Producers cut prices to defend market share as fundamentals soften

Market calls

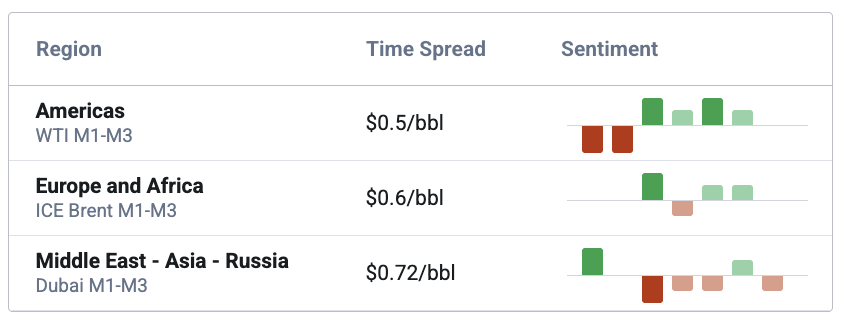

Market & Trading calls

Americas:

- Expect US market structures to remain exceptionally volatile in December as several bullish and bearish factors converge.

- Optimistic regarding Venezuelan crude supply, with weekly flows rebounding strongly, suggesting that the country's upgrading-related outages are largely resolved.

- Bearish near-term outlook for WCS Hardisty differentials as demand from the US remains weaker-than-average.

Europe and Africa

- Decline expected for CPC crude exports in December, as the slow pace of loadings following the drone attack on 29 November should weigh on the monthly average.

- Decline expected for crude intake in Nigeria as we project Dangote’s refinery runs to drop from above 400 kbd to 320-350 kbd in the Dec-Feb period.

- Stable on Nigeria’s gasoline imports which surged in November due to the RFCC downtime tightening domestic fuel availability.

Middle East and Asia

- Bearish Iranian and Russian crude differentials in China, as sellers are likely to further lower offers to attract buying interest even with teapots receiving more import quotas.

- Expect steady or higher Middle Eastern exports in December, driven by the ongoing refinery overhauls in Saudi Arabia and Kuwait and the OPEC+ output hike.

- Moderately bearish on Dubai prices and January OSPs, as Putin is anticipated to push India to raise Russian oil buying during his visit this week.

