Fundamentals to diverge cross regions

Market & Trading Calls

LPG:

- We have modestly increased our West of Suez propane price forecast for H2 2025 compared with last month, on the back of improving US-China trade and our expectations that flows will normalise by end-Q3 as US export terminal capacity increases, preventing WoS inventories from plumping record highs

- Meanwhile, we have modestly increased our Far East butane price forecasts for H2 2025, as the current glut in China due to reliance on Middle Eastern barrels will ease going forward as buyers slowly move back to US-origin cargoes as the year progresses

Naphtha:

- European naphtha cracks were adjusted through the front of the curve to reflect weaker y/y fundamentals in Q3 amid additional cracker rationalization, although export demand East will ensure cracks continue to trade above the five-year average.

- E/W spread will trade above the five-year average as regional fundamentals continue to diverge as the year progresses.

- We have amended Asian crack forecasts modestly higher through the curve m/m, as recent US-Asia trade developments and the ending of unplanned outages at fresh cracking capacity will tighten naphtha balances through Q3, with China and Indonesia in particular remaining bright spots as import requirements strengthen.

- However, there remains downside risk to this view if US-Asia negotiations fail and if new units ramp up more slowly than anticipated.

Gasoline:

- Neutral WoS cracks as the region awaits clear indications from an erratic US market. While European fundamentals look constructive compared to previous years on capacity closures and improving domestic demand, the US balance is expected to lengthen y/y, with no clear sustained demand upside from attractive pump prices yet.

- The outlook for the Atlantic Basin has nonetheless improved vis-à-vis last month, given mounting evidence of persistent challenges with Dangote’s RFCC, and more capacity at risk in Europe. We maintain our view of upside potential for cracks through to August, in line with strengthening seasonal demand, with pressure on the cards come September.

- Bearish EoS cracks as demand continues to underperform, intensifying the regional overhang this month. A shrinking transpacific arbitrage window and rising Chinese exports will add further weight.

- With Asian balances lengthening this month and remaining longer on a y/y basis through to September, we struggle to see cracks recover substantially before Q4.

Middle Distillates:

- CIF NWE market to ease eventually: The transatlantic arbitrage dysfunction is temporary and should correct soon.

- Stable WoS jet/kero: ARA remains well-supplied, and fresh arrivals from the Far East will support stock builds.

- Tight EoS gasoil: Asian buyers remain heavily dependent on tight Chinese exports, with the E/W spread capping arrivals from India and the Middle East.

Fuel Oil:

- Neutral to moderately bearish Singapore HSFO cracks following the anticipated correction from recently inflated values.

- Neutral Singapore VLSFO cracks amid a balanced outlook on Singapore VLSFO. The drop in Kuwaiti and Indonesian exports and constrained blendstock availability are offset by steady Dar Blend flows and the continued erosion of VLSFO’s bunkering share.

- Neutral to moderately bearish NWE & USGC HSFO cracks amid spillover weakness from Asia. Yet, downside is limited by persistently low inventories and Egypt’s ongoing import demand.

- Neutral NWE VLSFO cracks from current levels as a supply-led bounce aligns with expectations following output shifts post-Med ECA rollout.

Trades of the Month

- The US rescinding licensing controls on ethane exports to China is bullish USGC ethane ratios to natural gas. However, resupplies of ethane won’t arrive in force until August, meaning alternative cracking feeds in China (naphtha and butane in particular) will remain supported through July as ethane crackers are forced to keep runs low or remain offline until next month

- The recent rally in NWE middle distillates stems largely from freight dislocations and a transatlantic arbitrage that remains shut — a situation we believe is temporary, with tanker economics poised to normalize. While cracks and timespreads have rebounded, we’d caution against chasing length here deeper into July, as easing freight rates, cargo arrivals, and Atlantic Basin length are likely to cap further upside.

