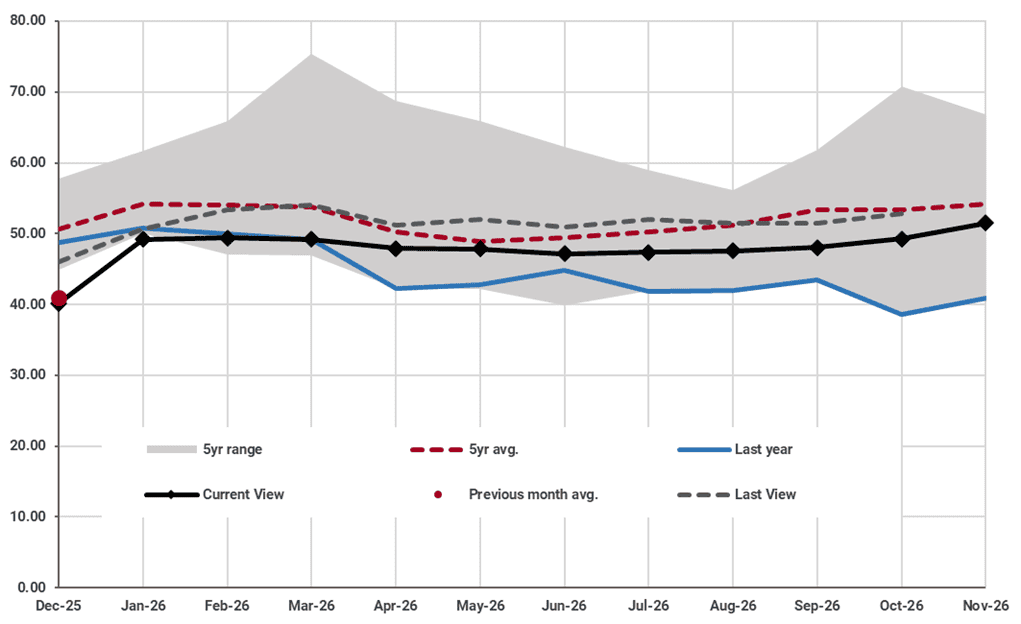

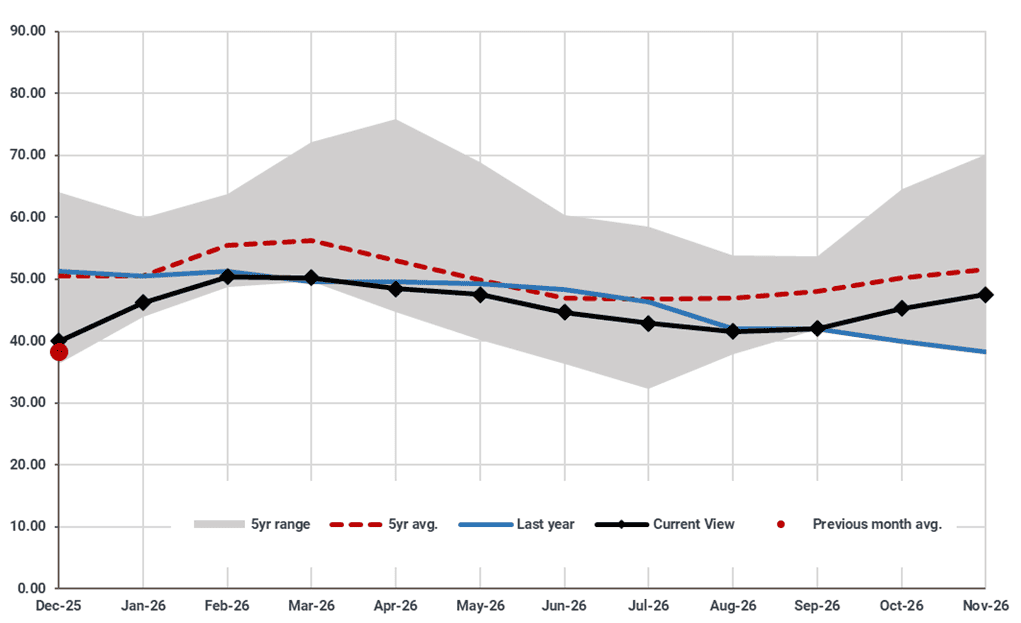

In the US, we decreased our outlook for Mont Belvieu propane beginning in Q2 2026, as higher than expected EIA production data has lengthened 2026 balances. While a new dock starting up at ET Nederland in early November has allowed exports to jump as the facility’s 125 kbd propane expansion comes online, no significant US-China talks are scheduled until April, keeping a lid on US propane exports and USGC prices under pressure. We also decreased our Mont Belvieu butane outlook for mid-2026 amidst strong production growth, but increased contracted volumes to India and strong cylinder and petchem demand elsewhere East of Suez led us to increase our outlook for the next three months.