Americas: Volatility to remain high in December

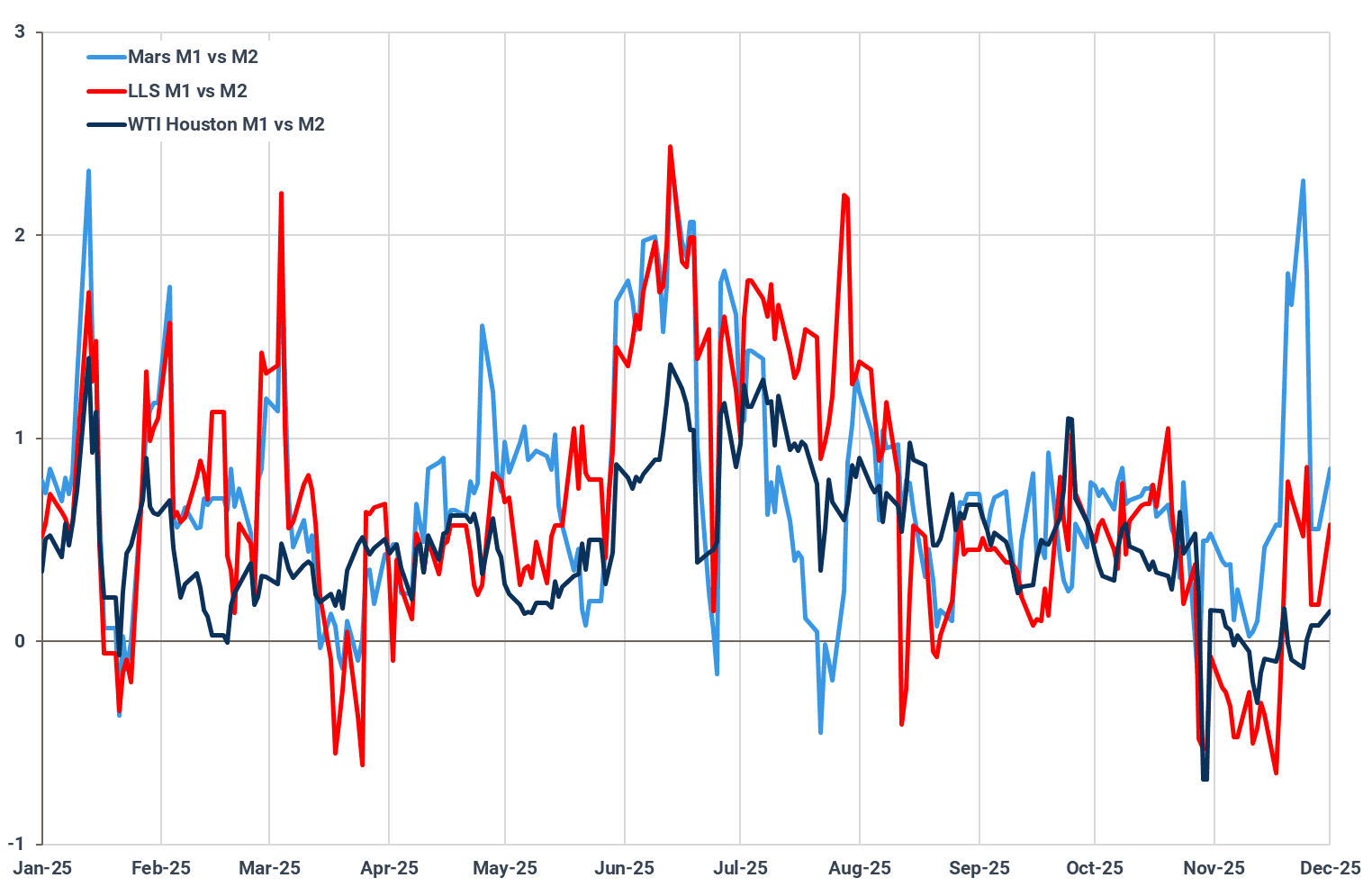

US M1/M2 spreads to remain volatile in December

December is expected to remain a volatile month for US crude markets, as several factors (both bearish and bullish) converge. Bullish developments, such as tax-driven inventory draws and an expected ramp-up in US refinery throughput (+500 kbd month-on-month to 16.6-16.7 Mbd in December; weekly EIA data will be discussed below), are set to be offset by bearish factors, including declining net exports, partly due to an expected rise in imports and surging VLCC rates, which will weigh on demand from Asia.

Moreover, record US crude and condensate supply, which averaged an all-time high of 13.8 Mbd in September (latest official monthly data), will keep availability of crudes plentiful into year-end. Domestic crude output is forecasted to remain flat at 13.8 Mbd, keeping a lid on any significant upside for regional market structures.

This view is corroborated by the latest US M1/M2 spreads (see chart below), especially for domestically consumed grades such as Mars, which saw a strong uptick in mid-November amid a rise in US crude demand in November (with some refiners emphasizing their ambition to run a heavier crude diet amid widening of sweet-sour spreads) and below average US crude imports. Nevertheless, with US crude demand expected to fall by ~1 Mbd month-on-month in January, the upside will remain limited in the near-term, with the trend likely to favour the downside amid lengthening balances over the next months.

US M1/M2 spreads by selected grades, $/bbl

Source: Argus Media

Venezuelan crude supply is staging a recovery

Venezuelan crude supply is staging a recovery following outages at three major crude upgrading facilities—Petrocedeno, Petromonagas, and Petrororaima—with a combined capacity of approximately 500 kbd. This market shift is confirmed by the sharp increase in Venezuelan weekly crude flows, which averaged 1 Mbd for the week starting 24 November, up from the one-year low of 220 kbd recorded the week prior (see chart).

Disruptions at these upgraders had previously placed a floor under domestic crude supply in mid-November, with preliminary domestic output estimates expected to average a multi-year low of 650 kbd in November. These temporary outages have supported Merey differentials, which rallied by $1/bbl to a discount of $13/bbl versus February Ice Brent in late November. However, the expected resumption of operations and the resulting supply injection will now exert stronger downward pressure on Merey pricing in the near future. This bearish outlook is intensified by the already massive availability of heavy sour crude, with floating storage levels holding near multi-year highs of 15 Mbbls, despite a recent decline.