LPG: C3 and C4 values to diverge, slowly normalise on positive US-China developments and cooling Middle East tensions

West of Suez

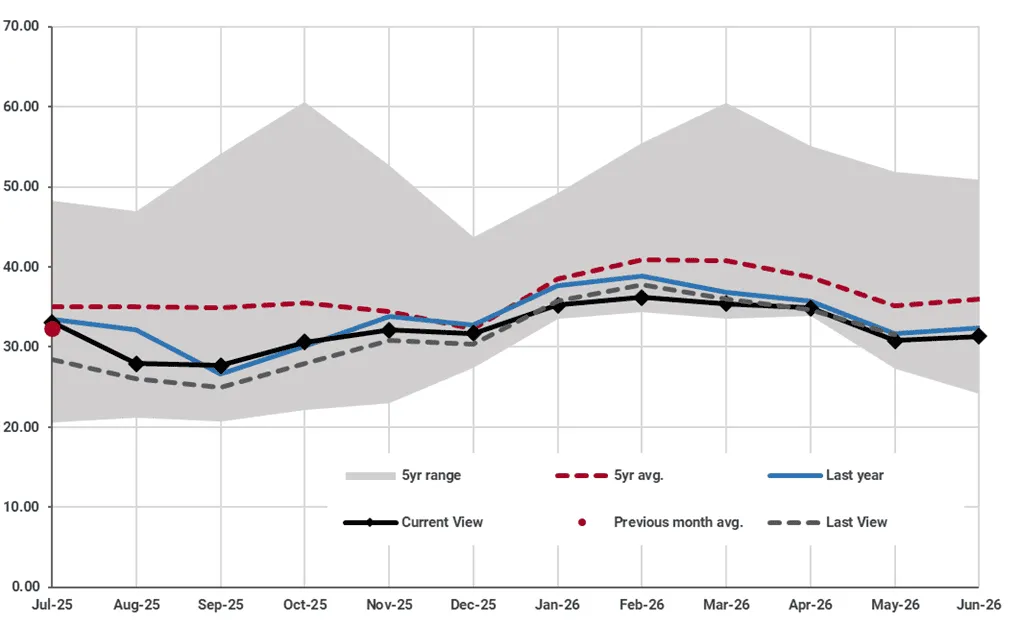

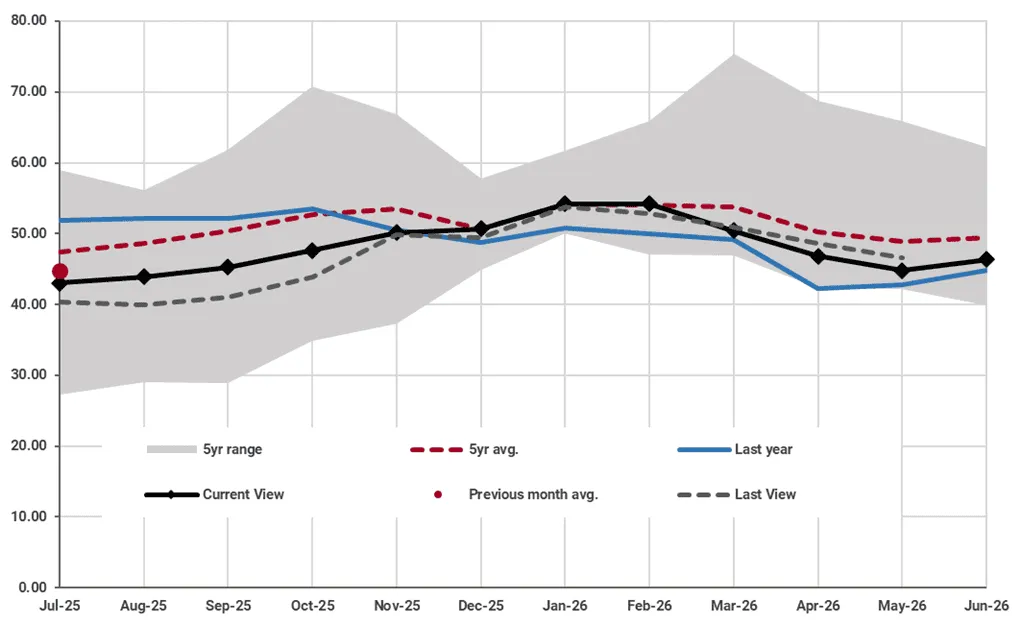

USGC propane values came under pressure in June due to sizeable stock builds linked to falling overseas propane demand (and rising butane), with Chinese buyers reluctant to meaningfully return to US barrels.

However, we have modestly increased our Mont Belvieu price forecast m/m for H2 2025, considering improving US-China trade negotiations and agreements which have cooled relations and allowed NGLs exports to begin slowly picking up once more.