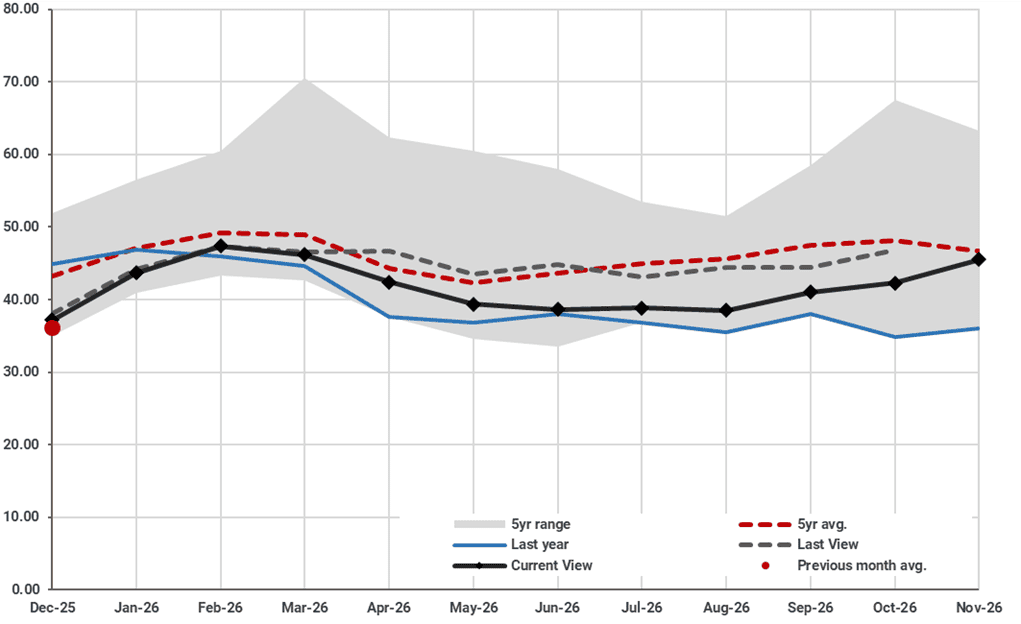

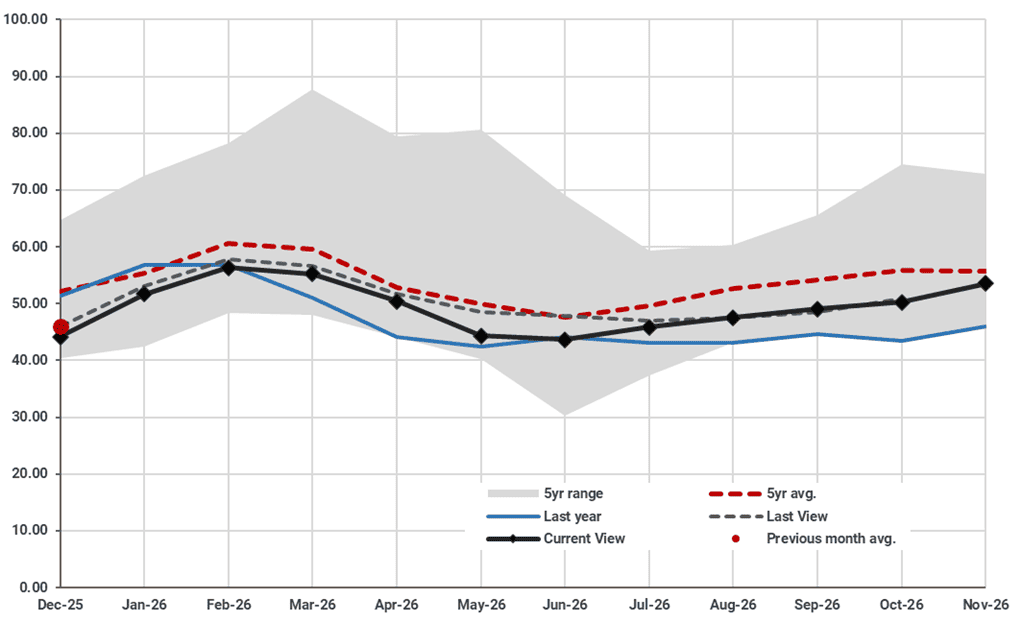

In NWE, we decreased our propane outlook beginning Q2 2026 as Europe will absorb some excess US cargoes at lower prices, and we made only marginal changes to our NWE butane outlook. While maintenance at Norway’s Karsto gas plant has lasted longer than expected, limiting regional LPG supply, natural gas is no longer trading at a premium to LPG which will keep LPG out of the gas stream. Firming LPG prices have helped naphtha steam cracking margins regain advantage versus lighter feeds, but cheap US cargoes combined with maintenance wrapping up at refineries and also at Karsto will add supply and keep LPG competitive among flexi-crackers, preventing petchem demand from dropping further.

Propane Mt Belvieu ($/bbl)

Source: PVM Data Services (Vienna), Argus Media (historical data), Kpler (forecasts)

Propane NWE CFR ($/bbl)

Source: PVM Data Services (Vienna), Argus Media (historical data), Kpler (forecasts)

Butane Mt Belvieu ($/bbl)

Source: PVM Data Services (Vienna), Argus Media (historical data), Kpler (forecasts)

Butane NWE CFR ($/bbl)

Source: PVM Data Services (Vienna), Argus Media (historical data), Kpler (forecasts)

East of Suez

Both propane and butane prices climbed in the East since our last report, supported by firm heating and cylinder demand, while butane in particular saw a boost from a new cracker in China. The VLGC Astomos Earth is due to deliver a butane cargo late next week at BASF’s new naphtha/butane cracker at Zhanjiang as that facility begins to start up.

In the Far East, we lowered our outlook for propane beginning in Q2 2026 as US-China trade normalization is unlikely before H2 2026, and recent improvements like removing port fees do not stabilize expectations adequately for Chinese buyers who are still faced with 11% import tariffs on US cargoes. This will leave growing US output largely clearing into weakening demand centers in Japan, South Korea, and a patchwork of other non-China destinations. We increased our outlook for Far East butane this winter, though prices will remain near the five-year average for much of 2026 as supply from the US and upcoming Middle Eastern projects will help offset demand strength in the petchem and cylinder markets.

Firming LPG prices have made naphtha more competitive for flexi-crackers in Northeast Asia, but we do not expect a significant shift towards naphtha as Russian supply issues and stronger petchem demand in the East will prevent naphtha cracks from falling further, keeping LPG competitive.