Weekly Venezuelan crude exports by destination, kbd

Source: Kpler

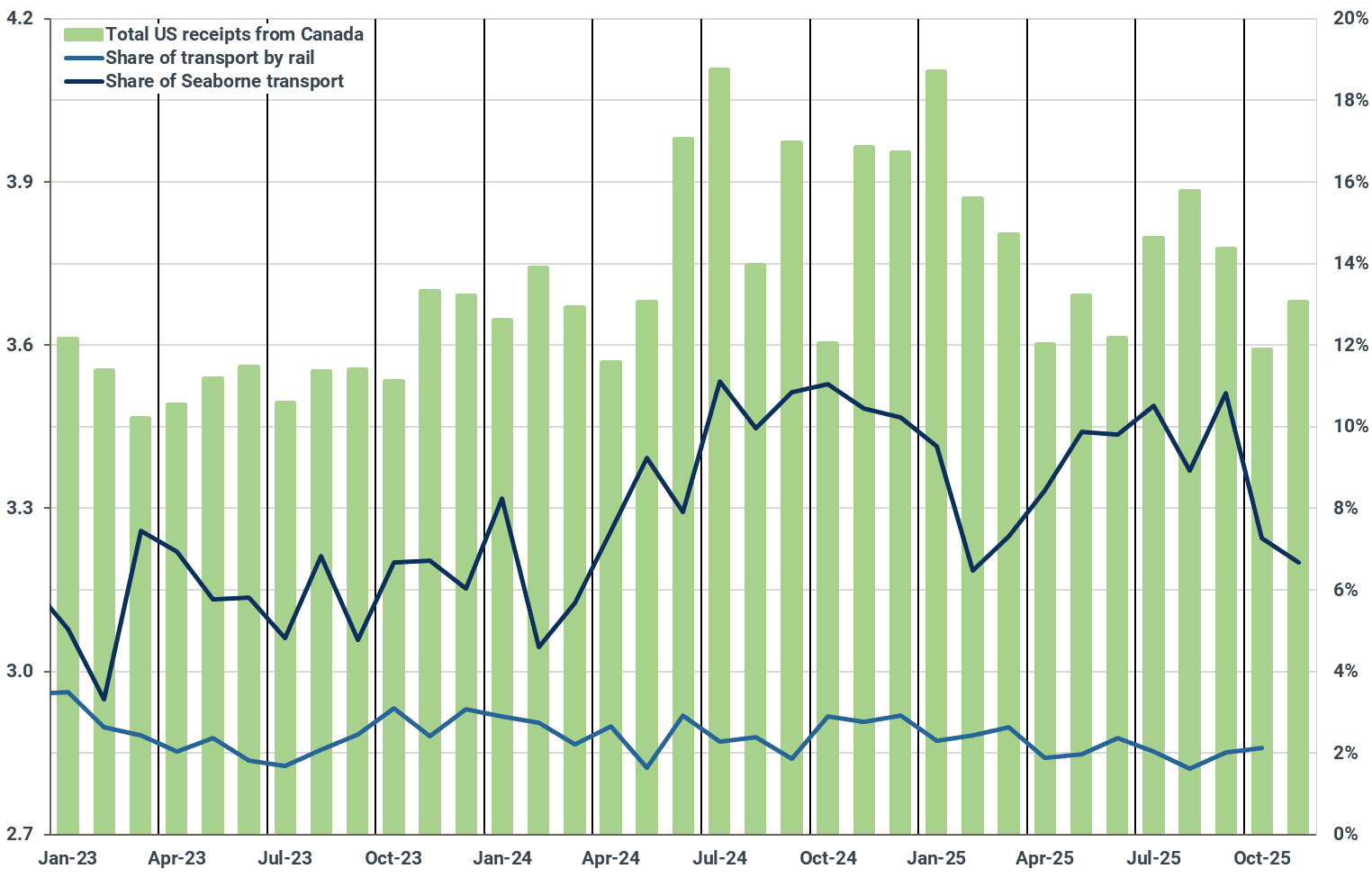

Lower Canadian flows to the US pressure WCS Hardisty

Steadily rising US crude throughput is currently supporting the regional market. The latest EIA weekly data for the week ending 28 November shows domestic crude intake jumping to 16.9 Mbd, an increase of 400 kbd week-on-week and marking a three-month high. While this elevated throughput should also boost demand for Canadian barrels, Canadian exports to the US (both seaborne and pipeline) averaged only 3.45 Mbd for the week ending November 28, marking the lowest level since late October.

Despite expectations for a reversal in this trend in December, driven by scheduled elevated US throughput this month, Canadian exports to the US are averaging well below last year's levels. November 2024 exports averaged around 4 Mbd.

A portion of the decline in Canadian exports is due to lower flows to US West Coast refineries, which averaged 100 kbd last month, approximately half of the volumes seen last year. However, this only accounts for a small part of the overall drop. This difficulty in finding sufficient outlets emphasizes the bearish near-term outlook for WCS Hardisty differentials. WCS Hardisty differentials have recently been trading at discounts of approximately $12-$13/bbl versus WTI Cushing (Argus Media). This bearish view is further reinforced by the expectation that US crude demand will ease by around 1 Mbd next month (see preceding section).

