Refined products: Top 5 market drivers in 2026

This article was first posted on Kpler Insight on 7 January.

Global oil markets enter 2026 at a fragile inflection point, shaped by unresolved geopolitical risk, structural refining shifts, and a decisive rebalancing of liquids demand. While easing inventories and capacity additions offer tentative relief after a volatile 2025, sanctions enforcement, delayed mega-refinery deliveries, and rising conversion intensity continue to skew balances—particularly in middle distillates. At the same time, growth is increasingly led by NGLs and petrochemicals rather than transport fuels, with China accelerating its pivot away from gasoline and diesel. The coming year is less about headline capacity and more about optimization — where yield uplift, trade dislocation, and policy execution will determine whether markets transition toward stability or remain exposed to disruption.

1. Geopolitical risks remain centre stage

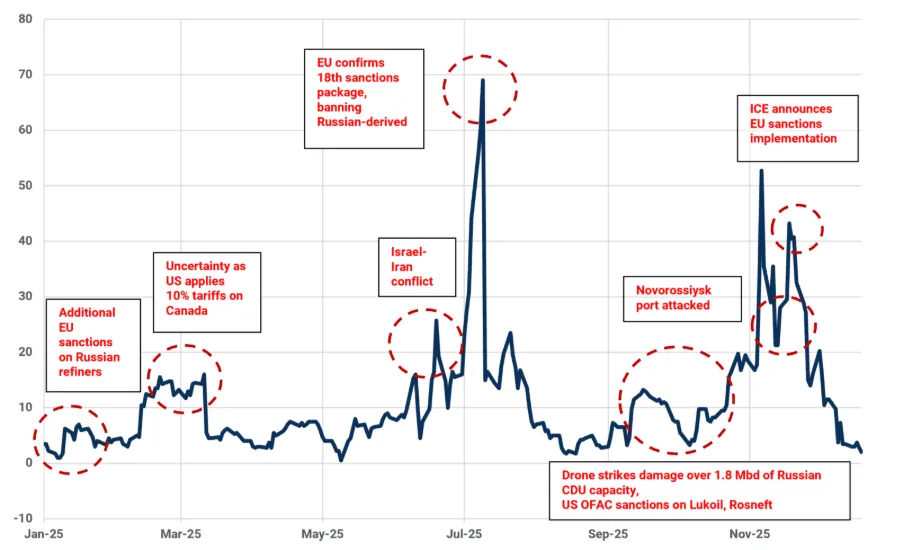

Middle distillate price action in 2025 was heavily shaped by geopolitics, and early 2026 looks set to be no different as the EU ban on oil products derived from Russian crude takes effect. Prices have recently eased on the back of looser balances, healthy stocks and ongoing Ukraine–Russia peace talks, but tangible progress remains uncertain and EU buy-in will be decisive. Assuming talks remain unresolved and EU sanctions are enforced, NWE gasoil importers will be forced to pay a premium for sanctions-compliant, traceable winter-spec ULSD, just as the USGC turnaround season begins.

Geopolitical risk also abounds in light ends, where US-China trade barriers continue to redirect US LPG to more butane-rich demand centres. Growing US propane production has struggled to find a home with exports to China set to remain low, leading to elevated stocks in the US which will continue through 2026 even assuming a more durable trade deal.

Naphtha has also been impacted on the geopolitical front as Ukrainian drone strikes hinder Russian output and increasing US-Venezuela tensions disrupt a typical outlet for US naphtha exports. We expect the elevated East/West spread to persist into 2026 as stronger demand in the East and waning cracking and blending demand in the West pulls swing barrels from the Med and the US.

Although gasoline has been less affected, there have been some spillovers, especially in the Med region, which is more exposed to both Russia and the Middle East. Any escalation of tensions could then inject bullish sentiment and overwrite fundamental dynamics, keeping cracks seasonally elevated.

