US-Iran conflict extends distillates strength post winter

Escalating US–Iran tensions have shifted distillate markets from pricing geopolitical risk to confronting non-performance. Shipping disruptions, war-risk insurance cancellations, and tightening freight economics are reinforcing prompt strength just as Northwest Europe enters maintenance season. If disruptions persist, ICE gasoil appears underpriced relative to embedded transit and insurance risk.

*Updated with context about drone strikes on Novorossiysk

Key takeaways:

- The market’s reliance on Middle East Gulf flows leaves roughly 1.15 Mbd of middle distillates exposed to transit disruption.

- Traffic reductions, war-risk cancellations, and selective port suspensions have shifted the prompt market from risk premium to potential non-performance.

- ICE Gasoil appears underpriced should freight disruption persist.

- European buyers may need to relax self-inflicted procurement rigidity under EU Article 3ma, with Reliance and Far East cargoes emerging needed more than ever as ICE Gasoil M1/M2 market structure jumps by over $25/t d/d.

- China is well positioned to increase middle distillate exports this month as export economics strengthen materially.

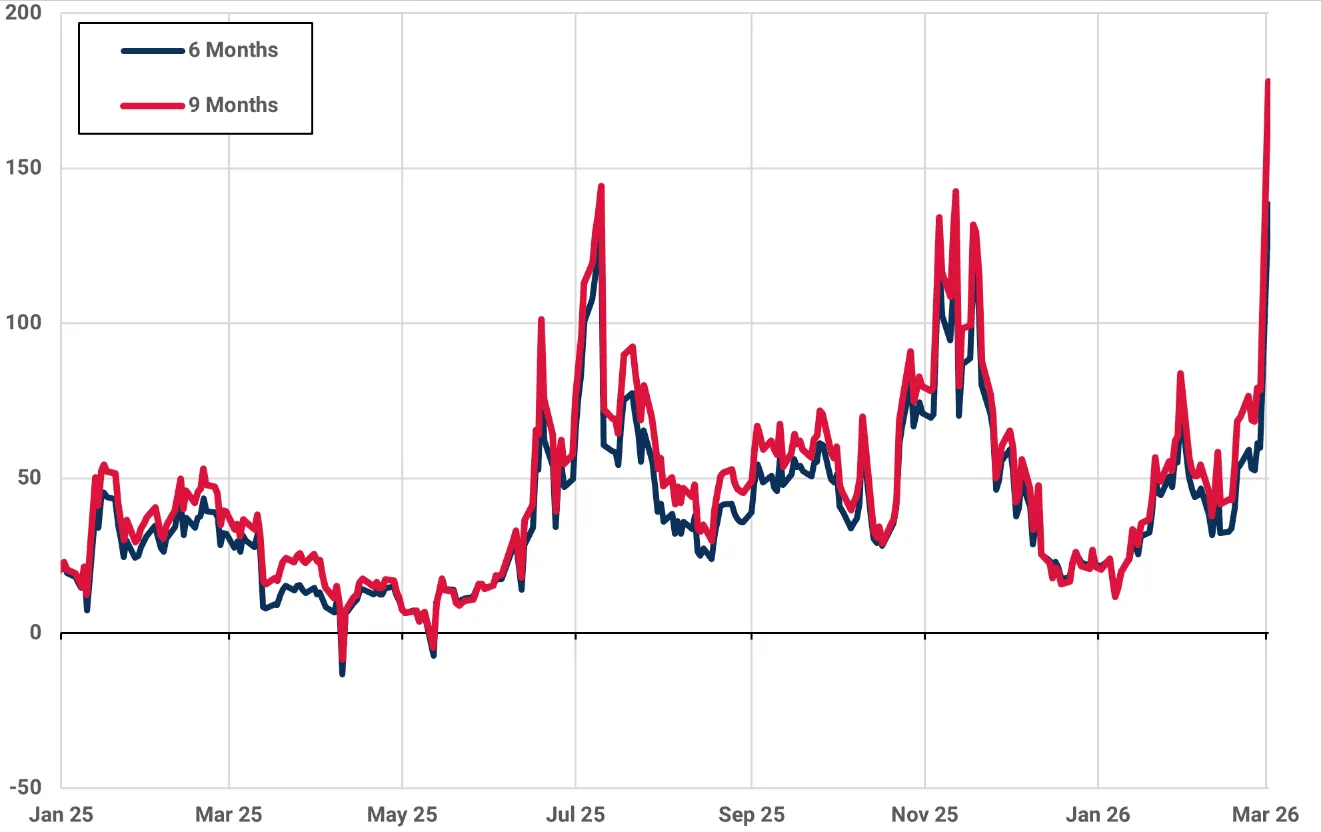

Forward ICE Gasoil structure

*Prices correct as at 0800 GMT

Source: Kpler using Marketview

Shipping disruption in the Gulf has moved beyond elevated rhetoric and into measurable operational strain. Confirmed vessel security incidents off Oman, a reported 75% reduction in traffic through the Strait of Hormuz, and selective port suspensions across Bahrain, Kuwait, Oman, and the UAE indicate that transit hesitation and loading issues have beyond mere possibility.

Gulf-loading bids and offers have been suspended within the regional refined products assessment framework as the market steps back from pricing open exposure. Meanwhile, maritime war-risk underwriters have issued 72-hour cancellation notices for Middle East Gulf and Gulf of Oman cover, while remaining insurers have repriced policies materially higher, in some cases by roughly 50%. This is a tightening of market mechanics, not merely a geopolitical premium.

For distillates, the implications are disproportionate. Roughly 10% of global gasoil trade and 20% of jet and kerosene flows transit Hormuz. Even without confirmed disruptions, higher insurance costs, suspended vessel movements, and anchorage delays tighten delivered availability.