US crude and condensate imports from Canada by method, Mbd, %

Source: EIA, Kpler

Atlantic Basin: Ukrainian drone strikes on CPC terminal, shadow fleet, Druzhba pipeline

Despite attacks, CPC loadings resume at slow pace and Druzhba flows continue

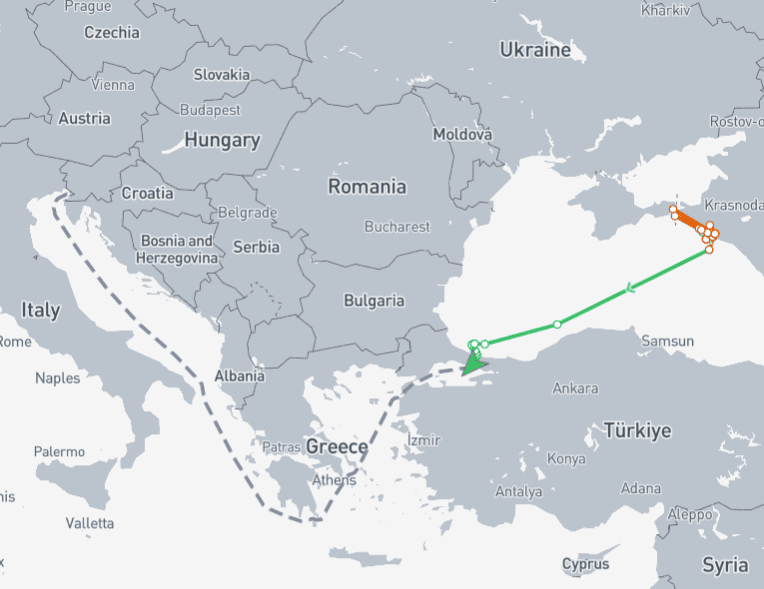

Ukrainian drone attacks have recently had a significant impact on Russian oil infrastructure, including various refineries, shadow-fleet tankers, upstream assets, and export terminals. On 29 November, the CPC terminal—which normally exports 1.5–1.6 Mbd of crude (≈90% Kazakh CPC blend and ≈10% CPC Russia)—was struck. One of the terminal’s three single-point moorings (SPMs) was reportedly seriously damaged, prompting a suspension of loading operations and a shutdown of connected pipelines as a precaution. As we anticipated, exports resumed within days. No loadings occurred between 28–30 November, but the Advantage Sweet departed on 1 December to Trieste and the Saturn Moon on 3 December to Le Havre. The recovery was largely enabled by the terminal’s standard practice of loading crude through two SPMs, with the third typically held in reserve. Nevertheless, CPC shipments may continue at a reduced pace for the remainder of the month—either because SPM-3 remains tied up in planned maintenance, or because repairs to the damaged SPM take longer than expected. Under this scenario, December CPC exports could fall below 1 Mbd. Given that Europe sources nearly 1.2 Mbd of Kazakh CPC crude from the affected terminal, any prolonged tightening in CPC availability would drive substitution toward comparable Mediterranean, North Sea, West African and U.S. grades, including Azeri BTC, Es Sider, Bonga, and WTI. Separately, on Wednesday reports surfaced that Ukraine had attacked the Druzhba oil pipeline using remote-controlled explosives. The pipeline transports roughly 200 kbd of Russian crude (~100 kbd to Slovakia and ~100 kbd to Hungary). However, both Slovakia’s pipeline operator and Hungary’s national oil and gas company stated yesterday that Druzhba crude flows are currently running normally.

Advantage Sweet vessel on its way from CPC terminal to Trieste

Source: Kpler, mapbox

Dangote maintenance schedule: RFCC offline for 2 months in Dec–Jan; CDU offline for 1 week in late Jan/early Feb