Geopolitics is once again reshaping global fuel oil markets, with 2026 starting decisively following the swift capture of Venezuela’s President Maduro. The sudden re-routing of Venezuelan barrels toward the US has provided a clear boost to the Asian HSFO complex, while structurally lengthening US fuel oil balances at Asia’s expense. A potential Russia-Ukraine peace deal could also reshuffle exports from the world’s top fuel oil supplier, while a recovery in Suez Canal traffic following the halt in Houthi attacks would weigh on bunkering demand after rerouting around Africa had added roughly 500kt per month to global consumption.

ICE Gasoil M1/M2 spread excluding expiry days ($/t)

Source: Kpler using Marketview

2. 2026 Refining Outlook: Smarter Barrels

2025 has remained a tumultuous year for global refining, shaped by significant capacity closures. Around ~900kbd of capacity in the West of Suez was permanently removed from the system. This erosion of baseline capacity reduced operational flexibility and amplified the market impact of outages, keeping refined product balances tight and margins elevated through much of the year.

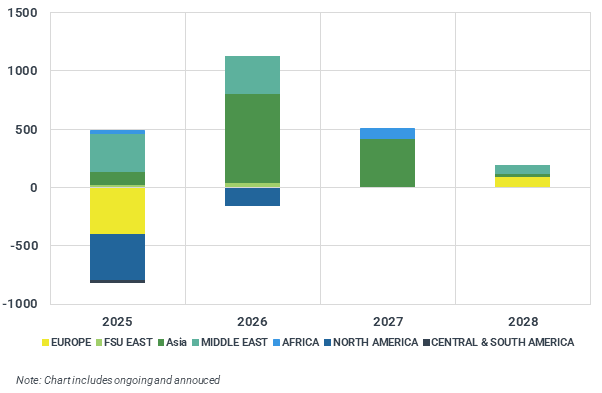

Looking into 2026, the supply backdrop begins to normalize, easing some of the extreme tightness and loss of flexibility experienced through 2025, with ~1Mbd of global refining capacity additions expected. Growth is heavily skewed toward Asia, led by India’s ~560kbd additions, followed by growth in China and the Middle East. However, the key change is not only the return of capacity, but also the quality of capacity being added.

Global Refinery capacity addition Net Change (kbd)

Source: Kpler

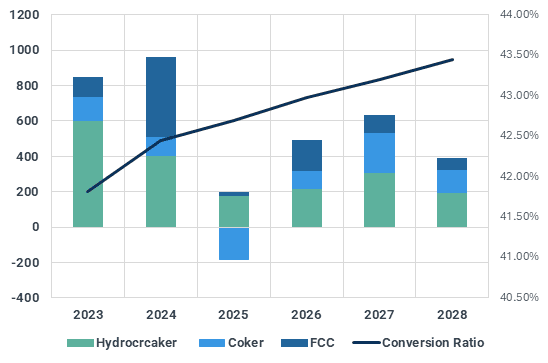

The defining theme of the next cycle is rising conversion intensity—driven not only by new upcoming refineries, but equally by the upgrading of existing assets. Refineries such as Sitra, Vizag, Balikpapan and Russian refineries highlight this trend, where investments in residue upgrading are materially lifting conversion capability.

This structural shift is reflected in the refinery conversion ratio (FCC, HCU and Coker capacities relative to primary capacity). From around 41.8% in 2023, it has climbed through 2025 and is projected to reach ~43.5% by end-2028.

Higher conversion ratios enable incremental clean product supply even without proportional growth in crude runs, marking a transition increasingly shaped by yield uplift in the coming years. However, this yield growth will not be uniform across products. While additional hydrocracking and residue upgrading capacity structurally supports gasoil and middle-distillate expansion, much of the upcoming FCC capacity is increasingly configured for petrochemical integration. As a result, FCC growth may not translate into meaningful gasoline yield gains, with new units optimized to maximize propylene and light olefins rather than conventional gasoline blending components.

These upgrades will also help keep both HSFO and VLSFO markets relatively supported into 2026 despite demand side pressures from the utility and bunkering sectors.