USGC prices will be supported by the ramping up of propane sent outs at ET’s expanded terminal (estimated +125 kbd once it reaches capacity by end-Q3). As such, rising export demand will put a floor of support under ratios to crude as Chinese buying slowly moves back to US barrels through Q3. Nonetheless, we expect USGC propane values to remain below the five-year average on the back of ample field supply growth (y/y) and China’s 11% tariff on US-origin barrels keeping a lid on prices.

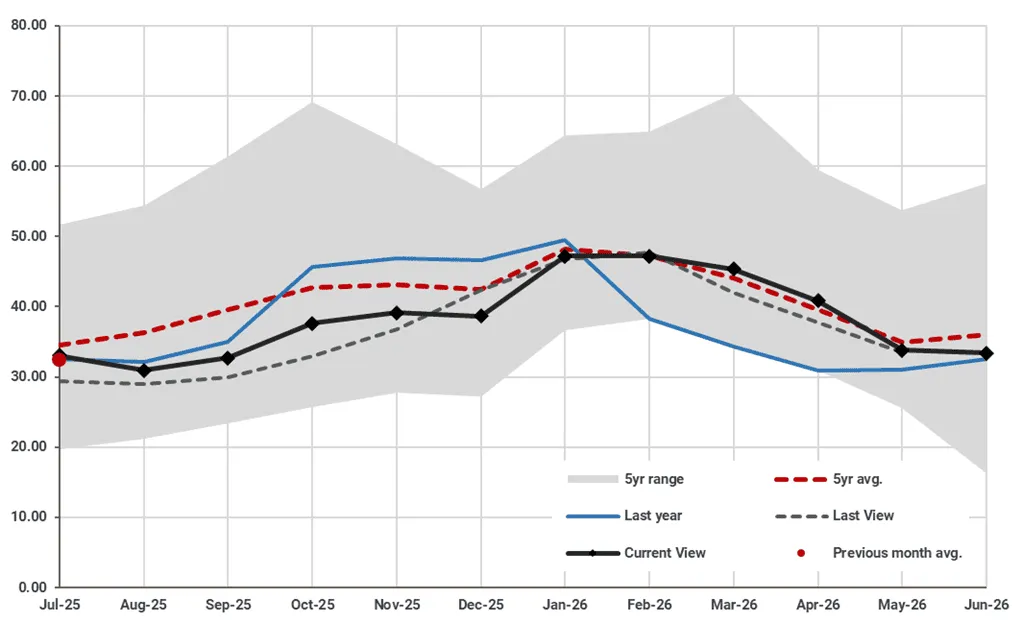

For butane, we also amended our USGC forecast modestly higher for H2 2025, mostly due to the recent bullishness in send outs amid the ongoing reshuffling of LPG flows with mixed cargoes more in demand from the US, and Middle Eastern barrels continuing to head to China in greater volumes. However, butane ratios have recently begun correcting lower with US-China trade negotiations progressing, as such we expect butane prices to move back in line with the five-year seasonal average by Q4 as butane export demand slowly wanes m/m through Q3 as flows normalise.