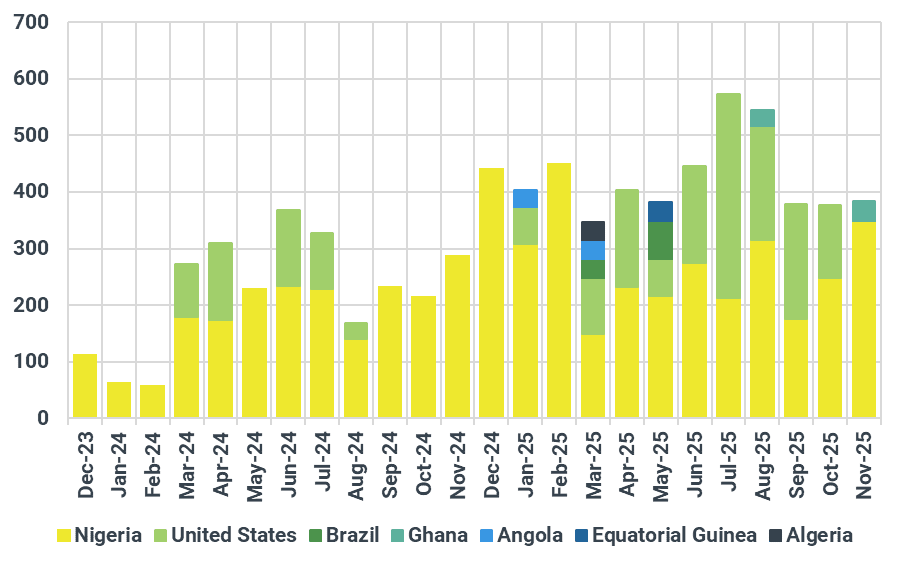

Crude imports into Nigeria's Dangote refinery have fallen sharply from their highs over July and August. Arrivals averaged ~380 kbd over September–November, roughly 180 kbd (30%) below volumes purchased during the summer. The lower intake reflects recurrent outages and major maintenance works planned over the next two months. The RFCC unit, which has struggled with regenerator-related issues and spent much of Q3 cycling between offline and online modes, is now scheduled for a major shutdown beginning 4 December and lasting ~2 months, with a restart planned for 1 February 2026. This represents a shift from the earlier plan of a mid-December start and 45–60-day duration, and will involve a full RFCC overhaul and equipment replacement. In addition, a planned 1-week shutdown of the CDU is set to begin 30 January 2026, with a restart on 5 February. The CDU had previously experienced difficulties with its overhead cooling water system, which may again be contributing to this intervention. Both the CDU and RFCC are expected to be back online by early February. In November, Dangote’s crude receipts consisted almost exclusively of Nigerian grades, predominantly Bonny Light, followed by Amenam, Forcados, Utapate and Qua Iboe. It is notable that the second ever cargo from Ghana arrived as well, carrying Sankofa. Looking ahead, we expect Dangote’s crude slate to remain primarily domestic, supplemented by smaller volumes from other West African producers or the United States.

