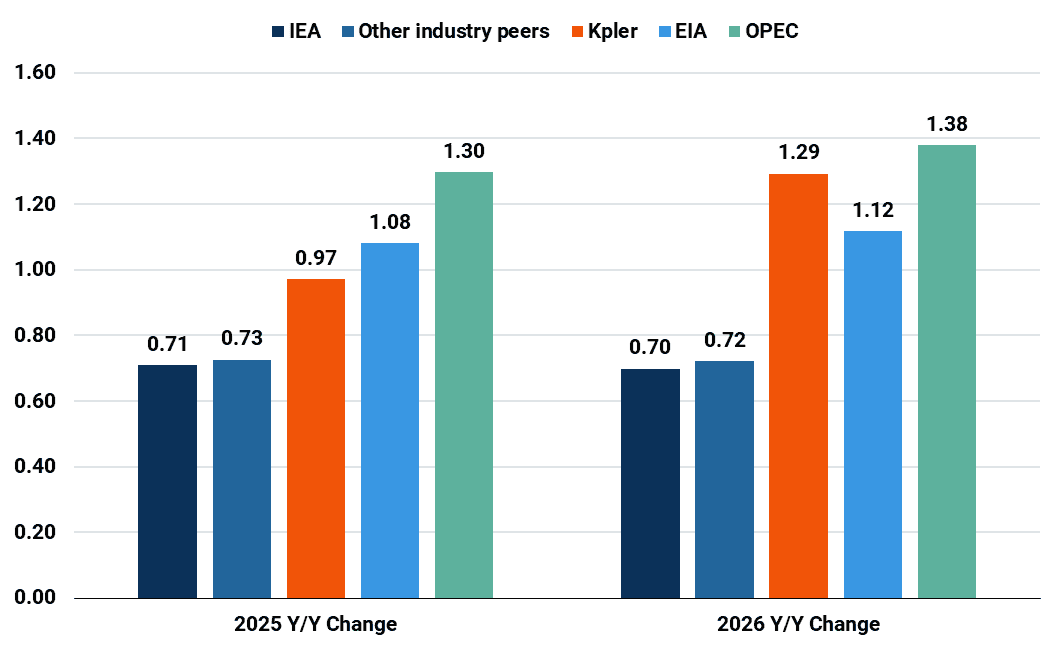

2026 Oil demand outlooks stand unreasonably bearish

Lackluster light ends consumption growth in a tariff-laden environment has justifiably weighed on 2025 oil demand outlooks. However, a rebound in petrochemical feedstock demand and robust gasoline use in Europe and non-OECD countries are set to boost demand next year. Our 2026 liquids demand growth forecast stands at 1.29 mbd, differing from the 0.8-1.0 mbd industry consensus.

The prevailing industry narrative is that oil use will remain subdued, with consensus forecasts for annual gains averaging just 950 kbd and 980 kbd for 2025 and 2026, respectively, a pace well below historical norms. Our 970 kbd y/y growth outlook for 2025, with petrochemical feedstocks demand heavily impacted by US-China tariffs and a harsher macro climate, aligns with the consensus. Our 2026 y/y growth forecast, however, diverges significantly. At 1.29 mbd, our projection is closer to the OPEC outlook and, in our view, more accurately reflects where market fundamentals are heading.

World oil demand growth forecasts (Mbd)

Source: Kpler, IEA, OPEC, EIA, other industry sources

Looking into 2026, there are areas of broad agreement. Jet fuel demand, despite efficiency gains and lagging international traffic, should continue to experience material growth as the aviation sector expands, particularly in Asia-Pacific.

With China’s diesel demand declining amid rising LNG and electric adoption in the trucking sector, and consumption stagnant or falling across most OECD markets, developing economies will bear the burden of sustaining only modest global growth in gasoil/diesel demand.

Fuel oil demand, mainly concentrated in marine bunkers and power generation, will be pressured by substitution. Egypt’s new FSRUs are set to displace half of this year’s fuel oil requirements, and Saudi Arabia’s utility targets (50% renewables and 50% gas mix) will become a more prominent factor toward the end of the decade.

Following what is set to be a subdued year for naphtha demand, the consensus calls for higher growth in 2026, led by new Chinese cracking capacity. While we share this directional view, our forecast is tempered by factors we believe are being overlooked: persistently weak naphtha cracking margins relative to ethane and LPG forcing ongoing naphtha cracking capacity rationalization. These pressures are evident not only in Europe and OECD Asia but globally, as reflected in recent news of ExxonMobil’s planned cracker shutdown in Singapore. It is, nevertheless, increasingly clear that future demand growth is shifting toward the light ends, particularly as petrochemical feedstock demand rises and also, in the case of LPG, as cylinder use and cleaner fuel substitution continue to expand.