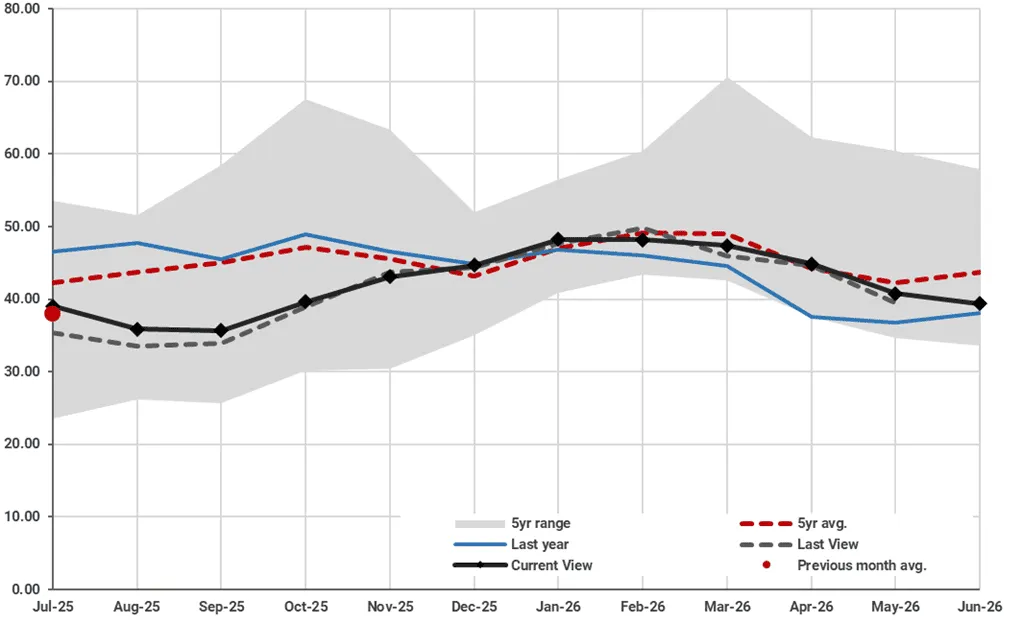

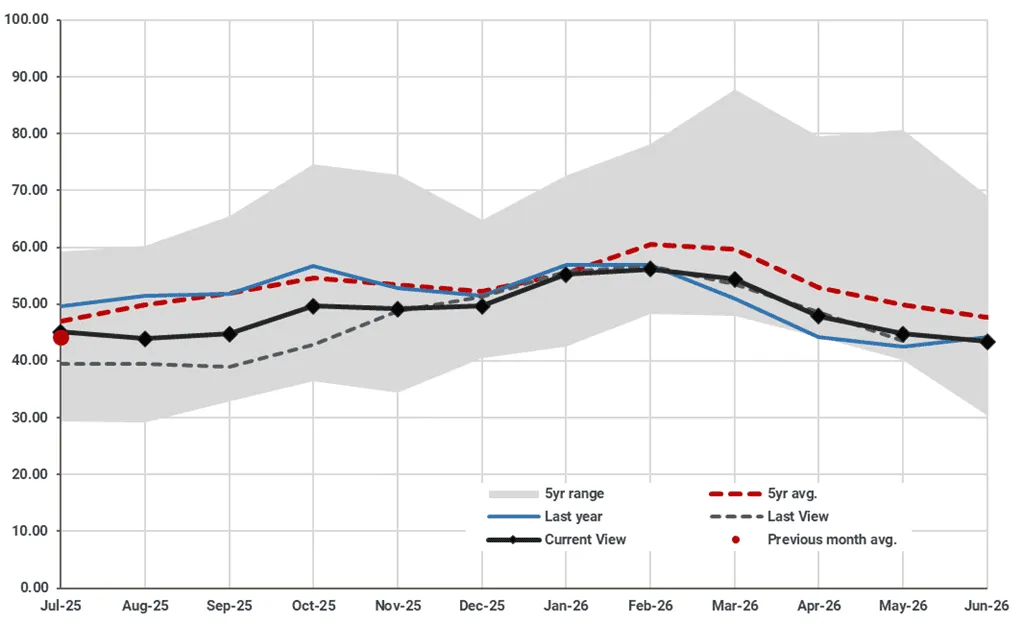

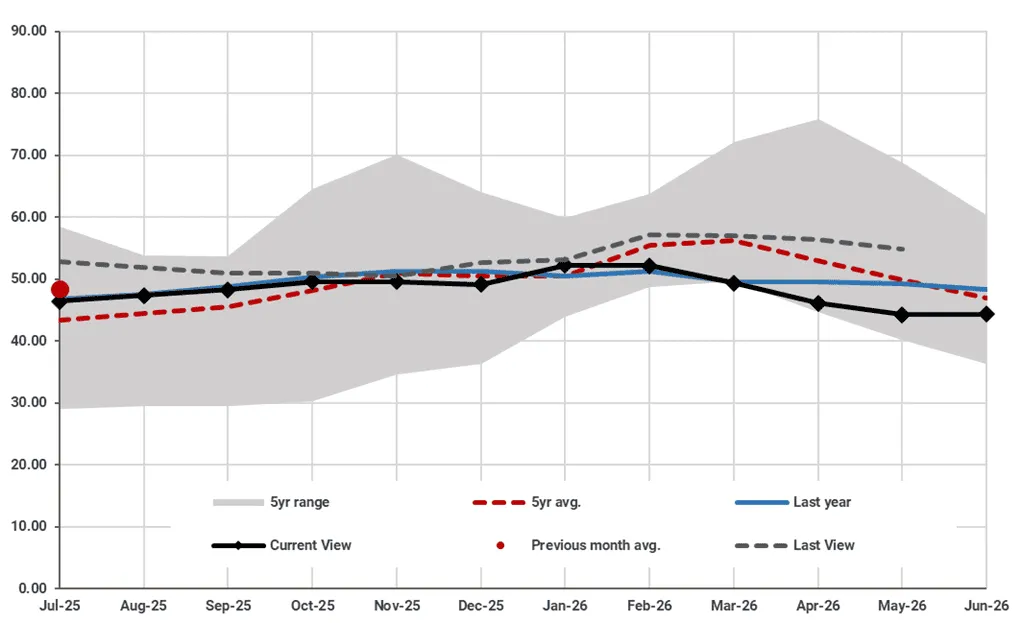

For Europe, more US cargoes aimed at the continent due to Chinese buyers only slowly moving back to US barrels will keep prices in check, especially with local supply lengthening post-North Sea gas plant and refinery maintenance. Dow’s closure of its Olefins No.3 flexi-cracker in June has helped reduce import requirements in NWE, but LPG will remain favoured over naphtha in the region, which will stop prices from falling to the bottom of the five-year range in Q3 and early Q4.

Propane Mt Belvieu ($/bbl)

Source: PVM Data Services (Vienna), Argus Media (historical data), Kpler (forecasts)

Propane NWE CFR ($/bbl)

Source: PVM Data Services (Vienna), Argus Media (historical data), Kpler (forecasts)

Butane Mt Belvieu ($/bbl)

Source: PVM Data Services (Vienna), Argus Media (historical data), Kpler (forecasts)

Butane NWE CFR ($/bbl)

Source: PVM Data Services (Vienna), Argus Media (historical data), Kpler (forecasts)

East of Suez

Conversely in the Middle East, conflict in the region and record propane exports to China buoyed values in the region through June, keeping them above the five-year average and year-ago levels.