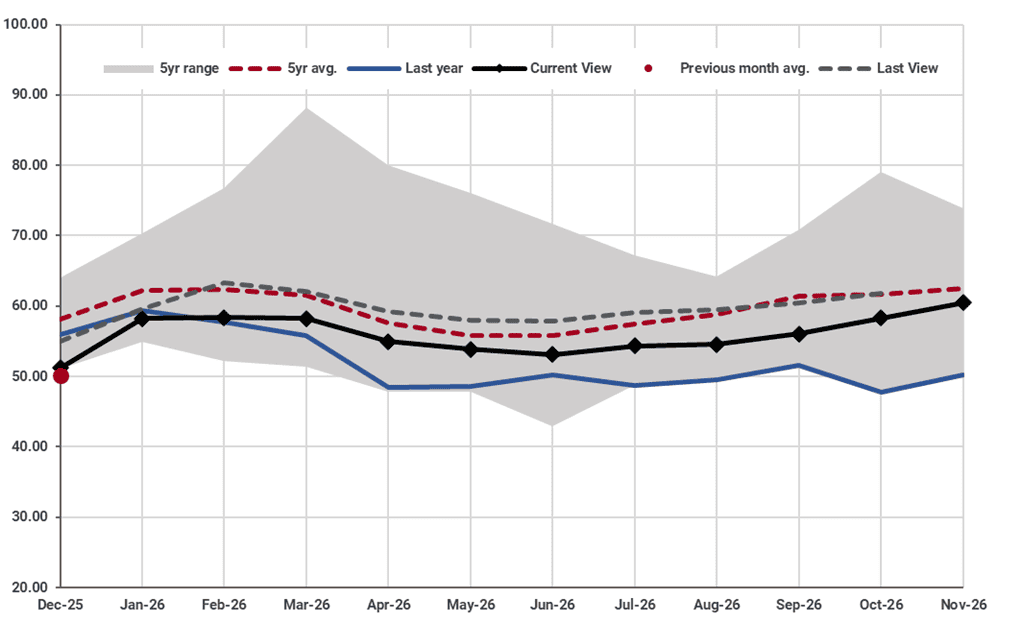

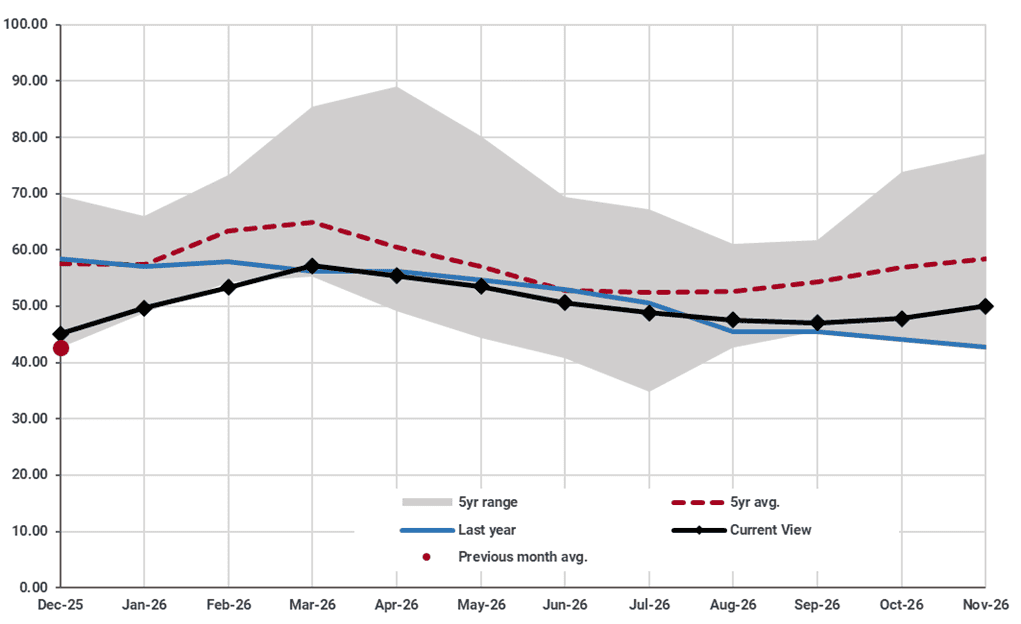

In the Middle East, we decreased our outlook for propane and butane in Spring 2026, as ample US supplies and Aramco’s move to defend market share in India and China will prevent prices from rising, absent a cold end to winter. India has recently contracted for US supply to cover around 10% of their 2026 import needs, underscoring the need for Middle Eastern suppliers to defend market share despite their proximity to India. China may have no other choice as of now, but a more buyer-friendly and transparent CP process will also help the Middle East keep Chinese buyers if US-China trade begins to normalize. This will lead to continued pressure on CP propane and butane next year, limiting prices to near the five-year average.

Propane Far East ($/bbl)

Source: PVM Data Services (Vienna), Argus Media (historical data), Kpler (forecasts)

Propane CP FOB AG ($/bbl)

Source: PVM Data Services (Vienna), Argus Media (historical data), Kpler (forecasts)

Butane Far East ($/bbl)

Source: PVM Data Services (Vienna), Argus Media (historical data), Kpler (forecasts)

Butane CP FOB AG ($/bbl)

Source: PVM Data Services (Vienna), Argus Media (historical data), Kpler (forecasts)

Want market insights you can actually trust?

The full report is available within Insight and provides:

- Naphtha: Cracks modestly adjusted as outlook for 2026 remains largely unchanged

- Gasoline: Cracks remain sticky, but Eastern markets should at last attain a premium over the West

- Middle Distillates: Sanctions set the stage for a constructive start to 2026

- Fuel Oil: HSFO pressured as fundamentals sour, while Asia’s VLSFO outlook improves

- Refinery Margins Forecast

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler