Russian coal faces headwinds as China demand plateaus

Russian coal producers now confront a fundamental dilemma: accept razor-thin margins to maintain volumes, or cut production to support prices. China, Russia’s main coal buyer, faces a steep drop in import demand in 2025, with limited prospects for another strong rebound in seaborne volumes in the coming years.

The declining import appetite in the Asia-Pacific basin is intensifying competition with low-cost Indonesian suppliers. Meanwhile, the anticipated end to the Russia-Ukraine conflict under the Trump presidency has not materialized, with EU and US sanctions remaining in place.

Russian producers maintained production through 2023-2024 by redirecting volumes from the EU, Morocco, and Japan toward China, India, and Turkey. This split the seaborne market into two distinct segments based on their stance against Russian coal. However, this strategy succeeded primarily because it coincided with steep Chinese demand growth during 2023-2024. That cushion is now gone.

The volume vs. price dilemma intensifies

Russian producers face a structural challenge regardless of sanctions. They can either maintain high output at low or negative margins, or scale back volumes to support prices. Neither option is attractive.

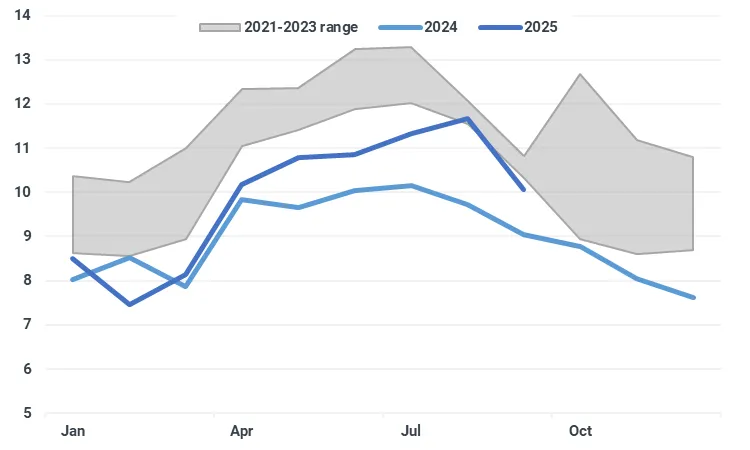

Russia thermal coal exports (Mt)

Source: Kpler

Russian thermal coal shipments to China are likely to remain stable even if sanctions are lifted. Kpler analysis shows producers have limited incentive to raise volumes further, since additional shipments would require deeper discounts that aren't feasible at current prices. The slowdown in Chinese demand has intensified competition with Indonesian suppliers, pressuring Russian margins due to higher logistics costs from Far Eastern ports.

Limited growth markets ahead

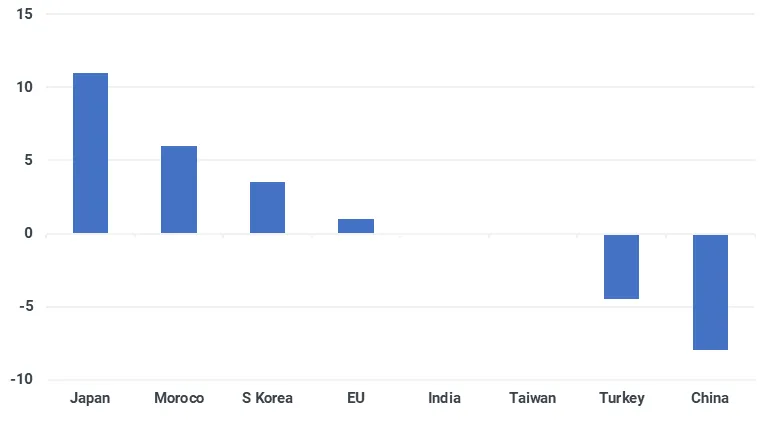

Estimated change in annual demand by country if sanctions on Russian coal are lifted (Mt)

Source: Kpler Insight

If sanctions were lifted, Russian coal would likely continue trading at a discount to other origins, with the price gap against other benchmarks narrowing. However, the total addressable market remains constrained:

Japan offers the most promising growth potential at around 10 Mt per year. Japan has almost completely diversified away from Russian supply, but given its strict quality requirements, Russian coal could regain meaningful share.

Morocco is the only notable Atlantic Basin growth market. Russian material benefits from freight and specification advantages, and US, South African, and Colombian suppliers would struggle to compete.

South Korea has limited upside, as Russian coal already retained market share. Korean utilities likely reached their informal quota after increasing Russian purchases this summer.

India saw growth primarily in metallurgical coal, while thermal coal shipments increased only marginally. Competing against low-cost Indonesian thermal coal remains challenging.

Turkey has reached saturation with no further upside. Russian suppliers must maintain discounts to retain share.

EU offers no comeback potential. European coal demand has declined structurally, with Germany expanding renewables and rising gas availability reducing coal's power mix share.

The path ahead

Russian coal producers face modest production cuts unless sanctions are lifted. Small and mid-sized producers may need to scale back as demand from key markets weakens. The long-term viability of Russian coal exports is now directly linked to consumption trends in China and India, both have the capability to reduce import reliance when it is not favourable to them.

The market has split into two camps, and even if sanctions are removed, it would redirect trade flows without raising total demand. The EU stays closed, leaving only Japan and Morocco with meaningful growth potential.

Get deeper insights into Russian coal trade flows and dry bulk markets

This analysis only scratches the surface. Kpler Dry Bulk Insight subscribers get access to:

- Real-time Russian coal export tracking by destination and vessel

- Granular market share analysis across thermal and metallurgical coal

- Forward-looking supply-demand balances for key importing nations

- Freight cost analysis and netback calculations by origin-destination pair

Want to stay ahead of coal market shifts and trade flow disruptions? Request a demo of Kpler Dry Bulk Insight today.

See why the most successful coal traders and shipping experts rely on Kpler.

See why the most successful traders and shipping experts use Kpler

Ready to navigate dry bulk shifts with precision and confidence?