Fed cuts 25bp, but Powell more hawkish than expected

Powell made it clear a December rate cut is not a foregone conclusion as markets re-price rate cut probabilities

Summary

- More Hawkish Than Expected: The Fed delivered a widely expected 25bp cut and an end to quantitative tightening (QT). However, Chair Powell stressed that a December rate cut is far from a foregone conclusion and highlighted strong disagreement across the Committee. Powell’s somewhat more hawkish position is a reminder that FOMC concerns about inflation should not be discounted.

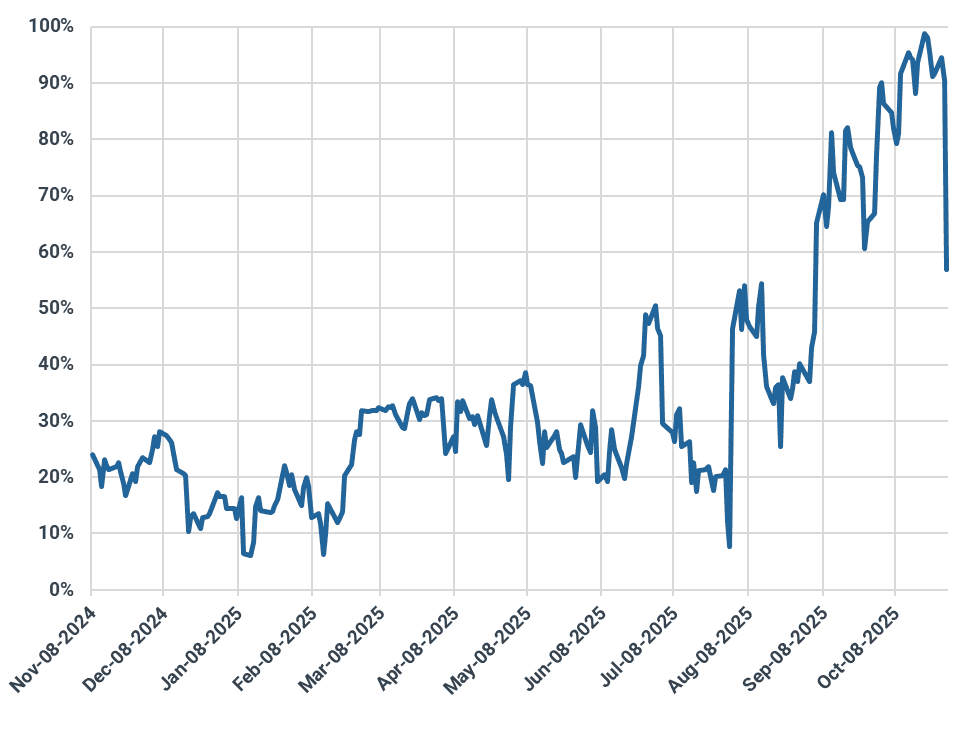

- Cut Outlook: CME market odds for a 25bp December rate cut fell sharply during the press conference, sliding from roughly 90% ahead of the FOMC meeting, to 60% as traders parsed Powell’s caution. We still see a cut as the most likely outcome for December, but the meeting could be “live,” with the outcome in question.

- Market Reaction: Front-end rates repriced with 2y yields trading up to 3.6%, and the 10y back above 4%, while USD strengthened. Equities and gold slipped on the hawkish tone, which dented the “run it hot” narrative somewhat, albeit the S&P was able to rally into the close.

Market Analysis

Coming into the FOMC meeting today (October 29th), the market was expecting a dovish tilt from Chairman Powell. In recent months, the Fed has shown a bias towards emphasizing its employment mandate ahead of its inflation mandate. In the minutes ahead of the press conference, the Fed announced it was cutting the Fed Funds rate by 25bp and ending quantitative tightening, in line with forecasts, and yet, the vibe quickly shifted after Powell took to the podium.

In prepared remarks, Powell made it clear that there was elevated disagreement on the Committee, and the probability of a rate cut in December was not a foregone conclusion. He reiterated this reality several more times as he took questions. Before today’s meeting, CME rate futures were pricing a 90% probability of a 25bp cut in December. In the minutes after Powell’s comments, the probability of a 25bp rate cut fell back to 60%. The voting committee had two dissents in different directions, a rare occurrence. Miran, a recent Trump appointee, argued for a 50bp cut, while Kansas City President Schmid, argued for no cut.

Probability Fed Funds Rate Cut to 3.5 – 3.75% Range at December Meeting (%, assumes a 25bp cut in December)

Source: CME; current Fed Funds rate at 3.75 – 4%

It has been our view since Powell’s Jackson Hole speech earlier this year that despite persistent above target inflation, the Fed would focus on cutting rates in an attempt to support a somewhat stable, yet stagnant labor market. At present, US job creation is anemic, but layoff activity remains limited. A flat to declining labor force, a result of Trump immigration restrictions and deportation policy, is acting as an offset to weak job growth.

Nonetheless, Powell’s comments today were a reminder that a guaranteed forward path for rate cuts is not a foregone conclusion. While it is our belief that the Fed will continue to cut at their final meeting of the year, concerns about inflation remain on the minds of many on the FOMC and should not be discounted. On inflation, Powell added that the effects of tariffs were beginning to flow through to the goods side of the consumption basket. He later added that non-housing services was also a problem. In our view, the United States is roughly living in a world closer to 3% inflation, rather than the Fed’s target of 2%.

One- and Six-Month Pace of Durables Inflation (%)

Source: BLS

Bond markets reacted swiftly to the FOMC meeting with 2y yields rising to 3.6%, a sizeable reversal off an intraday low of 3.38% set on October 17th. The 2s - 10s spread fell to 0.466% as the front end of the yield curve reacted more aggressively to the Powell press conference. Even so, 10y yields, a good barometer for fiscal sustainability, inflation, and growth, pushed back above the 4% “line in the sand” that has generally served as a source of support over the past year. Through mid-October, the market toyed with the idea of pushing yields sustainably below the 4% level. That might be off the table for now, albeit rising bill issuance, and a narrower than expected government deficit could still weigh on long duration yields.

Alongside the increase in government bond yields was an expected strengthening in USD. DXY, a weighted index of USD against a basket of currencies, rallied to the highest level in eleven trading days. Given stronger than expected US growth levels, we believe there is a chance for additional USD strength through the end of the year before weakness takes hold again next year. A DXY break above the 99.50 level would mark a critical technical move.

Equity markets and gold both took a hit as the “run it hot” US economy narrative eased off a bit given Powell’s somewhat more hawkish commentary. After trading as high as $4,046/oz intraday, gold was trading back towards $3,965/oz following the press conference. We remain bullish on gold over the long-term as monetary debasement remains a real issue. The S&P initially traded down by as much as 0.5% as Powell spoke, albeit these losses narrowed into the close. S&P price action tomorrow will be a good signal of to watch for whether the rally following the October 10th selloff can maintain. Microsoft, Meta, and Alphabet post earnings this evening.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data