Net Global Conversion unit capacity change (kbd) vs Conversion ratio (%, rhs)

Source: Kpler

3. Mega-Refineries and the Atlantic Basin Reset: Will 2026 Be the Year of Delivery?

The Atlantic Basin enters 2026 at a structural inflection point. The permanent closure of nearly 800kbd of refining capacity across Europe and North America has materially tightened product balances, particularly for middle distillates. Against this backdrop, the market’s ability to rebalance increasingly depends on the operational normalization of two late-cycle mega-refineries— 650kbd Dangote and 340kbd Dos Bocas—both of which were designed to anchor regional supply but have so far underdelivered.

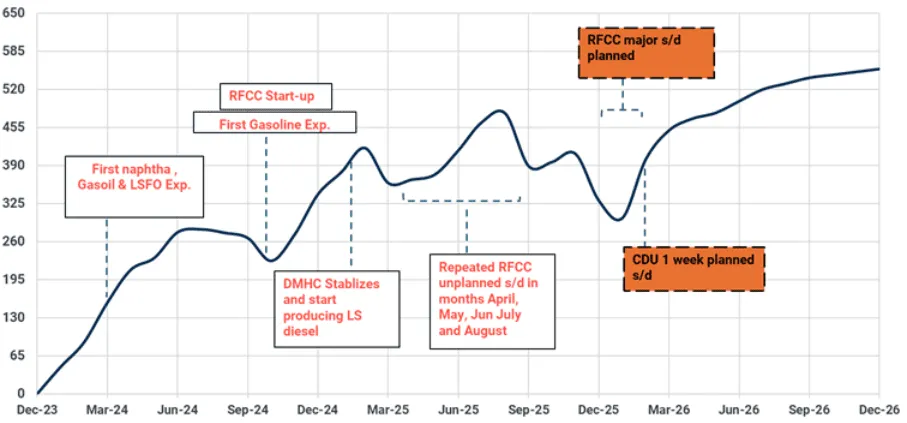

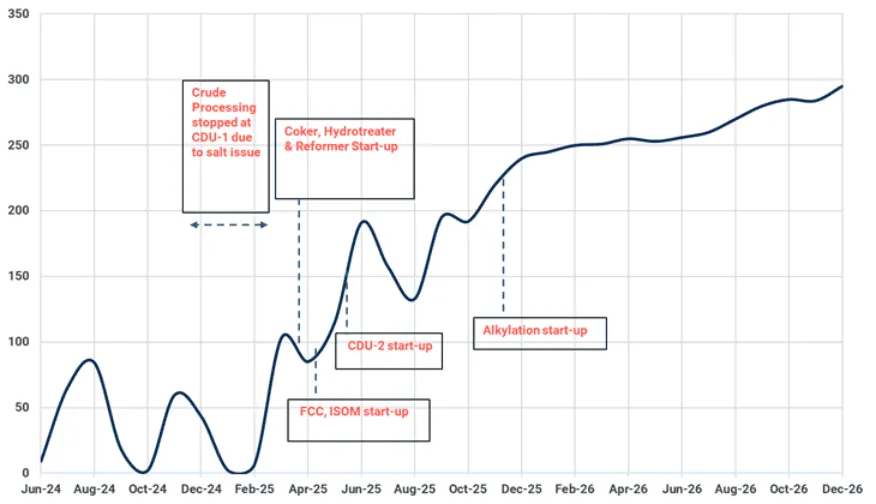

While distinct in geography, the two projects share a common narrative: scale alone has not translated into stability. Dangote has demonstrated meaningful progress by commissioning all secondary units and sustaining partial throughput to meet domestic demand. However, unresolved mechanical issues at the RFCC, its core conversion unit, have capped utilization at roughly 60–65%, preventing the refinery from exerting its intended influence on Atlantic Basin product flows. A major corrective shutdown initiated in mid-December, lasting 50–60 days, represents a pivotal inflection point. Successful execution would allow Dangote to move from marginal participation to structural relevance in clean product balances from mid-2026 adding ~300kbd of gasoline, ~150kbdd of gasoil, and ~140kbd of jet fuel at full utilization.