Dangote crude oil imports, kbd

Source: Kpler

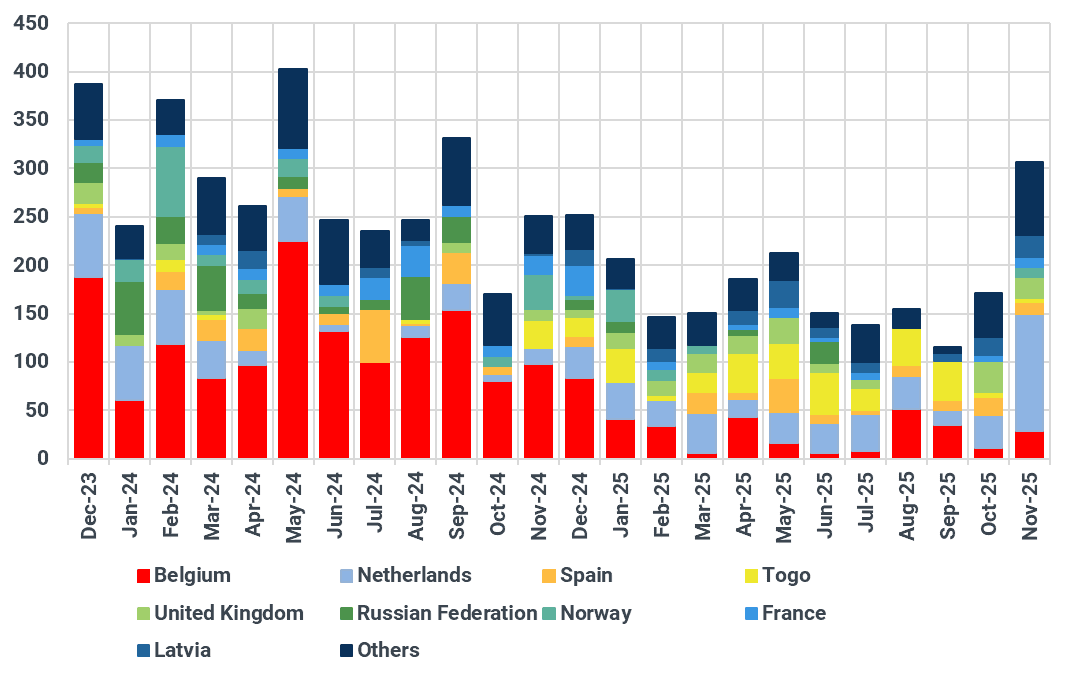

Nigeria’s gasoline imports surge to 14-month highs in November

The shutdown of the CDU and RFCC units is expected to reduce Nigeria’s refinery runs from ~450 kbd in October to ~320–350 kbd, with throughput likely to remain in this range through December–February. A recovery should follow once maintenance concludes, with runs potentially exceeding 500 kbd by April 2026. Lower crude intake at Dangote naturally translates into lower product output, particularly gasoline. Nigeria’s gasoline demand has averaged ~300 kbd in recent months, with imports over Jan–Oct covering ~200 kbd of consumption. Dangote has been producing ~100–130 kbd of gasoline in past months, but this output is expected to drop toward ~80 kbd during December–February, when the RFCC is offline and gasoline production relies only on the Reformer and Isomer units. This tightening in domestic supply has already triggered higher overseas buying. In November, Nigeria’s gasoline imports nearly doubled m/m to ~300 kbd—the highest inflow in 14 months. Volumes have originated mainly from Europe, particularly the Netherlands and Belgium. The sharp pull on European barrels could encourage refiners to lift crude runs during December to meet Nigeria’s incremental product demand.

Nigeria gasoline imports, kbd

Source: Kpler

Middle East-Asia-Russia: Oil sellers cut prices to compete for Asian market share

Iranian, Russian crude vie for Chinese teapots as new quotas land

Iranian crude oil floating storage appears to be slowing in clearing even as China issues fresh import quotas to independent refiners that lean heavily on sanctioned barrels as core refinery feedstocks. More than 20 teapots secured at least 7.4 mt of quotas last week, to be consumed before end-December. Teapots are likely to prioritise moving crude held in bonded storage through customs first, since many of these volumes were booked several weeks earlier.

Kpler data shows more than 50 mb of Iranian crude sitting on the water this week — the highest level since April 2023 — with around 36 mb anchored off Malaysia and Indonesia. Volumes waiting off China have begun to ease since last week, now down to 5.6 mb from roughly 12 mb in mid-November.

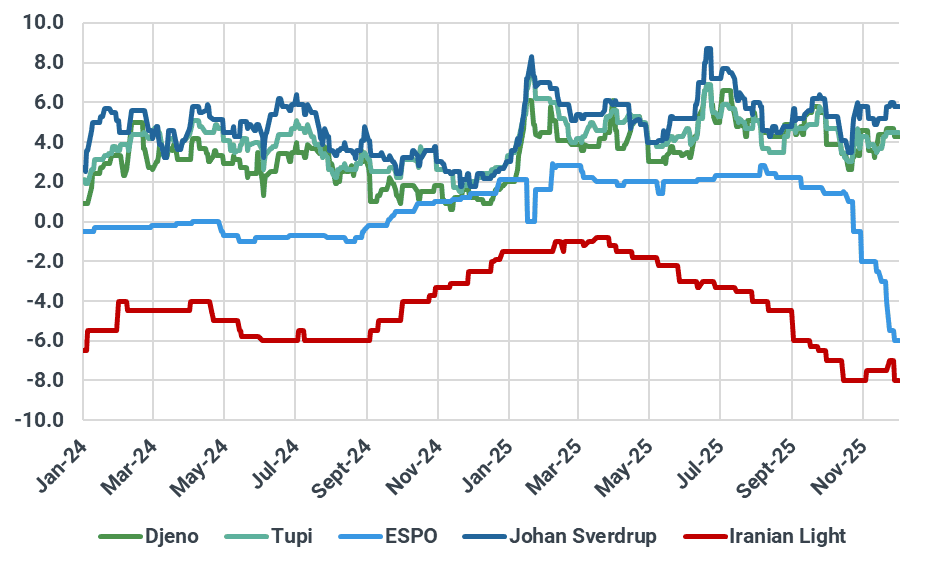

That said, Iranian oil is encountering growing competition from Russian crude in China. With state-owned refiners still steering clear of Russian barrels and Indian refiners also cutting back purchases, Chinese teapots have become the primary eligible buyers. Light sweet Russian ESPO crude is now trading around -$6/bbl versus ICE Brent on a DES basis in China, according to market sources — a sharp drop from the $1/bbl premium seen before the US sanctions on Rosneft and Lukoil. Medium sour Urals is priced at roughly -$7/bbl against the same benchmark, Argus Media data shows, marking the lowest level since at least November 2023. In this environment, Iranian sellers have been compelled to trim offers to stay competitive: Iran Light is now around -$8/bbl, down from roughly -$7 to -$7.5/bbl in late November.

