The big APPEC takeaway

This APPEC has certainly not been short of heated discussion about the fair flat crude prices and the reasons behind the unexpected resilience that regional benchmarks have enjoyed since late August. In what follows, we outline some arguments which may help explain why flat prices remain undefeated in the face of evident crude stock builds.

This APPEC has certainly not been short of heated discussion about the fair flat crude prices and the reasons behind the unexpected resilience that regional benchmarks have enjoyed since late August. In what follows, we outline some arguments which may help explain why flat prices remain undefeated in the face of evident crude stock builds.

Geopolitical risk premium

While it is difficult to put a number on this metric, it is undoubtedly a factor we need to live with in the current macro environment. Unexpected Israeli strikes against Qatar as well as Ukrainian drone strikes (jeopardizing a sizeable chunk of Russia’s processing capacity as well as up to 1 Mbd of crude exporting capacity at Primorsk), have undoubtedly played their role in adding to the positive momentum in flat prices this month-to-date.

Admittedly, a couple of dollars per barrel premium to any assumption on top of what forecasting calculations seems to be the new normal for the foreseeable future, as neither of the above conflicts are nearing their conclusion.

This is probably one of the points also keeping forward markets on their toes, with the market generally wary of going short, in the face of unforeseen supply shocks, something which has admittedly been playing a major role in recent months.

Chinese stock building and buying activity

This is probably the shakiest argument that the crude bears like to point to, as, even though we capture a massive increase in Chinese crude inventories, nobody can really tell where the top of this stock building effort is. Moreover, given the challenges in obtaining Chinese data, it is possible that there are more underground caverns that are simply impossible to monitor.

On top of that, China’s recent indications that buying activity will continue unabated for another couple of months, implicitly shared by Chinese SOEs also point towards a tighter-than-expected physical crude balance. Moreover, OECD stocks have built already this summer, but the size of these builds remains limited in scope. And while US stock builds also have been captured by EIA data for August, only a couple of times when this has occurred historically, these remain more of an interesting observation of historical data, rather than an actual market mover.

Crack resilience

One of the central points around why flat prices remain elevated has been around strength in crack spreads, which as things stand, seems to be the new normal in refinery economics over the upcoming winter months.

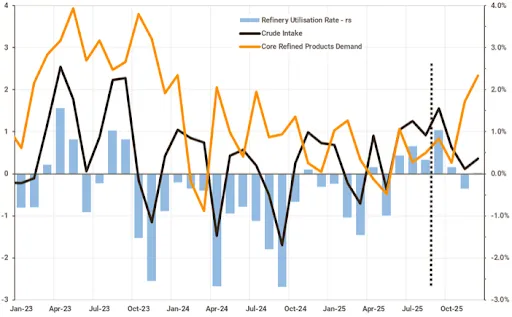

While in and of itself, this argument is still valid, the premise of crack strength hinges more on constrained supply (lost capacity, slow start-ups, maintenance season), rather than burgeoning demand. What we have observed so far this year is that demand, particularly in the middle of the barrel, the current engine of margin strength globally, has been far from encouraging (European manufacturing slowdown, Chinese LNG/BEV displacement, Indian reported demand at a mild decline y/y, US demand flat y/y at best, among other factors).

And while Q4 is set to see core demand growth registering a robust 1.45 Mbd y/y jump, this assumption needs to be tested by observed reported figures. More importantly, crude intake will almost certainly fail to keep up with demand growth (EU+US lost capacity, Dangote woes, currently expected until the end of the year, heavy turnarounds in Europe and Asia, according to our calculations based partially on IIR data, all pointing towards a slowdown in crude demand.

Indeed, we see crude intake rising by some 300-400 kbd y/y over Q4. There is a convincing counter argument to this point, that if margins are good, there is a possibility that marginal capacity creep could be used by some refiners to try and lock in these gains, before the end of turnaround season. According to our initial estimates, the scope of this incremental crude demand upside, however, is somewhat limited, due to capacity constraints and already announced turnarounds.

Still, in a scenario where refiners decide to max out on processing, we can imagine Q4 seeing some 200 kbd of additional crude intake demand in Europe, 150 kbd in the US and up to 150 kbd for the rest of the world, on top of already assumed crude intake, based on recently seen seasonal run rates and available capacity, less known repair works. A back-of-the-envelope calculation from the above shows that even under the optimistic capacity creep scenario, the gap between product supply and demand will remain wide over Q4.

VLCC rates jump

Meanwhile, VLCC rates are nearing annual highs, driven by bullish sentiment. MEG-China (TD3C) rates rallied by an additional $0.52/bbl to $2.70/bbl, fuelled by OPEC+ announcements and Saudi OSPs. While by itself this fact could not hold an explanation for lengthening crude balances, we believe it holds a key early indication of this happening, the extent of which will become clear in the coming weeks.

In short, we acknowledge that the oil glut has not yet convincingly made itself visible and there have been some compelling bullish arguments that probably are still at play when it comes to flat price dynamics. Indeed, the 'fair' flat price is probably around current levels over the next couple of weeks, which comes in a tad above our previous expectations.

That being said, while the downside is more limited to flat prices, probably a level in the low-60s is a reasonable bet over Q4, we also acknowledge the fact that even if there is a physical 'oil glut' making itself glaringly obvious to market observers, the blow to flat prices is to be cushioned by the above factors, among other things, with upside risks contingent more on headlines.

World: y/y change in crude intake, core refined products demand (Mbd; pp)

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Research & analysis driven by proprietary data