Dangote Refinery Ramp up chart Projected (kbd)

Source: Kpler

Dos Bocas reflects a similar “delayed impact” story. Since commissioning in 2024, operations have been disrupted by contamination events and power outages, limiting sustained runs. Yet recent operational and trade data increasingly point to stabilization. Declining Maya crude exports alongside improving gasoil balances suggest operational stabilization and a sustained ramp-up trajectory. At full utilization, the refinery is expected to add ~160kbd of gasoline and ~110kbd of gasoil, materially reshaping regional trade flows.

If both mega-refineries transition from intermittent operations to stable utilization, mid-2026 could mark a shift from structural tightness to a controlled imbalance, though the path remains narrow and time critical.

Dos Bocas Refinery Ramp up chart Projected (kbd)

Source: Kpler

4. NGLs take the lead in total liquids growth

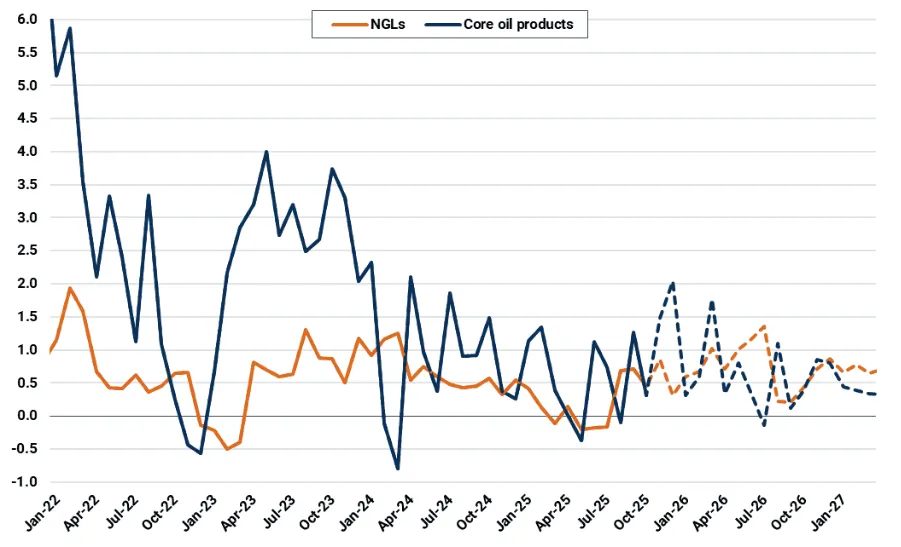

In 2026, NGLs are projected to account for 0.75Mbd of the expected 1.40Mbd total liquids demand growth, marking a shift that is now structural. Global NGLs demand continues to build momentum, supported by structural drivers that are set to persist. Petrochemicals remain the core engine of growth, underpinned by rising petrochemical and polymer demand alongside sustained urbanization and industrialization in emerging economies. This trend is reinforced by a new wave of NGLs-fed capacity additions: new PDH plants China, India, and Belgium are set to add a combined 3 Mt/year of propylene capacity in 2026, on paper, while ethane-fed crackers in the UAE, US, Russia and China ramp up sustaining robust demand growth (+8% y/y or 420kbd). At the same time, rising field output in Saudi Arabia, Qatar, the UAE, the US and Russia will ensure NGLs remain the most competitive petrochemical feedstock from Q2 2026 onward, meaning near-term rationalization pressure from base chemicals oversupply will continue to primarily affect naphtha-fed plants first (in South Korea, Japan, Singapore, the EU).