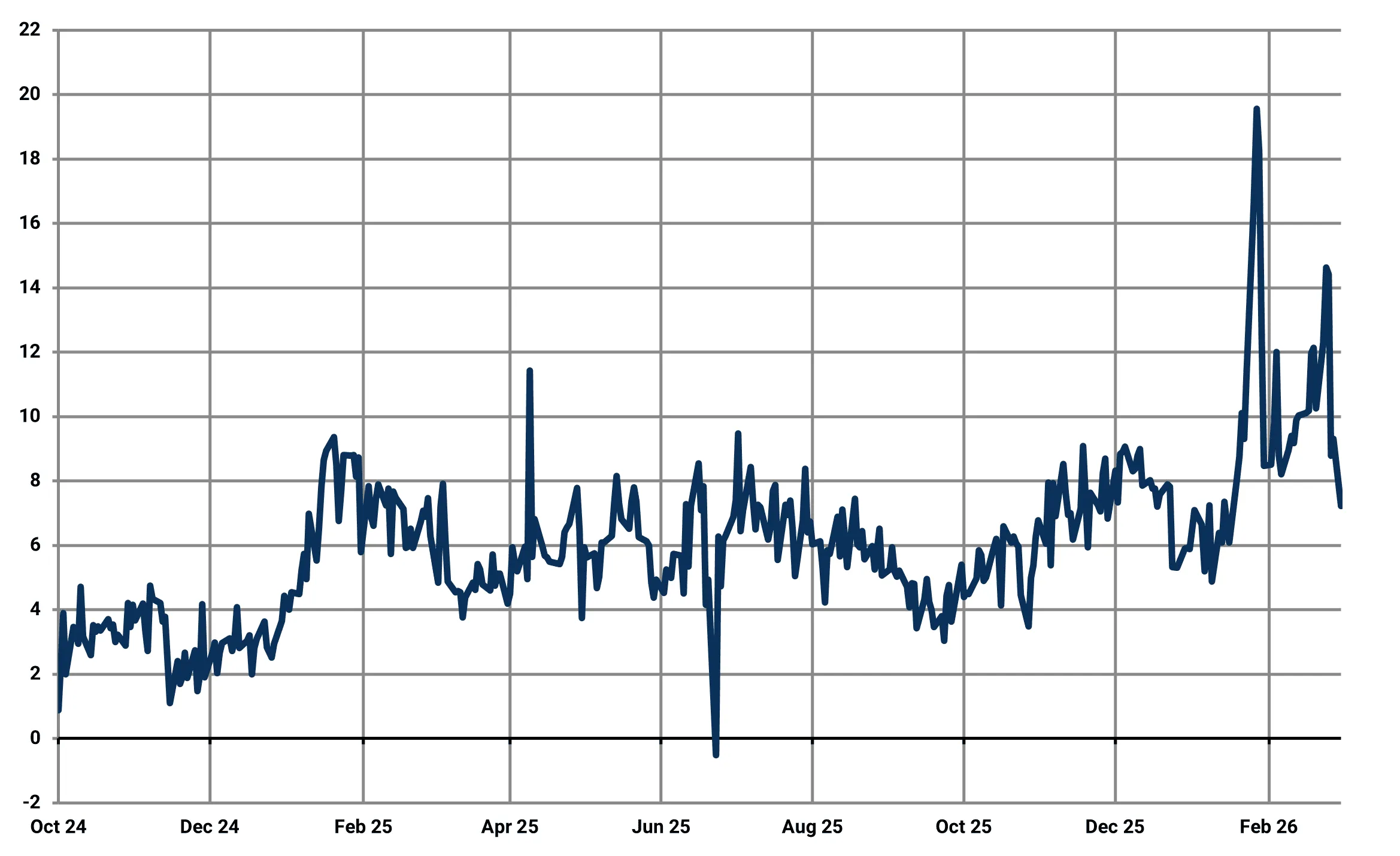

Our base case remains that Northwest Europe will need to price higher to pry cargoes from the US Gulf Coast, particularly given persistent strength along PADD 1 following the recent cold snap. The HOGO spread has already compressed to $7/bbl in early Asia trade Monday, confirming that Atlantic Basin arbitrage is adjusting in that direction.

NYMEX Heating Oil/ICE Gasoil spread ($/bbl)

*Prices correct as at 0800 GMT

Source: Kpler using Marketview

The timing is inopportune. Northwest Europe continues to debate merchantability nuances under EU Article 3ma, but tightening logistics may remove that luxury. The upcoming spring maintenance season will further tighten regional balances, while relatively low Russian refinery runs and declining exports to Brazil are likely to intensify competition for compliant barrels. This pressure may increase further following reports that Ukraine has struck Russia’s Black Sea port of Novorossiysk, adding another layer of uncertainty to regional export flows. This issue is particularly acute for jet/kero. We have recently highlighted Northwest Europe’s reliance on the Mideast Gulf, and how it will be difficult to find alternative suppliers that can meet the stringent safety, traceability and certification requirements.

The list of alternative suppliers capable of matching the Middle East Gulf’s scale remains short. Reliance has continued to demonstrate that its cargoes do not run afoul of EU sanctions, leasing storage in ARA and marketing barrels after achieving EU T2 status. However, incremental supply may also emerge from Asia. The EFS has widened below minus $60/t in early Asian trade, improving long-haul economics. Recent East–West jet fixtures provide precedent for such flows, including at least one cargo loading from China. While that refinery has not processed Russian crude since 2020, Chinese origin will attract additional scrutiny given China’s status as a net crude importer. The willingness to transact nonetheless suggests Far East–West runs are increasingly viable, albeit with higher documentation and compliance costs that justify firmer pricing.