However, in light of improving US-China relations and rising US export capacity, we have modestly reduced our CP propane forecast for H2 2025, as we expect Chinese buyers to slowly return to US barrels by end-Q3. Moreover, a small uptick in output (+0.5-1%) will add length to the region as OPEC unwinds production cuts and planned refinery outages taper off.

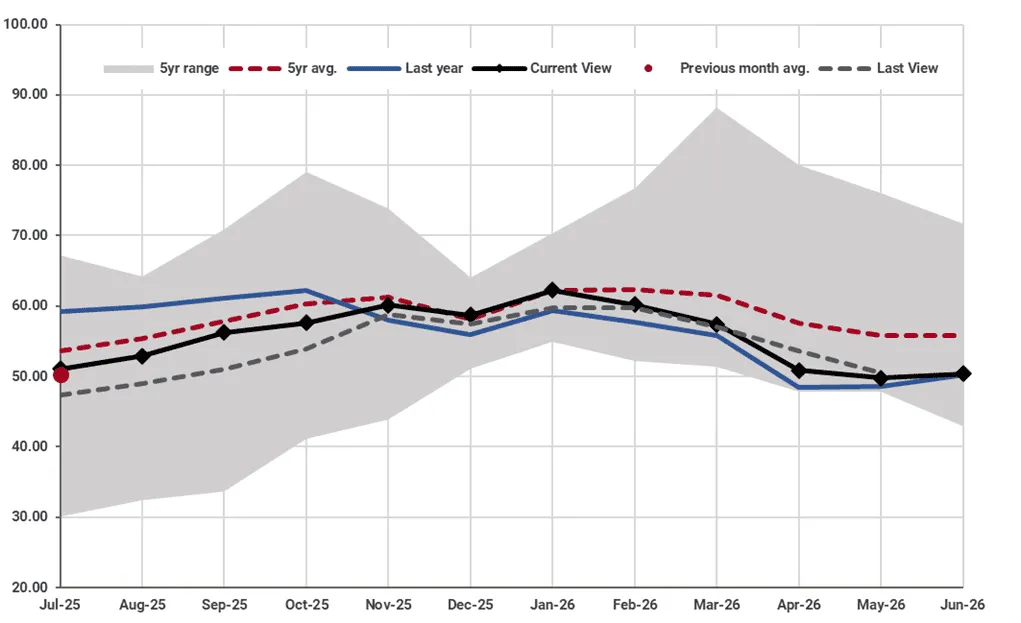

In the Far East, weak Chinese PDH margins and the retrofitting of another cracker (Wanhua No.1 1 mt/year) in June weighed on prices, with Chinese buyers having to pay a premium to secure non-US cargoes in May and June, pressuring petchem demand. Looking ahead, we have modestly increased our Far East propane price forecast through H2 2025. Indeed, Chinese PDH margins have improved on falling crude and rising domestic propylene prices in recent weeks, and margins should find a floor of support from increased US-cargo send outs through Q3 as terminal capacity expands. That said, growing structural length in China’s propylene market this year from alternative technology routes (cracking, FCC, C/MTO plants) will firmly cap PDH runs at around 75% or below going forward, ensuring Far East prices trade below year-ago levels and the five-year average until December.