Core refined products vs. NGLs y/y demand growth (Mbd)

Source: Kpler

5. China transitions away from transportation fuels to petchems

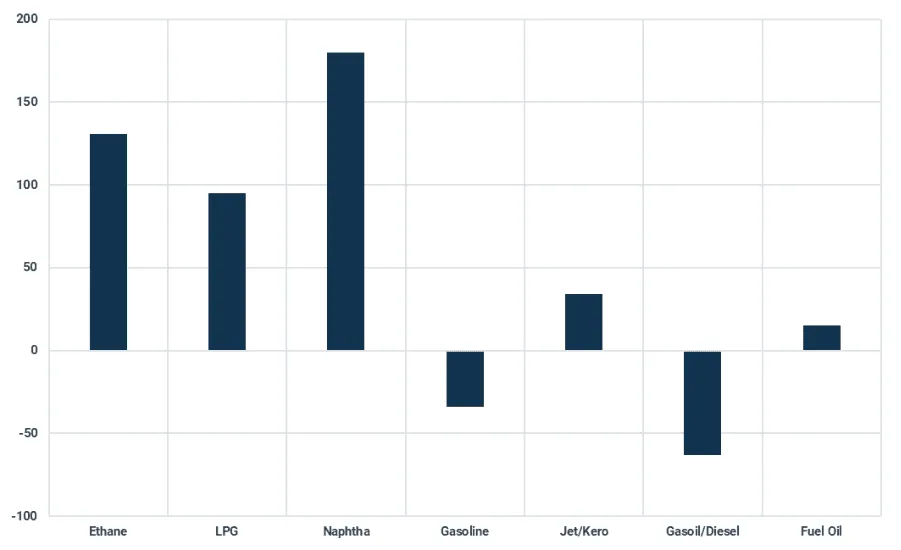

China’s total liquids demand is projected to increase by 360kbd in 2026, with all incremental growth coming from light ends (+410kbd y/y) as China’s petchem capacity expansion continues to reduce dependency on imports and boost export volumes into non-US markets. This strategy is already evident in the customs data, showing that China’s polymer imports have dropped 8% y/y and exports soared by 27% y/y during January-October 2025.

By contrast, transportation fuels remain structurally under pressure. Gasoline demand is forecast to decline by 34kbd (-1%) amid accelerating passenger-fleet electrification. Total EV (BEV and PHEV) sales are forecast to reach 16.1 million in 2026, lifting the total EV fleet to 50.5 million and displacing roughly 550kbd of gasoline demand.

In line with the ongoing transformation of the heavy-duty vehicle (HDV) fleet, gasoil/diesel demand is projected to contract by over 60kbd (-1.4%). While LNG-powered HDV sales are losing momentum, electric truck adoption remains strong, with sales expected to reach 200k units. Our HDV model suggests that LNG and electric trucks could displace approximately 480kbd of gasoil/diesel demand in 2026. Jet/kerosene is the sole transport fuel still posting growth (+34kbd), though momentum has clearly faded following the robust post-Covid rebound in 2023–24.

China oil demand growth by product in 2026 (kbd)

Source: Kpler

Beyond the Top 5: Why biofuels deserve attention in 2026

Despite delays in final legislative approvals, Europe is accelerating its HVO uptake through rising mandates, particularly in Germany and the Netherlands, pushing total renewable diesel demand higher by 2.5 Mt in 2026. In contrast, some new capacity additions are delayed, especially in France and Spain, limiting European production growth to just 1.4 Mt. As a result, the region will rely more heavily on imports. While Asian producers are scaling up, Europe will still require volumes from the US, even with countervailing duties in place. US demand remains subdued despite rising mandates, as RINs carry-out continues to grow, prompting American producers to maintain exports to Europe in order to keep their plants running.

High renewable diesel prices in Europe are also encouraging more refiners, particularly in Central and Eastern Europe, to adopt co-processing as a way to capitalize on margins and offset limited standalone HVO capacity.

Europe remains short on SAF, where the import replacement is more cost-competitive than for HVO due to the absence of import duties. As a result, SAF production margins are weaker, and producers are prioritising renewable diesel yields over aviation fuels.