With ample feedstock availability and increasingly attractive pricing, China’s teapots are poised to step up crude purchases and boost refinery runs. Oilchem data shows the utilisation rate at Shandong teapots reached 54.99% last week — the highest level since October 2024.

Selected crude differentials against ICE Brent on DES China basis, $/bbl

Source: Argus Media

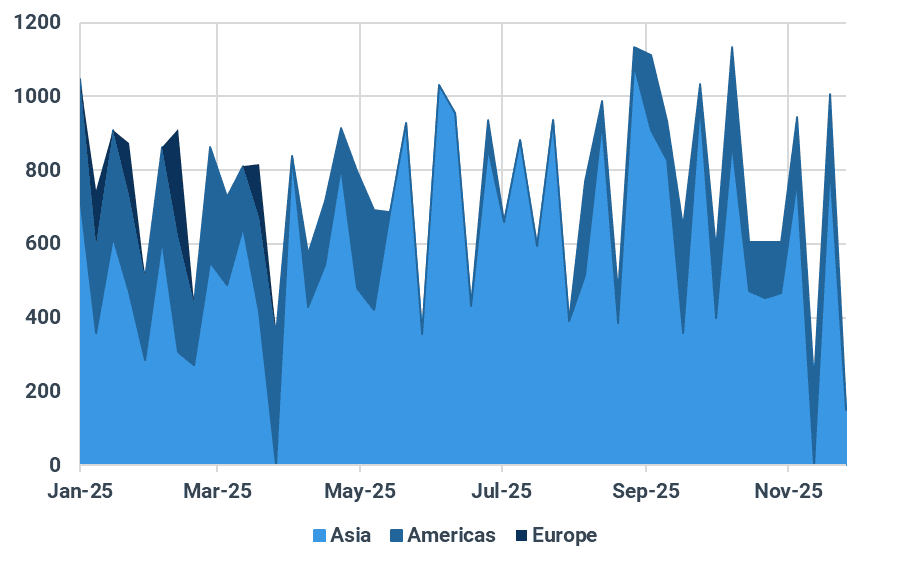

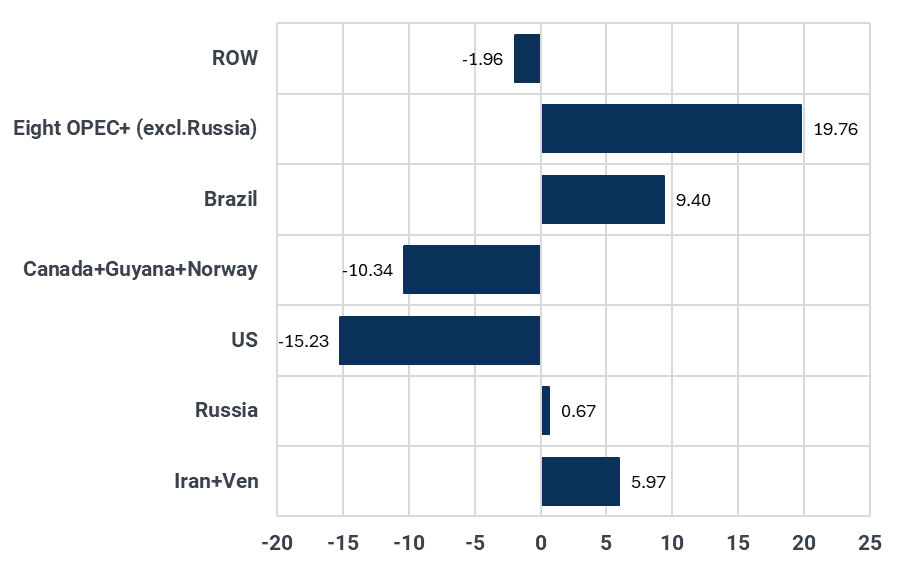

November oil-on-water growth eases, but Middle Eastern exports jump

The build-up of global oil-on-water slowed markedly in November, rising by just 8.3 mb versus 86.4 mb in October and 118.5 mb in September. The moderation reflects lower exports from the US, Brazil and Norway, while drone attacks and sanctions also prompted Russia to pare back shipments. However, oil-on-water originating from the eight OPEC+ members (excluding Russia) jumped sharply last month, increasing by nearly 20 mb. This aligns with a notable rise in crude exports of non-sanctioned Middle Eastern OPEC+ barrels, which reached 16.4 mbd in November — a level last seen in April 2023.