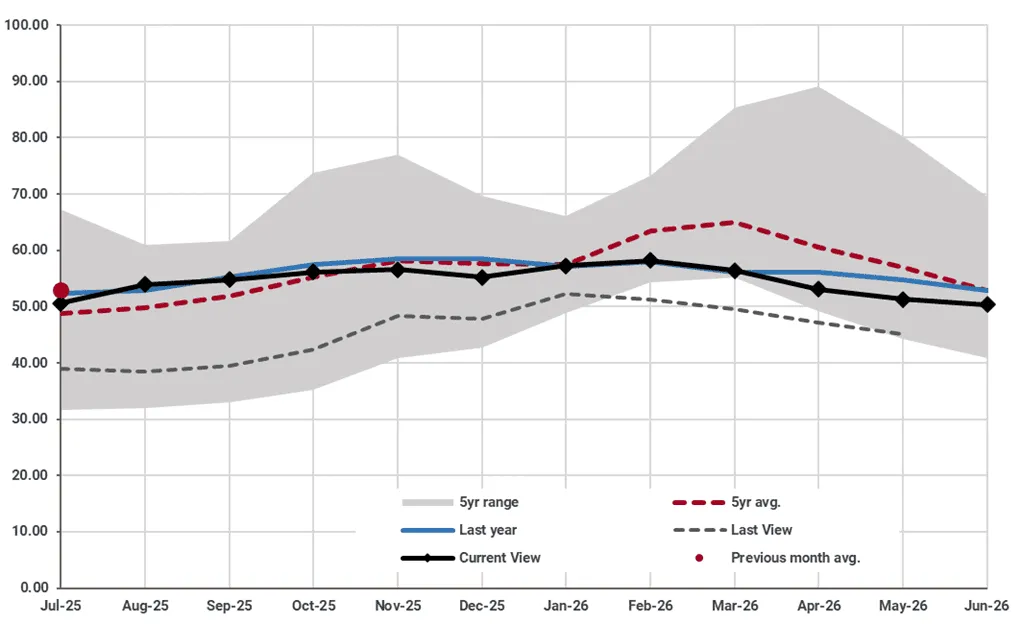

Meanwhile, we have moderately increased our Far East butane price forecasts for H2 2025, although they remain below year-ago and the five-year average. Indeed, butane prices in Asia have been weighed down by a growing glut in the Chinese market due to limitations in procuring fully laden propane cargoes from the region and therefore having to manage higher volumes of mixed cargoes. However, as we expect trade flows to slowly normalise through Q3, this will lead to the butane glut in China easing and prices moving back in line with the five-year average by November.

Propane Far East ($/bbl)

Source: PVM Data Services (Vienna), Argus Media (historical data), Kpler (forecasts)

Propane CP FOB AG ($/bbl)

Source: PVM Data Services (Vienna), Argus Media (historical data), Kpler (forecasts)

Butane Far East ($/bbl)

Source: PVM Data Services (Vienna), Argus Media (historical data), Kpler (forecasts)

Butane CP FOB AG ($/bbl)

Source: PVM Data Services (Vienna), Argus Media (historical data), Kpler (forecasts)

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. The full report is available within Insight and contains:

- Market & Trading Calls

- Trades of the Month

- LPG: C3 and C4 values to diverge, slowly normalise on positive US-China developments and cooling Middle East tensions

- Naphtha: E/W to continue to diverge through Q3 as crackers close in Europe, ramp up in Asia

- Gasoline: Outlook broadly unchanged

- Middle Distillates: Unviable transatlantic arb keeps NWE unbalanced

- Fuel Oil: HSFO Cracks Soften Across Regions, While Fundamentals Cap Downside

- Refinery Margins Forecast

Unbiased. Data-driven. Essential.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data