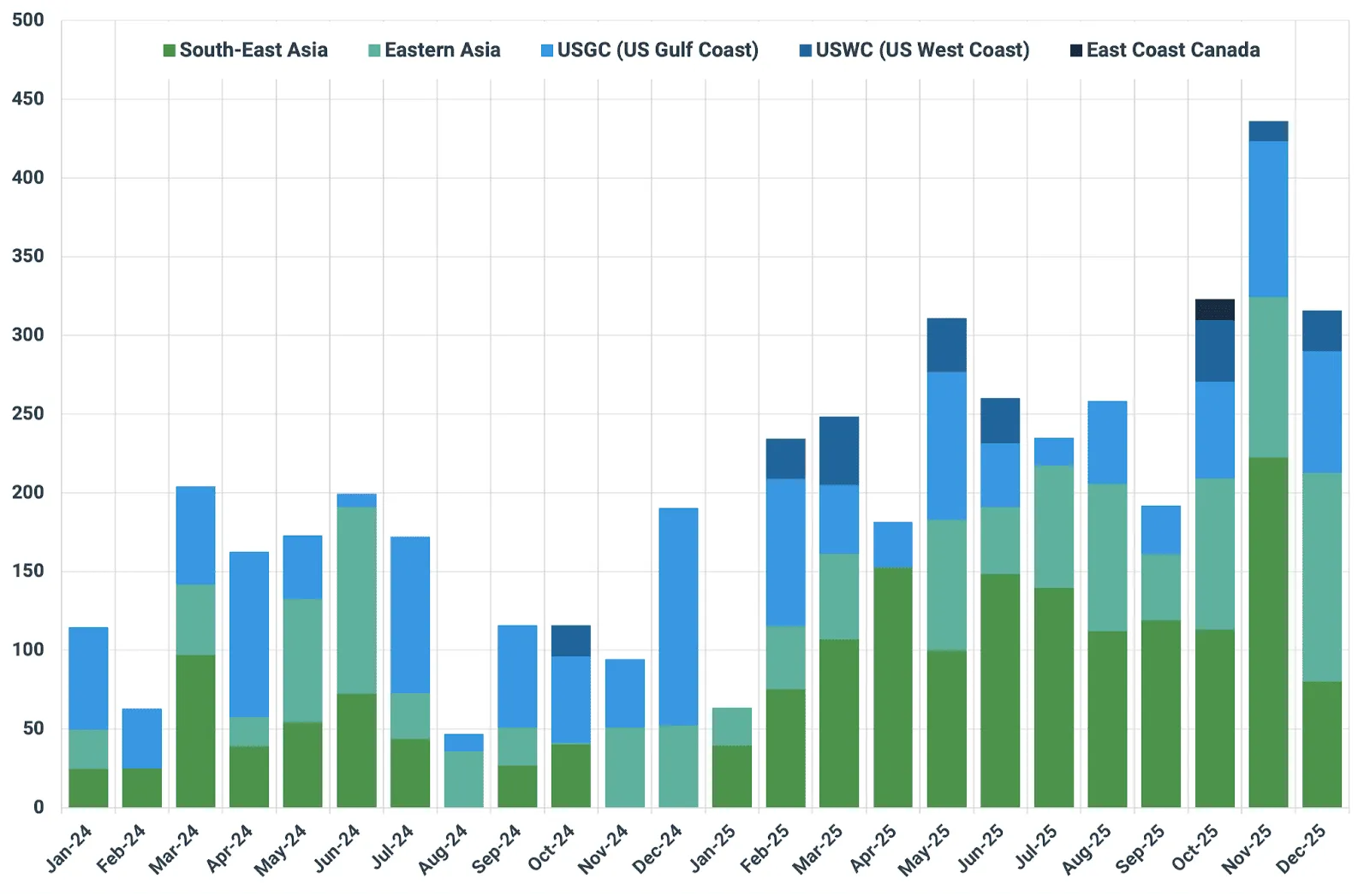

Europe monthly HVO, SAF imports by origin trading region (kt)

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

.jpg)