Saudi Arabia delivered the largest export increase last month, rising by 147 kbd m/m to 6.7 mbd, supported by weaker domestic crude demand during maintenance at the SASREF and SATORP refineries, which together account for 610 kbd of processing capacity. Kuwaiti shipments also grew by around 140 kbd, partly reflecting the outage at the Al-Zour refinery.

December crude exports from these Middle Eastern producers are expected to hold at similarly elevated levels, with domestic refinery maintenance still ongoing and production set to rise further under higher output quotas. Despite strong refining margins and firm crude processing demand to meet heating oil needs, the growing supply from the Middle East would keep pressure on the Dubai market, particularly as the narrowed Brent–Dubai EFS continues to leave the arbitrage window wide open.

Global crude oil-on-water change (Nov.30 vs Nov 1) by origin, mb

Source: Kpler

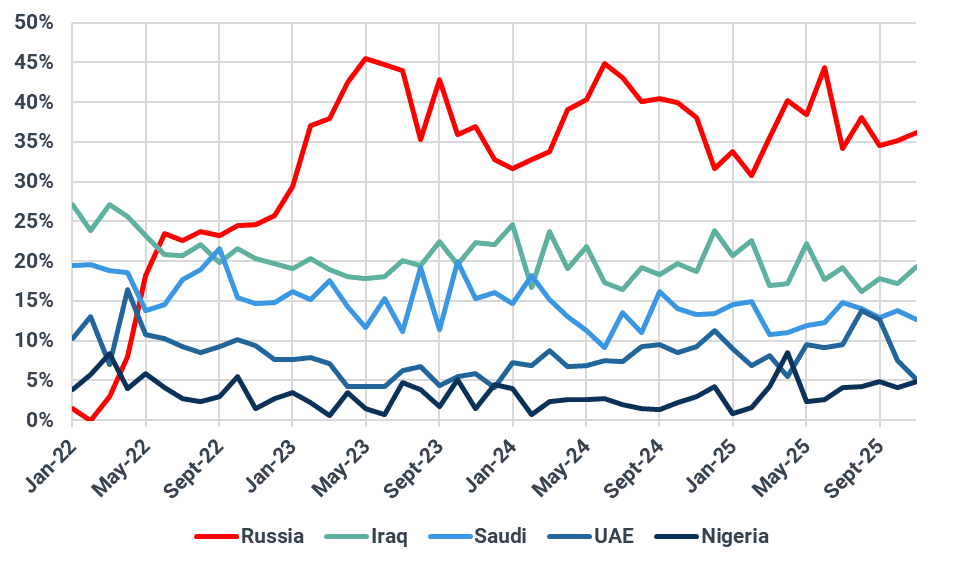

Putin set to press India for higher Russian crude intake

Russian President Vladimir Putin’s visit to India this week is expected to press for increased Russian oil sales to the South Asian nation, which has scaled back purchases since the US sanctions on Rosneft and Lukoil in late October, according to media reports. India’s imports of Russian crude climbed to a five-month high of 1.84 mbd in November, as buyers rushed to secure cargoes ahead of the sanction grace period ending on 21 November. Discharges of Russian crude continued last week, with sanctioned Nayara Energy still maximising its intake and other Indian refiners taking barrels supplied by non-blacklisted entities. Even so, overall arrivals have begun to slow.

New Delhi is seeking to secure a lower trade tariff with Washington before year-end, as Indian refiners have already scaled back their purchases of Russian oil. Kpler currently forecasts India’s Russian crude imports at around 1.4 mbd in December, though some cargoes may struggle to discharge on time or could be redirected to China due to sanction-related complications.

Putin may use his visit to encourage India to resume its buying spree, a move that aligns with refiners’ economic interests given Russian barrels are roughly $8–$9/bbl cheaper than Middle Eastern crude on a delivered basis. If New Delhi responds positively, the shift could put downward pressure on Dubai-linked prices and prompt Middle Eastern NOCs to trim OSPs to stay competitive for Indian demand. Kpler expects Saudi Aramco to lower its flagship Arab Light OSP for January loading by about $0.4/bbl, broadly in line with the monthly shift in the Dubai M1–M3 spread.

India's key crude suppliers by share, %

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler