Weak fundamentals and growing bearish sentiment after Arctic LNG 2 cargo docked in China

Market & trading calls

European TTF front-month price outlook: Bearish as lower temperatures, strong renewable generation, and higher LNG imports are expected to outweigh the bullishness stemming from the start of the maintenance season in Norway. The news of Arctic LNG 2 cargo docking in China will likely weigh down on prices in the coming days. An upside price risk to the outlook stems from any delay or unplanned event extending Norwegian maintenance.

Asian LNG front-month price outlook: Slightly bearish as high LNG inventories, steady supply, and weak regional demand outweigh increased gas burn in China and higher LNG consumption in India.

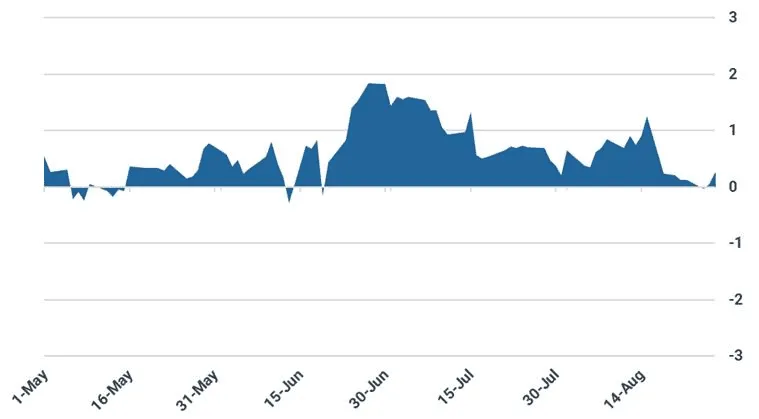

Asian LNG – TTF spread outlook: Slightly widened as we expect a larger drop in TTF prices relative to Asian LNG prices. The spread slightly widened last week to $0.25/MMBtu on 27 August.

US Henry Hub front-month price outlook: Steady with bearish inventories, production, and demand capping upside as September contract rolls off.

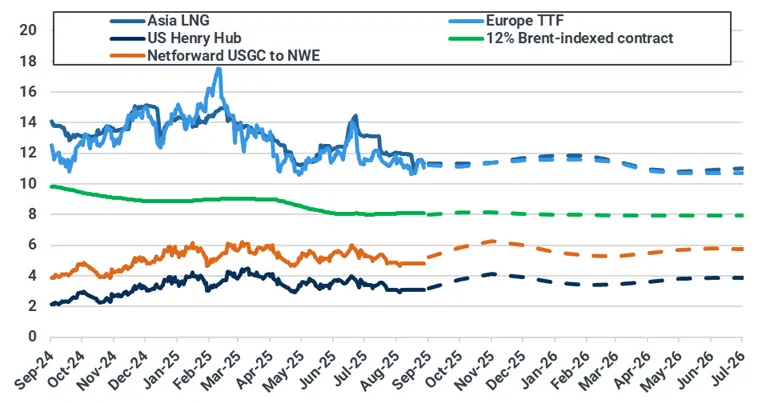

Key natural gas and LNG front-month prices ($/MMBtu)

Source: ICE, NYMEX, Spark Commodities. Brent-indexed price represents 12% slope of 90-day moving average of Brent contract. Netforward USGC to NWE calculation is 115% Henry Hub contract plus shipping and regasification costs into Gate (Spark Commodities).

Asian LNG-TTF front-month spread ($/MMBtu)

Source: ICE, Kpler Insight

LNG Supply: First Russian Arctic LNG 2 cargo docks in China; steady outlook capped by Nigeria Bonny maintenance