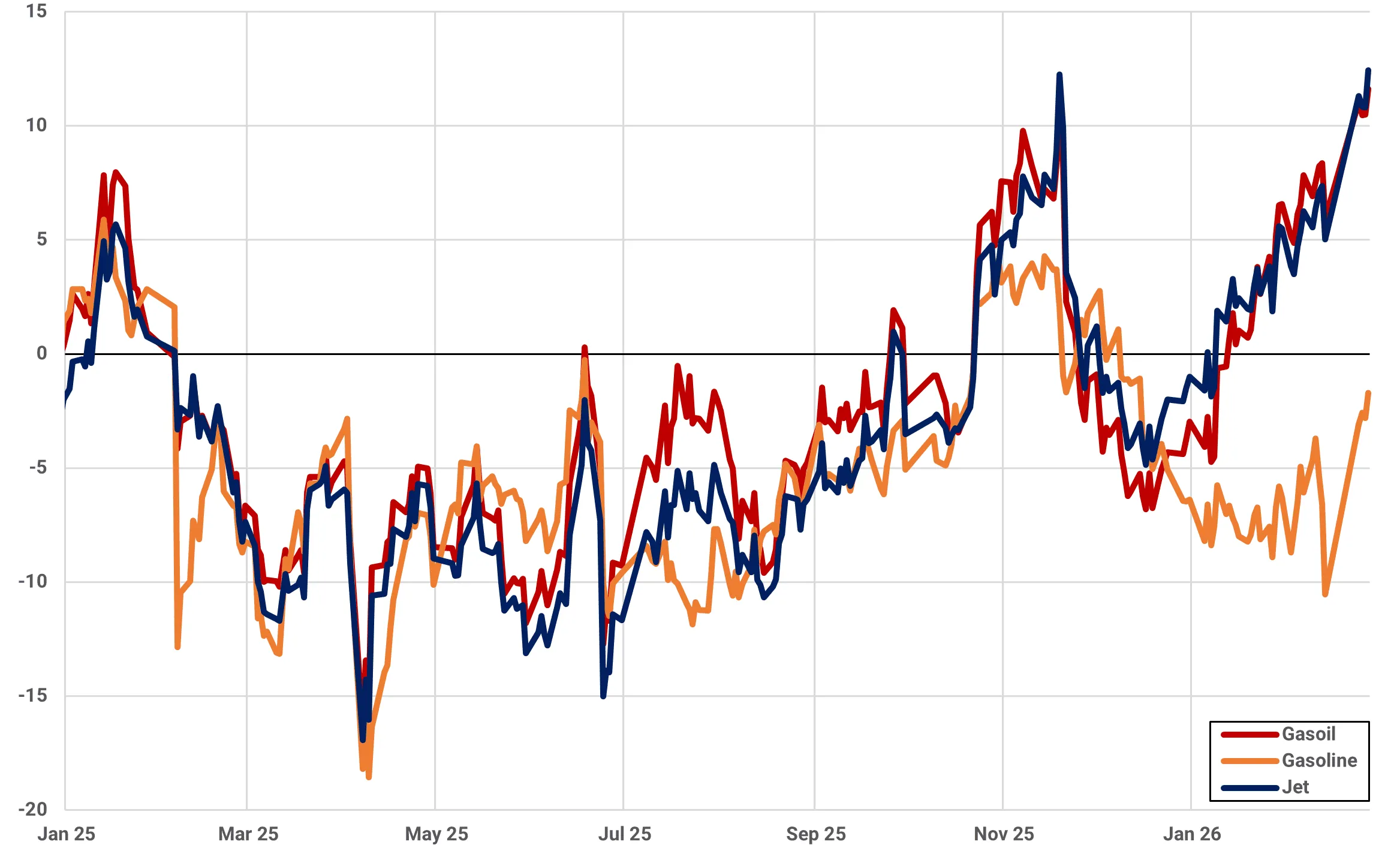

China is in a uniquely strong position to increase clean product exports this month. Export economics for middle distillates into Singapore exceed $12/bbl, and incremental Asian supply will eventually displace barrels that can move West. Even if flows are indirect, the effect is the same: Atlantic Basin markets will need to bid higher to secure supply.

China-Singapore oil products arbitrage incentive ($/bbl)

Source: Argus

Freight economics will ultimately dictate Europe’s response. If war-risk premia remain elevated and tanker availability tightens, delivered replacement barrels into Northwest Europe will price significantly higher. In that context, ICE gasoil appears underpriced relative to the scale of transit and insurance risk now embedded in the supply chain. The market is still pricing disruption probability, not persistent freight constraint.

Market insights you can actually trust

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions. In times of conflict and geopolitical uncertainty, our real-time data keeps you ahead of supply disruptions and price volatility.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler