US pressure clouds Venezuelan crude exports to China, but spot supply remains ample

Heavy crude prices showed little reaction to the latest US seizure of a Venezuelan oil cargo so far, as the market waits to verify Trump’s threat of further tanker arrests, while ample supply on the water buys refiners time to seek alternatives.

Market & Trading Calls:

- Pessimistic on near-term Venezuelan crude exports to non-US destinations, as shipowners turn more cautious amid Washington’s threat of further tanker seizures.

- Neutral to slightly bullish on February-delivery Merey prices in China, as refiners are likely to gradually feel supply tightness as floating storage clears.

- Neutral on February and March TMX and Iraqi heavy crude prices, as teapot buying interest to substitute Venezuelan crude is expected to remain limited due to high prices.

Venezuelan crude exports face a potential slowdown after the US seized a sanctioned oil tanker off the coast of Venezuela on December 10, loaded with nearly 1.85 mb of heavy Merey crude. Kpler data shows that three tankers have lifted crude from the Latin American nation since the seizure, with two set to ship to the US and the remaining one yet to reveal its destination. At the time of writing, some 19 laden tankers carrying a combined total of around 11 mb of Venezuelan crude are sitting in Venezuelan or nearby waters, while seven tankers in ballast are idling in the region.

Reuters reported last week, citing sources, that Washington is preparing to intercept more ships carrying Venezuelan oil, a move that may have prompted cargo owners to stay put and discouraged shipowners from entering Venezuela to haul crude. Crude loadings totalled 678 kbd last week, little changed from the first week of December.

Venezuela shipped 750–775 kbd of crude in October and November, of which around 20% was bound for the US under a license granted to Chevron, while most of the remainder was likely to end up in China. While the US threat is also likely to deter vessels from delivering Russian naphtha to Venezuela, this—coupled with the outage of three crude upgraders with a combined nameplate capacity of 500 kbd —could further threaten 150–200 kbd of heavy crude production from the November level of around 800 kbd. That said, current data and recent reports suggest that shipments to the US remain largely unaffected, while up to 600 kbd of Venezuelan supply to non-US markets could face disruption.

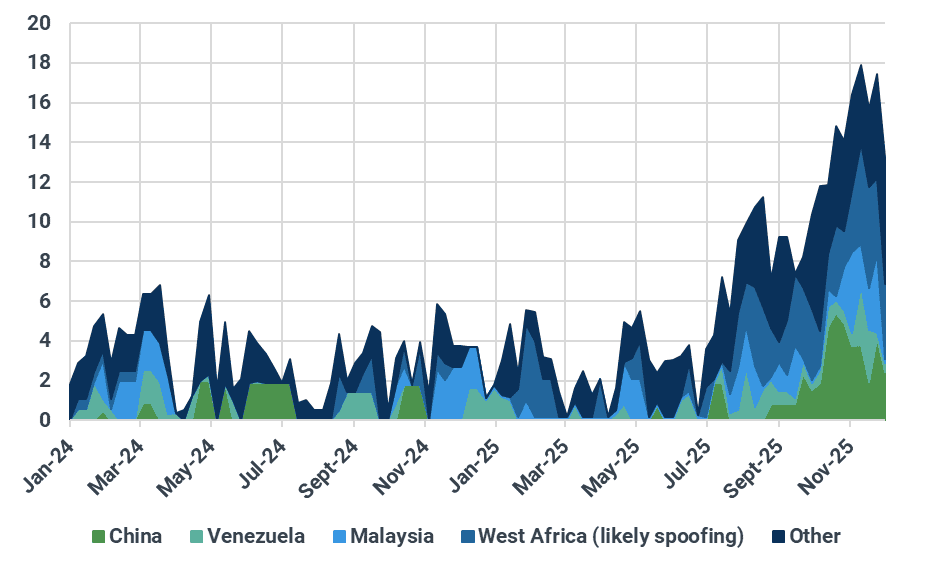

As the single largest buyer of Venezuelan heavy crude, China’s teapot refiners stand to be the biggest losers from the escalating tensions between Washington and Caracas. However, teapots do not appear to be panicking over potential supply disruptions—at least not yet—with January-arrival Merey still assessed at around -$13 to -$13.5/bbl versus ICE Brent on a delivered China basis, according to market sources. A key factor capping Merey prices is the large volume of floating storage. Kpler data shows that around 16.4 mb of Venezuelan crude is sitting on the water, while total Venezuelan crude in transit—including floating storage—stands near 72 mb, the highest level since May 2022. This suggests that China is unlikely to face a supply crunch until February, or even March.

Venezuelan crude oil floating storage by current loaction, mb

Source: Kpler

That said, teapot refiners are exploring potential alternatives to Venezuelan heavy crude, as mounting US pressure on the Maduro government makes exports to China increasingly uncertain. Canada’s TMX grades and Iraq’s Basrah Heavy and Qaiyarah are potential alternatives due to their similar quality, but significantly higher costs could make such purchases unsustainable. The high-TAN TMX grade AWB is currently assessed at -$2 to -$3/bbl versus ICE Brent on a dap China basis, down from -$1.2/bbl a month ago, but still remains more than $10/bbl more expensive than Merey, according to Argus Media data.

Abundant supplies of steeply discounted Iranian and Russian crude could also attract additional buying interest from teapots should Venezuelan shipments decline. However, despite comparable pricing, Russian grades are generally too light for refiners that primarily use Merey to produce bitumen, as is the case for medium sour Iranian crude. Iran Heavy and even heavier grades such as Soroosh and Pars are more suitable substitutes for Merey, but these heavy barrels account for only around 30% of total Iranian supply and are unlikely to fully cover the gap left by Venezuelan cargoes.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Kpler Insight: Get the analysis that matters