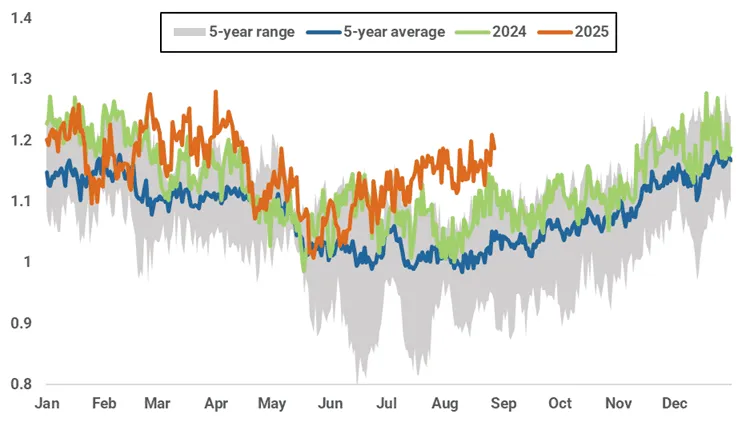

Global LNG exports climbed to 8.51 mt last week, the highest since early April, driven by stronger US and Australian flows. Kpler Insight anticipates steady supply this upcoming week, with maintenance at Nigeria’s 22 mtpa Bonny plant likely capping gains. Kpler continues to monitor signs of buying interest for sanctioned Russian Arctic LNG 2 cargoes, with a first laden vessel docking at the Beihai port in China on 28 August.

Global LNG exports (mt, 10-day moving average)

Source: Kpler

In the Atlantic basin, the sanctioned , carrying LNG from Russia’s Arctic LNG 2 project, docked at Beihai, China, on 28 August — the first loaded vessel from the project to call at an import terminal.Arctic Mulan The ship berthed at PipeChina’s 6 mtpa Guangxi regas facility. At least five more Arctic LNG 2 cargoes are en route to Asia, following the 15 August meeting between Presidents Trump and Putin. Arctic Mulan’s arrival could be the first sign of softer enforcement of US sanctions imposed since November 2023.

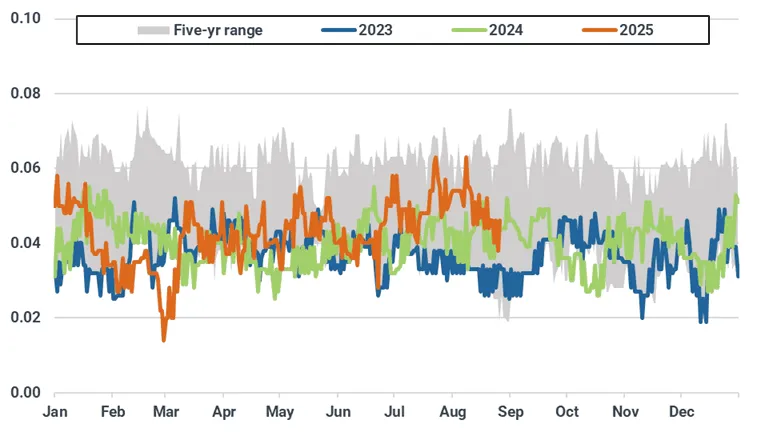

Meanwhile, Nigeria’s 22 mtpa Bonny LNG plant is likely undertaking planned maintenance, with 10-day moving averages consistently reducing over the past few weeks (see chart). The drop in exports impacts supply to both Asia and Europe alike, with 53% of exports headed to Asia and 35% to Europe in August. Maintenance is also ongoing at Russia’s 17.4 mtpa Yamal plant.

Nigeria’s LNG exports (mt, 10-day moving average)

Source: Kpler

In the Pacific basin, maintenance at Australia’s 9 mtpa Ichthys plant runs through mid-October. Indonesia’s 3.8 mtpa Tangguh train 3 is offline for planned work from 23–29 August, curbing supply. Meanwhile, the UAE’s 5.7 mtpa Das Island plant continues to underperform due to maintenance.

The full report is available within Insight and contains:

- Europe: Lower temperatures, above-average renewable generation, and higher LNG imports to weigh on TTF prices despite Norwegian maintenance

- Asia: Prices to slightly lower next week as high inventories and steady Pacific supply outweigh modest demand gains

- US: Henry Hub edges up as October takes front-month, but weak fundamentals cap prices below $3.00/MMBtu

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Research & analysis driven by proprietary data