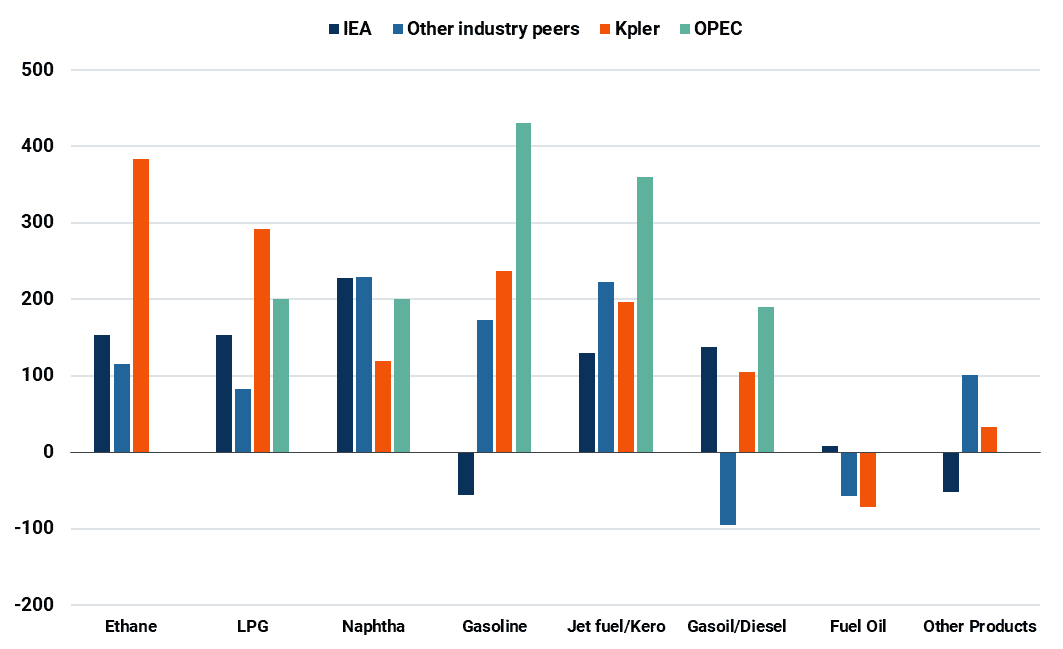

Oil demand growth forecasts for 2026 by product (kbd)

Source: Kpler, IEA, OPEC, EIA, other industry sources

Note: A 50/50 split has been used for IEA ethane and LPG demand for simplification purposes, and the same split has been used for OPEC LPG and naphtha demand.

The outlooks for ethane, LPG, and gasoline represent the largest discrepancies for 2026.

Ethane and LPG: The prevailing rationale for a marked slowdown in 2026 NGL demand growth is predicated on minimal 2025 demand growth, despite a surge in new processing capacity. This weakness is commonly ascribed to sluggish economic performance in emerging economies. While we acknowledge this element, our view is that naphtha will be the primary feedstock impacted next year, not ethane or LPG. The latter two benefit from materially better margins and an expanding capacity base that is already forcing competing naphtha crackers into closure. In our assessment, based on observed data, the primary factor suppressing NGL demand in 2025 has been the disruption to US-China LPG and ethane shipments linked to tariffs in Q2. Therefore, under our current base case, assuming trade tensions do not escalate further this year and begin to ease next year, we reject the bearish outlook for this sector and do not concur with the minimal 20-30 kbd growth forecasts for China published by many other forecast providers.

Gasoline: We believe the IEA’s view of a sharp swing from 180 kbd of growth this year to a 60 kbd decline in 2026 is an overstatement. European gasoline and HEV sales remain firm, pointing to further demand gains. While US gasoline will remain affected by efficiency gains and, to a lesser extent, EV penetration after the removal of tax credits, lower oil prices should provide a floor to next year’s expected decline. The non-OECD countries pose the biggest challenge to the consensus view, with the IEA showing a swing from 160 kbd of growth in 2025 to a 55 kbd decline in 2026. We find the projected rate of Chinese gasoline decline to be excessive; in our view, the continued expansion, rather than substitution, of the total car fleet will temper the impact of EVs. Furthermore, Southeast Asia should continue to post growth into 2030, supported by the dominant existing fleet of gasoline-powered cars and two-wheelers.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data

.png)